The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, as Public Law 119-21, made sweeping changes to the clean energy tax credit landscape established by the Inflation Reduction Act of 2022. For teams active in the credit transfer market under IRC Section 6418, the most operationally significant OBBBA change is not a repeal of transferability it is the addition of a new category of prohibited transferees and the introduction of buyer-side diligence requirements that did not exist before enactment.

Understanding what changed, what did not, and what it means for transactions in the second half of 2025 and into 2026 is the central task for tax and finance teams active in this market. This post maps those changes precisely, in the sequence that transactions teams encounter them.

What Is Section 6418 and How Did It Work Before the OBBBA?

Section 6418 of the Internal Revenue Code was enacted as part of the Inflation Reduction Act of 2022. It allows eligible taxpayers that generate certain clean energy tax credits called "applicable credits" to transfer all or a portion of those credits to an unrelated third-party buyer for cash. The transferee-buyer pays cash for the credit and uses it to offset its own federal income tax liability. The cash consideration paid by the buyer is neither includable in the seller's gross income nor deductible by the buyer.

Before the OBBBA, eleven clean energy credits were transferable under Section 6418. These included the Section 45Y Clean Electricity Production Credit, Section 48E Clean Electricity Investment Credit, Section 45X Advanced Manufacturing Production Credit, Section 45Q Carbon Oxide Sequestration Credit, Section 45U Zero-Emission Nuclear Power Production Credit, Section 45V Clean Hydrogen Production Credit, Section 45Z Clean Fuel Production Credit, and several others. The transferability of each credit was tied to the phaseout date of the underlying credit a taxpayer that could still claim the credit in a given tax year could also transfer it.

The IRS issued final regulations under Treas. Reg. Section 1.6418-1 through 1.6418-4 in March 2024, which established the pre-filing registration process, the documentation requirements, and the mechanics of the transfer election. Under those regulations, a seller must complete pre-filing registration through the IRS Energy Credits Online portal to receive a registration number for each credit being transferred, and the buyer must include the registration number on its return when claiming the transferred credit.

Before the OBBBA, there was no restriction on who could be a transferee. Any taxpayer with a federal income tax liability could buy a transferred credit, subject only to the requirement that the buyer and seller be unrelated as defined in Sections 267(b) and 707(b)(1). The buyer could be a domestic corporation, a partnership, an S corporation, an individual, or a foreign person with U.S. tax liability. The OBBBA changed this.

What Did the OBBBA Change About Section 6418 Tax Credit Transfers?

The OBBBA made one structural change to Section 6418 and left the rest of the transfer framework intact. The structural change is the addition of Section 6418(g), which prohibits the transfer of specified credits to Specified Foreign Entities (SFEs).

According to Arnold and Porter's analysis of the OBBBA's clean energy provisions, transferability of credits under Section 6418 generally remains unchanged from the IRA framework, and eligibility for direct pay under Section 6417 is also maintained. The OBBBA did not repeal Section 6418. It did not reduce the number of credits that can be transferred. It did not change the mechanics of the transfer election, the pre-filing registration requirement, or the documentation standards under the final Treasury regulations.

What the OBBBA added is a prohibition on the buyer side for specific credit types. Under new Section 6418(g), for tax years beginning after July 4, 2025 (the date of OBBBA enactment), a taxpayer may not transfer a credit under Section 45Q, 45U, 45X, 45Y, 45Z, or 48E to a Specified Foreign Entity. The prohibition applies to the transfer transaction itself, not merely to the underlying credit claim. According to Bracewell's analysis, the OBBBA prohibits the transfer of any portion of the tax credits under these six sections to Specified Foreign Entities.

The OBBBA did not impose the SFE transfer prohibition on all transferable credits. Credits under Sections 45V (clean hydrogen) and the legacy Section 45 and Section 48 credits (for projects placed in service before 2025) are not subject to the Section 6418(g) SFE transfer prohibition. This distinction matters for deal teams structuring transactions involving projects or credits generated under different statutory authorities.

What Is a Specified Foreign Entity for Section 6418 Purposes?

A Specified Foreign Entity (SFE) is a defined term under the OBBBA with specific legal criteria. Understanding the definition precisely is necessary because the SFE determination drives both seller-side eligibility and buyer-side diligence in every affected credit transfer.

The OBBBA distinguishes between two categories of Prohibited Foreign Entities (PFEs): Specified Foreign Entities (SFEs) and Foreign Influenced Entities (FIEs). The Section 6418(g) transfer prohibition applies to SFEs. FIEs face separate restrictions on credit eligibility but are not subject to the Section 6418(g) transfer prohibition in the same way.

