On May 19, 2026, FASB issued Accounting Standards Update 2026-02, Environmental Credits and Environmental Credit Obligations, establishing the first authoritative U.S. GAAP guidance specifically addressing how entities account for carbon allowances, renewable energy credits, renewable identification numbers, and other transferable instruments used to meet emissions compliance obligations or voluntary sustainability commitments.

Before this ASU, no explicit standard governed environmental credits. Entities applied analogies to Topic 330 (Inventory), Subtopic 350-30 (General Intangibles), or Topic 450 (Contingencies), producing substantial diversity in how the same instruments appeared on financial statements across companies in the same industry and the same regulatory program. Two companies subject to identical cap-and-trade obligations could show materially different balance sheets under pre-ASU practice.

ASU 2026-02 creates new Topic 818, Environmental Credits and Environmental Credit Obligations, codified in the FASB Accounting Standards Codification. It applies to a broad range of entities and instruments and takes effect for public business entities for annual and interim periods beginning after December 15, 2027.

This post maps every substantive requirement of the new standard in the sequence your technical accounting team will encounter them.

What Is FASB ASU 2026-02 and What Does It Change?

ASU 2026-02 is FASB's first authoritative accounting standard for environmental credits and the obligations associated with regulatory compliance programs that require settlements in those credits. It creates Topic 818 in the FASB Accounting Standards Codification and provides recognition, measurement, presentation, and disclosure requirements for all entities that generate, purchase, receive, or hold environmental credits, or that have regulatory compliance obligations settleable with environmental credits.

Prior to this ASU, U.S. GAAP contained no specific guidance on environmental credits. According to the FASB's project page and the ASU's stated basis for conclusions, entities were applying analogies to three different existing standards depending on how they characterised the credit internally. Some applied Topic 330 (Inventory). Others applied Subtopic 350-30 (General Intangibles). Others applied Topic 450 (Contingencies). That three-way divergence produced fundamentally different financial statement presentations for entities holding economically identical instruments.

The EITF had previously attempted to address emissions allowances in 2003 with Issue No. 03-14, but it never finalised that guidance. The gap persisted for over twenty years.

ASU 2026-02 closes that gap. The four things it establishes that did not exist before are: a definition of what an environmental credit is for GAAP purposes, a definition of what an environmental credit obligation (ECO) is, a recognition and measurement model for both assets and liabilities, and enhanced disclosure requirements that apply regardless of whether an entity has recognised credits as assets.

Who Must Apply ASU 2026-02?

The scope of Topic 818 is broader than carbon compliance programs alone. The standard applies to any entity that meets one or more of the following conditions.

It generates environmental credits through verified environmental projects such as reforestation, methane capture, or renewable energy production. It purchases or receives environmental credits, whether for compliance with a regulatory program or for voluntary purposes such as net-zero or carbon-neutral commitments. It holds transferable environmental credits, including emissions allowances originating from domestic or global cap-and-trade programs, Renewable Identification Numbers (RINs) originating from the U.S. Renewable Fuel Standard, and renewable energy certificates (RECs). It has a regulatory compliance obligation arising from existing or enacted laws or regulations that may be settled with environmental credits.

FASB provided non-exhaustive examples of instruments subject to Topic 818 in the ASU: emissions allowances from cap-and-trade programs, RINs from the Renewable Fuel Standard, and other regulatory compliance credits. The standard applies to both mandatory compliance participants and voluntary buyers of credits for sustainability goal purposes.

