Choosing the wrong registration statement form is not a paperwork error. It is a filing that the SEC will reject outright or that will require extensive amendment to correct. The three most commonly confused Securities Act registration forms S-1, S-11, and S-4 each apply to distinct transaction types, carry different financial statement requirements, and generate different SEC staff comment patterns during review.

The threshold form selection decision is not typically made by the CFO or the internal finance team. It is made by outside securities counsel. But understanding why a particular form applies, what it requires, and how its review process differs from the others is operationally important for the finance and disclosure team that will spend the next several weeks or months preparing the filing. This post gives your team that understanding before the drafting process begins.

What Is the Difference Between an S-1, S-11, and S-4?

The S-1, S-11, and S-4 are all registration statements filed under the Securities Act of 1933. They register different types of securities offerings with the SEC and serve fundamentally different transaction purposes.

The S-1 is the general-purpose registration statement used for initial public offerings by domestic companies that are not registering securities of a specific type requiring a specialised form. It is the default form when no other form is prescribed by SEC rules and when the registrant has either never filed under the Securities Act or the Exchange Act, or has been in the Exchange Act reporting system for less than 12 months.

The S-11 is the specialised registration statement required for securities issued by real estate investment trusts (REITs) as defined under Section 856 of the Internal Revenue Code, or by other issuers whose business is primarily the acquisition and holding of real estate or interests in real estate for investment. It is not a form companies choose as a matter of preference. It is the form the SEC requires when the issuer qualifies as a REIT or as a real estate holding company under the applicable definition.

The S-4 is the registration statement used when securities are being issued in connection with business combinations: mergers, acquisitions where the consideration includes the acquirer's registered securities, exchange offers, and similar transactions. Its defining characteristic is that it combines Securities Act registration obligations with proxy statement or information statement disclosure requirements, serving both the shareholders of the issuer being absorbed into the transaction and the investors who will receive new securities as consideration.

The most practical way to understand the three forms is by the question each one answers for an investor. The S-1 answers: should I invest in this company at this offering price in this IPO? The S-11 answers: should I invest in this REIT or real estate holding company at this offering price? The S-4 answers: should I vote in favour of this merger or exchange offer, and do I want to hold the acquirer's shares that I will receive if the transaction closes?

Each answer requires different information, different financial statements, and different SEC staff review focus.

When Do You Use an S-1 Filing?

The S-1 is used when a domestic company is conducting an initial public offering and is not a REIT, not a foreign private issuer, and is not registering securities in connection with a business combination. It is the most common registration statement form for US IPOs across all industries except real estate.

Beyond the traditional IPO, the S-1 is also used in three additional situations that are frequently encountered by established companies.

**First S1 or less than 12 months of Exchange Act reporting. **A company that has never filed with the SEC under either the Securities Act or the Exchange Act must use the S-1 for its initial registration. A company that has been in the Exchange Act reporting system for less than 12 months is also required to use the S-1 rather than the more streamlined S-3 form, even if it is not conducting a traditional IPO.

SPAC IPOs. Special purpose acquisition companies (SPACs) file their initial IPO registration statement on Form S-1. The SEC has specific disclosure requirements for SPACs under Items 1602 and 1603 of Regulation S-K, which must be included in any S-1 filed for a SPAC offering that is not in connection with a de-SPAC transaction. The de-SPAC transaction itself, when the SPAC merges with a target company, is typically registered on Form S-4 rather than Form S-1.

Follow-on offering before S-3 eligibility. A newly public company that wants to register additional shares for sale before it becomes S-3 eligible (which generally requires 12 months of Exchange Act reporting and timely filing of all required reports) must use the S-1 for its follow-on offering. S-3 eligibility allows companies to use a more streamlined short-form registration statement that incorporates prior filings by reference. Until that eligibility is established, the S-1 is the only option.

The S-1 does not permit forward incorporation by reference in most circumstances, which means the prospectus must contain all required disclosure within the four corners of the document rather than pulling in Exchange Act reports by reference. This makes the S-1 a longer and more detailed document than the forms available to seasoned registrants.

