Virtually every S-1 registration statement receives SEC staff comments. That is not a sign that something went wrong. It is the nature of the S-1 review process. The question is not whether comments will arrive but how many, how substantive, and how long it takes to resolve them.

The teams that move through the SEC review process fastest are not the ones with the longest prospectuses or the most experienced bankers. They are the ones who understood, before they filed, exactly what SEC staff would be looking for in each section, what the most common comment triggers are, and what documentation and disclosure depth resolves those comments in a single round.

This post maps the S-1 filing process from first principles through the top five comment patterns IPO teams encounter, in the sequence your team will encounter the questions. For each section, you will find what the requirement actually is, where teams consistently fall short, and what good looks like.

What Is an S1 Filing?

An S-1 is a registration statement filed with the SEC under the Securities Act of 1933. It is the primary disclosure document required before a company can offer securities to the public in an initial public offering. The S-1 is the legal and financial record that gives investors the information they need to make an informed decision about whether to invest in the offering.

The S-1 is not simply a company overview or a pitch deck in regulatory format. It is a binding legal document in which every material statement must be accurate, complete, and not misleading at the time of effectiveness. Misstatements or omissions in an S-1 can create liability for the issuer, its officers, its directors, and its underwriters under Section 11 of the Securities Act. That liability framework is why the SEC review process is rigorous and why the disclosure standards are high.

The S-1 is reviewed by the SEC's Division of Corporation Finance (CorpFin), which assigns the filing to the industry group whose sector best matches the registrant's primary business. Technology companies are reviewed by the Technology industry group. Healthcare companies by the Healthcare and Insurance group. Financial services companies by the Finance group. Each group develops sector-specific knowledge about common disclosure issues, and their comment letters reflect that knowledge. A technology company's S-1 will be reviewed by staff who have read thousands of technology S-1s and who know exactly what a thorough disclosure looks like for a SaaS revenue model or a platform business.

According to the SEC's Division of Corporation Finance overview, the purpose of the S-1 review is to ensure investors receive accurate, complete, and non-misleading disclosure. The SEC does not evaluate whether the offering is a good investment. It evaluates whether investors have been given what they need to make that judgment themselves.

What Does an S1 Filing Need to Include?

The S-1 follows a defined structure governed by Regulation S-K (for non-financial disclosure) and Regulation S-X (for financial statements). Understanding what each part requires before drafting begins is what separates teams that produce a complete first filing from those who spend two rounds of comments filling gaps that should not have existed.

The S-1 is organised into a prospectus and exhibits. The prospectus is the disclosure document investors read. The exhibits include the material agreements, certificates of incorporation, equity compensation plans, and other documents referenced in the prospectus.

Cover page and summary. The cover page identifies the issuer, the securities being offered, the proposed offering price range (or a statement that it will be determined by the market), the underwriters, and the use of proceeds. The prospectus summary immediately follows and must give investors a concise picture of the company, the offering, and the risk factors. The summary is not required to be comprehensive but it must identify what is most significant about the offering. SEC staff frequently comment on summaries that are too long, too repetitive of information in the body, or that fail to highlight the most material risks in plain language.

Risk factors. The risk factors section is one of the most intensively reviewed parts of any S-1. It must disclose all material risks to the business and the investment. The SEC requires that risk factors be specific to the company, not generic. A risk factor that could apply to any company in any industry without modification will generate a comment asking for greater specificity.

**Business description. ** The business section describes the company's products or services, its competitive position, its strategy, its customers, and its intellectual property. It must be factually accurate and consistent with everything else in the filing. Statements in the business section that are not supported by disclosed financial data or that conflict with the MD&A analysis are a standard comment trigger.

Management's Discussion and Analysis (MD&A). The MD&A is the most analytically demanding section of the S-1. It requires management to explain the results of operations, identify the key drivers of revenue and profitability, discuss known trends and uncertainties, and provide a liquidity and capital resources analysis. More than any other section, the MD&A is where SEC staff assess whether the disclosure is analytical or merely descriptive.