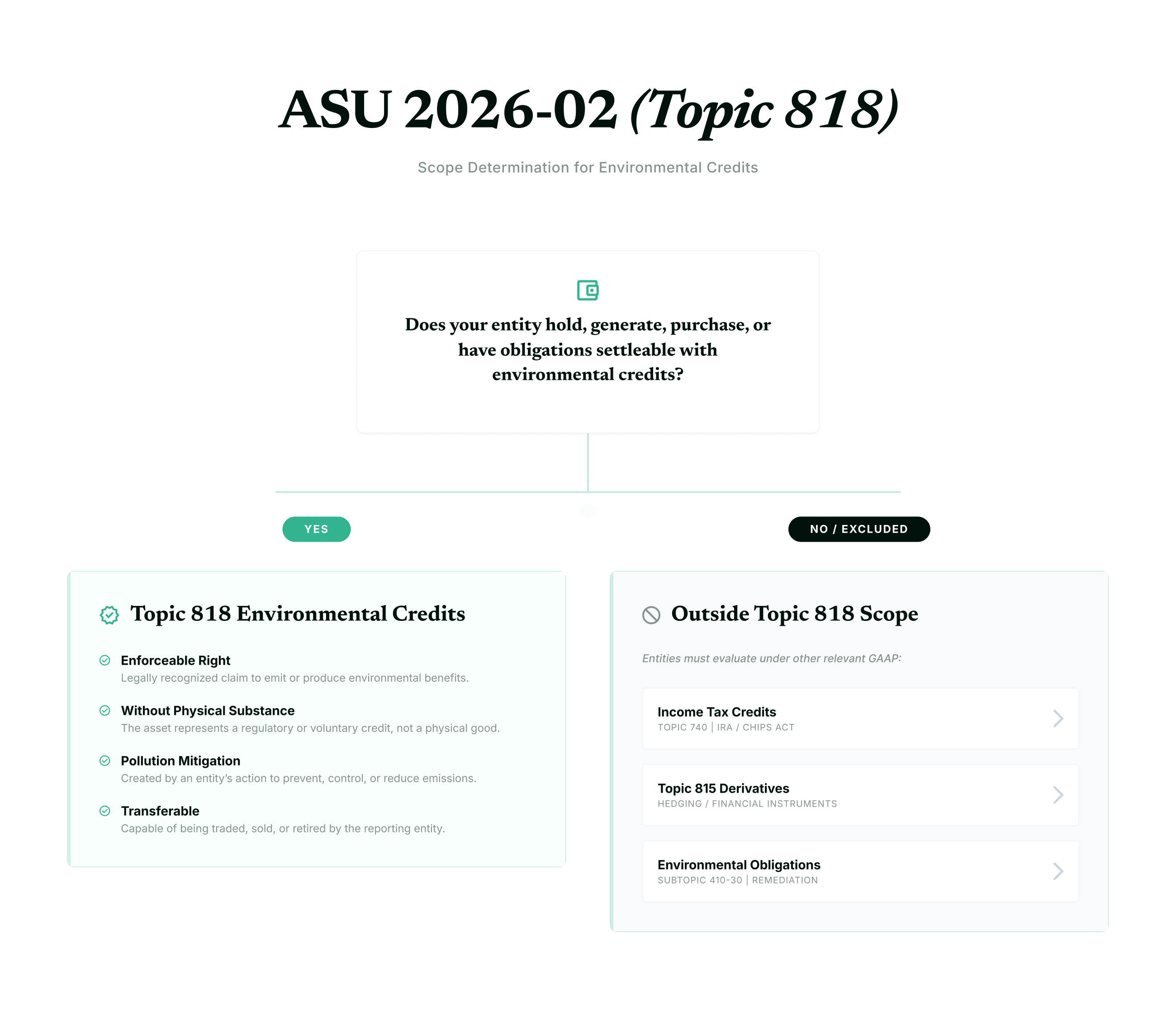

What is not in scope. Income tax credits, including clean energy credits under the Inflation Reduction Act and the OBBBA, are not environmental credits under Topic 818 and are excluded from its scope. Environmental obligations addressed by Subtopic 410-30 (Environmental Obligations) are also not ECOs for Topic 818 purposes. Environmental credits and obligations accounted for under Topic 815 (Derivatives) remain within that standard. Broker-dealers and investment companies that account for environmental credits under Topic 940 or Topic 946 continue to follow the applicable industry guidance, which typically requires fair value measurement.

How Are Environmental Credits Defined Under Topic 818?

