The SEC's 2024 climate-related disclosure rule occupies an unusual regulatory position as of May 2026. The rule was validly adopted through notice-and-comment rulemaking in March 2024. It was voluntarily stayed by the SEC in April 2024 pending litigation. The SEC voted in March 2025 to end iats defense of the rule in court. The Eighth Circuit ordered the case held in abeyance in September 2025. And on May 4, 2026, the SEC submitted a proposed rescission rule to the Office of Information and Regulatory Affairs (OIRA) for review the first formal step in a notice-and-comment process to eliminate the rule.

The rule is simultaneously on the books, unenforceable, and formally headed toward rescission. Nothing like this has appeared in the SEC's regulatory framework in recent memory.

For disclosure teams, the question this creates is specific and technically demanding: what does SAB 74 the SEC's standing requirement to disclose the effects of recently adopted but not yet effective accounting and regulatory standards require when the standard being adopted is a rule the SEC itself is trying to undo? This post answers that question precisely.

What Is the Current Status of the SEC Climate Disclosure Rule?

The SEC's climate-related disclosure rule, Release No. 33-11275, was adopted on March 6, 2024, after three years of development and over 24,000 public comments. It required public companies to disclose climate-related risks, the financial impacts of severe weather events, and for some companies, greenhouse gas emissions, in their periodic filings and registration statements.

The compliance timeline was phased. Large accelerated filers were to provide climate-related financial disclosures beginning with their fiscal year 2025 annual reports (filed in early 2026). Accelerated filers were to follow one year later. Smaller reporting companies, emerging growth companies, and non-accelerated filers were to follow in 2027.

Before any company filed under the rule, it was stayed. The SEC voluntarily stayed the rule's compliance deadlines in April 2024 pending judicial review in the consolidated Eighth Circuit litigation. In March 2025, the SEC voted to end its defense of the rule in the pending litigation. Several months later, the Eighth Circuit held the case in abeyance, effectively pausing the proceedings until the SEC either rescinded or resumed defending the rule.

As of May 2026, according to Goodwin Procter's analysis of the OIRA submission, the SEC submitted a proposed rulemaking titled "Rescission of Climate-Related Disclosure Rules" to OIRA on May 4, 2026. This is the first formal step in the notice-and-comment process required to rescind the rule. The public cannot yet see the substance of the proposed rescission rule only that it has been submitted for OIRA review. After OIRA review, the SEC must publish the proposed rescission for public comment, receive and respond to those comments, and publish a final rescission rule before the 2024 rule is formally eliminated.

According to the D&O Diary's analysis of the rescission trajectory, in a May 7, 2026, letter to the Eighth Circuit, the SEC confirmed it "does not intend to renew its defense of the Rules" and had submitted the rescission proposal for review. The rule appears headed for formal rescission, but the APA-mandated process takes time. The rule remains on the books in its current form while the rescission process proceeds.

For disclosure teams, this creates the central drafting challenge of the 2026 cycle: a rule that was adopted, that has a defined compliance timeline, and that requires planning and systems investment but that may never actually take effect must still be addressed in SAB 74 disclosures.

What Is SAB 74 and When Does It Apply?

SAB 74 is Staff Accounting Bulletin No. 74, formally titled "Disclosure of the Impact That Recently Issued Accounting Standards Will Have on the Financial Statements of the Registrant When Adopted in a Future Period." It is codified as SAB Topic 11.M and incorporated into the Accounting Standards Codification at ASC 250-10-S99-5.

SAB 74 was issued in 1987 and has been applied consistently through every major accounting standard transition since: ASC 606 (revenue recognition), ASC 842 (leases), ASC 326 (credit losses), and numerous others. Its purpose is to ensure that financial statement users receive advance notice of the impact that a recently issued but not yet effective standard will have on a company's financial statements, while there is still time to factor that information into investment and voting decisions.

Under SAB 74, when a recently issued accounting standard or SEC rule is not yet effective, registrants must disclose in both their MD&A and their financial statement footnotes:

- A brief description of the standard or rule and its required adoption date

- The date the company plans to adopt, if earlier than required

- The methods of adoption allowed and the method the company expects to use, if determined

- A discussion of the expected impact on the financial statements, unless not known or reasonably estimable in which case a statement to that effect may be made, along with qualitative information about the likely significance of the impact

- Any other significant matters expected to result from adoption, such as changes to debt covenants, business practice changes, or significant new disclosure requirements

The SEC's Office of the Chief Accountant has consistently reinforced that SAB 74 disclosures should not be boilerplate. According to the SEC's published speech on implementing new GAAP standards, the SEC staff expects SAB 74 disclosures to become more robust and quantitative as the adoption date approaches, and expects them to reflect the actual state of the company's implementation progress. A company that has made no progress in preparing for the standard should not file a SAB 74 disclosure that suggests otherwise.