Financial statements. The S-1 must include audited financial statements for the required number of fiscal years depending on the company's filer status. Most IPO registrants must include two years of audited income statements and three years of audited balance sheets, though emerging growth companies (EGCs) may include only two years of audited financial statements in some circumstances. The financial statements must comply with US GAAP for domestic registrants, or IFRS as issued by the IASB for foreign private issuers that elect IFRS reporting.

Use of proceeds. The S-1 must disclose how the company intends to use the net proceeds of the offering. Vague descriptions of intended use, such as "general corporate purposes" without any further specificity, will generate a comment asking for more detail when the amounts involved are material.

Dilution. The S-1 must present a dilution table showing the difference between the public offering price per share and the net tangible book value per share after the offering. This table is a frequent source of SEC comments, particularly around the treatment of options, warrants, and convertible securities in the dilution calculation.

Executive compensation. The executive compensation section must disclose the compensation of the named executive officers (NEOs) for the required periods, including base salary, bonus, equity awards, and other components. Pre-IPO companies frequently underestimate the disclosure depth required here because their historical compensation practices were not designed with public company disclosure standards in mind.

According to the SEC's plain English disclosure guidelines, every section of the S-1 must be written in plain English, using short sentences, active voice, and everyday language. Legal and technical jargon should be avoided or defined.

How Long Does SEC Review of an S1 Take?

The SEC has 30 calendar days to complete its initial review of a publicly filed S-1 registration statement. In practice, the staff almost always issues a comment letter within 25 to 30 days of the filing date. Once the comment letter is issued, the clock stops. The SEC does not have a prescribed deadline for completing subsequent rounds of review, but staff typically respond to each amendment within 10 to 30 days of receipt.

The total time from first filing to SEC effectiveness depends on two variables: the number of comment rounds and the time the company takes to respond to each round. For a well-prepared S-1 with a strong disclosure team, one to two comment rounds and a total review period of six to twelve weeks is achievable. For a filing with significant disclosure gaps in multiple sections, three or more comment rounds and a review period of four to six months is not uncommon. In extreme cases, particularly where financial statement issues require amendment and re-audit, the process can extend further.

The 2025 expansion of the SEC's confidential submission process, announced in the SEC's March 2025 guidance, changes the practical timing for many IPO teams. Under the expanded policy, all issuers not just first-time registrants or EGCs can submit a draft registration statement for confidential, non-public staff review prior to any public filing. This means IPO teams can now receive and resolve one or more rounds of SEC comments before the filing ever becomes public, significantly compressing the visible timeline between public filing and effectiveness.

The 30-day review clock runs from the date of the public filing, not from the date of the confidential submission. Companies that use the confidential submission process effectively arrive at their public filing with a pre-cleared draft that has already addressed the most significant SEC staff concerns. For most IPO teams, this is the most underutilised efficiency in the IPO process.

Can You File an S1 Confidentially Before the IPO?

Yes. As of March 2025, any company regardless of size, sector, or whether it qualifies as an emerging growth company can submit a draft registration statement for confidential, non-public SEC staff review before the S-1 is publicly filed on EDGAR.

The confidential submission process was originally created under the JOBS Act in 2012 for emerging growth companies (EGCs). EGCs are companies with total annual gross revenues of less than $1.235 billion (as adjusted) in their most recent fiscal year and that have not previously sold common equity securities pursuant to an effective registration statement. The JOBS Act allowed EGCs to submit draft S-1s confidentially to receive SEC staff feedback before going public, reducing the competitive intelligence risk of a premature public disclosure of the company's financials and strategy.

In 2017, the SEC extended this option to all companies for their IPO registration statements. The March 2025 guidance expanded it further, removing the prior limitation that confidential submission was only available for initial filings. All issuers can now submit any Securities Act or Exchange Act registration statement confidentially, regardless of whether they are first-time registrants.

The practical requirements for the confidential submission process are straightforward. The draft must be submitted in text-searchable PDF format through the SEC's secure submission system. The transmittal letter must identify the issuer, the type of offering, and whether the company qualifies as an EGC. For EGCs, the initial public filing must be made at least 15 days before the road show or, if there is no road show, at least 15 days before the registration statement's requested effective date.