According to Novogradac's analysis of the FEOC and SFE rules, an SFE is generally an entity that is a foreign entity of concern from a country designated as a foreign adversary for purposes of the OBBBA. The four countries designated as foreign adversaries under the applicable provisions are China, Russia, North Korea, and Iran. An entity is an SFE if it is incorporated in, organised under the laws of, or has its principal place of business in one of those countries, or if it is owned or controlled by the government of one of those countries.

The SFE determination is made as of the last day of the tax year for which the applicable credit is claimed. For the first taxable year beginning after July 4, 2025, the determination is made on the first day of that taxable year. For calendar-year taxpayers, this means the SFE test for the 2025 tax year is applied on January 1, 2026, and the test for all subsequent years is applied on December 31 of the applicable year.

According to Reunion Infrastructure's comprehensive guide, entities are tested on the last day of the tax year for which the applicable credit is claimed, except that the only exception is the first taxable year after July 4, 2025, where the test takes place on the first day of the taxable year.

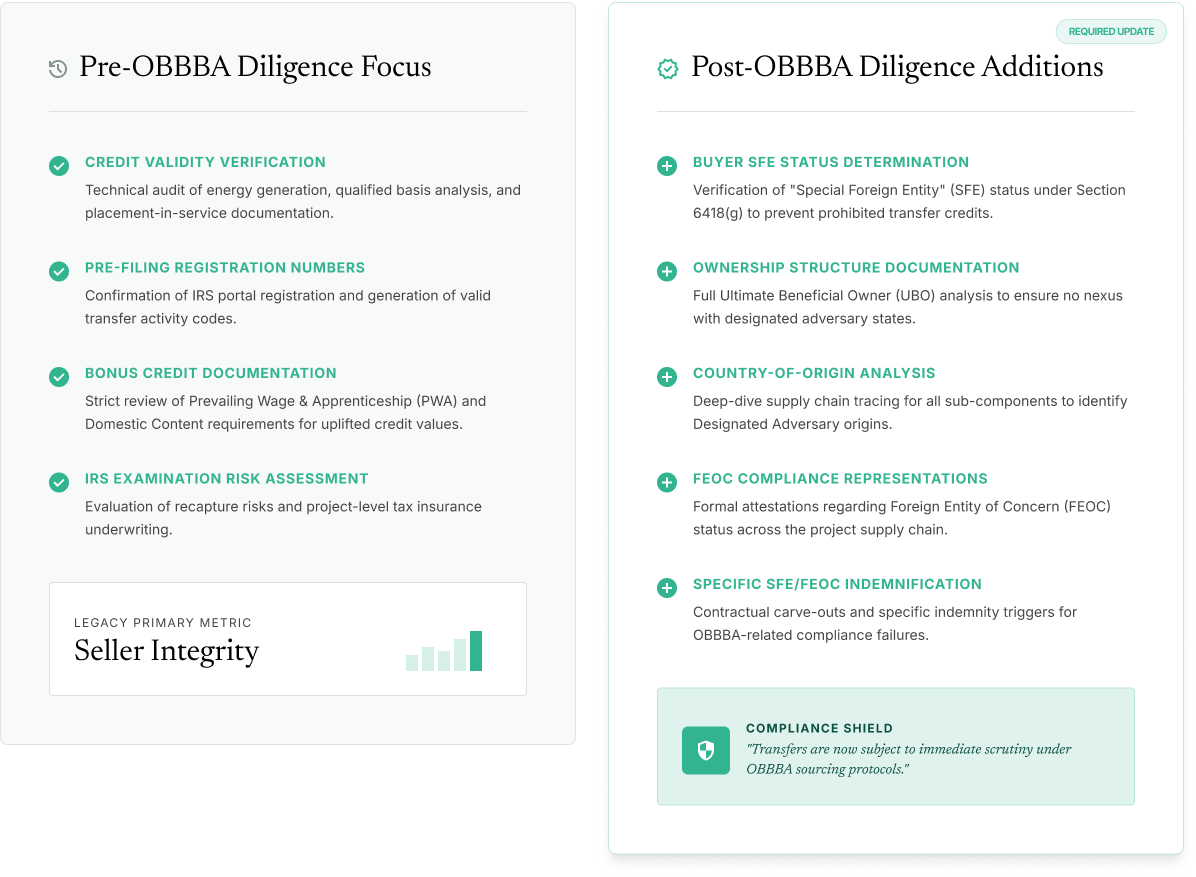

The practical consequence for deal teams: every credit transfer agreement involving the six affected credit types must now include a buyer representation that the buyer is not an SFE as of the applicable test date, and sellers must obtain and retain documentation supporting that representation. Misrepresentations by buyers regarding SFE status carry penalties.

