On February 20, 2026, the U.S. Supreme Court held in Learning Resources, Inc. v. Trump that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. The Court of International Trade subsequently ordered U.S. Customs and Border Protection (CBP) to refund all IEEPA duties to importers of record. CBP launched Phase 1 of its Consolidated Administration and Processing of Entries (CAPE) tool on April 20, 2026, to process those refunds. By late April 2026, CBP had received 75,306 CAPE Declarations covering approximately 11.2 million entries roughly 21% of the total entry population and anticipated issuing the first refunds on or about May 11, 2026.

The accounting question these refunds create is not straightforward. There is no explicit US GAAP guidance on how to account for a tariff refund when the underlying tariff has been judicially invalidated. This is not a gap FASB anticipated when it wrote the existing standards. In the absence of direct guidance, companies and their auditors must choose between two established frameworks each with a different recognition threshold and different income recognition timing. Getting this choice wrong, or failing to document the rationale, creates financial statement risk and potential SEC comment letter exposure.

This post maps both frameworks precisely, explains the recognition criteria under each, addresses the CAPE tool's effect on your probability assessment, and covers the follow-on questions that most technical accounting teams encounter once they have selected a model.

What Are IEEPA Tariff Refunds and Why Do They Create an Accounting Question?

IEEPA tariff refunds are payments owed to importers of record by CBP representing the duties previously paid on goods imported under tariff orders issued under the International Emergency Economic Powers Act duties the Supreme Court held were unlawful. According to CBP, approximately 330,000 importers paid or deposited an estimated $166 billion in IEEPA duties across more than 53 million entries between February 2025 and January 2026.

The accounting question arises because US GAAP does not contain explicit guidance on recognising a receivable for a tariff refund resulting from judicial invalidation of the underlying tariff. The question is whether a company should treat its expected refund as a potential recovery of a previously recognised loss (an asset recovery question governed by ASC 410-30 by analogy) or as a contingent gain (a gain contingency question governed by ASC 450-30). The two frameworks answer the same question when can we put this receivable on the balance sheet but they require different levels of certainty before recognition is permitted and produce different financial statement presentations.

The Supreme Court ruling does not itself resolve the accounting question. The ruling establishes the legal right to a refund. The accounting question is a separate determination: when has the company's right to the refund become sufficiently certain, and sufficiently measurable, to support balance sheet recognition under US GAAP.

For December 31, 2025 fiscal year-end filers, the SCOTUS ruling of February 20, 2026 is a post-balance-sheet date event that must be evaluated under ASC 855 (Subsequent Events). Because the ruling occurred after the balance sheet date and the condition creating the right to a refund did not exist at December 31, 2025, it is a non-recognised subsequent event requiring disclosure only, not a balance sheet adjustment to the fiscal 2025 financial statements. The recognition question applies to interim and annual periods beginning after the ruling date principally Q1 2026 for calendar-year companies.

Is There Specific US GAAP Guidance on Accounting for IEEPA Tariff Refunds?

No. There is no authoritative US GAAP standard that directly addresses how to account for a tariff refund when the underlying tariff has been judicially invalidated. FASB did not anticipate this fact pattern when drafting either ASC 410 (Asset Retirement and Environmental Obligations) or ASC 450 (Contingencies).

In the absence of direct guidance, accounting standards require companies to select an accounting policy by analogy to the most relevant existing guidance. According to Deloitte's Heads Up, two models have emerged as the frameworks that technical accounting teams and their auditors are applying:

Model A - ASC 410-30 loss recovery model. The company treats the IEEPA tariffs it previously paid as a loss that has been recognised on its income statement or capitalised into an asset. The refund is an expected recovery of that loss. This model is used by analogy because ASC 410-30 addresses the accounting for recoveries of losses related to environmental and other obligations.

Model B - ASC 450-30 gain contingency model. The company treats the expected refund as a contingent gain a potential asset arising from a past event (the overpayment of duties) whose realisation depends on future events (CBP processing and payment). Under this model, the company applies the gain contingency recognition framework of ASC 450-30 directly.

Both models are acceptable under US GAAP as of the date of this publication. According to Deloitte, the loss recovery model under ASC 410-30 represents the most appropriate analogy; however, application of the gain contingency model may represent an acceptable alternative accounting policy. The choice between models must be applied consistently and disclosed.

What Is the ASC 410-30 Loss Recovery Model for IEEPA Tariff Refunds?