According to the SEC's Division of Corporation Finance guidance on registration forms, the S-1 is the appropriate form when no other Securities Act registration statement form is prescribed and the issuer does not qualify for a specialised or short form. For domestic operating companies conducting an IPO, this means the S-1 is the default choice in the overwhelming majority of cases.

When Do You Use Form S-11 Instead of an S-1?

The S-11 applies when the issuer is a real estate investment trust as defined in Section 856 of the Internal Revenue Code, or when the issuer's business is primarily the acquisition and holding of real estate or interests in real estate for investment purposes. The form is not optional for issuers that meet this definition. An entity that qualifies as a REIT and attempts to register its securities using Form S-1 will be required by the SEC to refile on the correct form.

The distinction between an S-1 and an S-11 is not simply about what the company owns. It is about what the company's primary business activity is. A technology company that owns its office building is not a real estate holding company. A company whose business is acquiring commercial properties and leasing them to tenants where rental income is the primary revenue stream and asset management decisions are the primary operational activity is a real estate holding company within the meaning of the S-11 rule.

The S-11 has several disclosure requirements that differ meaningfully from the S-1, reflecting the particular investment analysis that real estate securities require.

**Property specific financial disclosure. **The S-11 requires disclosure of operating data for each property or group of properties the issuer has acquired or proposes to acquire, to the extent the acquisition represents a significant portion of total assets. This is analogous to the Rule 3-14 financial statement requirements of Regulation S-X, which require audited financial statements of real estate operations acquired above significance thresholds. A REIT conducting an IPO that has recently acquired significant properties must include separate financial statements for those acquisitions in the S-11, in addition to the REIT's own consolidated financial statements.

Investment policy disclosure. The S-11 specifically requires disclosure of the issuer's policies with respect to certain types of investment activities, including policies on leveraging, dispositions, investments in other companies, and changes to investment policies that can be made without shareholder approval. These items are S-11-specific and are not required in an S-1.

REIT qualification and tax disclosure. Because a REIT's tax status under Section 856 of the Internal Revenue Code is central to its investment value (REIT distributions are often tax-advantaged), the S-11 requires specific disclosure about the issuer's REIT qualification status, the opinion of tax counsel regarding REIT qualification, and the risks to REIT status if applicable. This disclosure is a standard S-11 item with no equivalent in the S-1.

Non-GAAP metrics specific to real estate. REITs routinely use non-GAAP financial measures that are industry-specific: Funds From Operations (FFO), Adjusted Funds From Operations (AFFO), Net Operating Income (NOI), and same-store NOI growth. These measures are not prohibited by SEC rules but they are subject to the same non-GAAP prominence and reconciliation requirements that apply to any non-GAAP measure in any registration statement. SEC staff reviewing S-11 filings are familiar with these metrics and focus on whether they are presented with adequate GAAP reconciliation and with GAAP metrics given equal or greater prominence.

According to the SEC's Form S-11 instructions, the form cannot be used by issuers that are investment companies registered or required to register under the Investment Company Act of 1940, or for offerings of asset-backed securities. REITs that are structured as mortgage REITs holding mortgage-backed securities rather than physical real estate should confirm with securities counsel whether the S-11 or an alternative form is appropriate for their specific structure.

The SEC staff review of an S-11 is conducted by the Real Estate industry group within the Division of Corporation Finance, which brings specific expertise in REIT accounting, FFO disclosure, Rule 3-14 financial statement requirements, and the investment policy disclosures that distinguish S-11 review from S-1 review.

When Do You Use a Form S-4?

The S-4 is the registration statement for securities issued in business combinations. If a company is acquiring another company and paying for some or all of that acquisition with its own registered securities, those securities must be registered before they can be issued to the target company's shareholders. The vehicle for that registration is the S-4.

The S-4 is simultaneously a Securities Act registration statement and a proxy statement or information statement. The Securities Act component registers the acquirer's securities that will be issued in the transaction. The proxy or information statement component gives the target company's shareholders the information they need to vote on the merger or exchange offer. This dual purpose is what makes the S-4 the most complex registration statement form in common use.