For non-EGC issuers using the confidential process since the 2017 expansion, the public filing must also be made at least 15 days before the road show. The comment letters received during the confidential review period and the company's responses are subsequently made public on EDGAR, typically on the date the S-1 is declared effective or within a short period thereafter.

One important planning consideration: while the SEC staff will review a confidential submission as long as it at least complies with the financial statement requirements, submitting an incomplete or low-quality draft is counterproductive. Staff who receive a draft with significant gaps will comment extensively, creating a longer review cycle than a cleaner submission would have generated. The confidential submission should represent a serious effort at a complete and accurate filing, not a placeholder designed to start the clock.

What Are the Most Common SEC Comment Letters on S1 Filings?

Virtually all S-1 registration statements receive SEC staff comments. The question is which sections draw the most comments and why. Based on SEC staff comment letter patterns across hundreds of IPO filings accessible in the EDGAR correspondence archive, five areas generate the highest volume and most substantive comment activity.

Comment Pattern 1: Financial statements that do not reflect public company accounting standards.

The single highest-volume comment area in S-1 filings is the financial statements themselves, specifically the failure to apply accounting standards as they apply to public business entities rather than private companies.

Many pre-IPO companies have applied accounting standards using private company alternatives or effective dates that differ from public company requirements. When the S-1 is filed, those financial statements must be restated or retrospectively adjusted to reflect public company standards for all periods presented. The most common specific issues are: failure to adopt ASC 842 (Leases) on the public company effective date rather than the private company effective date, revenue recognition policies under ASC 606 that followed private company transition elections that are not available to public companies, and EPS calculations that did not apply ASC 260 (Earnings Per Share) as required for public entities.

According to the SEC's Financial Reporting Manual, Topic 10, EGCs that use private company effective dates for accounting pronouncements must disclose that fact and reassess which standards apply to their financial statements in the context of the S-1.

The practical fix: before beginning S-1 preparation, have your technical accounting team conduct a comprehensive accounting standards assessment comparing your current accounting policies against the public company requirements for all periods that will be presented in the filing. Any difference needs to be addressed and audited before the financial statements are finalised.

Comment Pattern 2: Risk factors that are generic rather than company-specific.

SEC staff consistently comment on S-1 risk factors that are written at a level of generality that provides no specific information about the risks actually facing the company. A risk factor that says "we face competition in our market" without identifying who the competitors are, what competitive advantages they hold, and how the company's competitive position could be affected is not adequate disclosure.

Staff comments on generic risk factors typically take two forms: a request to revise the risk factor to include specificity about the company's circumstances, or a request to explain why the risk factor cannot be made more specific. Both responses require significant drafting effort and can result in multiple comment rounds if the first revision is still not specific enough.

The standard for an adequate risk factor is that it should tell a reasonable investor something meaningful about the specific risk they are accepting by investing in this company. If the risk factor would be equally applicable to any company in any industry, it fails that test.

Comment Pattern 3: MD&A that describes results without explaining them.

The MD&A comment pattern in S-1s is the same as in annual reports but the stakes are higher because investors are making an initial investment decision based on the S-1 MD&A without the context of prior public filings.

Staff comment when the MD&A describes what happened to revenue or margins without explaining why. A statement that "revenue increased 45% year over year" without identifying the specific drivers, whether those drivers are sustainable, and what management expects going forward does not meet the analytical standard the SEC requires. This is not a stylistic preference. It is a regulatory requirement. The SEC's MD&A interpretive release states explicitly that the purpose of the MD&A is to give investors a view of the company through management's eyes, including insight into known trends, uncertainties, and events that could materially affect future performance.

For pre-IPO companies, the MD&A challenge is compounded by the fact that management has never written public company MD&A before. Executives who are accustomed to internal reporting that focuses on operational metrics often produce an MD&A first draft that reads like an internal management report rather than a public disclosure. The distinction is significant: internal reports can assume the reader has business context. Public MD&A cannot.