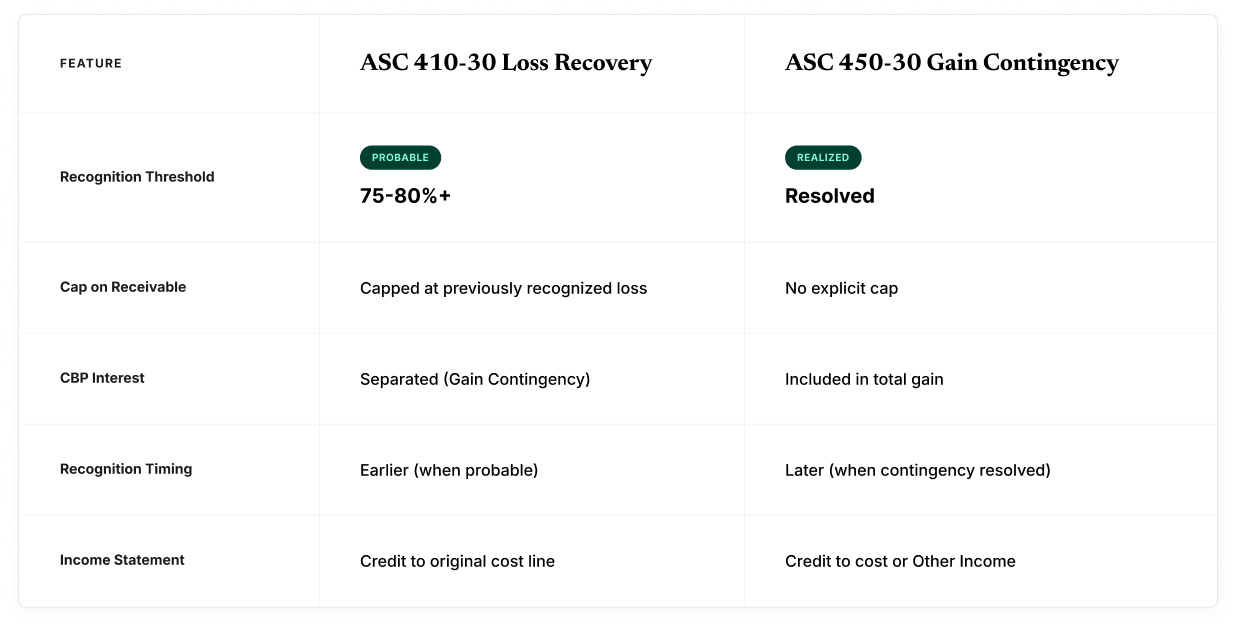

Under the ASC 410-30 loss recovery model applied by analogy, a company recognises a receivable for an anticipated IEEPA tariff refund when it is probable that the refund will be received, subject to a cap equal to the carrying amount of the previously recognised loss.

The recognition criteria under ASC 410-30 by analogy are two conditions that must both be met:

Condition 1: Probable receipt. The refund must be probable. In US GAAP, probable means likely to occur a threshold generally interpreted as significantly more likely than not, often described as approximately 75-80% or higher certainty. This is a higher threshold than the everyday use of the word. According to Grant Thornton's analysis, if an entity applying this model concludes it is probable it will receive IEEPA tariff refunds, it may only recognise an asset to the extent of previously recognised tariff costs.

Condition 2: Cap at previously recognised loss. The ASC 410-30 model caps the recognised asset at the amount of the previously recognised loss. A company cannot recognise a receivable that exceeds the carrying amount of the tariff cost it previously expensed or capitalised. This cap is a structural feature of the loss recovery framework and distinguishes it from the gain contingency model.

Under ASC 410-30 by analogy, a company cannot recognise a gain on the refund that exceeds the amount of loss it previously recognised. Interest that CBP will pay on the refunded duties (at the applicable overpayment interest rate 6% for corporate filers for Q1 2026) represents a gain element that exceeds the prior loss and would be accounted for separately under the gain contingency model when received or when all contingencies are resolved.

According to RSM's Q1 2026 IEEPA tariff reporting publication, the CAPE tool's phased deployment affects the probability assessment under ASC 410-30. By bifurcating the total refund population into entries subject to Phase 1 versus later phases, a company can support a higher probability conclusion for Phase 1 entries (unliquidated entries and entries within 80 days of liquidation) than for entries that would not be covered under Phase 1. This phase-based approach requires separate analysis for each entry category.

