Form 13F has existed since 1975 and its core mechanism has not changed: institutional investment managers that exercise discretion over $100 million or more in Section 13(f) securities must file a quarterly public report of their holdings with the SEC. What has changed is the enforcement environment. In September 2024, the SEC charged eleven institutional investment managers with failing to report certain securities holdings. In September 2023, the SEC brought an enforcement action against a manager that failed to file Form 13F from 2016 through 2022. The SEC levied more than $3.8 million in penalties in a single sweep of late beneficial ownership and insider transaction reports in 2024.

For compliance teams that have been treating Form 13F as a routine administrative exercise, the enforcement pattern is a signal that warrants closer attention to the technical requirements of the filing. This guide maps those requirements precisely.

What Is SEC Form 13F?

Form 13F is a quarterly disclosure form required under Section 13(f) of the Securities Exchange Act of 1934 and Rule 13f-1 thereunder. It requires institutional investment managers that exercise investment discretion over $100 million or more in Section 13(f) securities to publicly report their equity holdings to the SEC within 45 calendar days after the end of each calendar quarter.

The form was first required in 1975. Congress enacted Section 13(f) to increase public visibility into the holdings of large institutional investors, to allow the SEC to monitor market activity and detect potential manipulation, and to support market integrity and investor confidence by making institutional ownership data publicly available.

Form 13F information is filed electronically through the SEC's EDGAR filing system and is publicly available immediately upon filing. The disclosure includes the name and class of each Section 13(f) security held, the number of shares, the fair market value at the end of the reporting period, and whether the manager holds the security in sole, shared, or no voting authority.

According to the SEC's investor education page on Form 13F, institutional investment managers that may have this obligation include investment advisers, banks, insurance companies, broker-dealers, pension funds, and corporations including those headquartered outside the United States, provided they use U.S. mail or other means of interstate commerce in the course of their business.

Who Must File Form 13F?

An institutional investment manager must file Form 13F if it meets two conditions simultaneously: it exercises investment discretion over accounts holding Section 13(f) securities, and the aggregate fair market value of those securities equals or exceeds $100 million on the last trading day of any month of any calendar year.

Both conditions require precise understanding.

Investment discretion. Rule 13f-1 defines an institutional investment manager as any person, other than a natural person, that exercises investment discretion with respect to accounts holding Section 13(f) securities. A person exercises investment discretion if, directly or indirectly, it is authorised to determine what securities are purchased or sold on behalf of the account, or if in practice it makes or participates in such decisions. Managers who share investment discretion with another manager must each separately assess their own filing obligation.

The $100 million threshold. The threshold is assessed on the last trading day of any month of a calendar year, not just at quarter-end. If a manager crosses $100 million in Section 13(f) securities even once during a calendar year, the obligation is triggered. According to the SEC's Form 13F FAQ page, once the threshold is met, the manager must file for the full calendar year and through at least the third calendar quarter of the following year, even if assets subsequently fall below $100 million. The obligation does not terminate immediately when assets drop below the threshold.

Trigger and continuation mechanics. A manager that first crosses $100 million on the last trading day of, for example, August 2026 must file for the quarter ending December 31, 2026 (its first required filing), and then continue through at least the quarter ending September 30, 2027. If assets remain above $100 million at the end of any month in 2027, the obligation continues through 2027 and into 2028.

Foreign managers. The obligation applies to non-U.S. managers if they use U.S. mail or other means or instrumentality of interstate commerce in the course of their business and exercise investment discretion over $100 million or more in Section 13(f) securities. Location of incorporation or headquarters is not a determining factor.

What Are Section 13(f) Securities?

Section 13(f) securities are the specific universe of securities whose holdings must be reported on Form 13F. A manager must count only these securities toward the $100 million threshold and must report only these securities in its quarterly filing.

The SEC publishes the official list of Section 13(f) securities quarterly. Managers may rely on the current list in determining what to report. The list is updated each quarter and managers should use the list published for the relevant quarter-end reporting period.