SAB 74 is most commonly associated with FASB accounting standard updates. But its scope is not limited to FASB standards. According to Deloitte's DART guidance on SAB Topic 11.M, SAB 74 covers the disclosure obligations when "a new accounting standard has been issued but is not yet effective." SEC rules that impose new financial statement or disclosure obligations can trigger the same pre-adoption disclosure obligation where the rule's requirements have not yet taken effect but the compliance date is defined.

Does SAB 74 Apply to an SEC Rule That Has Been Stayed?

This is the most technically complex question in the 2026 climate disclosure drafting environment, and it does not have a simple yes-or-no answer. The answer depends on the specific rule's status and the company's assessment of whether adoption is probable.

The general principle. SAB 74 requires pre-adoption disclosure when a standard has been "recently issued." The 2024 climate rule was validly issued through the APA-required notice-and-comment process. Its issuance is not in doubt. What is uncertain is whether it will take effect. SAB 74 does not expressly address what happens when an issued standard is subject to a stay, litigation, or a rescission proceeding.

The analytical framework. According to PwC's Viewpoint guidance on SAB 74, SAB 74 applies when a standard has been issued. The stay does not rescind the rule. The OIRA submission does not rescind the rule. The rule is on the books, with defined compliance dates, and companies are required to assess its impact. The question is not whether SAB 74 disclosure is required but rather what that disclosure should say given the deep uncertainty about whether the rule will ever take effect.

The practitioner consensus. Law firms and accounting firms advising public companies in 2025 and 2026 have generally taken the position that SAB 74-style disclosure remains appropriate for the climate rule despite the stay. As the Harvard Law Forum's analysis of the 2025 annual reporting season notes, although the climate disclosure rules are not currently operative, public companies must continue to consider whether climate-related disclosures are required. This is consistent with the SAB 74 obligation to disclose the potential effects of an issued but not yet effective rule.

The rescission complication. The OIRA submission changes the analysis at the margin. A rule for which a rescission proposal has been formally submitted to OIRA is qualitatively different from a rule that is merely stayed. Companies that had been disclosing the climate rule as a pending rule with a compliance date may now appropriately update their SAB 74 disclosure to reflect that the SEC has formally initiated the rescission process and that the rule may not take effect in its current form.

The practical conclusion. Most disclosure teams should continue to include a SAB 74-style footnote for the 2024 climate rule in their 2026 filings, but the content of that footnote should be substantially updated from the 2025 version to reflect the current regulatory reality. The footnote that said "this rule is expected to require disclosure beginning with our FY2025 10-K" needs to be replaced with language that accurately describes the rule's current status, the rescission proceeding, and the resulting uncertainty about whether and when the rule will take effect.