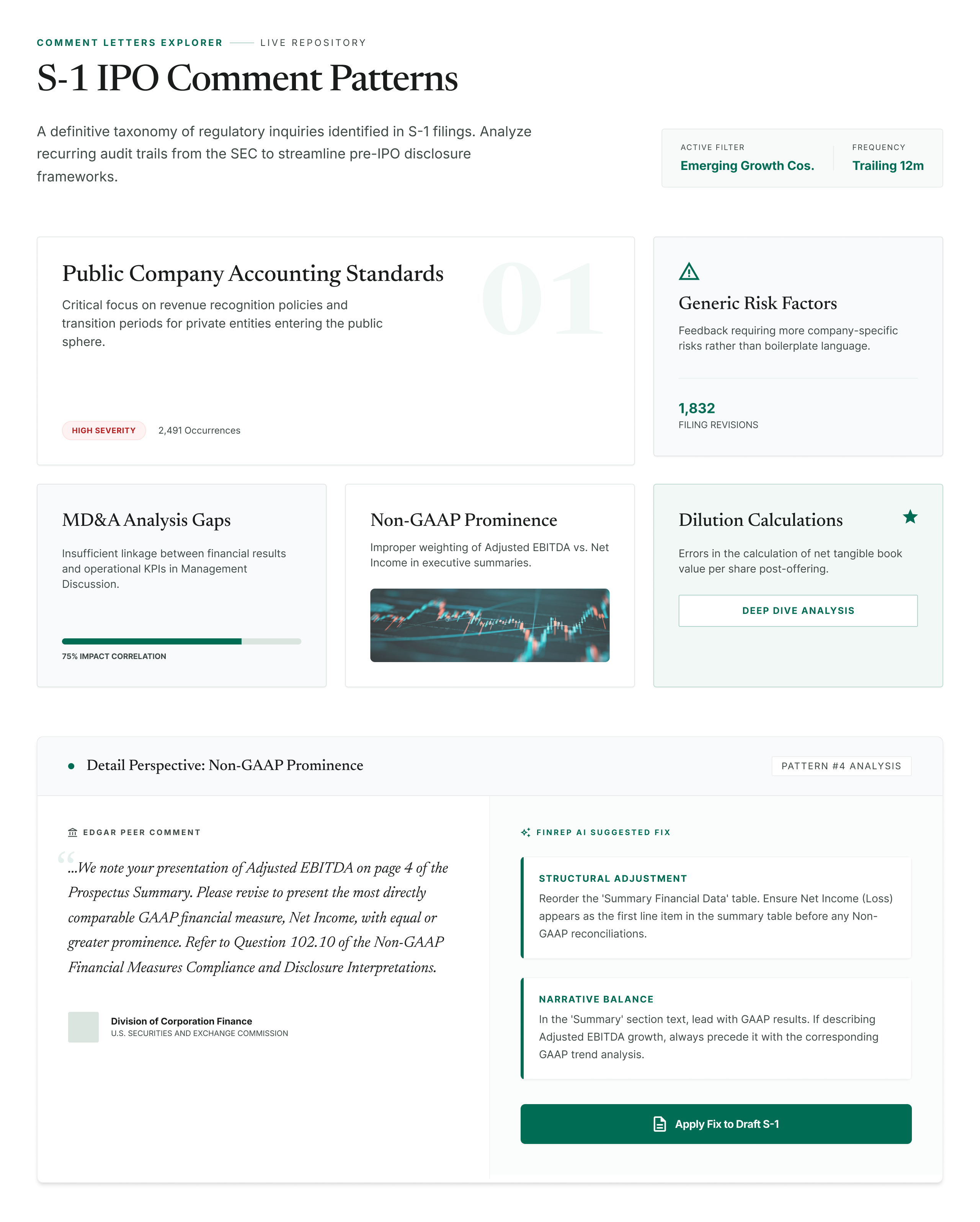

Comment Pattern 4: Non-GAAP financial measures that do not comply with SEC requirements.