Topic 818 provides a specific definition of an environmental credit that limits the standard's scope to instruments meeting all of the following attributes simultaneously.

An environmental credit must be an enforceable right. The holder must have a legally enforceable claim to the credit that can be asserted against the issuer or the regulatory authority.

It must be without physical substance. Physical commodities such as fuel or timber are not environmental credits. The instrument itself must be intangible.

It must be represented to mitigate pollution. The credit must be issued within a framework designed to prevent, control, reduce, or remove emissions or other pollution. Credits issued for purposes unrelated to pollution mitigation are outside scope.

It must be transferable in an exchange transaction. Non-transferable instruments, such as internal renewable energy tracking records that cannot be sold or transferred to third parties, are not environmental credits under Topic 818. If an instrument cannot be transferred in an exchange transaction, its cost is expensed as incurred rather than recognised as an asset.

An environmental credit obligation (ECO) is separately defined as a regulatory compliance obligation arising from existing or enacted laws, statutes, or ordinances represented to prevent, control, reduce, or remove emissions or other pollution that may be settled with environmental credits. The ECO definition is narrower than the credit definition: it covers only regulatory program obligations, not voluntary commitments. An entity that voluntarily commits to net-zero emissions does not have an ECO. It may hold environmental credits for voluntary purposes, but those credits are accounted for differently from compliance credits.

How Are Environmental Credits Recognised as Assets?

Recognition of an environmental credit as an asset under Topic 818 depends on a single probability test applied at the time the entity first acquires or generates the credit, and reassessed at each subsequent reporting date.

An environmental credit is recognised as an asset when it is probable that the entity will either use it to settle an environmental credit obligation or transfer it in an exchange transaction.

If neither condition is probable at the time of acquisition or generation, the cost of the credit is expensed as incurred. A credit that does not meet the recognition criteria at acquisition cannot be recognised as an asset later, even if conditions change to make settlement or transfer probable. Under ASU 2026-02, previously derecognised or never-recognised credits cannot subsequently be brought onto the balance sheet.

This probability-based recognition model creates a distinction between two categories of credits that govern all subsequent accounting.

Compliance environmental credits are credits that are probable of being used to settle an ECO. These are recognised as assets and subsequently measured at cost with no subsequent remeasurement. They are not tested for impairment while classified as compliance credits.

Noncompliance environmental credits are credits that are probable of being transferred in an exchange transaction but are not probable of being used to settle an ECO. These are recognised as assets at cost and subsequently tested for impairment at each reporting date. Impairment is recognised when the carrying amount of the credit exceeds its fair value. An accounting policy election is available to remeasure noncompliance credits at fair value at each reporting period rather than applying cost-less-impairment.

The classification between compliance and noncompliance is reassessed at each reporting date. If a credit originally classified as a noncompliance credit subsequently becomes probable of being used to settle an ECO, it is reclassified to compliance and the impairment testing ceases. Before reclassification, impairment must be assessed one final time at the reclassification date.

How Are Environmental Credits Initially and Subsequently Measured?

Initial measurement. Environmental credits are initially measured at cost. The definition of cost depends on how the credit was obtained.

Credits purchased in a market transaction are measured at their acquisition cost, which follows the asset acquisition guidance in Subtopic 805-50 unless another Topic specifically addresses the measurement.

Credits received as grants from a regulator or its designees, or internally generated by the entity, are initially measured at the transaction costs incurred to obtain them, which may be zero if no such costs exist. A company that receives emissions allowances from a government allocation programme without paying for them records those allowances at zero on day one.

Credits obtained in a transaction initially measured under another Topic follow the measurement requirements of that other Topic.

Subsequent measurement of compliance credits. Compliance environmental credits are measured at cost with no subsequent remeasurement. They are not amortised and are not tested for impairment while classified as compliance credits. The carrying amount is the recognised cost at initial measurement.