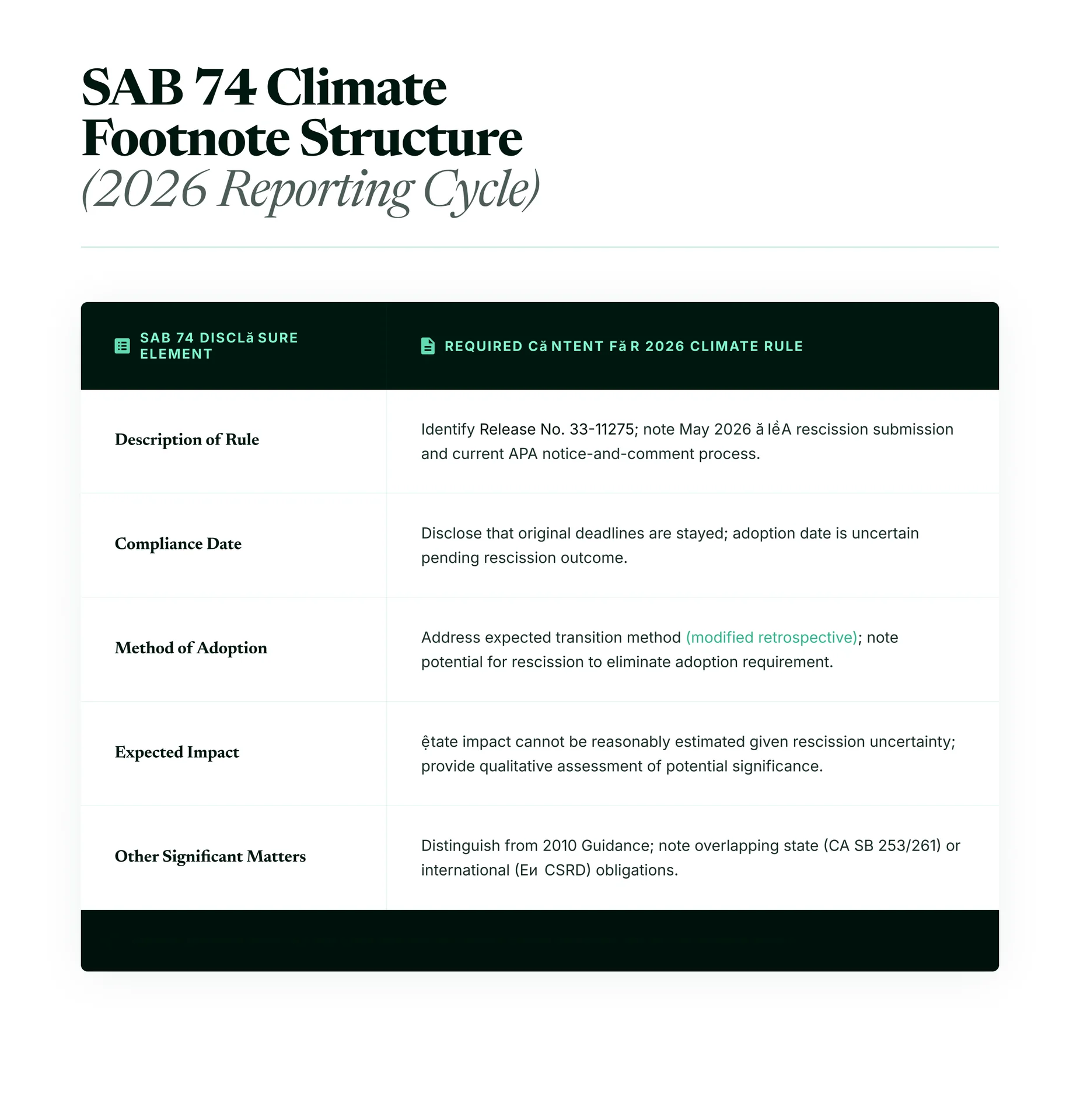

What Must the SAB 74 Climate Footnote Actually Say in 2026?

The SAB 74 climate footnote for 2026 filings must accurately reflect where the rule stands, what is uncertain, and what the company's response has been. Here is the framework for drafting that disclosure.

Element 1: Description of the rule and its current regulatory status

Identify the rule (Release No. 33-11275, Enhancement and Standardization of Climate-Related Disclosures for Investors), the date it was adopted (March 2024), its general scope, and its current regulatory status. The description must accurately convey that the rule is on the books but subject to a voluntary stay, that the SEC has voted not to defend the rule in pending Eighth Circuit litigation, and that the SEC submitted a proposed rescission to OIRA on May 4, 2026.

A disclosure that simply says "this rule is expected to be effective for large accelerated filers for fiscal year 2025" is inaccurate and should not be included. A disclosure that says "this rule was adopted in March 2024, is currently subject to a voluntary stay, and may be rescinded through a formal notice-and-comment process initiated in May 2026" is accurate.

Element 2: The company's compliance date position

Given the stay and the rescission proceeding, most companies will disclose that the compliance dates originally established in the rule have not taken effect due to the voluntary stay, and that the outcome of the rescission process will determine whether any compliance obligations arise. Companies that had been undertaking implementation activities can describe the status of those activities and whether they have been paused or modified in response to the regulatory uncertainty.

Element 3: Assessment of the expected impact

SAB 74 requires a discussion of the expected impact on financial statements unless not known or reasonably estimable. For the climate rule, the honest disclosure for most companies in 2026 is that the impact cannot be reasonably estimated given the deep uncertainty about whether the rule will take effect in its current form, in a modified form, or not at all. That conclusion that the impact is not reasonably estimable due to regulatory uncertainty is itself a meaningful disclosure and should be stated plainly rather than hedged into meaninglessness.