The S-4 is used in four primary transaction structures.

Stock-for-stock mergers. When the acquirer pays for a merger entirely or substantially with its own equity securities, those shares must be registered on Form S-4. The S-4 in this context functions as both the merger registration statement and the merger proxy. It must be declared effective by the SEC before shareholder votes can be solicited.

Exchange offers. When a company makes an offer directly to the shareholders of a target company to exchange the target's shares for the acquirer's shares, the acquirer registers the securities to be issued in the exchange offer on Form S-4. The S-4 is filed as the offering document and must be declared effective before the exchange offer can commence.

SPAC de-SPAC transactions. When a SPAC completes its business combination with a target company and issues new shares to the target's shareholders, the transaction is registered on Form S-4 rather than Form S-1. The S-4 in this context includes the SPAC's proxy statement for the shareholder vote on the business combination and registers the shares to be issued to the target's equityholders.

Debt exchange offers and recapitalisation transactions. When a company offers to exchange existing debt securities for new debt or equity securities, the new securities are registered on Form S-4. This use is less common than equity transaction S-4s but follows the same basic structure.

The financial statement requirements of the S-4 are more complex than either the S-1 or the S-11. The S-4 must include financial statements of the acquirer and, in most cases, financial statements of the target company (the number of years required depends on the target's significance to the acquirer under the Rule 3-05 significance tests). It must also include pro forma combined financial statements prepared under Article 11 of Regulation S-X, showing what the combined entity's financial results would have looked like had the transaction occurred at the beginning of the prior fiscal year. The preparation of these pro forma statements is one of the most technically demanding aspects of S-4 preparation and is consistently the highest-volume SEC comment category in S-4 filings.

How Do the Financial Statement Requirements Differ Across the Three Forms?

The financial statement differences across the three forms reflect the different investment decisions each registration statement supports. Understanding these differences before the drafting process begins is essential for planning the financial statement preparation timeline accurately.

S-1 financial statements. The S-1 requires audited financial statements of the registrant covering the most recent two completed fiscal years for EGCs (emerging growth companies with annual gross revenues below $1.235 billion) and three completed fiscal years for non-EGCs. Interim financial statements (unaudited) are required for any interim period completed since the most recent audited year-end if the registration statement is filed or effective more than 134 days after that year-end. The financial statements must comply with US GAAP and must reflect accounting standards as they apply to public business entities, not private company alternatives. This requirement most commonly affects EGCs that applied private company effective dates for ASC 842 (Leases) or other recent standards.

S-11 financial statements. The S-11 requires the same base financial statements as the S-1 for the issuer itself, but adds the Rule 3-14 financial statements for significant real estate acquisitions. Under Regulation S-X Rule 3-14, if a REIT has acquired or proposes to acquire real estate operations above the significance threshold (20% significance under the amended rules), audited financial statements of those acquired properties and pro forma financial information must be included in the S-11. The significance calculation for real estate acquisitions uses the purchase price as a substitute for total assets when calculating the investment test, which is specific to real estate and differs from the Rule 3-05 methodology used for non-real estate acquisitions. The interaction between the issuer's own financial statements, the Rule 3-14 property financial statements, and the required pro forma presentation makes S-11 financial statement preparation among the most operationally complex of any registration statement type.

S-4 financial statements. The S-4 requires audited financial statements of the acquirer covering the required periods (two years for EGCs, three years for non-EGCs), audited financial statements of the target company covering the required periods under the Rule 3-05 significance tests, and pro forma combined financial statements under Article 11 of Regulation S-X. The pro forma statements are the defining complexity of S-4 financial statement preparation. They must reflect all acquisition-date fair value adjustments, exclude non-recurring transaction costs from the pro forma income statement, limit synergy adjustments to those that are factually supportable, and be presented at both the income statement level (as if the transaction occurred at the beginning of the prior fiscal year) and the balance sheet level (as of the most recent balance sheet date). Each of these requirements is a potential SEC comment trigger, and the pro forma financial statements are consistently the most commented section of any S-4 filing.

