Section 16 of the Securities Exchange Act of 1934 is one of the most technically precise areas of SEC compliance. The reporting obligation is straightforward in principle: directors, officers, and ten percent beneficial owners of registered equity securities must disclose their holdings and transactions. In practice, the exemption framework is dense, the edge cases are numerous, and a wrong call in either direction creates a compliance problem. Claim an exemption that does not apply and you have a late Form 4. Fail to claim an exemption that does apply and you have an unnecessary filing that may expose the insider to short-swing profit liability.

This post maps the complete Section 16 exemption framework for Form 4 purposes, in the sequence that compliance teams most commonly encounter the questions: from who is a reporting person, through which transactions are fully exempt, through the critical Rule 16b-3 and Rule 16a-13 distinctions, through the new FPI landscape post-HFIAA, and finally to the enforcement risk and audit tools available.

What Is Section 16 and Who Has to File Form 4?

Section 16 of the Securities Exchange Act of 1934 imposes three separate obligations on insiders of companies with registered equity securities. Section 16(a) requires reporting of beneficial ownership and changes in ownership. Section 16(b) requires disgorgement of short-swing profits from purchase and sale transactions within a six-month window. Section 16(c) prohibits short sales. A Form 4 is the vehicle for reporting changes in beneficial ownership under Section 16(a), and it must be filed within two business days of a reportable transaction.

A Section 16 reporting person is any person who falls into one of three categories at the time of the transaction in question.

Directors include any member of the board of directors of the issuer, including shadow directors and directors by deputization. A person is a director by deputization when an entity that owns securities of the issuer has the right to designate a director and exercises that right, even if the designated director is formally employed by the entity rather than the issuer. According to the SEC's Division of Corporation Finance guidance on Section 16, deputized directors are subject to Section 16 as directors of the issuer.

Officers are defined under Exchange Act Rule 16a-1(f), which covers the president, principal financial officer, principal accounting officer, any vice president in charge of a principal business unit, division or function, any other officer who performs a policy-making function, and any other person who performs similar policy-making functions. The definition is functional, not title-based. A person who performs policy-making functions is an officer for Section 16 purposes regardless of whether their title includes the word "officer."

Ten percent beneficial owners are any person who directly or indirectly beneficially owns more than ten percent of any class of equity securities registered under Section 12. The beneficial ownership calculation uses the same constructive ownership rules that apply under Section 16(a), including attribution through trusts, partnerships, and certain family relationships.

The reporting obligation attaches at the moment a person becomes a reporting person and continues for as long as they remain one. Initial ownership must be disclosed on Form 3 within ten calendar days of becoming a reporting person. Subsequent changes in ownership must be reported on Form 4 within two business days of the transaction. Transactions not previously reported on Form 4 are reported annually on Form 5.

Which Transactions Are Exempt From Section 16 Form 4 Filing?

The Section 16 exemption framework separates into three distinct tiers, and understanding which tier a transaction falls into is the foundational compliance decision. Tier one: transactions that are entirely exempt from Section 16 reporting with no Form 4 or Form 5 required. Tier two: transactions exempt from Section 16(b) short-swing profit liability but still required to be reported on Form 4 within two business days. Tier three: transactions reportable but deferrable to Form 5 rather than requiring an immediate Form 4.

Most compliance errors occur because teams treat tier one and tier two as the same category. They are not.

Tier one - completely exempt, no filing required:

Transactions by persons who are not reporting persons at the time of the transaction fall entirely outside Section 16. For ten percent owners, the Supreme Court held in Foremost-McKesson, Inc. v. Provident Securities Co. (1976) that Section 16(b) applies only if the person held more than ten percent at both the time of the purchase and the time of the sale.

Transactions in non-equity securities are entirely outside Section 16, which applies only to equity securities registered under Section 12. A director who buys the company's debt securities has no Section 16 obligation.

Odd-lot acquisitions under Rule 16a-6 are exempt when the acquisition results in the reporting person holding less than one thousand dollars in market value of the securities class. This exemption is narrow and rarely determinative for typical executive transactions.

Transfers pursuant to a qualified domestic relations order (QDRO) in connection with a divorce proceeding are not reportable. The SEC staff has confirmed in interpretive guidance that QDRO transfers fall outside Section 16(a).