Subsequent measurement of noncompliance credits. Noncompliance environmental credits are subsequently measured at cost less impairment, unless the entity has elected to remeasure them at fair value. The impairment test is applied at each reporting date. If the carrying amount exceeds fair value, an impairment loss is recognised in earnings. Impairment is not reversed. If the entity elects the fair value option, changes in fair value are recognised in earnings at each period end.

Costing methods. Entities may use average cost, first-in first-out (FIFO), or specific identification to measure their portfolio of similar environmental credits. The method must be applied consistently to all similar credits.

How Are Environmental Credit Obligations Recognised and Measured?

Environmental credit obligation liabilities are recognised based on the events that have occurred by the reporting date, not based on projections of future emissions.

Recognition trigger. An ECO liability is recognised when events occurring on or before the reporting date have given rise to a regulatory compliance obligation that may be settled with environmental credits. For a cap-and-trade programme, this means that actual emissions occurring before the reporting date create the obligation. The liability represents the obligation as if the reporting date were the end of the compliance period.

This is a significant departure from the prior practice of recognising an ECO only when the entity's cumulative emissions exceeded its credit inventory. Under Topic 818, any compliance shortfall as of the reporting date triggers liability recognition, regardless of whether the compliance period end date has passed.

Initial and subsequent measurement. The ECO liability is measured in two parts.

The funded portion of the liability is measured at the carrying amount of the compliance environmental credits the entity holds and intends to use to settle the obligation. Because compliance credits are measured at cost, this means the funded portion of the liability equals the carrying amount of those credits.

The unfunded portion of the liability is measured at the fair value of the environmental credits the entity would need to purchase to satisfy the remaining obligation as of the reporting date. Fair value for this purpose is the price the entity would pay in an orderly transaction in the relevant credit market.

The practical effect of this two-part measurement model is that funded and unfunded portions of the same ECO liability are measured on different bases. The funded portion moves with the cost basis of the credits on hand. The unfunded portion moves with the market price of credits. Changes in both portions are recognised in earnings.

Subsequent measurement uses the same method as initial measurement at each balance sheet date. No fair value option is available for ECO liabilities. The fair value option in Topic 825 does not apply to ECO liabilities under Topic 818.

Gross presentation required. Topic 818 prohibits netting environmental credit assets against ECO liabilities on the balance sheet. Both the asset and the liability must be presented on a gross basis. This eliminates the net-presentation approach that some entities had been using under prior practice.

Derecognition. ECO liabilities are derecognised when the obligation to the regulatory authority is satisfied through a transfer of credits, cash, or both, following the derecognition guidance in ASC 405-20. Any gain or loss on derecognition is presented in the same income statement line as the initial and subsequent measurement of the ECO.

What Disclosures Does Topic 818 Require?

ASU 2026-02 requires separate quantitative and qualitative disclosures for environmental credits and ECOs that are significant to the entity. The disclosure requirements address both the financial statement amounts and the broader context of the entity's participation in environmental credit programmes.

For environmental credits, entities must disclose how credits are obtained (purchased, granted, internally generated), how they are used (compliance settlement, voluntary offset, traded), the volume and carrying amount of credits held at period end by type, any impairment losses recognised during the period, and the fair value of noncompliance credits if the cost-less-impairment method is used. Entities that elect to remeasure noncompliance credits at fair value must disclose the inputs and assumptions used in the fair value measurement.

For environmental credit obligations, entities must disclose the nature and terms of the regulatory compliance programme giving rise to the ECO, the total obligation at period end separated into funded and unfunded portions, the carrying amount of compliance credits designated to settle the funded portion, the fair value of credits needed to settle the unfunded portion, and the amount of any gains or losses recognised on derecognition during the period.

Qualitative disclosures must describe the entity's involvement in environmental credit programmes, the regulatory or voluntary framework under which obligations arise, and any significant judgements made in applying the recognition and measurement requirements.

The disclosure requirements apply regardless of whether the entity is a mandatory compliance participant or a voluntary buyer. An entity that purchases carbon credits for voluntary net-zero purposes and does not have a regulatory ECO is still subject to the enhanced disclosure requirements for its credit holdings.