What Is the ASC 450-30 Gain Contingency Model for IEEPA Tariff Refunds?

Under the ASC 450-30 gain contingency model, a company treats its expected IEEPA tariff refund as a contingent gain and applies the gain contingency recognition framework directly. ASC 450-30 establishes a strict recognition standard: a contingent gain is recognised only when the gain is realised or realisable meaning all contingencies have been resolved and the gain is no longer contingent.

In practice, this means recognising the refund receivable only when the outcome is essentially certain when there are no remaining contingencies that could prevent receipt. The gain contingency model deliberately delays recognition to avoid overstating assets before the outcome is assured. According to multiple technical accounting analyses, this model generally results in later recognition than the loss recovery model, often deferring recognition until the refund is actually received or the specific entry has been processed and approved through CAPE.

The ASC 450-30 model does not impose a cap on the recognised amount. Under the gain contingency framework, interest income from CBP can be recognised together with the principal refund amount when the contingency is resolved, because the entire amount (principal plus interest) represents the realisation of the gain contingency. This distinguishes it from the ASC 410-30 treatment, under which interest must be separated from the principal refund.

As Uniqus notes in its analysis, a reporting entity may reasonably apply the guidance in ASC 450-30 on gain contingencies and recognise IEEPA tariff recoveries when received. This means some companies applying the gain contingency model will have no balance sheet recognition until cash is received from CBP a conservative approach that eliminates recognition risk but also delays income recognition relative to the loss recovery model.

What Is the Difference Between ASC 410-30 and ASC 450-30 for Recognising IEEPA Refunds?

The five practical differences between the two models are the following.

Recognition threshold. ASC 410-30 by analogy permits recognition when receipt is probable a meaningful but not absolute level of certainty. ASC 450-30 requires recognition only when all contingencies are resolved and the gain is realised or realisable a higher certainty threshold that in practice often means waiting until CAPE processing is complete for the specific entries.

Cap on recognised receivable. Under ASC 410-30, the receivable is capped at the amount of the previously recognised loss the tariff cost the company expensed or capitalised. Under ASC 450-30, there is no explicit cap. The company recognises the full amount once the contingency is resolved, including CBP interest.

Treatment of CBP interest. Under ASC 410-30, interest owed by CBP on the refunded duties (at the applicable overpayment interest rate) represents a gain in excess of the previously recognised loss and is accounted for separately under the gain contingency framework. Under ASC 450-30, interest is part of the total contingent gain and recognised at the same time as the principal refund.

Balance sheet timing. The ASC 410-30 model generally permits earlier balance sheet recognition when receipt is probable which under the phased CAPE framework may allow recognition for Phase 1 entries in Q1 or Q2 2026 depending on company-specific facts. The ASC 450-30 model generally results in recognition closer to actual cash receipt.

Income statement classification. When a refund is recognised under ASC 410-30, the offsetting credit reverses the cost accumulated in whatever line item originally carried the tariff cost: reduction of inventory still on hand, reduction of cost of goods sold for inventory already sold, or reduction of the carrying value of property, plant and equipment if tariffs were capitalised into a fixed asset. Under ASC 450-30, the same classification logic applies to the extent the refund reverses a prior period cost but any amount exceeding the prior period cost (including interest) is recognised as other income.

When Can You Recognise an IEEPA Tariff Refund Receivable on the Balance Sheet?

The answer depends on which model you are applying and the specific facts of your entries as of your reporting date.

Under ASC 410-30 by analogy: You can recognise a refund receivable when it is probable that you will receive the refund for a specific pool of entries, measured at no more than the amount of the tariff cost you previously recognised for those entries. The CAPE tool's phased structure creates a natural segmentation for this analysis. According to RSM, Phase 1 entries unliquidated entries and entries within 80 days of liquidation are more likely to support a probable conclusion as of Q1 2026 than entries that will not be addressed until later phases. For entries excluded from Phase 1, the uncertainty about timing and amount may prevent a probable conclusion in Q1 2026.

Under ASC 450-30: You recognise the refund receivable when all contingencies are resolved and the gain is no longer contingent. Factors that bear on this assessment include whether your specific entries have been accepted through CAPE, whether CBP has completed its validation and recalculation for those entries, and whether any compliance review is pending. For most companies as of Q1 2026, the existence of remaining uncertainty including uncertainty about the administration's potential appeal of CIT rulings and the phased nature of CAPE processing means the gain contingency has not been fully resolved.