Companies that have material Scope 1 or Scope 2 GHG emissions, significant physical climate risk exposure, or significant adaptation investment that would have been required under the 2024 rule should note that even if the federal rule is rescinded, state law obligations (California's SB 253 and SB 261, for companies of the applicable revenue thresholds and California nexus) and international obligations (the EU's CSRD, for companies with significant EU operations) may require disclosure on overlapping topics.

Element 4: Distinction from the 2010 SEC climate guidance

This is the element most frequently omitted from 2026 climate footnotes and the one most likely to generate SEC comment. The SAB 74 discussion of the 2024 rule must be clearly distinguished from the company's ongoing obligations under the SEC's 2010 climate guidance (Release No. 33-9106). The 2010 guidance is not affected by the 2024 rule's stay or the rescission proceeding. It is fully in effect and requires companies to disclose material climate-related risks under Regulation S-K and S-X. Failing to address the 2010 guidance while describing the 2024 rule's uncertain status creates an impression that climate disclosure obligations have been suspended, which is inaccurate.

Does the OIRA Rescission Submission Change the SAB 74 Disclosure Analysis?

The May 4, 2026 OIRA submission marks a qualitative change in the regulatory status of the climate rule that should be reflected in SAB 74 disclosures filed after that date.

Before the OIRA submission, companies disclosing the climate rule under SAB 74 could accurately describe it as a rule that had been adopted, was subject to a stay pending litigation, and whose ultimate fate was uncertain. The appropriate disclosure was uncertainty language acknowledging that the rule might be modified, rescinded, or ultimately enforced.

After the OIRA submission, companies can more specifically describe the SEC's formal regulatory action: the Commission has submitted a proposed rescission for OIRA review, representing the first formal step in the APA-required process to eliminate the rule. According to Known Trends' analysis of the OIRA submission, the public can only see that a proposed rule has been submitted to OIRA and will not see the substance of the proposed rule until after OIRA review and further SEC action. The timeline for that process is uncertain but could take months.

The OIRA submission is meaningful but not conclusive. The APA requires notice-and-comment rulemaking for rescission, which means a public proposal, a comment period, SEC staff responses to comments, and a final rule. That process could take 12 to 24 months. During that time, the 2024 rule technically remains on the books.

For SAB 74 drafting purposes, the most defensible approach post-OIRA submission is:

- Reference the specific OIRA submission date (May 4, 2026) as a material regulatory development

- State that the proposed rescission has not yet been published for public comment and the substance of the proposal is not yet public

- Note that the APA-required notice-and-comment process must be completed before formal rescission takes effect

- Conclude that the company cannot estimate the financial statement impact of the 2024 rule given the uncertainty about whether it will take effect in its current form, in a modified form, or not at all

- Reaffirm that the company continues to assess and disclose material climate-related risks under the SEC's 2010 interpretive guidance, which remains fully operative

What Does the SEC's 2010 Climate Guidance Still Require?

The SEC's 2010 interpretive guidance (Release No. 33-9106, Commission Guidance Regarding Disclosure Related to Climate Change) is separate from the 2024 rule and is fully in effect, regardless of the 2024 rule's regulatory trajectory.

The 2010 guidance requires companies to assess and disclose material climate-related risks under existing Regulation S-K requirements. Specifically, it identifies four disclosure contexts in which climate-related information may be material:

Item 101 (Business description): Companies must disclose the material effects of compliance with environmental laws, including environmental regulations prompted by climate change, on capital expenditures, earnings, and competitive position.

Item 103 (Legal proceedings): Material climate-related legal proceedings, including regulatory enforcement actions and significant litigation, must be disclosed.

Item 503(c) (Risk factors) and Item 1A: Material risks related to climate change, including physical risks (changes in weather patterns, flooding, drought) and regulatory risks (the cost of complying with existing or anticipated climate-related regulations), must be disclosed as risk factors if material.

Item 303 (MD&A): Known trends and uncertainties related to climate change that are likely to have a material effect on the company's financial condition or results of operations must be addressed in MD&A. This includes both physical impacts of climate on operations and the regulatory and financial risks from climate-related legislation and regulation.

According to Continuuiti's analysis of the regulatory environment, while the 2024 rule remains in limbo, the 2010 interpretive guidance is still fully in effect. This guidance requires public companies to disclose material climate-related risks under existing Regulation S-K and S-X.

For SAB 74 disclosure purposes, this means the footnote addressing the 2024 rule's uncertain status must be accompanied by, or clearly distinguish itself from, the company's substantive Regulation S-K disclosures under the 2010 framework. These are not the same exercise. The SAB 74 footnote addresses the potential future impact of an unenforceable rule. The 2010 guidance compliance requires current, material, specific disclosures about climate-related risks that exist today.