According to the SEC's Financial Reporting Manual, the financial statement requirements for each form are determined by the registrant's filer status (EGC, accelerated filer, large accelerated filer, smaller reporting company) and by the significance of any acquisitions included in the registration statement. Teams should confirm the applicable filer status and significance calculations with their external auditors at the outset of registration statement preparation rather than discovering a requirement gap late in the drafting process.

How Does the SEC Review Process Differ for Each Form?

The SEC's Division of Corporation Finance reviews all three forms, but the review focus, the industry group assigned, and the typical comment profile differ meaningfully across form types.

S-1 review. The S-1 is assigned to the CorpFin industry group matching the registrant's primary business sector: Technology, Healthcare, Finance, Consumer Products, and so on. The staff reviewing an S-1 bring sector-specific knowledge of what the business model looks like and what adequate disclosure for that sector includes. SEC staff have 30 calendar days to complete their initial review of a publicly filed S-1. Virtually all S-1s receive at least one comment letter. The most common comment areas are generic risk factors, MD&A sections that describe rather than analyse results, non-GAAP measures that violate the equal prominence or reconciliation rules, and financial statements that do not reflect public company accounting standards.

S-11 review. The S-11 is assigned to the Real Estate industry group, which brings specific expertise in REIT accounting, Rule 3-14 financial statements, FFO and NOI presentation, and the investment policy and property disclosure requirements specific to the form. S-11 comment letters frequently address the adequacy of Rule 3-14 financial statements for significant acquisitions, the presentation of non-GAAP real estate metrics (particularly FFO, AFFO, and NOI) relative to GAAP metrics, and the specificity of REIT qualification risk factor disclosure. A company that attempts to file its REIT IPO on Form S-1 rather than Form S-11 will receive a comment directing it to refile on the correct form as the first substantive item in the comment letter.

S-4 review. The S-4 is assigned to the industry group corresponding to the acquirer's primary business sector, but the review focus is heavily weighted toward the transactional disclosure: the background of the merger narrative, the fairness opinion description, the pro forma financial statements, the target financial statements and their compliance with applicable accounting standards, and the related party disclosures. The S-4 review is mandatory before effectiveness (unlike S-1 reviews, which occur after the filing is publicly available), which means comments must be resolved before the transaction can close. This creates direct transaction execution risk from extended comment letter cycles. SEC staff reviewing S-4s have 30 days to complete initial review, but complex transactions with extensive pro forma statements often generate comment letters near the 30-day mark and require multiple rounds of response before the filing is cleared for effectiveness.

How Do SEC Comment Patterns Differ Across S-1, S-11, and S-4 Filings?

The practical value of understanding the differences between the three forms is understanding what SEC staff will focus on when reviewing each. Comment patterns by form type are the most actionable intelligence available to a disclosure team preparing a registration statement.

S-1 comment patterns cluster around five areas: financial statements reflecting private company rather than public company standards, risk factors that are generic rather than company-specific, MD&A that describes results without explaining the business reasons behind them, non-GAAP measures that violate the equal prominence or reconciliation rules, and dilution calculations that are incomplete or incorrectly calculated. These five patterns are consistent across industries and across company sizes. The variation is in which comment area generates the most rounds of back-and-forth for any specific company. For technology companies with complex revenue recognition, ASC 606 disclosure is frequently the deepest comment area. For pre-profit companies, the liquidity and going concern analysis in the MD&A draws more attention.

S-11 comment patterns are distinct from S-1 patterns in three key ways. The Rule 3-14 financial statement requirement for significant real estate acquisitions is an S-11-specific comment area with no S-1 equivalent. The REIT-specific non-GAAP metrics (FFO, AFFO, NOI) generate comment activity around prominence and reconciliation that differs from the standard Adjusted EBITDA comments common in S-1 filings. The investment policy and property disclosure requirements of the S-11 produce comment letters addressing the specificity and completeness of disclosures that have no equivalent in an S-1.