The categories of securities that appear on the Section 13(f) list include:

Exchange-traded equity securities. Shares of U.S. companies listed and traded on a national securities exchange, including the New York Stock Exchange, Nasdaq, and NYSE American. This is the largest category of Section 13(f) securities for most institutional managers.

Equity options and warrants. Exchange-traded put and call options on equity securities, and warrants to acquire equity securities, are Section 13(f) securities. The underlying equity security and any options or warrants on that security are each separately reportable.

Shares of closed-end investment companies. Shares of registered closed-end funds listed on a national securities exchange are Section 13(f) securities.

Certain convertible debt securities. Convertible notes and debentures that are traded on a national securities exchange are Section 13(f) securities. Plain debt instruments without an equity conversion feature are not.

American Depositary Receipts (ADRs). Exchange-listed ADRs representing ownership in foreign issuers are Section 13(f) securities.

What is not a Section 13(f) security. Mutual fund shares, private fund interests, U.S. Treasury securities, corporate bonds without an equity conversion feature, and most foreign securities not listed on a U.S. exchange are not Section 13(f) securities and are not counted toward the $100 million threshold or reported on Form 13F.

The omission threshold. Under current rules, a manager may omit individual holdings from its Form 13F report if the position is fewer than 10,000 shares and has a fair market value of less than $200,000, or if the position is convertible debt with a principal amount of less than $200,000. Both conditions must be met for the omission to be available. Note that this omission threshold applies to reporting, not to the $100 million threshold calculation all Section 13(f) securities count toward that calculation regardless of size.

What Are the Form 13F Filing Deadlines in 2026?

Form 13F must be filed within 45 calendar days after the last day of each calendar quarter. When the 45th day falls on a Saturday, Sunday, or federal holiday, the deadline moves to the next business day under SEC Rule 0-3(a).