Non-GAAP financial measures are common in IPO prospectuses. Adjusted EBITDA, Adjusted Operating Income, Free Cash Flow, and various sector-specific metrics (ARR, net revenue retention, gross profit excluding stock-based compensation) are routinely included in S-1 filings because they reflect how management views the business and are often the metrics the investor community uses to value companies in the sector.

The SEC's Regulation G and the C&DI guidance on non-GAAP financial measures apply to S-1 filings. The most common non-GAAP comment patterns in S-1s are: presenting non-GAAP measures more prominently than the corresponding GAAP measures, failing to include a reconciliation from the non-GAAP measure to the most directly comparable GAAP measure, excluding charges from non-GAAP metrics that recur regularly (and therefore cannot be characterised as non-recurring), and defining non-GAAP measures inconsistently across periods.

The exclusion of stock-based compensation from Adjusted EBITDA or non-GAAP operating income has been an active SEC comment focus, particularly for technology and software companies where stock-based compensation is a significant and recurring expense. Staff have questioned whether excluding SBC from non-GAAP metrics presents a misleading picture of the company's ongoing cost structure. The SEC's C&DI on non-GAAP financial measures is the authoritative reference for how these measures must be presented.

Comment Pattern 5: Dilution disclosure that is incomplete or incorrectly calculated.

The dilution section of the S-1 presents the difference between the public offering price and the post-offering net tangible book value per share. It is a section that many pre-IPO finance teams underestimate in complexity.

Common comment triggers include: the dilution calculation excludes options, warrants, or convertible securities that should be included in the calculation of shares outstanding for dilution purposes, the historical net tangible book value calculation includes or excludes items inconsistently, and the treatment of noncontrolling interests in the dilution calculation is unclear or incorrect. Staff often ask companies to reconcile specific line items in the dilution table to the financial statements to confirm consistency.

The dilution section also frequently draws comments when the implied valuation of insider shares at recent grant prices differs significantly from the IPO offering price without adequate explanation of the difference. If founders, executives, or investors received shares or options at prices substantially below the offering price in the twelve to eighteen months preceding the IPO, staff may ask the company to explain the valuation basis for those grants and why the implied valuation difference does not indicate an unrealised compensation charge.

What Do IPO Companies Get Wrong in Their S-1 Risk Factors?

Risk factors are the section where the gap between what companies produce and what SEC staff expect is widest and most consistent. Understanding the specific ways risk factor disclosures fail is the most direct path to drafting a risk factor section that does not generate multiple comment rounds.

The most common risk factor failure is the generic headline risk. A risk factor that says "we may not be able to attract and retain key personnel" without specifying which roles are critical, what the competitive market for that talent looks like, whether the company has experienced turnover in those roles, and what the consequences of losing key personnel would be on the business is a headline, not a disclosure. Every software company could copy that risk factor. That is the problem.

The second failure is the disclosure of a risk without explaining the potential magnitude of its impact. A risk factor that identifies a single customer accounting for 35% of revenue as a risk but does not explain what would happen to revenue, cash flow, and operations if that customer reduced or terminated its relationship is incomplete. Staff will ask for disclosure of the materiality of the risk, not just its existence.

The third failure is organising risk factors by category rather than by materiality. The SEC requires that risk factors be presented in order of significance to the investment decision, with the most material risks first. Companies that group risks by category (regulatory risks, market risks, operational risks) often bury their most material risks in the middle of a long section because the categorical organisation obscures the materiality ranking.

A practical test for any risk factor: can a reasonable investor read this disclosure and understand specifically what could go wrong, how likely it is, what the magnitude of the impact would be, and what the company is doing about it? If any of those four elements is missing, the risk factor is incomplete.

How Should Management Discussion and Analysis Be Written in an S1?

The MD&A in an S-1 is harder to write than the MD&A in an annual report for one reason: the reader has no prior context. In a 10-K, investors can compare this year's MD&A to last year's. In an S-1, the MD&A is often the first time investors are seeing an analytical discussion of the company's financial results. Everything must be explained from first principles.

The structure that consistently produces the most defensible and comment-resistant MD&A in S-1 filings follows a specific pattern.