Which Section 6418 Transferable Credits Are Still Available After the OBBBA?

All eleven credits that were transferable under Section 6418 before the OBBBA remain transferable after it, subject to the credit-specific phaseout and termination dates that the OBBBA imposed on many of them. The OBBBA's changes to transferability are the SFE buyer prohibition (for six specific credits) and the natural reduction in the credit transfer market driven by accelerated phaseouts of the underlying credits.

Here is the credit-by-credit status for each affected credit type following OBBBA enactment:

Section 45Y - Clean Electricity Production Credit. Transferable under Section 6418. Transfer to SFEs prohibited. Wind and solar projects that begin construction after July 4, 2026 must be placed in service before January 1, 2028 to qualify for the credit. Projects with construction beginning before July 5, 2026 remain eligible under the prior IRA phaseout schedule. Foreign entity restrictions (FIE rules) apply beginning in taxable years starting after July 4, 2025 for projects claiming Section 45Y credits, regardless of when construction commenced.

Section 48E - Clean Electricity Investment Credit. Transferable under Section 6418. Transfer to SFEs prohibited. Wind and solar projects beginning construction after July 4, 2026 must be placed in service before January 1, 2028. Energy storage technology is not subject to the placed-in-service deadline. FIE and SFE restrictions parallel those for Section 45Y.

Section 45X - Advanced Manufacturing Production Credit. Transferable under Section 6418. Transfer to SFEs prohibited. Wind component credits under Section 45X are eliminated for components sold after December 31, 2027. Critical minerals credits phase down starting in 2034, with termination after 2033. Material assistance from a PFE can disqualify the underlying credit for projects manufacturing under affected arrangements.

Section 45Q - Carbon Oxide Sequestration Credit. Transferable under Section 6418. Transfer to SFEs prohibited. The underlying credit structure is largely unchanged by the OBBBA. SFE transfer prohibition applies.

Section 45U - Zero-Emission Nuclear Power Production Credit. Transferable under Section 6418. Transfer to SFEs prohibited. The OBBBA omits the phaseout schedule that was proposed in earlier versions of the legislation. The credit termination date remains December 31, 2032, unchanged from the IRA.

Section 45Z - Clean Fuel Production Credit. Transferable under Section 6418, but transfers to SFEs are prohibited. The OBBBA extends the Section 45Z credit. Transfers of Section 45Z credits to SFEs are specifically prohibited under the amended Section 6418(g).

Section 45V - Clean Hydrogen Production Credit. Transferable under Section 6418. The Section 6418(g) SFE transfer prohibition does not apply to Section 45V. Hydrogen production credit transfers remain unrestricted by the SFE prohibition as enacted. According to the Tax Law Center's analysis, the law does not apply foreign entity rules to Section 45V, and therefore Section 45V credits remain transferable without the SFE restriction.

How Does the OBBBA Change Buyer Diligence in Section 6418 Transactions?

Before the OBBBA, buyer diligence in a Section 6418 credit transfer focused primarily on the seller and the project: verifying that the credit was validly generated, confirming that the seller completed pre-filing registration, reviewing the project's eligibility for the claimed credit amount and any bonus amounts (prevailing wage, apprenticeship, domestic content), and assessing the risk of an IRS examination of the underlying credit claim.

After the OBBBA, buyer diligence must now extend to an assessment of the buyer's own SFE status for transactions involving the six restricted credit types. This is a structural change to the diligence framework: the buyer is now an active diligence subject, not merely the counterparty.

According to Bricker and Eckler's guide to Section 6418 transfers post-OBBBA, FEOC concerns are top of mind for every party looking to buy or sell IRA tax credits post-OBBBA. Sellers may need to represent to buyers that they have complied with applicable FEOC requirements and provide documentation to substantiate the same for diligence purposes. Correspondingly, buyers must confirm and represent to sellers that they are not SFEs.