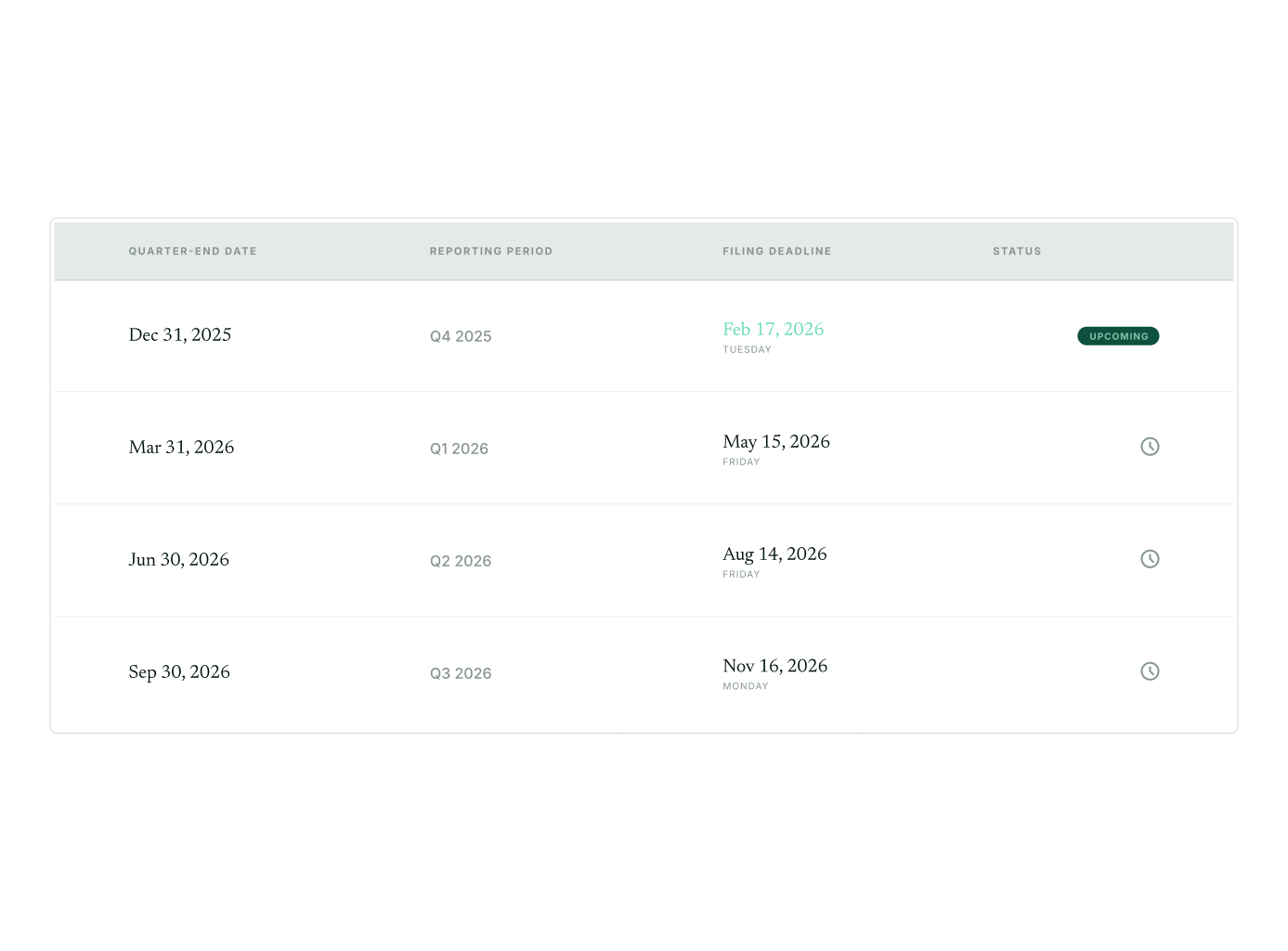

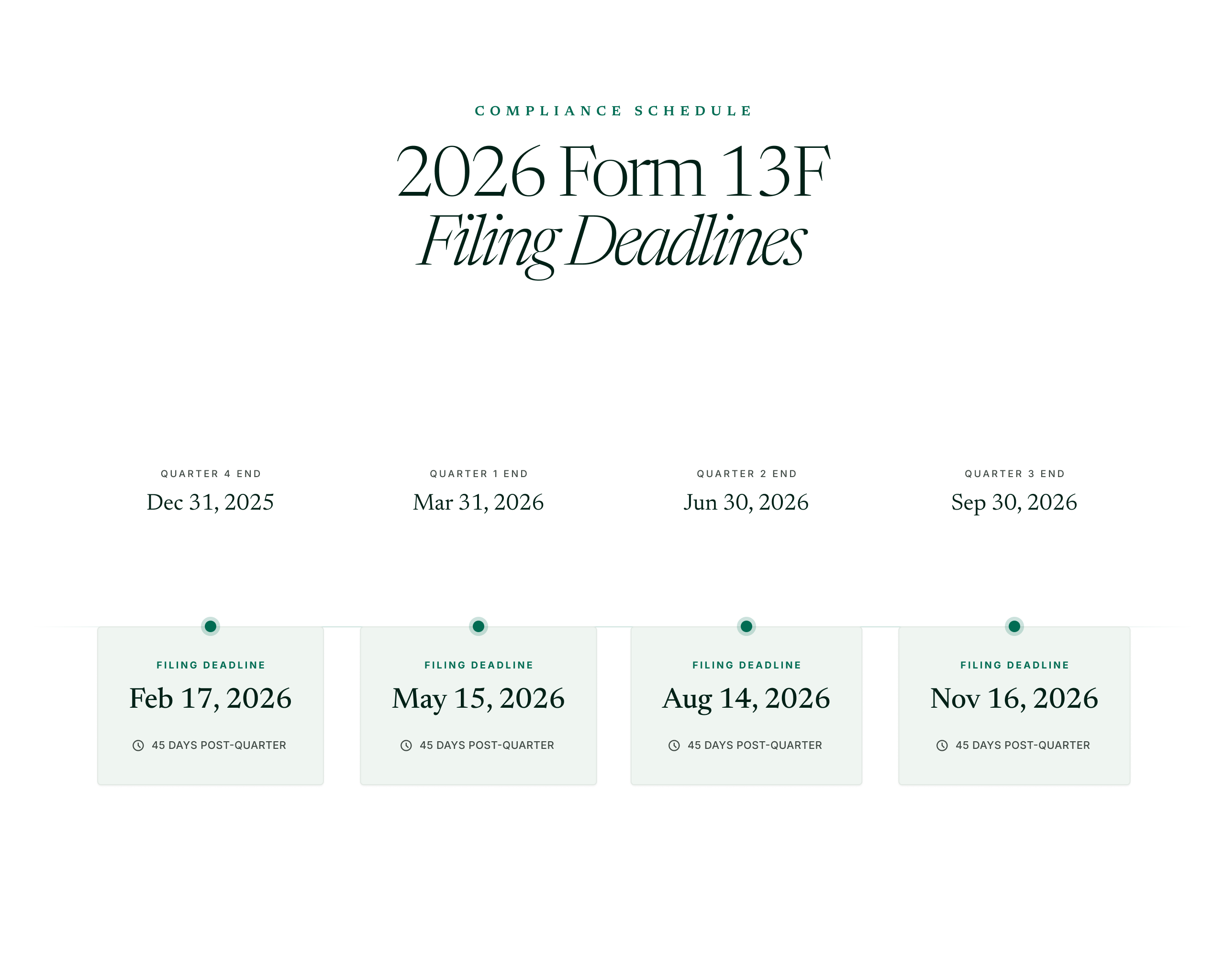

The 2026 Form 13F filing deadlines, as published by the SEC, are:

The February 17, 2026 deadline for Q4 2025 reflects two adjustments: February 14 (the 45th day) was a Saturday, and February 16 (President's Day) was a federal holiday, so the deadline moved to Tuesday February 17, 2026.

The SEC does not grant extensions for Form 13F filing deadlines. There is no Form 12b-25 equivalent for Form 13F. A manager that cannot meet the deadline is expected to file as soon as possible after the deadline rather than waiting for the next filing period. Late filings are accepted by EDGAR but are flagged as late and are subject to enforcement action.

What Must Be Included in a Form 13F Filing?

A complete Form 13F submission consists of two parts: a Cover Page and an Information Table. Both must be filed electronically on EDGAR.

The Cover Page. The Cover Page identifies the filer, the reporting period, the filer's investment manager type, and the total number of issuers and total market value of Section 13(f) securities reported. It also contains a checkbox indicating whether a confidential treatment request accompanies the filing, and fields for the filer's Central Registration Depository (CRD) number and SEC file number if applicable fields added by the 2022 amendments to Form 13F.