Start with a business overview paragraph that gives investors the analytical frame: what drives revenue in this business, what drives costs, and what metrics matter most. This paragraph is not required by regulation but it is the context that makes everything else in the MD&A readable for an investor who is encountering the company for the first time.

For each period comparison (year over year, and in many cases quarter over quarter for the most recent interim period), explain each material change with three components: the amount of the change, the primary driver of the change, and whether the driver is expected to continue. The third component is where most first-draft MD&As fail. Describing what happened and why is description. Adding what management expects going forward is analysis.

Quantify drivers wherever possible. A statement that revenue increased due to growth in the company's enterprise customer segment is less useful than a statement that enterprise customer revenue increased 62% year over year, driven by an increase in average contract value from $85,000 to $124,000 and a 28% increase in the number of enterprise customers, partially offset by a 12% increase in churn among customers with fewer than 50 users. The second version is what SEC staff expect to see.

The liquidity and capital resources section deserves specific attention in an S-1 because it must address a question that most annual report MD&As do not face: is the company's current trajectory sustainable, and does it have sufficient capital to execute its plan? For pre-profit companies, the liquidity section must honestly address the runway question how long the company's cash will last at current burn rates, what assumptions underlie that estimate, and what the company would do if those assumptions do not hold.

What Are the Non-GAAP Financial Measure Rules for S1 Filings?

Non-GAAP measures in S-1 filings are governed by the same rules that apply to periodic reports filed by public companies: Regulation G and the SEC's C&DI guidance on non-GAAP financial measures. Two aspects of this framework are particularly important for pre-IPO companies that are applying it for the first time.

The equal or greater prominence rule requires that whenever a non-GAAP financial measure is presented, the corresponding GAAP measure must be presented with equal or greater prominence. This rule applies to tables, charts, and narrative text. A company that leads its results discussion with Adjusted EBITDA before presenting GAAP operating income violates this rule. A table that places the non-GAAP metric in the first column and the GAAP metric in a subsequent column may also violate it depending on context. The SEC's non-GAAP C&DI guidance provides specific examples of prominence violations.

The reconciliation requirement means that for every non-GAAP measure presented, a reconciliation from the most directly comparable GAAP measure must be included in close proximity to the non-GAAP measure. The reconciliation must identify each adjustment made, explain why it was made, and be mathematically complete. Reconciliations that include line items labelled "other adjustments" without further explanation will generate a comment requesting disclosure of what those items are.

The most practically important guidance for IPO companies is the SEC's position on adjustments that exclude charges that are normal to the business even if they are non-cash or non-recurring in a given period. Stock-based compensation, restructuring charges that occur across multiple periods, and acquisition costs that form part of a pattern of M&A activity have all been subjects of SEC staff comments asking companies to justify their exclusion from non-GAAP metrics.

The rule of thumb: if an adjustment would not exist but for the company's specific accounting choices or transaction history and it does not reflect an ongoing cash cost of operating the business, it is a more defensible exclusion. If the adjustment reflects an ongoing economic cost that is simply accounted for in a way the company finds inconvenient for its narrative, the exclusion is likely to draw a comment.

How Do I Respond to an SEC Comment Letter on My S1?

The comment letter response process is where IPO timelines are made or lost. Teams that respond to SEC staff comments strategically, completely, and with the right tone resolve comment letters in one or two rounds. Teams that respond defensively, partially, or with insufficient specificity extend the review process significantly.

The mechanics are straightforward. The SEC issues its comment letter within 30 days of the public filing. The company responds by filing an amendment to the S-1 (an S-1/A) that incorporates revised disclosure in response to each comment, along with a separate response letter that addresses each comment individually and cross-references the corresponding changes in the amended filing.

The most important principle in drafting a comment letter response: every comment must be addressed completely. If a staff comment requests that the company revise its disclosure to include specific information, the response must either provide that information in the amended filing or explain specifically why the information cannot be provided. A response that partially addresses a comment or that redirects the staff to a different section of the filing without making the requested disclosure will generate a follow-up comment.