Tier two - exempt from Section 16(b) but Form 4 required within two business days:

This is the tier that generates the most missed filings. Equity award grants, tax withholding transactions, option exercises, and discretionary plan transactions all fall here. They are exempt from short-swing profit liability under Rule 16b-3 when the applicable approval conditions are met, but they must be reported on Form 4 within two business days using the applicable transaction code. The exemption eliminates the liability risk, not the disclosure obligation.

Tier three - reportable but deferrable to Form 5:

Bona fide gifts (transaction code G), inheritances and acquisitions by will or descent (transaction code W), deposits into or withdrawals from voting trusts (transaction code Z), and portfolio transfers under Rule 16a-13 where the person's economic exposure to the securities does not change may all be reported on the annual Form 5 rather than on Form 4 within two business days.

What Is Rule 16b-3 and What Transactions Does It Exempt?

Rule 16b-3 is the most practically significant exemption rule for directors and officers at public companies. It exempts from Section 16(b) short-swing profit liability transactions between the issuer and its directors and officers, provided the applicable conditions are met. Understanding precisely what Rule 16b-3 does and does not exempt is essential because it governs the vast majority of equity compensation transactions at every public company.

The threshold point: Rule 16b-3 applies only to transactions between the issuer and directors or officers. It does not apply to ten percent beneficial owners who are not also directors or officers. A ten percent owner who is solely a shareholder cannot rely on Rule 16b-3 regardless of how a transaction with the issuer is structured.

Rule 16b-3 organises its exemptions into three categories.

Grants, awards, and other acquisitions from the issuer under Rule 16b-3(d). Acquisitions of issuer equity securities by a director or officer from the issuer are exempt from Section 16(b) liability if the board of directors, a committee of the board composed solely of two or more non-employee directors, or the shareholders of the issuer approves the transaction in advance or ratifies it after the fact. The approval must cover the specific transaction or a class of transactions of which the specific transaction is a part. The most common application is equity award grants: stock option grants, RSU grants, restricted stock awards, and performance share awards approved by the compensation committee.

Dispositions to the issuer under Rule 16b-3(e). Dispositions of issuer equity securities back to the issuer by a director or officer are exempt from Section 16(b) if the transaction is approved in advance by the board, a committee of two or more non-employee directors, or the shareholders. Common applications include share repurchases by the issuer from insiders and tax withholding transactions where the company withholds shares to satisfy the reporting person's tax liability on a vesting event.

Discretionary transactions under tax-conditioned plans under Rule 16b-3(f). Discretionary transactions made pursuant to tax-conditioned plans are exempt from Section 16(b) if the election to effect the transaction is made at least six months after an opposite-way election was last made under any plan of the issuer. This six-month waiting period is one of the more operationally demanding elements of Rule 16b-3 compliance.

The non-employee director standard for Rule 16b-3 committee approval is defined specifically in the rule. A non-employee director is a director who is not currently an officer of the issuer, does not receive compensation from the issuer for services rendered as a consultant or in any non-director capacity (with limited exceptions), and does not possess an interest in any transaction for which disclosure would be required under Item 404 of Regulation S-K.

According to the SEC's Section 16 C&DI guidance, Rule 16b-3 does not exempt transactions between the issuer and persons who are subject to Section 16 solely because they are more than ten percent beneficial owners. It is available, however, to a ten percent owner who is also subject to Section 16 by virtue of being an officer or director.

Do Equity Award Grants Require a Form 4 Filing?

Yes. This is the single most common misconception in Section 16 compliance practice, and getting it wrong is the most frequent source of late Form 4 filings.

Equity award grants approved by the compensation committee under Rule 16b-3(d) are exempt from Section 16(b) short-swing profit liability. They are not exempt from Form 4 reporting. Under Rule 16a-3(g)(1), grants, awards, and acquisitions from the issuer that are exempt from Section 16(b) by Rule 16b-3(d) are nonetheless reportable on Form 4 using transaction code A (grant, award, or other acquisition from the issuer). The Form 4 must be filed within two business days of the grant date.

The same rule applies to each transaction type in the equity award lifecycle.

RSU vesting: When restricted stock units vest and shares are delivered, the delivery of shares is reportable on Form 4 using transaction code A for the acquisition of the underlying shares.

Tax withholding at vesting: When the company withholds shares at RSU vesting or option exercise to satisfy the reporting person's income tax obligation, that withholding is a disposition to the issuer exempt from Section 16(b) under Rule 16b-3(e). It is reportable on Form 4 as transaction code F (payment of exercise price or tax liability by delivering or withholding securities) within two business days of the vesting date.