The Summary Page. The Summary Page, which precedes the Information Table, sets out the total number of Section 13(f) securities reported and their aggregate market value. It also identifies any other investment managers with whom the reporting manager shares investment discretion over any of the reported securities. If discretion is shared, each manager must identify the other and describe the nature of the sharing arrangement.

The Information Table. The Information Table is the main disclosure. For each Section 13(f) security held at the end of the reporting quarter, the manager must report:

- The name of the issuer

- The title and class of the security (e.g., common stock, put option, call option)

- The CUSIP number of the security

- The fair market value of the holding as of the last trading day of the reporting quarter, rounded to the nearest dollar (amended from the prior standard of rounding to the nearest thousand dollars)

- The number of shares or principal amount held

- The investment discretion classification: sole discretion (SOLE), shared discretion (SHARED), or no discretion (NONE) and the number of shares in each category

- Voting authority: the number of shares over which the manager has sole voting authority, shared voting authority, and no voting authority

- Optionally, the Financial Instrument Global Identifier (FIGI) for the security, if the manager elects to report it

Rounding to the nearest dollar. The 2022 amendments to Form 13F changed the rounding standard for fair market value from the nearest thousand dollars to the nearest dollar. This is a reporting precision change that affects the Information Table calculations for all filers. Compliance teams that use automated data feeds should confirm their systems apply the current rounding standard.