The documentation requirements under the existing final regulations (Treas. Reg. Section 1.6418-2) require sellers to provide buyers with the minimum documentation necessary to substantiate the credit claim and any bonus amounts. The OBBBA adds to this framework the need for representations and warranties addressing SFE status, and in many transactions, supporting documentation such as corporate formation records, ownership structure charts, and, where applicable, government certifications addressing foreign ownership or control.

From a seller's perspective, a sale of credits to a buyer that turns out to be an SFE creates significant legal risk. The credit transfer is prohibited under Section 6418(g), and the buyer would be unable to legally claim the transferred credit. Transaction documentation should include representations by the buyer regarding non-SFE status, a covenant to notify the seller if SFE status changes during the applicable test period, and indemnification provisions covering the seller's exposure if the buyer's representation proves false.

What Remained Unchanged About Section 6418 After the OBBBA?

The OBBBA preserved the core Section 6418 transfer framework in full. Understanding what did not change is as operationally important as understanding what did, because several features of the credit transfer market were subject to legislative debate during the OBBBA's passage and ultimately were not modified.

The transfer mechanism itself is unchanged. Sellers still elect to transfer credits by filing the transfer election with their return and providing the buyer with required documentation. The pre-filing registration requirement through the IRS Energy Credits Online portal remains in place. Buyers still claim transferred credits on their own returns using the seller's registration number.

The cash consideration treatment is unchanged. The consideration received by the seller for a transferred credit is not includable in the seller's gross income. The consideration paid by the buyer is not deductible. This fundamental tax treatment of the transfer cash is preserved.

Direct pay under Section 6417 is unchanged. Tax-exempt entities, state and local governments, and other specified entities that qualify for elective payment (direct pay) under Section 6417 retain that option independently of the Section 6418 transfer framework.

The unrelated party requirement is unchanged. The buyer and seller must remain unrelated parties under Sections 267(b) and 707(b)(1). No affiliated entity transfer exception was created or modified.

The prohibition on retransfer is unchanged. A credit buyer cannot further transfer the credit to another party. The credit purchased through a Section 6418 election can only be claimed by the original buyer-transferee.

Section 45V transfers are unchanged. Clean hydrogen production credits under Section 45V remain transferable without the SFE restriction.

According to RSM's analysis of OBBBA changes to clean energy credits, the OBBBA maintains the pairing of eligibility dates with credit transferability, meaning a taxpayer that can claim a credit in a given year can also transfer it, and the SFE prohibition does not otherwise disrupt this pairing for credits not listed in Section 6418(g).

What Do Sellers Need to Do Before Closing a Section 6418 Transfer Post-OBBBA?

For sellers of credits under the six affected sections (45Q, 45U, 45X, 45Y, 45Z, 48E), the OBBBA introduces a seller-side obligation that is distinct from the buyer-side SFE prohibition: sellers must verify their own FEOC compliance for credit eligibility before assuming the credit they generated is valid and transferable.

The OBBBA imposes FIE and material assistance restrictions on credits under Sections 45X, 45Y, and 48E at the project level. If a project received material assistance from a Prohibited Foreign Entity in the manufacturing of applicable components, the project may be ineligible for the underlying credit. A seller that transfers a credit that was ineligibly claimed creates exposure for both the seller and the buyer.

Sellers should take the following steps before closing a post-OBBBA credit transfer:

Step 1: Confirm the credit is still eligible under the OBBBA phaseout timeline. Wind and solar projects must satisfy construction commencement and placed-in-service deadlines that differ by technology type. Confirm that the project and credit period remain within the applicable eligibility window.

Step 2: Assess FIE and material assistance compliance for Section 45X, 45Y, and 48E credits. Review the project's supply chain for any manufactured products or eligible components sourced from or under effective control of a PFE. According to Bracewell's FEOC guide, until Treasury issues new safe harbor tables by December 31, 2026, taxpayers may rely on the tables in IRS Notice 2025-08 and supplier certifications.

Step 3: Confirm pre-filing registration is complete. The IRS Energy Credits Online registration must be completed for each transferred credit before the transfer election can be filed. Registration numbers must be included in the buyer's return when claiming the credit.

Step 4: Obtain buyer SFE representation. For transfers of credits under the six restricted sections, obtain written representations from the buyer regarding non-SFE status as of the applicable test date, along with supporting ownership documentation. Review indemnification provisions to address the risk that a buyer representation is false.

Step 5: Document everything. A six-year statute of limitations applies to IRS assessments related to material assistance violations under the OBBBA, according to Bracewell's analysis. Documentation standards that were adequate before the OBBBA may be insufficient for transactions closing after July 4, 2025.