Practical conclusion for Q1 2026: Most companies will not have sufficient certainty as of March 31, 2026 to recognise a refund receivable for their entire IEEPA tariff exposure. Companies applying ASC 410-30 by analogy may be able to support recognition for Phase 1 entries if they can document a probable conclusion for those specific entries. Companies applying ASC 450-30 will generally defer recognition until CAPE processing is complete for their specific entries and refunds are received or their receipt is no longer contingent.

What Is the CBP CAPE Tool and What Does It Mean for Your Accounting?

CAPE (Consolidated Administration and Processing of Entries) is a new functionality within CBP's Automated Commercial Environment (ACE) system, launched April 20, 2026, to process IEEPA duty refunds. Rather than handling refunds entry-by-entry, CAPE allows importers of record or their licensed customs brokers to submit a single electronic CAPE Declaration covering up to 9,999 entries.

The CAPE process works as follows according to CBP's official CAPE page:

After a CAPE Declaration is submitted and accepted, ACE removes the IEEPA HTS Chapter 99 codes from the affected entry summaries and recalculates duties without the IEEPA amounts. For unliquidated entries, CBP liquidates them approximately 45 days from the CAPE Declaration acceptance date. For entries already liquidated but not yet final, reliquidation occurs the next business day. CBP then issues a single consolidated lump-sum refund per importer of record via ACH electronic payment to the designated bank account. CBP's stated timeline for valid refunds following CAPE Declaration acceptance is 60 to 90 days, absent compliance review. The applicable overpayment interest rate for Q1 2026 is 7% for non-corporate filers and 6% for corporate filers, calculated from the date of original duty payment through the date of liquidation or reliquidation.

Phase 1 scope. Phase 1 is limited to unliquidated entries and entries liquidated within 80 days of the CAPE submission date. According to Holland and Knight's analysis, Phase 1 is estimated to cover approximately 63% of affected entries. Entries subject to antidumping and countervailing duties, entries in reconciliation, and warehouse entries are excluded from Phase 1 and will be addressed in later phases.

What CAPE means for your accounting: The acceptance of a CAPE Declaration and the transition of entries from "accepted" to "updated" status within CAPE is an observable indicator of progress toward refund receipt. According to Baker Tilly's analysis, early indicators suggest some claims are beginning to move beyond initial acceptance, with a shift in claim status that aligns with reduced pressure on importer bond sufficiency. For companies applying ASC 410-30, CAPE progress can support a probability assessment for Phase 1 entries. For companies applying ASC 450-30, resolution of the contingency still requires completion of CAPE processing and issuance of the refund.

Practical requirement: Only the importer of record or the licensed customs broker who filed the entries can submit a CAPE Declaration. Companies must have an ACE Portal account with the Importer sub-account and must have banking information registered in the ACE Portal for ACH refund receipt. CBP ceased issuing paper refund checks on February 6, 2026. All IEEPA refunds are issued electronically.

What Is the Offsetting Entry When You Recognise an IEEPA Refund Receivable?

The offsetting credit entry for a recognised IEEPA tariff refund receivable depends on where the tariff cost currently resides in your financial statements. According to Grant Thornton's analysis, the appropriate treatment for each scenario is as follows.

Inventory on hand. If the goods on which IEEPA tariffs were paid are still in inventory at the recognition date, recognise the refund receivable as a reduction in the carrying value of that inventory. The inventory cost was originally capitalised to include the tariff cost under the cost accumulation model of ASC 805-50 (Business Combinations) applied by analogy to inventory costing. The refund partially reverses that capitalised cost.

Inventory sold cost of goods sold. If the goods have been sold and the tariff cost has already passed through cost of goods sold in a prior period, recognise the refund receivable as a reduction in cost of goods sold in the current period. There is no restatement of prior period cost of goods sold. The recognition of the receivable in the current period is the mechanism for reflecting the expected recovery.

Property, plant and equipment. If tariffs were paid on imported capital equipment and capitalised into the cost of a fixed asset, recognise the refund receivable as a reduction in the carrying value of that fixed asset. This will affect the future depreciation of the asset, because depreciation is based on the net carrying amount after the cost reduction.