Investment discretion classifications. A manager reports a holding under SOLE discretion if it alone makes the investment decision for that position. It reports under SHARED discretion if the investment decision is made jointly with another manager. NONE is used for accounts where the manager is the filer of record but does not exercise investment discretion. Securities reported under NONE discretion are not counted toward the $100 million threshold but are reported for completeness.

How Do You File Form 13F on EDGAR?

Form 13F must be filed electronically through the SEC's EDGAR system. Paper filings are not accepted. The EDGAR filing system accepts Form 13F submissions in the EDGAR Full Text Search EDGAR XML format (using the EDGAR Form 13F data specifications) or as structured XML data.

The steps to file Form 13F on EDGAR are as follows.

Step 1: Obtain EDGAR filing access. Managers that have not previously filed on EDGAR must obtain EDGAR access credentials. The process involves submitting Form ID to the SEC to obtain a Central Index Key (CIK) number and filing access codes. Form ID can be submitted online through the EDGAR company search system. Processing typically takes one to two business days.

Step 2: Prepare the filing. Prepare the Cover Page, Summary Page, and Information Table in the required format. The SEC's Form 13F instructions provide the complete data specifications. Most institutional managers use compliance software or third-party service providers to generate the required XML file from their portfolio data systems.

Step 3: Verify the Section 13(f) securities list. Before finalising the Information Table, confirm that each security reported appears on the current SEC Section 13(f) securities list for the relevant quarter. The official list is published quarterly on the SEC's investment management page. Reporting a security that is not on the current list is an error that may require an amendment.

Step 4: Submit through EDGAR. Submit the completed filing through EDGAR using the Form 13F-HR form type (for new initial filings and continuing quarterly filings) or Form 13F-HR/A form type (for amendments to a previously filed Form 13F-HR). EDGAR will provide a confirmation of submission. The filing becomes publicly accessible immediately upon acceptance.

Step 5: File the confidential treatment request simultaneously, if applicable. If the manager is requesting confidential treatment for any holdings, the confidential Form 13F must be filed electronically through EDGAR simultaneously with the public Form 13F. The confidential filing is not publicly accessible. See the following section for confidential treatment requirements.

Amendment filings. If a manager discovers an error in a previously filed Form 13F, it should file an amendment on Form 13F-HR/A as promptly as possible. The amendment should explain the nature of the correction and provide the corrected information. The SEC does not have a specific deadline for amendments, but prompt correction is relevant to the enforcement context. A manager that discovers and corrects an error proactively is in a meaningfully different position than one that allows a known error to remain unremedied.

How Does Confidential Treatment Work for Form 13F?

A manager may request that specific holdings disclosed in its Form 13F be withheld from public disclosure for a limited period. This is called a confidential treatment request. The SEC has authority to grant confidential treatment under two categories established in Section 13(f)(4) of the Exchange Act.

Category 1: Ongoing acquisition. Information that would reveal the acquisition strategy of the manager for securities it is actively in the process of acquiring may be granted confidential treatment for up to one year from the required filing date.

Category 2: Risk arbitrage position. Information identifying that the manager holds a risk arbitrage position may be granted confidential treatment for up to one year. The manager must represent in writing that the position was open as of the last day of the reporting period and that the manager had a reasonable belief it may not be able to close the entire position by the required filing date.

How to request confidential treatment. Since the 2022 rule amendments, confidential treatment requests must be filed electronically through EDGAR. The request consists of two elements filed simultaneously with the public Form 13F:

First, a cover letter submitted as a separate EDGAR filing, explaining the factual and legal basis for the confidential treatment request. The cover letter must demonstrate that the information is customarily and actually kept private by the manager, and that failure to grant confidentiality would be likely to cause harm. This standard derives from a 2019 U.S. Supreme Court decision and was formalised in the 2022 amendments.

Second, a confidential Form 13F listing only the securities for which confidential treatment is requested, clearly marked "CONFIDENTIAL TREATMENT REQUESTED" on each page of the Information Table.

The confidential form is submitted through EDGAR but is not publicly accessible. The public Form 13F must still be filed and will list all other holdings not subject to the confidential treatment request. Holdings for which confidential treatment is granted will not appear in the public filing for the duration of the confidential treatment period.