Frequently Asked Questions

What is Section 6418 and what did the OBBBA change about it?

Section 6418 allows eligible taxpayers generating certain clean energy tax credits to transfer those credits to unrelated third-party buyers for cash. The cash is not taxable to the seller and not deductible by the buyer. The OBBBA, signed July 4, 2025, added Section 6418(g), which prohibits the transfer of credits under Sections 45Q, 45U, 45X, 45Y, 45Z, and 48E to Specified Foreign Entities (SFEs). All other aspects of the Section 6418 transfer framework the mechanism, the cash treatment, the pre-filing registration requirement, the unrelated party rule, and the retransfer prohibition remained unchanged.

Which credits are affected by the OBBBA's Section 6418 SFE transfer prohibition?

Six credits are subject to the new transfer-to-SFE prohibition: Section 45Q (carbon capture), Section 45U (nuclear production), Section 45X (advanced manufacturing), Section 45Y (clean electricity production), Section 45Z (clean fuel production), and Section 48E (clean electricity investment). Section 45V (clean hydrogen) and legacy Section 45 and Section 48 credits for projects placed in service before 2025 are not subject to the SFE transfer prohibition.

What is a Specified Foreign Entity for Section 6418 purposes?

An SFE is generally an entity incorporated in, organised under the laws of, or having its principal place of business in China, Russia, North Korea, or Iran, or owned or controlled by the government of one of those countries. The SFE determination is made on the last day of the tax year for which the credit is claimed. For the first taxable year beginning after July 4, 2025, the determination is made on the first day of that taxable year (January 1, 2026 for calendar-year taxpayers).

Is a credit transfer to a foreign buyer still permitted after the OBBBA?

It depends on the credit type and the buyer's status. For credits not listed in Section 6418(g) including Section 45V and legacy credits transfers to foreign buyers remain permitted subject to the existing unrelated party rules and U.S. tax liability requirement. For credits under the six restricted sections, transfers to SFEs are prohibited. Transfers to foreign buyers that are not SFEs including buyers from countries other than the four designated foreign adversaries remain permissible.

What diligence should buyers perform before purchasing a Section 6418 credit post-OBBBA?

Buyers must now assess their own SFE status in addition to the seller-side project and credit diligence that was required before the OBBBA. For transactions involving the six restricted credit types, buyers should confirm their organizational structure, ownership, and country of principal operations to verify non-SFE status as of the applicable test date. Buyers should also review seller FEOC compliance documentation for Section 45X, 45Y, and 48E credits to confirm the underlying credit was validly generated without disqualifying material assistance from a PFE.

Did the OBBBA change the tax treatment of the consideration in a Section 6418 transfer?

No. The cash consideration paid by the buyer to the seller for a transferred credit is not includable in the seller's gross income and is not deductible by the buyer. This treatment is unchanged. Direct pay eligibility under Section 6417 is also unchanged. The OBBBA's changes to Section 6418 are limited to the SFE transfer prohibition added by new Section 6418(g).

Key Takeaways

- The OBBBA added Section 6418(g) to the IRC, prohibiting the transfer of credits under Sections 45Q, 45U, 45X, 45Y, 45Z, and 48E to Specified Foreign Entities. All other elements of the Section 6418 transfer framework are unchanged: the mechanism, cash treatment, pre-filing registration, unrelated party requirement, and retransfer prohibition remain intact.

- A Specified Foreign Entity is an entity with ties to China, Russia, North Korea, or Iran. The SFE test is applied on the last day of the tax year for which the credit is claimed or on January 1, 2026 for calendar-year taxpayers for the first post-OBBBA tax year.

- Section 45V (clean hydrogen) and legacy Section 45 and Section 48 credits are not subject to the SFE transfer prohibition. Transfers involving these credit types proceed under the pre-OBBBA framework without the buyer SFE restriction.

- Post-OBBBA buyer diligence must now include an SFE status assessment for every transaction involving the six restricted credit types. Sellers should obtain written buyer representations of non-SFE status and supporting ownership documentation, and include indemnification provisions in the transfer agreement covering false representations.

- A six-year statute of limitations applies to IRS assessments related to material assistance violations under the OBBBA. Documentation standards in credit transfer transactions should be calibrated to this longer review window.

- The OBBBA's phaseouts of the underlying credits particularly for wind and solar under Sections 45Y and 48E will reduce the volume of credits available for transfer over time. Deal teams should verify phaseout eligibility alongside SFE compliance in every affected transaction.