Stock option exercise:The exercise of a stock option involves two reportable events. First, the option itself is reported as a derivative security disposition (transaction code M for the exercise or conversion of a derivative security). Second, the shares acquired upon exercise are reported as a non-derivative acquisition. Both are reportable on the same Form 4 within two business days of the exercise date.

Performance share award settlement: When performance shares settle at the end of a performance period, the delivery of shares is reportable on Form 4 as transaction code A.

The practical implication: your team needs to track grant dates, vesting dates, exercise dates, and settlement dates for every equity award held by every Section 16 reporting person. Every one of those dates triggers a two-business-day Form 4 filing clock. Grant date calendars and vesting schedules should be integrated into your Section 16 compliance monitoring process from the beginning of each fiscal year, not reviewed at the end of the quarter.

What Transactions Are Exempt From Section 16(b) But Still Require a Form 4?

This is the tier that generates the most missed filings across public companies. The full list of transactions that are exempt from Section 16(b) short-swing profit liability under Rule 16b-3 but still required to be reported on Form 4 within two business days covers every major equity compensation event.

Transaction code A: Grant, award, or other acquisition from the issuer. Equity award grants, RSU grants, restricted stock awards, performance share awards, and any other acquisition of issuer equity securities from the issuer approved under Rule 16b-3(d). Reportable on Form 4 within two business days of the grant or delivery date.

Transaction code D: Sale or disposition back to the issuer. Dispositions of equity securities to the issuer approved under Rule 16b-3(e), other than transactions coded as F. Share repurchases by the issuer from an insider at the insider's initiative are coded D. Reportable on Form 4 within two business days.

Transaction code F: Payment of exercise price or tax liability by delivering or withholding securities. Tax withholding transactions where the company withholds shares to cover the reporting person's tax liability on a vesting or exercise event, and cashless net exercise transactions where the insider delivers already-owned shares to pay the option exercise price. Reportable on Form 4 within two business days of the vesting or exercise date.

Transaction code I: Discretionary transaction under Rule 16b-3(f). Discretionary transactions pursuant to qualified or tax-conditioned plans that meet the six-month opposite-election waiting period requirement. Reportable on Form 4 within two business days.

Transaction code M: Exercise or conversion of derivative security. The exercise or conversion of a derivative security (stock option, warrant, convertible instrument) into the underlying equity security. The derivative security portion is reported as a disposition in the derivative securities table. The underlying equity security received is reported as a non-derivative acquisition in the non-derivative securities table. Both are on the same Form 4 and must be filed within two business days of the exercise date.

The pattern across all five transaction codes is identical: Rule 16b-3 exempts the short-swing profit liability, not the disclosure obligation. Every equity compensation event generates a two-business-day Form 4 filing clock regardless of whether board or committee approval was obtained.

What Is Rule 16a-13 and When Does the Portfolio Transfer Exemption Apply?

Rule 16a-13 exempts from both Section 16(b) liability and Section 16(a) reporting the transfer of securities by a reporting person from one form of beneficial ownership to another, provided the person's economic exposure to the securities does not change as a result of the transfer.

The most common applications are transfers between direct individual ownership and a revocable living trust in which the person is the sole trustee and sole beneficiary, or transfers between a trust and individual direct ownership where the person's pecuniary interest in the securities is identical before and after the transfer. When those conditions are met, no Form 4 or Form 5 is required.

The exemption is narrower than it appears and several common structures fall outside it.

According to the SEC's C&DI guidance, Rule 16a-13 is not available for a transfer of the issuer's shares to a mutual fund because the director would not retain investment control over the transferred securities within the fund. Rule 16a-13 is also not available for a transfer to any entity where the beneficial owner shares investment control with others, or where the person's beneficial interest changes as a result of the transfer.

Trusts where another family member serves as a co-trustee with shared investment authority, family limited partnerships where other partners have economic interests, and transfers to irrevocable trusts where the person loses beneficial ownership all fall outside Rule 16a-13. Those transactions require a Form 4 using transaction code J (other acquisition or disposition described in footnotes) or may qualify for deferred Form 5 reporting depending on the circumstances.

The key test for Rule 16a-13 is whether the transfer is merely a change in the form of ownership with no change in the person's pecuniary interest in the securities. If the person's economic exposure to the securities is identical before and after the transfer and the person retains sole investment control, Rule 16a-13 applies. If any of those conditions are not met, the exemption is unavailable.