According to the SEC's guidance on Section 13(f) confidential treatment requests, Congress' clear intent in enacting Section 13(f) was that the information be promptly disseminated to the public. Confidential treatment is a narrow exception and is not routinely granted. Managers seeking confidential treatment should apply only where the legal standard is clearly met and should expect the SEC to evaluate the request carefully.

What Happens If You File Form 13F Late or Fail to File?

The SEC has materially increased Form 13F enforcement activity in recent years. In September 2024, the SEC charged eleven institutional investment managers with failing to report certain securities holdings. The charges covered a range of filer types and failure patterns, including both complete non-filing and the omission of specific required securities from otherwise filed reports.

The consequences of failing to file or filing inaccurate Form 13Fs include:

Civil monetary penalties. Under Section 21(d)(3) of the Exchange Act, the SEC can seek civil monetary penalties for violations of Section 13(f). The penalty amounts depend on the nature of the violation, whether it was negligent or intentional, and whether the manager cooperated with the SEC's investigation.

Cease-and-desist proceedings. The SEC can bring administrative proceedings to require a manager to cease and desist from future violations and to comply with existing obligations. These proceedings are public and appear in the SEC's EDGAR enforcement action database.

Reputational consequences. Form 13F enforcement actions are publicly announced and remain part of the SEC's enforcement record. For investment advisers registered with the SEC, an enforcement action may trigger disclosure obligations on Form ADV and may affect the adviser's regulatory relationship with the SEC.

The no-extension rule. Unlike Form 10-Q, for which a manager can file Form 12b-25 to request a five-business-day extension, there is no extension mechanism for Form 13F. The SEC does not grant extensions and expects late filers to file as promptly as possible after the deadline.

According to Nixon Peabody's FAQ on Form 13F enforcement, as the SEC ramps up enforcement actions related to Form 13F filing obligations, investment managers must assess their holdings against the SEC's reporting thresholds and ensure that their compliance programmes are calibrated to identify when the $100 million threshold is crossed, including mid-year threshold crossings that occur on the last trading day of any month.

What Else Must a Form 13F Filer Do?

Form 13F filers have two related obligations that arise from the Form 13F filing requirement and are worth addressing together.

Form N-PX. Any investment adviser with an obligation to file Form 13F must also file Form N-PX, an annual report of proxy votes. Form N-PX is due by August 31 of each year and covers the 12-month period ending June 30 of that year for say-on-pay votes. A manager that first files Form 13F in a given calendar year must file its initial Form N-PX no later than August 31 of the following calendar year. A manager that ceases to be a Form 13F filer must file a final Form N-PX by March 1 of the calendar year following its final Form 13F filing. The scope of Form N-PX reporting was expanded in 2024 to cover a broader range of votes, and managers should confirm their Form N-PX reporting addresses the current requirements.

Form SHO. Rule 13f-2, which establishes short sale reporting obligations for institutional managers, requires managers to report short positions on a monthly basis on new Form SHO. After a one-year exemption granted in February 2025, the initial Form SHO filing was due February 17, 2026, for the January 2026 reporting period. Unlike Form 13F, which covers long equity positions, Form SHO covers short positions meeting applicable thresholds. Managers that file Form 13F should confirm whether they also have Form SHO obligations under Rule 13f-2.

Shared discretion coordination. Where two managers share investment discretion over the same account or securities, both may have independent filing obligations. The SEC's guidance allows an authorised officer of one manager to file on behalf of both, provided the filing is identified as covering both managers and the shared discretion relationship is disclosed. Managers in this situation should document which entity is the filing entity and confirm that the filing covers all securities for which each manager has discretion.

Frequently Asked Questions

What is Form 13F and who must file it?

Form 13F is a quarterly disclosure form filed with the SEC by institutional investment managers that exercise investment discretion over $100 million or more in Section 13(f) securities. The $100 million threshold is assessed on the last trading day of any month of a calendar year. Once crossed, the obligation triggers for the current year and continues through at least the third calendar quarter of the following year. Filers include investment advisers, hedge funds, banks, insurance companies, broker-dealers, pension funds, and corporations, including those headquartered outside the United States.