**S-4 comment patterns ** are driven by the combination of transactional disclosure and financial statement complexity that defines the form. The highest-volume comment areas are pro forma financial statement completeness under Article 11 of Regulation S-X, the background of the merger narrative, fairness opinion methodology description, related party interest disclosure, and the target company's financial statements including their compliance with applicable accounting standards. S-4 comment patterns differ from S-1 patterns not just in subject matter but in consequence: because the S-4 must be effective before the transaction can close, each comment round directly extends the transaction timeline.

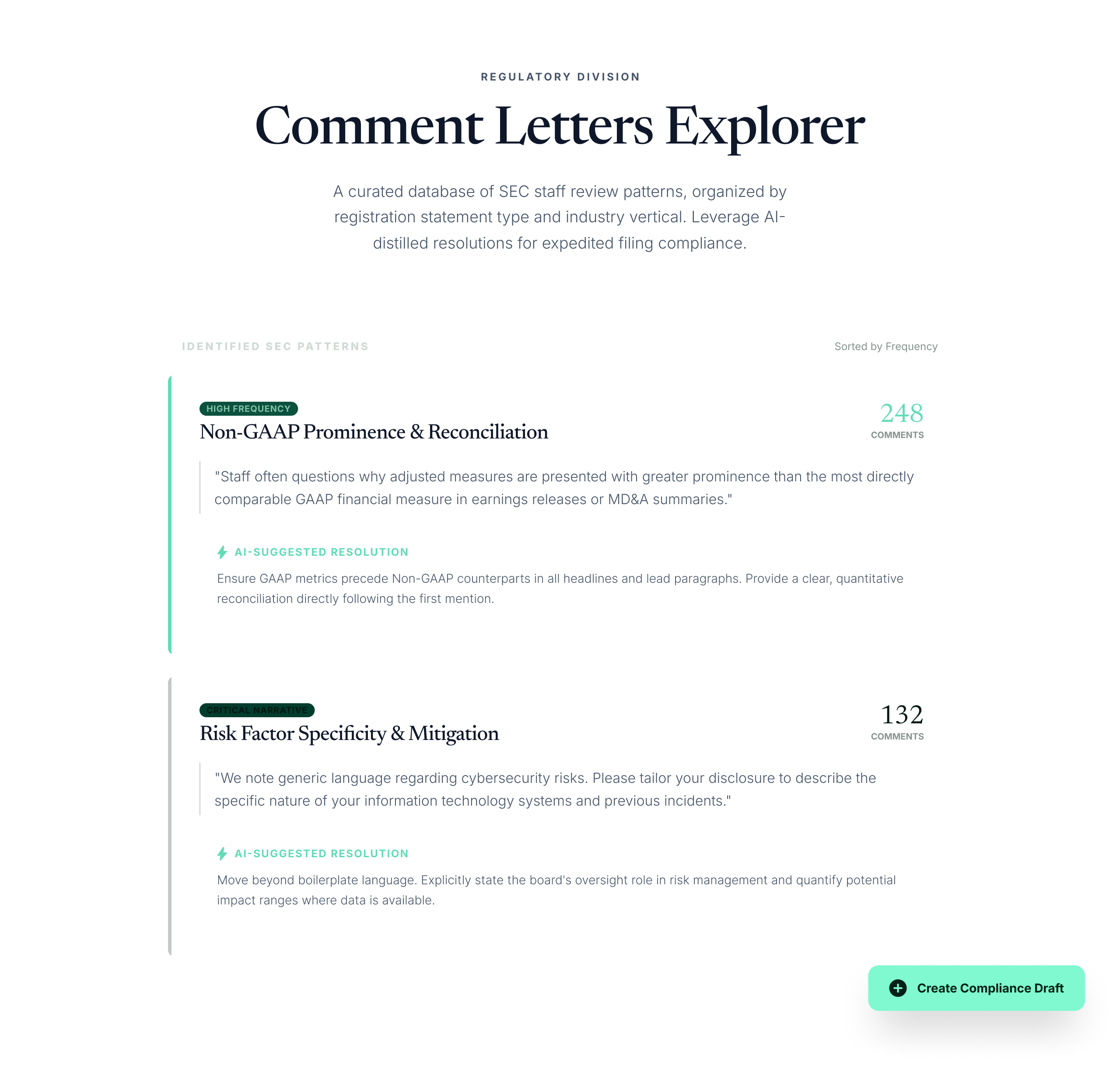

Finrep's Comment Letters Explorer filters the EDGAR comment letter archive by registration statement type, allowing your team to research S-1, S-11, and S-4 comment patterns separately. When your team is preparing a specific form, filtering Comment Letters Explorer by that form type and by your industry gives you the most precise available picture of what SEC staff will ask before you file.

The research that matters most is not the general list of common comment areas. It is the specific comment language that staff have used in your sector, for your transaction type, in the most recent filing cycle. That research, done before drafting begins rather than after the first comment letter arrives, is what allows your team to produce a first filing that resolves in one or two rounds rather than three or four.

Which Form Should Your Team File? A Decision Framework

The form selection decision follows a specific sequence of questions. Working through them in order produces the correct answer for virtually every domestic issuer.

Step 1: Is the issuer a REIT or a real estate holding company?

If yes, the form is S-11. This is not a discretionary choice. The SEC requires that REITs and real estate holding companies (whose business is primarily acquiring and holding real estate for investment) use Form S-11 for their Securities Act registration. Attempting to use Form S-1 will result in a comment directing you to refile on Form S-11.

If no, proceed to Step 2.

Step 2: Is the offering in connection with a business combination?

If the registrant is issuing its securities as consideration in a merger, acquisition, exchange offer, or similar business combination, the form is S-4. The S-4 requirement applies whenever the Securities Act registration obligation arises from the issuance of securities as consideration in a business combination, including de-SPAC transactions where the SPAC issues shares to the target company's equityholders.

If no, proceed to Step 3.

Step 3: Has the issuer been in the Exchange Act reporting system for at least 12 months with timely filings?