On tone: staff comments are professional inquiries, not accusations. The most effective responses are equally professional, direct, and factual. Responses that argue with the staff's characterisation of the company's disclosure or that explain at length why the existing disclosure is adequate without actually making the requested change rarely succeed. If the staff has asked for additional disclosure, provide it and explain why the additional disclosure is accurate and appropriate.

On timing: the SEC does not impose a deadline on the company's response to a comment letter, but the company's internal timeline almost always does. For an IPO with an equity markets window in mind, a delayed response to a comment letter is a costly delay in the offering timeline. Responses should be drafted by a team that includes outside securities counsel, the company's finance team, and the underwriters' counsel, with a target response time of two to four weeks for most comment letters.

After each round of comments is resolved, the SEC will either issue additional comments (a second or third comment letter) or indicate that its review is complete and that the registration statement may be declared effective at the company's request. Effectiveness is the moment the S-1 becomes operative and the company can price and close its IPO.

How Do I Research What the SEC Has Commented on in Similar S1 Filings?

The SEC publishes every comment letter it sends and every company response on EDGAR. For IPO teams, this archive is the most valuable pre-filing research tool available and the most underused.

Every S-1 comment letter the SEC has sent to a company comparable to yours, in the same industry, with a similar business model, revenue profile, or capital structure, is publicly accessible in the EDGAR correspondence archive. Those letters tell you exactly what SEC staff asked, what language in the filing triggered the question, and what disclosure change resolved the comment. Reading ten to fifteen comment letter exchanges from comparable IPO companies gives your team a concrete picture of what your filing will face and how to address it before it becomes a comment.

The research question your team needs to answer before filing is not just "what are the common S-1 comment areas?" It is "what specifically has the SEC asked companies like ours, in our sector, about the same disclosure topics we are preparing?" The first question has a generic answer. The second question has a specific answer that is worth several weeks of comment letter back-and-forth if you act on it.

Finrep's Comment Letters Explorer filters the EDGAR comment letter archive for S-1-specific SEC staff comments, organised by industry, comment type, and recency. Your team searches by the disclosure section you are preparing risk factors, MD&A, non-GAAP measures, dilution, financial statements and receives a structured view of what the SEC asked comparable companies, how those companies responded, and what disclosure resolved the comment.

The five comment patterns described in this post are not theoretical. Each one is drawn from the EDGAR correspondence archive and recurs across dozens of S-1 filings in every sector. Before your team finalises each section of the S-1, running it against the Comment Letters Explorer's S-1 filter gives you the same research that a senior securities lawyer would conduct manually in two to three days, in a fraction of the time.

For IPO teams using Finrep's IPO disclosure workflow, the Comment Letters Explorer integrates directly with the disclosure drafting process. Each section of the draft is benchmarked against peer S-1 disclosures and peer comment letter history simultaneously, so gaps in disclosure depth are identified before filing rather than after the comment letter arrives.

According to Finrep client data, 2025, teams using Finrep's disclosure intelligence tools reduce their SEC reporting preparation time from 10 days to 3 to 4 days, with 60 to 70% fewer review loops with auditors. In an IPO context, where the filing timeline is fixed by the equity markets window, that time reduction directly reduces transaction risk.

Request access to Finrep's Comment Letters Explorer with S-1 filter

Frequently Asked Questions

What is an S-1 filing and when is it required?

An S-1 is a registration statement filed with the SEC under the Securities Act of 1933, required before a company can offer securities to the public in an initial public offering. The S-1 is the primary disclosure document that gives investors the information they need to make an informed investment decision. It must be filed with the SEC and declared effective before the company can price and close its IPO. All domestic companies conducting a US IPO must file an S-1 unless they qualify to use a different registration form such as the S-11 (for real estate investment trusts) or the F-1 (for foreign private issuers).

What financial statements are required in an S-1?