Do Foreign Private Issuer Directors Need to File Form 4 After the HFIAA?

Yes, for directors and officers of FPIs not organised in an exempted jurisdiction, beginning March 18, 2026. This is the most significant structural change to Section 16 in decades.

The HFIAA (Holding Foreign Insiders Accountable Act), signed into law on December 18, 2025 and effective March 18, 2026, eliminates the longstanding exemption from Section 16(a) reporting for directors and officers of foreign private issuers with equity securities registered under Section 12 of the Exchange Act. Before the HFIAA, Exchange Act Rule 3a12-3(b) exempted securities registered by an FPI from all provisions of Section 16. After the HFIAA, that exemption is narrowed to Section 16(b) and Section 16(c) only.

The result is a structurally distinct compliance situation for FPI insiders. They must file Form 3, Form 4, and Form 5 on the same basis as domestic company insiders. They must file Form 4 within two business days of any reportable transaction. But because they remain exempt from Section 16(b), they face no short-swing profit risk and no need to structure transactions around the six-month window. The Form 4 is a disclosure obligation only, not a liability-management tool.

According to the SEC's HFIAA final rule release, adopted February 27, 2026, the SEC amended Rule 3a12-3(b), Rule 16a-2, and the text of Forms 3, 4, and 5 to implement these requirements. The SEC also issued an exemptive order on March 5, 2026 granting conditional exemptive relief for insiders of FPIs organised in jurisdictions that impose substantially similar reporting requirements under local law. According to Proskauer Rose's March 2026 analysis, FPIs organised outside the exempted jurisdictions and whose directors and officers are not subject to a qualifying local regulation remain subject to the new Section 16 requirements from March 18, 2026.

The HFIAA introduces several practical questions that FPI compliance teams must resolve.

Which transaction codes apply to FPI insiders? According to the Harvard Law Forum's March 2026 analysis of the SEC's final rule, the transaction codes in Forms 4 and 5 apply to FPI insiders, including the Rule 16b-3 codes (A, D, F, I, M), notwithstanding the continuing FPI exemption from Section 16(b). FPI compliance teams must apply the same transaction code framework as domestic company insiders for Form 4 reporting purposes.

What must be reported on the first Form 4? According to the SEC's HFIAA FAQ, for FPIs that had a class of equity securities registered under Section 12 prior to March 18, 2026, Rule 16a-2(a) does not require the first Form 4 to include transactions that occurred before March 18, 2026. Only transactions occurring on or after that date must be reported on Form 4.

Does Rule 16b-3 apply to FPI insiders? FPI insiders are exempt from Section 16(b) entirely, so Rule 16b-3's primary purpose (eliminating short-swing profit liability) is irrelevant to them. However, since they must still file Form 4 for the same transactions that domestic insiders file, the transaction codes associated with Rule 16b-3 transactions (A, D, F, I, M) still apply to FPI insiders for Form 4 coding purposes.

What Section 16 Violations Draw SEC Comment Letters?

Section 16 reporting failures are among the most mechanically scrutinised compliance areas in SEC review. Unlike many disclosure areas where SEC comment triggers require nuanced judgment, Section 16 failures are often objectively identifiable: a Form 4 was late, a transaction was omitted, or a transaction code was applied incorrectly.

Domestic issuers are required under Item 405 of Regulation S-K to disclose in their proxy statement or annual report on Form 10-K whether any Section 16 insiders failed to file required reports on a timely basis during the most recent fiscal year. That disclosure is what surfaces Section 16 failures for SEC review and generates follow-up comment letters.

The most common Section 16 comment letter triggers identified in EDGAR comment letter correspondence are the following.