If yes, the issuer may be eligible to use Form S-3, the short-form registration statement available to seasoned registrants. S-3 eligibility requires 12 months of timely Exchange Act reporting, no default on financial obligations since the last audited balance sheet date, and an aggregate market value of securities held by non-affiliates of at least $75 million for primary offerings (or the use of Rule 415 for shelf offerings). If S-3 eligibility is confirmed, the registrant should use S-3 rather than S-1 for efficiency.

If no, or if S-3 eligibility is not confirmed, the form is S-1.

The foreign private issuer parallel. This decision framework applies to domestic registrants. Foreign private issuers follow a parallel framework using F-1 (equivalent to S-1), F-4 (equivalent to S-4 for business combinations), and in some cases Form 20-F for annual reports that also function as registration statements. The analysis is similar in structure but different in regulatory detail. FPIs should confirm form eligibility with their securities counsel before filing.

According to the SEC's forms index, the complete list of available registration statement forms and their eligibility requirements is maintained on the SEC's website. The forms index is the authoritative reference for confirming which form applies to any specific transaction.

Frequently Asked Questions

What is the difference between Form S-1, S-11, and S-4?

The S-1 is the general-purpose IPO registration statement used by domestic companies that are not REITs and are not registering securities in connection with a business combination. The S-11 is the specialised registration statement required for REITs and real estate holding companies whose business is primarily acquiring and holding real estate for investment. The S-4 is the registration statement used when securities are issued as consideration in mergers, exchange offers, de-SPAC transactions, and similar business combinations. Each form serves a different transaction type and carries different financial statement and disclosure requirements.

Can a REIT file on Form S-1 instead of Form S-11?

No. REITs and issuers whose primary business is acquiring and holding real estate for investment are required to use Form S-11 for their Securities Act registration. The SEC will not accept an S-1 filing from an issuer that qualifies for S-11. A REIT that attempts to file on Form S-1 will receive a comment letter directing it to refile on Form S-11 as the first item in the comment letter. The SEC's Form S-11 is designed specifically for real estate securities and includes disclosure requirements, including Rule 3-14 financial statements and investment policy disclosures, that have no equivalent in Form S-1.