How Does the Transition to Topic 818 Work?

ASU 2026-02 is applied using a modified retrospective transition approach. Entities record a cumulative-effect adjustment to the opening balance of retained earnings (or net assets for nonprofits) in the period of adoption. Prior periods are not restated.

Effective dates. Public business entities must apply Topic 818 for annual reporting periods (and interim periods within those annual periods) beginning after December 15, 2027. For a calendar-year public company, this means Topic 818 applies beginning with the January 1, 2028 fiscal year, with the first affected Form 10-K filed in early 2029. All other entities have an effective date of December 15, 2028 (one year later).

Early adoption. Early adoption is permitted for both interim and annual periods for which financial statements have not yet been issued or made available for issuance. An entity that early adopts in an interim period must apply the standard from the beginning of the fiscal year containing that interim period.

Transition measurement. On the adoption date, entities measure previously held environmental credits and ECO liabilities as follows.

Noncompliance environmental credits are measured at their carrying amount immediately before initial application of Topic 818. This maintains continuity with the prior accounting basis.

Compliance environmental credits are measured at the lesser of their historical carryover basis or their fair value on the adoption date. This prevents entities from carrying compliance credits at historical costs that significantly exceed their current market value at adoption.

ECO liabilities are measured under the Topic 818 methodology as of the adoption date, applying the funded and unfunded portion framework.

An entity is permitted to continue including the costs of credits that were previously capitalised as part of an asset's cost basis (for example, renewable energy credits capitalised into a power purchase arrangement) without adjusting those amounts on adoption.

SAB 74 disclosure implications. Public business entities that have not adopted Topic 818 before it becomes effective are required to disclose the expected effects of adoption in their periodic filings under SAB 74 (codified as SAB Topic 11.M / ASC 250-10-S99-5). Given the effective date of December 15, 2027 for public companies and the significance of the accounting change for entities with material credit portfolios or compliance obligations, SAB 74 disclosures addressing Topic 818 should appear in 10-K and 10-Q filings beginning in 2026 and becoming more detailed as the adoption date approaches.

How Does Topic 818 Interact With Other Accounting Standards?

Several existing standards intersect with Topic 818 in ways that require specific attention.

Derivatives (Topic 815). Environmental credits and ECOs accounted for as derivatives under Topic 815 remain subject to that standard. Topic 818 does not displace derivatives accounting. An entity that enters into a forward contract to purchase carbon allowances would continue to account for the derivative under Topic 815 unless and until it takes physical delivery of the allowances, at which point the asset enters the Topic 818 scope. The ASU clarifies that ECO liabilities accounted for under Topic 818 are not in the scope of Topic 815.

Environmental Obligations (Subtopic 410-30). Obligations within the scope of Subtopic 410-30, which addresses environmental remediation liabilities, are not ECOs. A company facing an environmental cleanup obligation does not account for that obligation under Topic 818. The two standards address different regulatory frameworks.

Industry-specific guidance (Topics 940 and 946). Broker-dealers and investment companies that account for environmental credits under Topic 940 (Financial Services — Brokers and Dealers) or Topic 946 (Financial Services Investment Companies) continue to apply the applicable industry guidance. Topic 818 is not intended to override existing industry-specific GAAP that typically requires fair value measurement for inventory or investment assets.

Fair value option (Topic 825). The fair value option available under Topic 825 does not apply to ECO liabilities. An entity cannot elect to measure its ECO liabilities at fair value through the Topic 825 mechanism.

Asset acquisitions (Subtopic 805-50). Credits obtained in a transaction are initially measured following the asset acquisition guidance in Subtopic 805-50 unless another Topic specifically governs the measurement.

Frequently Asked Questions

What is FASB ASU 2026-02 and what does it do?