How Should You Draft the SAB 74 Climate Footnote for the 2026 Filing Cycle?

Based on the current regulatory environment, here is a structured framework for drafting a defensible SAB 74 climate footnote for fiscal year 2025 annual reports and Q1 2026 interim reports filed after May 4, 2026.

The disclosure must be in two locations. SAB 74 requires disclosure in both the MD&A and the financial statement footnotes. The two disclosures serve different purposes — the financial statement footnote addresses the quantitative financial statement impact (or explains why it cannot be estimated), while the MD&A addresses the prospective and forward-looking aspects including implementation status and business practice changes.

The footnote must describe the regulatory history accurately. The note should identify: the March 2024 adoption of the climate disclosure rule under Release No. 33-11275; the voluntary stay of the rule's compliance deadlines pending litigation; the SEC's March 2025 vote to end its defense of the rule; the Eighth Circuit's September 2025 decision to hold the case in abeyance; and the SEC's submission of a proposed rescission rule to OIRA on May 4, 2026. Each of these facts is publicly available and is relevant to the reader's assessment of the rule's likely impact.

The footnote must address quantification honestly. Most companies in 2026 cannot reasonably estimate the financial statement impact of the 2024 climate rule because the rule may never take effect. The disclosure should say so plainly: "Given the uncertainty about whether the rule will take effect in its current form, the Company cannot reasonably estimate the financial statement impact of adoption at this time." That conclusion is itself meaningful information and satisfies the SAB 74 disclosure requirement for situations where the impact is not known or reasonably estimable.

Companies with significant exposure should go further. Companies for which the 2024 rule would have imposed material compliance costs particularly those required to provide Scope 1 and Scope 2 emissions data, those with significant physical climate risk exposure requiring quantification, or those with material climate-related capital expenditure commitments should describe qualitatively what the rule would have required of them and why the uncertainty about its implementation prevents quantification at this time. This is more informative than a generic "not estimable" statement and more defensible in an SEC review.

The rescission limbo creates specific SEC comment letter risks that disclosure teams should anticipate in 2026.

Risk 1: Omitting SAB 74 disclosure entirely for the 2024 rule. Some companies may conclude that because the rule is being rescinded, they have no obligation to disclose it under SAB 74. This conclusion is legally and regulatorily risky. The rule has not been rescinded. It is on the books. SAB 74's obligation runs from issuance, not from enforcement. Companies that omit climate-rule SAB 74 disclosure entirely in their 2026 filings should expect the SEC to ask why.

Risk 2: Updating the 2025 SAB 74 language without acknowledging the regulatory change. Companies that carry forward their 2025 SAB 74 climate footnote language without updating it to reflect the OIRA submission and the rescission proceeding are providing stale disclosure. If the OIRA submission is a material regulatory development and for companies that had been preparing for compliance with the 2024 rule, it clearly is the disclosure must reflect it.

Risk 3: Conflating the 2024 rule's status with the 2010 guidance obligations. Language that suggests the rescission proceeding reduces the company's climate disclosure obligations under existing principles-based standards is inaccurate. The 2010 guidance is not affected by the 2024 rule's status. SEC staff will comment on any disclosure that creates the impression that climate-related risk disclosure obligations have been reduced when the 2010 guidance framework is unchanged.

Risk 4: Omitting state and international climate disclosure obligations. For companies subject to California's SB 253 or SB 261 (despite current enforcement injunctions), or to the EU's CSRD, the federal rescission proceeding does not reduce those obligations. SAB 74 and MD&A disclosures that address the federal climate rule without acknowledging other applicable climate disclosure obligations may be incomplete for companies with material California or EU operations.

Risk 5: Inadequate qualitative disclosure when quantification is not possible. SAB 74 does not excuse disclosure entirely when quantification is not possible. It requires companies in that situation to provide qualitative disclosures about the significance and nature of the expected impact. Generic statements like "the impact is unknown" without any qualitative assessment of what the rule would have required and why quantification is not possible are inadequate. According to BDO's SAB 74 guidance, the SEC staff expects that when a reasonable estimate for the impact of the standard is not available, the registrant should consider providing additional qualitative disclosures about the significance of the impact.

Frequently Asked Questions

What is SAB 74 and does it apply to the SEC climate disclosure rule?