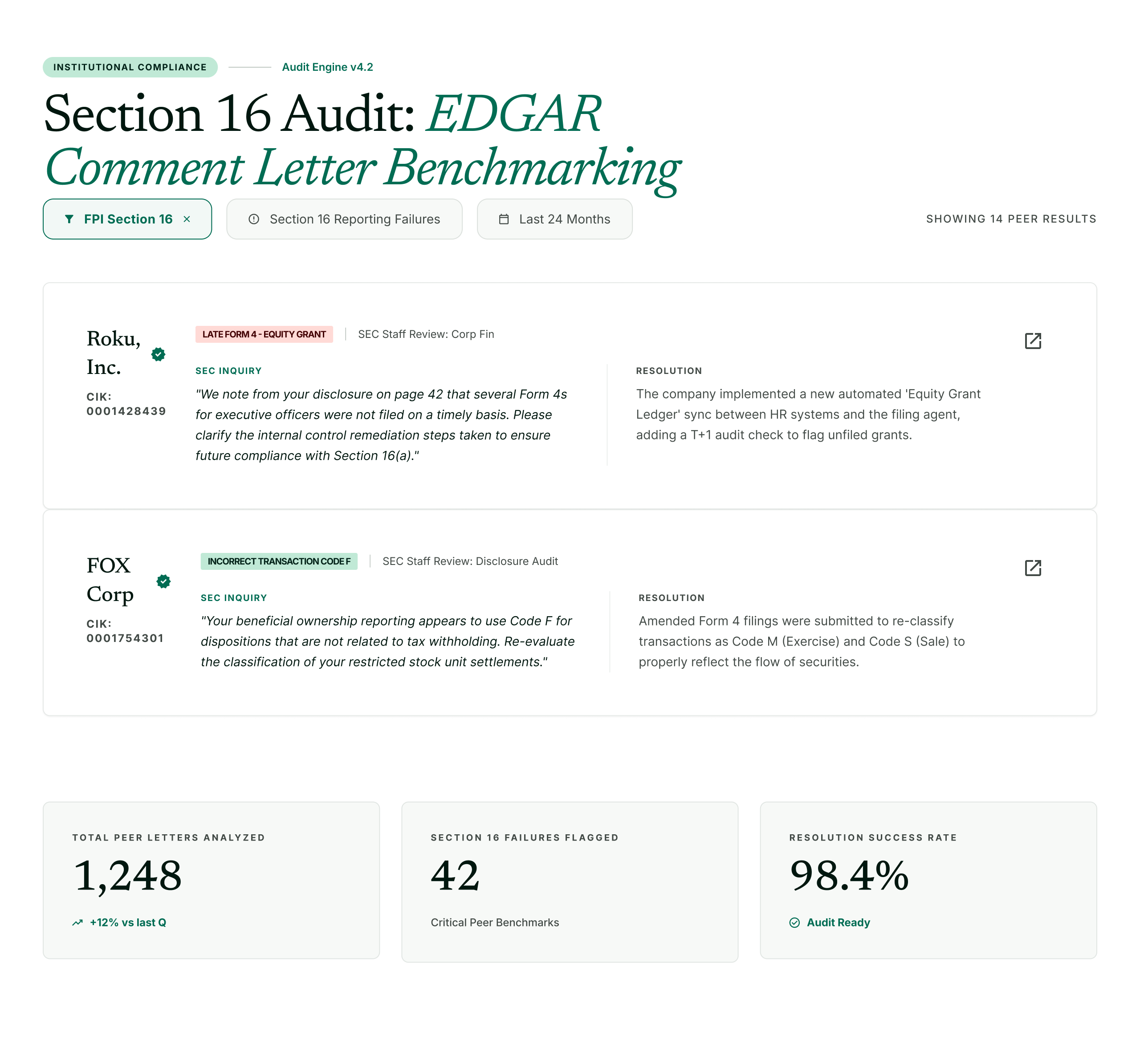

Late Form 4 filings for equity award events. The most frequently cited Section 16 reporting failure across all industries is a late Form 4 for an equity award transaction: a stock option grant, RSU vesting, or tax withholding event. These occur on predictable schedules that are known in advance and should never generate late filings. When they do, the SEC asks for an explanation of the company's internal controls over Section 16 reporting and what steps were taken to prevent recurrence. A pattern of late equity award filings across multiple insiders signals a systemic control failure and generates more intensive follow-up.

Incorrect transaction codes. Using the wrong transaction code is a reportable error that generates SEC comments. The most common coding error is using transaction code S (open market sale) for a tax withholding transaction that should be coded F. The distinction matters because code S implies a market transaction that could implicate short-swing profit concerns, while code F signals a pre-approved disposition to the issuer exempt under Rule 16b-3(e).

Missing transactions. The SEC's automated EDGAR review system cross-references Form 4 filings against proxy statement disclosures of insider transactions and against 8-K filings that reference insider transactions, such as Item 5.02 filings for officer appointments and departures that often include equity award grants. Missing Form 4 filings for transactions disclosed elsewhere in the EDGAR record generate comments asking for an explanation of the omission and whether additional corrective filings are required.