CBP interest. Interest that CBP will pay on the refunded duties represents an amount that, under the ASC 410-30 model, exceeds the previously recognised loss. It cannot be recognised under the loss recovery model at the time the principal refund receivable is recognised. It is recognised as other income under the gain contingency framework when received or when the interest amount is no longer contingent.

What Disclosures Does IEEPA Tariff Refund Accounting Require?

Disclosure requirements apply regardless of which recognition model a company selects and regardless of whether a receivable has been recognised on the balance sheet. Companies should assess disclosure obligations for their Q1 2026 Form 10-Q and all subsequent interim and annual reports until the refund process is resolved.

Accounting policy disclosure. Companies that have recognised, or expect to recognise, a refund receivable must disclose the accounting model they elected ASC 410-30 by analogy or ASC 450-30 and the rationale for that election. An accounting policy disclosure is required because neither model is prescribed by authoritative guidance and the choice constitutes an accounting policy determination.

Quantitative exposure disclosure. According to Uniqus's analysis, companies should disclose the aggregate IEEPA tariff exposure by financial statement line item inventory, cost of goods sold, and property, plant and equipment so readers can assess the magnitude of the potential refund relative to the financial statements.

Recognition status and receivable balance. If a receivable has been recognised, disclose the amount recognised, the basis for the probability or certainty conclusion that supported recognition, and the expected timing of receipt based on CAPE processing.

Uncertainty disclosure. If a receivable has not been recognised, disclose the existence of the contingency, the basis for the conclusion that recognition criteria are not yet met, and the range of possible outcomes including the maximum amount the company expects to recover.

Phase-specific disclosure. Given the CAPE tool's phased structure, disclosures should address separately, where material: the amount subject to Phase 1 processing, the amount subject to later phases, and the expected timing difference between the phases.

Vendor refund obligations. Companies that received tariff refunds from vendors or that owe tariff refunds to customers should disclose the nature and amount of those obligations. See the section below on customer and vendor follow-on accounting.

Monetisation transactions. Companies that have sold or are considering selling their IEEPA refund rights to a third-party funder must disclose the nature of the transaction, the accounting model applied to the proceeds, and the resulting obligation. According to Deloitte, such transactions should generally be accounted for as financing transactions under ASC 470 (akin to sales of future revenues), with the financing derecognised only when legally extinguished under ASC 405.

How Do We Account for IEEPA Tariff Refunds Owed to Our Customers?

Companies that passed IEEPA tariff costs through to customers as price increases must assess whether the Supreme Court ruling and the resulting refund obligation create a requirement to refund those amounts to customers and how to account for that obligation.

Revenue reduction under ASC 606. Consideration paid or payable to a customer that is not in exchange for a distinct good or service received from the customer is accounted for as a reduction of the transaction price under ASC 606-10-32-25. If a company is obligated to refund tariff-related price increases to customers, and those price increases were reflected in the transaction price, the refund obligation reduces revenue in the period in which the obligation arises the later of the period in which the company recognises revenue for the related goods or the period in which it promises or pays the refund.

Assessment of obligation. Not all companies that passed tariff costs to customers are legally obligated to refund them. The obligation depends on the terms of the customer contract, whether the tariff surcharge was a separately identified line item or embedded in the base price, and whether the contract contains provisions addressing tariff reversals. Companies must evaluate each significant customer contract individually before concluding that a customer refund obligation exists.

Inventory valuation impact. Companies that received refunds from vendors covering tariffs the company capitalised into inventory must reduce the carrying value of that inventory by the vendor refund amount. If the inventory has been sold, the vendor refund reduces cost of goods sold in the period of recognition.

Measurement uncertainty. The amount of the customer refund obligation may be uncertain at the balance sheet date because the IEEPA tariff refund from CBP has not yet been processed and the exact refund amount has not been determined. Companies should assess whether a contingent liability exists under ASC 450-20 and disclose it if the obligation is reasonably possible and material.

Frequently Asked Questions

What is the accounting for IEEPA tariff refunds under US GAAP?

There is no specific US GAAP standard on IEEPA tariff refunds. In the absence of direct guidance, companies apply one of two frameworks by analogy: the loss recovery model under ASC 410-30, which permits recognition when receipt is probable and caps the receivable at the amount of the previously recognised tariff loss; or the gain contingency model under ASC 450-30, which requires recognition only when all contingencies are resolved and the gain is realised or realisable. The choice is an accounting policy election that must be applied consistently and disclosed. Both models are currently acceptable under US GAAP.