SAB 74 (Staff Accounting Bulletin No. 74, codified as SAB Topic 11.M / ASC 250-10-S99-5) requires companies to disclose in their SEC filings the expected effects of recently issued but not yet effective standards. The 2024 SEC climate disclosure rule (Release No. 33-11275) was validly adopted and has defined compliance dates. Despite the voluntary stay and the pending rescission proceeding, the rule technically remains on the books and has not been formally rescinded. Most disclosure advisors recommend that SAB 74-style disclosure remain appropriate for the 2024 climate rule in 2026 filings, with substantially updated language reflecting the current regulatory status.

What is the current status of the SEC climate disclosure rule as of May 2026?

The rule was adopted March 2024, stayed April 2024 pending litigation, and its defense was abandoned by the SEC in March 2025. The Eighth Circuit held the case in abeyance in September 2025 and directed the SEC to determine the rule's fate through notice-and-comment rulemaking. On May 4, 2026, the SEC submitted a proposed rescission to OIRA the first formal step toward formal elimination of the rule. The substance of the rescission proposal is not yet public. The rule remains on the books but is unenforceable and appears headed toward formal rescission.

What does SAB 74 require for the 2026 climate footnote?

The footnote must describe the 2024 rule and its current regulatory status accurately, including the OIRA submission of May 4, 2026. It must address the expected financial statement impact or explain why the impact cannot be reasonably estimated. For most companies in 2026, the honest disclosure is that the impact cannot be estimated given the uncertainty about whether the rule will take effect. The footnote must be clearly distinguished from the company's obligations under the SEC's 2010 climate guidance, which is fully in effect and requires current, substantive Regulation S-K disclosures of material climate-related risks.

Does the 2010 SEC climate guidance still apply?

Yes. The SEC's 2010 interpretive guidance (Release No. 33-9106) is entirely separate from the 2024 rule and is not affected by the 2024 rule's stay, the rescission proceeding, or the OIRA submission. The 2010 guidance requires companies to assess and disclose material climate-related risks under existing Regulation S-K Items 101, 103, 1A, and 303. These obligations exist regardless of the 2024 rule's fate and must be separately addressed in every 10-K and 10-Q.

What climate disclosures are still required even if the 2024 rule is rescinded?

If the 2024 rule is formally rescinded, the 2010 SEC climate guidance remains fully in effect, requiring disclosure of material climate-related risks under existing Regulation S-K. For companies with significant California operations and revenues above the applicable thresholds, California's SB 253 (requiring GHG emissions disclosure) and SB 261 (requiring climate financial risk disclosure) impose separate obligations, subject to current enforcement injunctions. For companies with significant EU operations, the EU's Corporate Sustainability Reporting Directive (CSRD) imposes disclosure obligations that are not affected by SEC rulemaking.

What are the SEC comment letter risks for climate disclosure in 2026?

The primary comment risks are: omitting SAB 74 disclosure for the 2024 rule based on the erroneous conclusion that rescission eliminates the disclosure obligation; failing to update 2025 SAB 74 language to reflect the OIRA submission; conflating the 2024 rule's status with the 2010 guidance in a way that suggests reduced disclosure obligations; and providing only generic "impact unknown" language without the qualitative disclosure SAB 74 requires when quantification is not possible.

Key Takeaways

- The SEC's 2024 climate disclosure rule (Release No. 33-11275) remains on the books as of May 2026 despite the voluntary stay, the SEC's decision to end its defense, and the May 4, 2026 OIRA submission of a proposed rescission. The rule has not been formally rescinded and the APA-required rescission process takes time.

- SAB 74 disclosure for the 2024 climate rule remains appropriate in 2026 filings. The content of that disclosure must be substantially updated from 2025 versions to accurately describe the OIRA submission and the resulting uncertainty about whether the rule will take effect.

- The SAB 74 climate footnote must state that the financial statement impact cannot be reasonably estimated given the uncertainty about the rule's fate, while providing qualitative disclosure about what the rule would have required and why quantification is not possible for the company's specific situation.

- The SEC's 2010 climate guidance (Release No. 33-9106) is fully in effect and requires disclosure of material climate-related risks under Regulation S-K regardless of the 2024 rule's status. The SAB 74 footnote addressing the 2024 rule must be clearly distinguished from, not confused with, the company's ongoing 2010 guidance compliance obligations.

- Companies subject to California's climate disclosure laws or the EU's CSRD have climate disclosure obligations that exist independently of SEC rulemaking and must be addressed in their own disclosure framework analysis.