Inadequate Item 405 disclosure. When a company discloses in its proxy statement that Section 16 insiders had late filings without adequately explaining the circumstances or the number of transactions involved, the SEC asks for supplemental information and may ask the company to revise its Item 405 disclosure.

FPI Section 16 compliance failures post-HFIAA. For FPI insiders who became subject to Section 16 on March 18, 2026, the most likely near-term comment triggers are failure to file Form 3 by the March 18 deadline and late Form 4 filings for transactions occurring in the first weeks after the effective date. The SEC is monitoring FPI Section 16 compliance actively in the first reporting cycle following the HFIAA effective date.

How Do I Audit My Company's Section 16 Form 4 Exemption Decisions?

Auditing your team's Section 16 exemption decisions is a two-step process: internal review of your transaction log against the exemption framework, and external benchmarking of your approach against how comparable companies have handled similar transactions and how the SEC has responded.

Internal review: the transaction log check. For every equity award transaction, plan transaction, and insider securities transfer in the review period, confirm that the transaction was either (a) reported on Form 4 with the correct transaction code within two business days, (b) reported on Form 5 with the correct deferral rationale, or (c) documented as exempt from reporting with a specific rule reference. The three-tier framework described in this post is the organising structure for that review. Every transaction must be assigned to one of the three tiers with a specific rule citation for each assignment.

Internal review: the exemption documentation check. For transactions coded as Rule 16b-3 exempt, confirm that the required board or compensation committee approval is documented and that the approval covers the specific transaction or class of transactions. For transactions claimed as exempt under Rule 16a-13, confirm that the economic exposure test and sole investment control test are both documented and satisfied. For transactions deferred to Form 5, confirm the deferral basis is one of the specifically permitted categories (gift, inheritance, QDRO, voting trust, Rule 16a-13 portfolio transfer).

External benchmarking: EDGAR comment letter research. The most efficient way to validate your exemption decisions against current SEC expectations is to review EDGAR comment letter correspondence from comparable companies on Section 16 issues. When the SEC has questioned a company's exemption claim, transaction code, or Item 405 disclosure, the full exchange is publicly available in EDGAR under the CORRESP and UPLOAD form types. Those exchanges tell your team not just what the SEC asked, but what documentation and rationale resolved the comment.

Finrep's Comment Letters Explorer filters the EDGAR comment letter archive for Section 16-specific correspondence, organised by comment type (late Form 4, incorrect transaction code, missing transaction, Item 405 disclosure) and by filing category (domestic issuer versus FPI post-HFIAA). Your team searches by the specific Section 16 issue you are auditing and receives a structured view of what the SEC asked, how comparable companies responded, and what documentation resolved the comment.

For FPI teams navigating the post-HFIAA landscape, the Comment Letters Explorer's FPI Section 16 filter surfaces comment letter activity from FPI registrants, allowing your team to benchmark your own Form 4 exemption decisions and transaction code choices against peer filing patterns as FPI Section 16 compliance history accumulates on EDGAR from March 2026 onward.

The research that would otherwise require two to three days of manual EDGAR correspondence review is available in Finrep in minutes, with a structured, citable output your legal and compliance team can document as the basis for their exemption determination.

Request access to Finrep's Comment Letters Explorer with Section 16 and FPI filters

Frequently Asked Questions

Which transactions do not require a Form 4 under Section 16?

Transactions that do not require a Form 4 fall into two categories. Tier one is completely exempt from all Section 16 reporting: QDRO transfers, odd-lot acquisitions under Rule 16a-6 resulting in less than one thousand dollars in market value, transactions in non-equity securities, and transactions by persons who are not reporting persons at the time. Tier three is reportable but deferrable to Form 5 rather than requiring an immediate Form 4: bona fide gifts (code G), inheritances and distributions by will or descent (code W), deposits into or withdrawals from voting trusts (code Z), and portfolio transfers under Rule 16a-13 where the person's economic exposure to the securities does not change.

What is Rule 16b-3 and which transactions does it exempt?