What is the difference between ASC 410-30 and ASC 450-30 for IEEPA tariff refunds?

The ASC 410-30 loss recovery model permits earlier recognition when receipt is probable and caps the recognised receivable at the previously recognised tariff cost. The ASC 450-30 gain contingency model requires a higher level of certainty (realised or realisable) and generally delays recognition until the contingency is fully resolved, often near the time of actual receipt. Under ASC 410-30, CBP interest on the refund is accounted for separately as a gain contingency. Under ASC 450-30, interest is recognised together with the principal refund when the contingency is resolved.

What is the CBP CAPE tool and how does it affect accounting?

CAPE (Consolidated Administration and Processing of Entries) is CBP's electronic system, launched April 20, 2026, for processing IEEPA tariff refunds. Phase 1, covering approximately 63% of affected entries (unliquidated entries and entries within 80 days of liquidation), allows consolidated submission of up to 9,999 entries per CAPE Declaration. CBP's stated timeline for refund issuance is 60 to 90 days from CAPE Declaration acceptance. For accounting purposes, CAPE's phased structure allows companies to segment their entry population by phase when assessing the probable threshold under ASC 410-30. Phase 1 entries may support an earlier probable conclusion than entries subject to later phases due to greater certainty about timing and amount.

Was the Supreme Court ruling a subsequent event for December 31, 2025 year-end filers?

Yes. The Supreme Court's ruling of February 20, 2026 is a post-balance-sheet date event for December 31, 2025 fiscal year-end filers. Because the condition creating the right to a refund did not exist at December 31, 2025, it is a non-recognised subsequent event under ASC 855. It requires disclosure in the 2025 financial statements if material, but does not permit a balance sheet adjustment to fiscal 2025 financial statements.

What disclosures are required for IEEPA tariff refunds in Q1 2026?

Companies must disclose the accounting model elected (ASC 410-30 or ASC 450-30) and its rationale, the aggregate IEEPA tariff exposure by financial statement line item, the balance of any recognised receivable and the basis for the recognition conclusion, the estimated range of possible outcomes for unrecognised refunds if material, and the status of CAPE filing and expected processing timeline. Companies with customer refund obligations or vendor refund receivables should disclose those separately.

Can companies sell their IEEPA tariff refund rights to a third-party funder?

Yes, but the accounting is complex. According to Deloitte, transactions in which a company receives cash from an investor in exchange for the rights to IEEPA refund cash flows should generally be accounted for as financing transactions under ASC 470, regardless of whether they occur before or after the company has recognised a refund receivable. The financing liability is derecognised only when it is legally extinguished under ASC 405. Other considerations may apply depending on the specific terms of the arrangement, including potential derivative accounting under ASC 815.

Key Takeaways

- There is no authoritative US GAAP guidance specifically addressing IEEPA tariff refund accounting. Companies must apply one of two frameworks by analogy: ASC 410-30 (loss recovery, recognise when probable, cap at prior loss) or ASC 450-30 (gain contingency, recognise when realised or realisable). The choice is an accounting policy election requiring consistent application and disclosure.

- The ASC 410-30 model generally permits earlier recognition than ASC 450-30. For most companies as of Q1 2026, recognition under either model requires careful analysis of which specific entries have progressed through CAPE Phase 1 and whether the probable threshold (ASC 410-30) or the resolved contingency threshold (ASC 450-30) has been met for those entries.

- CBP's CAPE Phase 1, launched April 20, 2026, covers approximately 63% of affected entries. The phased structure is directly relevant to the accounting analysis. Phase 1 entries may support an earlier and stronger probability conclusion than entries deferred to later phases. Separate analysis by entry phase is recommended.

- The offsetting credit for a recognised refund receivable depends on where the tariff cost currently resides: reduction of inventory cost if goods are still on hand, reduction of cost of goods sold if goods have been sold, or reduction of the fixed asset carrying value if tariffs were capitalised into property, plant and equipment.

- CBP interest on refunded duties is accounted for separately from the principal refund under ASC 410-30 (because it exceeds the previously recognised loss) and together with the principal under ASC 450-30 (because it is part of the gain contingency).

- Disclosure is required regardless of whether a receivable has been recognised. Q1 2026 disclosures should address the model elected and its rationale, the total IEEPA exposure by financial statement line, the recognised receivable amount if any, and the uncertainty about remaining phases and timing.