ASU 2026-02, issued May 19, 2026, establishes the first authoritative U.S. GAAP standard for environmental credits and environmental credit obligations through new Topic 818 in the FASB Accounting Standards Codification. It provides recognition, measurement, presentation, and disclosure requirements for all entities that generate, purchase, receive, or hold environmental credits, or that have regulatory compliance obligations settleable with environmental credits. It ends the previous practice of accounting by analogy to Topic 330 (Inventory), Subtopic 350-30 (Intangibles), or Topic 450 (Contingencies), which produced significant diversity in practice.

What is the effective date of ASU 2026-02?

For public business entities, ASU 2026-02 is effective for annual and interim reporting periods beginning after December 15, 2027 — the fiscal year beginning January 1, 2028 for calendar-year filers, with the first affected annual 10-K due in early 2029. For all other entities, the effective date is December 15, 2028. Early adoption is permitted.

What types of environmental credits are in scope of Topic 818?

Topic 818 covers enforceable, transferable, intangible rights represented to mitigate pollution that may be transferred in an exchange transaction. Confirmed examples include emissions allowances from cap-and-trade programmes, Renewable Identification Numbers (RINs) from the U.S. Renewable Fuel Standard, and renewable energy certificates (RECs). Excluded from scope are income tax credits (including IRA and OBBBA clean energy credits), environmental obligations under Subtopic 410-30, derivatives under Topic 815, and instruments accounted for under industry-specific guidance in Topics 940 and 946.

What is the difference between a compliance environmental credit and a noncompliance environmental credit?

A compliance environmental credit is probable of being used to settle an environmental credit obligation (an ECO). It is measured at cost with no subsequent remeasurement and is not tested for impairment while classified as a compliance credit. A noncompliance environmental credit is probable of being transferred in an exchange transaction but not probable of being used to settle an ECO. It is measured at cost less impairment, or at fair value if the entity elects that option, and impairment is assessed at each reporting date.

How is an environmental credit obligation (ECO) liability measured?

An ECO liability is measured in two parts. The funded portion equals the carrying amount of compliance credits the entity holds and expects to use to settle the obligation. The unfunded portion is measured at the fair value of the credits the entity would need to purchase to settle the remaining obligation as of the reporting date. Assets and liabilities must be presented gross on the balance sheet. The fair value option under Topic 825 is not available for ECO liabilities.

What does Topic 818 require for SAB 74 disclosures before adoption?

Public business entities that have not yet adopted Topic 818 are required to disclose the expected effects of adoption in their SEC filings under SAB 74 (SAB Topic 11.M / ASC 250-10-S99-5). For entities with material environmental credit portfolios or significant compliance obligations, these disclosures should begin appearing in 2026 filings and become more quantitative as the December 15, 2027 effective date approaches. The disclosure should address the nature of the entity's environmental credit activities, the accounting model expected to be applied, and the estimated financial statement impact if it can be reasonably estimated.

Key Takeaways

- FASB issued ASU 2026-02 on May 19, 2026, establishing new Topic 818 as the first authoritative U.S. GAAP standard for environmental credits and environmental credit obligations. It ends twenty years of accounting by analogy.

- Topic 818 applies to all entities that generate, purchase, receive, or hold environmental credits, or that have regulatory compliance obligations settleable with those credits. Scope covers cap-and-trade allowances, RINs, RECs, and other qualifying instruments. Income tax credits are excluded.

- Environmental credits are recognised as assets only when it is probable they will settle an ECO or be transferred in an exchange transaction. Credits that do not meet this test are expensed as incurred and cannot be subsequently recognised as assets.

- Compliance credits (probable of settling an ECO) are measured at cost with no subsequent remeasurement or impairment. Noncompliance credits (probable of transfer, not ECO settlement) are measured at cost less impairment, with an option to elect fair value remeasurement.

- ECO liabilities are measured in two parts: the funded portion at the carrying amount of compliance credits on hand, and the unfunded portion at fair value of credits needed to settle the remaining obligation. Gross presentation is required. Netting is prohibited.

- The effective date is December 15, 2027 for public business entities and December 15, 2028 for all other entities. Modified retrospective transition applies. SAB 74 disclosures addressing Topic 818 should begin appearing in public company filings in 2026.