Rule 16b-3 exempts from Section 16(b) short-swing profit liability three categories of transactions between the issuer and its directors or officers: grants and awards from the issuer (Rule 16b-3(d)), dispositions to the issuer (Rule 16b-3(e)), and discretionary transactions under tax-conditioned plans (Rule 16b-3(f)). All three require board, compensation committee of two or more non-employee directors, or shareholder approval. Rule 16b-3 eliminates Section 16(b) liability but does not eliminate the Form 4 reporting obligation. Every Rule 16b-3-exempt transaction must still be reported on Form 4 within two business days using transaction codes A, D, F, I, or M.

Do equity award grants require a Form 4 filing?

Yes. This is the most common misconception in Section 16 compliance. Equity award grants approved by the compensation committee under Rule 16b-3(d) are exempt from Section 16(b) short-swing profit liability but are required to be reported on Form 4 within two business days of the grant date using transaction code A. The same applies to every subsequent equity award event: RSU vesting (code A), tax withholding at vesting (code F), option exercises (code M for the derivative and code A for the underlying shares), and performance share settlement (code A). No equity award event is exempt from Form 4 reporting.

Do foreign private issuer directors need to file Form 4 after the HFIAA?

Yes, for FPIs not organised in an exempted jurisdiction. The HFIAA, effective March 18, 2026, eliminated the longstanding Section 16(a) exemption for directors and officers of FPIs with equity securities registered under Section 12. FPI insiders must now file Form 3, Form 4, and Form 5 on the same timeline as domestic insiders. However, FPI insiders remain exempt from Section 16(b) short-swing profit disgorgement and Section 16(c) short sale prohibitions. The SEC granted conditional exemptive relief for FPIs organised in jurisdictions imposing substantially similar reporting requirements under local law.

What is Rule 16a-13 and when does the portfolio transfer exemption apply?

Rule 16a-13 exempts from both Section 16(b) and Section 16(a) reporting the transfer of securities from one form of beneficial ownership to another, provided the person's economic exposure does not change. The most common application is a transfer between direct individual ownership and a revocable living trust where the person is sole trustee and sole beneficiary. Rule 16a-13 is not available for transfers to mutual funds, entities where investment control is shared, irrevocable trusts where beneficial ownership changes, or any structure where the person's pecuniary interest in the securities is not identical before and after the transfer.

What Section 16 reporting failures draw SEC comment letters?

The most common triggers are late Form 4 filings for equity award events (grants, vestings, tax withholding), incorrect transaction codes particularly coding F transactions as S, missing Form 4 filings for transactions disclosed elsewhere in the EDGAR record, and inadequate Item 405 proxy statement disclosures when late filings are identified without adequate explanation. For FPI insiders post-HFIAA, late Form 3 filings at the March 18, 2026 initial deadline and late Form 4 filings in the first post-effective date reporting cycle are the most anticipated near-term comment triggers.

Key Takeaways

- The Section 16 exemption framework has three tiers, not two. Completely exempt from reporting, exempt from Section 16(b) but still requiring Form 4 within two business days, and reportable but deferrable to Form 5. Confusing tier one and tier two is the most common source of missed Form 4 filings.

- Rule 16b-3 exempts equity award grants, dispositions to the issuer, and discretionary plan transactions from Section 16(b) short-swing profit liability when the required board or committee approval conditions are met. It does not exempt any of those transactions from Form 4 reporting. Every equity award event generates a two-business-day Form 4 filing clock.

- The HFIAA, effective March 18, 2026, requires directors and officers of FPIs with Section 12-registered equity to file Forms 3, 4, and 5. FPI insiders remain exempt from Section 16(b) and Section 16(c) but must apply the same transaction code framework as domestic insiders for all Form 4 filings.

- Rule 16a-13 exempts portfolio transfers from both Section 16(b) and reporting only when the person's economic exposure to the securities is identical before and after the transfer and the person retains sole investment control. Transfers to mutual funds, shared-control entities, or irrevocable trusts fall outside the exemption.

- Finrep's Comment Letters Explorer filters EDGAR Section 16 correspondence by comment type and FPI status, allowing compliance teams to benchmark their exemption decisions against peer filing patterns and prepare documented, citable support for their determinations.

Request access to Finrep's Comment Letters Explorer with Section 16 and FPI filters

Finrep is an AI-powered financial disclosure intelligence platform for the Office of the CFO. 40 purpose-built AI agents for SEC reporting, technical accounting, investor relations, legal counsel, and disclosure committee functions. SOC2 Type II and ISO 27001 certified. Zero data residency. Backed by Accel. Trusted by CFO teams at FOX, Roku, HP, RingCentral, Wells Fargo, and Infosys.