What is the Form 13F filing deadline?

Form 13F must be filed within 45 calendar days after the end of each calendar quarter. For 2026, the four filing deadlines are February 17, May 15, August 14, and November 16. When the 45th day falls on a weekend or federal holiday, the deadline moves to the next business day. The SEC does not grant extensions. There is no Form 13F equivalent of Form 12b-25.

What securities must be reported on Form 13F?

Only Section 13(f) securities must be reported. These are securities that appear on the SEC's official Section 13(f) securities list, which is published quarterly. The list includes exchange-traded U.S. equities, listed equity options and warrants, closed-end fund shares, listed convertible debt, and ADRs. Mutual fund shares, U.S. Treasuries, non-convertible bonds, and most foreign securities not listed on U.S. exchanges are not Section 13(f) securities. Individual positions of fewer than 10,000 shares and less than $200,000 in market value may be omitted from the report under the omission threshold.

What is the omission threshold for Form 13F?

A manager may omit a specific holding from its Form 13F if the position represents fewer than 10,000 shares and has a fair market value of less than $200,000, or if the position is convertible debt with a principal amount of less than $200,000. Both the share/unit count and the value threshold must be met simultaneously for the omission to apply. Note that securities subject to the omission threshold still count toward the $100 million threshold determination the omission applies only to the Information Table reporting, not to the threshold calculation.

How do you request confidential treatment for Form 13F holdings?

Confidential treatment requests must be filed electronically through EDGAR simultaneously with the public Form 13F. The request requires a cover letter explaining the factual and legal basis for confidential treatment, demonstrating that the information is customarily kept private and that disclosure would cause harm to the manager. A separate confidential Form 13F listing only the securities subject to the request must also be filed. The SEC may grant confidential treatment for up to one year for active acquisition positions and open risk arbitrage positions. Confidential treatment is not routinely granted and requires meeting a specific legal standard articulated in the 2022 rule amendments.

What happens if Form 13F is filed late or contains errors?

The SEC has increased Form 13F enforcement activity significantly, charging eleven managers with reporting failures in September 2024. Consequences include civil monetary penalties, cease-and-desist proceedings, and reputational consequences including disclosure obligations on Form ADV. No extension is available for Form 13F. A manager that discovers an error should file a Form 13F-HR/A amendment promptly. The SEC does not have a specific amendment deadline but views proactive correction more favourably than unremedied known errors.

Key Takeaways

- Form 13F is required of institutional investment managers that exercise investment discretion over $100 million or more in Section 13(f) securities, assessed on the last trading day of any month of any calendar year. Once the threshold is crossed, the obligation continues through at least the third calendar quarter of the following year regardless of whether assets subsequently fall below $100 million.

- The four 2026 Form 13F filing deadlines are February 17, May 15, August 14, and November 16. These are hard deadlines. The SEC does not grant extensions and there is no Form 13F equivalent of Form 12b-25.

- Form 13F must be filed electronically through EDGAR on Form 13F-HR. The Information Table must report fair market values rounded to the nearest dollar, following the 2022 amendments that changed the prior standard of rounding to the nearest thousand dollars.

- Section 13(f) securities are limited to the securities on the SEC's official quarterly list: exchange-traded U.S. equities, listed options and warrants, closed-end fund shares, listed convertible debt, and ADRs. Individual positions under 10,000 shares and $200,000 in value may be omitted from reporting under the omission threshold, but still count toward the $100 million filing threshold.

- Confidential treatment requests must be filed electronically through EDGAR simultaneously with the public Form 13F. The legal standard, formalised in the 2022 amendments, requires that information be customarily kept private and that disclosure would cause harm. Confidential treatment is narrow and not routinely granted.

- Form 13F filers also have Form N-PX obligations (annual proxy vote report, due August 31) and should assess whether Rule 13f-2 creates Form SHO short-position reporting obligations, with the first Form SHO due February 17, 2026 for January 2026 positions.