When does a SPAC use Form S-1 versus Form S-4?

A SPAC uses Form S-1 for its initial IPO, when it is raising capital from investors to pursue an acquisition. It uses Form S-4 for the de-SPAC business combination transaction, when it merges with a target company and issues new shares to the target's equityholders. The S-4 in the de-SPAC context includes both the Securities Act registration of the shares being issued to the target's shareholders and the proxy statement disclosure required for the SPAC shareholder vote on the business combination.

How long does SEC review of an S-4 take compared to an S-1?

Both the S-4 and S-1 are subject to a 30-calendar-day initial review deadline. The critical difference is that the S-4 review is mandatory before effectiveness, which means comments must be resolved and the registration statement must be declared effective before the transaction can close. An S-1 is already publicly available when SEC staff review it. An S-4 must be cleared before it becomes effective. This makes comment letter delays in S-4 review directly consequential for the transaction timeline in a way that S-1 delays are not. For complex S-4 filings with extensive pro forma statements and detailed target company financial statements, two to three rounds of comments and a review period of two to four months is not uncommon.

What are the most common SEC comment areas for each form type?

S-1 comments cluster around generic risk factors, MD&A analysis quality, non-GAAP measure presentation, and financial statements reflecting private rather than public company standards. S-11 comments focus on Rule 3-14 financial statements for significant real estate acquisitions, REIT-specific non-GAAP metric presentation (FFO, NOI, AFFO), and investment policy and property disclosure completeness. S-4 comments concentrate on pro forma financial statement completeness under Article 11 of Regulation S-X, merger background narrative, fairness opinion description, and target company financial statement adequacy.

How do I research SEC comment patterns for my specific form type and industry?

The SEC publishes all comment letters and company responses on EDGAR in the CORRESP and UPLOAD filing types. You can search by company name, SIC code, or filing type to find comment letter correspondence for companies comparable to yours. For S-1 comment research, filter EDGAR full-text search by CORRESP form type, date range, and topic. Finrep's Comment Letters Explorer allows your team to filter specifically by registration statement type (S-1, S-11, S-4) and by industry, returning structured results that show what SEC staff asked, how companies responded, and what disclosure resolved each comment.

Key Takeaways

- The S-1, S-11, and S-4 are not interchangeable. Each applies to a specific transaction type and is required for that type. Using the wrong form will result in SEC comments directing you to refile on the correct form, delaying the transaction.

- Form S-1 is the default IPO registration statement for domestic companies that are not REITs and are not registering securities in connection with a business combination. It requires full financial statements and does not allow forward incorporation by reference in most circumstances.

- Form S-11 is required for REITs and real estate holding companies. It adds REIT-specific disclosure requirements including Rule 3-14 financial statements for significant acquisitions, investment policy disclosure, and REIT qualification and tax disclosure that have no equivalent in the S-1.

- Form S-4 is required when securities are issued as consideration in a business combination. It combines Securities Act registration with proxy or information statement disclosure. Its review is mandatory before effectiveness, creating direct transaction execution risk from extended comment letter cycles.

- The SEC comment patterns for each form type differ meaningfully. Understanding which patterns apply to your form before drafting begins is the most effective way to reduce comment letter rounds and timeline risk.

- Finrep's Comment Letters Explorer filters EDGAR comment letter correspondence by registration statement type, allowing your team to research the specific comment patterns that apply to your form and industry before the first draft is complete.

Request access to Finrep's Comment Letters Explorer with registration statement type filters

Finrep is an AI-powered financial disclosure intelligence platform for the Office of the CFO. 40 purpose-built AI agents for SEC reporting, technical accounting, investor relations, legal counsel, and disclosure committee functions. SOC2 Type II and ISO 27001 certified. Zero data residency. Backed by Accel. Trusted by CFO teams at FOX, Roku, HP, RingCentral, Wells Fargo, and Infosys.