Most S-1 registrants must include two years of audited income statements, statements of comprehensive income, statements of cash flows, and statements of stockholders' equity, plus two years of audited balance sheets. EGCs (emerging growth companies with annual gross revenues below $1.235 billion) may in some cases include only two years of audited financial statements rather than the three years generally required. The financial statements must comply with US GAAP for domestic registrants and must reflect the accounting standards applicable to public business entities, not private company alternatives, for all periods presented.

How long does SEC review of an S-1 take?

The SEC has 30 calendar days to complete its initial review of a publicly filed S-1. Staff typically issue a comment letter within 25 to 30 days of filing. The total time from first filing to effectiveness depends on the number of comment rounds and the company's response time. A well-prepared S-1 with strong disclosure can achieve effectiveness in six to twelve weeks. Filings with significant disclosure gaps across multiple sections can take four to six months or longer. Companies using the confidential submission process can resolve one or more comment rounds before public filing, significantly compressing the visible timeline.

Can you file an S-1 confidentially before the IPO?

Yes. Since March 2025, any company can submit a draft S-1 for confidential, non-public SEC staff review before the filing becomes public on EDGAR. The confidential submission option was originally created for EGCs under the JOBS Act in 2012 and extended to all companies for IPO filings in 2017. The March 2025 expansion removed the prior limitation that it was only available for initial filings. For EGCs, the public filing must be made at least 15 days before the road show. The comment letters received during confidential review are subsequently published on EDGAR when the registration statement becomes effective.

What are the most common SEC comment letter areas for S-1 filings?

Based on EDGAR comment letter correspondence across hundreds of IPO filings, the five highest-volume comment areas are: financial statements that do not reflect public company accounting standards (particularly EGCs applying private company effective dates for new standards), risk factors that are generic rather than company-specific, MD&A sections that describe financial results without explaining the business reasons behind them, non-GAAP financial measures that violate the equal prominence rule or have incomplete reconciliations, and dilution disclosures that are incorrectly calculated or exclude securities that should be included. These five areas account for the majority of substantive S-1 comment letters across all industries.

What is the difference between an S-1 and an S-1/A?

An S-1 is the initial registration statement filed with the SEC. An S-1/A is an amendment to the S-1, filed to incorporate revisions in response to SEC staff comments, to update financial statements, or to include pricing and other offering information that was not available at the time of the initial filing. Most IPO registration statements go through at least one S-1/A before becoming effective. The pricing amendment, which adds the final offering price and related information, is typically filed as the last S-1/A immediately before the registration statement is declared effective.

Key Takeaways

- Virtually every S-1 receives SEC staff comments. The goal is not to avoid comments entirely but to minimise their number and resolve them in one or two rounds by addressing the most common comment triggers before filing.

- The five highest-volume S-1 comment areas are financial statements that do not reflect public company accounting standards, generic risk factors, descriptive MD&A, non-GAAP measures that violate the equal prominence or reconciliation rules, and dilution calculations that are incorrect or incomplete.

- The confidential submission process, expanded in March 2025 to all issuers, is the most underutilised efficiency in the IPO process. Filing a clean draft confidentially and resolving one or more comment rounds before public filing compresses the visible timeline between public S-1 filing and effectiveness.

- MD&A in an S-1 must explain the reasons behind financial results and discuss known trends and uncertainties. Description of what happened is not sufficient. Management's analytical view of why it happened and what they expect going forward is what the SEC requires and what investors need.

- Researching peer S-1 comment letters in the EDGAR correspondence archive before drafting is the most direct way to identify disclosure gaps in advance. Finrep's Comment Letters Explorer automates this research, filtering by S-1 filing type, industry, and comment category.

Request access to Finrep's Comment Letters Explorer with S-1 filter

Finrep is an AI-powered financial disclosure intelligence platform for the Office of the CFO. 40 purpose-built AI agents for SEC reporting, technical accounting, investor relations, legal counsel, and disclosure committee functions. SOC2 Type II and ISO 27001 certified. Zero data residency. Backed by Accel. Trusted by CFO teams at FOX, Roku, HP, RingCentral, Wells Fargo, and Infosys.

For further reading on SEC comment letters, see How to Use SEC Comment Letters to Audit Your Own Filings.