Most SEC reporting teams encounter comment letter research in the wrong order.

The letter arrives. The clock starts. Your team pulls EDGAR, searches peer responses, reads through correspondence files, and builds a picture of what the SEC wants. Then you draft your response.

That research, the EDGAR search, the peer response analysis, the pattern recognition, is exactly the right work. The problem is the timing. By the time you are doing it, you have already filed. The disclosure gap the SEC found already exists in your public record.

The SEC publishes every comment letter it sends and every company response on EDGAR (the SEC's Electronic Data Gathering, Analysis, and Retrieval system). That is a complete, searchable archive of what the SEC scrutinises, which specific language triggers follow-up questions, and how comparable companies resolved those questions. It is publicly available before you file, not just after.

By the end of this post, you will know exactly how to find relevant comment letter history on EDGAR, how to read a comment letter exchange to extract the insight that matters, and how to apply that research to pressure-test your own disclosures before your next filing goes in. You will also see how Finrep's Comment Letters Explorer does this research in minutes rather than days.

What the SEC's Comment Letter Archive Actually Tells You

An SEC comment letter is a formal written inquiry from the SEC's Division of Corporation Finance (CorpFin) to a public company. It identifies specific disclosures the SEC found insufficient and asks the company to clarify, expand, or revise them. According to the SEC's Division of Corporation Finance overview, staff review filings to monitor compliance with disclosure requirements and to ensure investors receive the information they need to make informed decisions.

Here is what makes the archive valuable for pre-filing work: the SEC does not invent new concerns for every company it reviews. It applies consistent analytical frameworks across industries and filing types. When CorpFin staff review an MD&A (Management's Discussion and Analysis) section, they ask the same core question regardless of the company: does this explain the reasons behind material changes, or does it just describe them? When they review a non-GAAP reconciliation, they check the same set of conditions every time.

This consistency means that what the SEC asked your peer company last quarter is a reliable signal of what it might ask you. Reading peer comment letter exchanges does not tell you that you will receive a comment. It tells you exactly what question you would need to answer if you did, so you can answer it before anyone asks.

The SEC's comment letters page describes the correspondence process in full. Every letter and response is published on EDGAR within 20 business days of the exchange being completed. For companies in active capital markets activity, unresolved comment letters can prevent registration statements from being declared effective, which directly blocks offerings and debt issuances. The incentive to resolve comment concerns before filing rather than after is significant.

Why Most Teams Miss This Research Window

The pre-filing comment letter research window exists. Very few teams use it systematically. The reasons are practical rather than strategic.

Manual EDGAR research is slow. Finding comment letter correspondence for a meaningful peer group, 10 to 15 companies in your SIC (Standard Industrial Classification) code and size range, requires navigating individual company filing pages, filtering by correspondence form types, and reading through letters that may or may not be relevant to your disclosure areas. For a thorough pre-filing review, that process takes two to three days of focused analyst time. During close cycle, that time does not exist.

The research is also unstructured. A comment letter exchange is a document, not a database. When you read a letter, you are extracting patterns manually: what did the SEC ask, what language in the filing triggered the question, what did the company change in response. Without a structured way to organise those patterns across multiple companies and multiple letters, the insight stays in an analyst's head rather than becoming a repeatable team process.

The result is that most teams treat comment letter research as reactive work, something you do after a letter arrives, not before a filing goes out. This guide flips that sequence.

How to Read a Comment Letter Exchange for Maximum Pre-Filing Insight

Before you search, you need to know what you are looking for. A comment letter exchange has three parts, and each one tells you something different.

The SEC's comment letter itself

The letter identifies the filing under review, the specific section being questioned, and the exact language the SEC found insufficient. Read the SEC's letter first and pay attention to two things: the section cited and the type of question being asked.

SEC comment questions fall into recognisable categories. Some ask for more explanation: "Please explain the basis for your conclusion that..." Some ask for additional disclosure: "Please revise future filings to include..." Some ask the company to reconcile an inconsistency: "Your MD&A states X but your financial statements reflect Y. Please explain." Recognising the question type tells you what kind of gap the SEC identified.

The company's response

The response, filed under form type CORRESP on EDGAR, tells you two things: what the company said to resolve the comment, and whether that resolution required a disclosure change. Some responses explain why the existing disclosure was adequate and no change is needed. Others commit to revised disclosure language in future filings. Others file an amendment.

When a company commits to revised language, that revised language is often included in the response letter itself. That is the most useful output from this research: the exact disclosure the SEC considered sufficient. Use it as a benchmark for your own draft.

The follow-up letter, if there is one

If the SEC's initial comment was not fully resolved by the company's first response, a follow-up letter arrives. The presence of a follow-up letter on EDGAR tells you the SEC considered the first response inadequate. Reading what the SEC pushed back on in a follow-up is more instructive than reading the original comment, because it reveals the minimum threshold for resolution, not just the opening question.

Now that you know what to look for in each document, here is how to find the right ones.

A Step-by-Step Guide to Searching Comment Letter History on EDGAR

This is the research method your team should run four to six weeks before every 10-K or significant 10-Q filing. Here is how to do it efficiently.

Step 1: Open EDGAR Full-Text Search and Set Your Parameters

Go to EDGAR Full-Text Search. This is the SEC's native search tool for all public filings, including comment letter correspondence.

In the search bar, enter the specific disclosure topic you want to research. Use the language the SEC uses, not the language your team uses internally. A few examples:

- "revenue recognition variable consideration" rather than "ASC 606 revenue"

- "segment aggregation criteria" rather than "segment reporting"

- "non-GAAP reconciliation prominence" rather than "Adjusted EBITDA"

- "cybersecurity risk factor specificity" rather than "cyber disclosure"

In the filing type field, enter CORRESP to filter for company responses to SEC comment letters. Set your date range to the past 24 months. Comment letter focus areas shift with SEC regulatory priorities, and older letters may reflect concerns that have since been addressed by updated guidance or new accounting standards.

Step 2: Filter by Industry Using SIC Code

The EDGAR filing search portal allows you to search for registrants by SIC code. Every registrant is classified by SIC code based on their primary business activity. Searching by SIC code gives you a peer list to cross-reference against your Step 1 results.

Why this matters: CorpFin staff are organised into industry groups. The technology group reviews technology company filings. The healthcare group reviews healthcare company filings. Staff within each group develop familiarity with industry-specific disclosure practices, and their comment focus clusters around issues that are material for that industry. Filtering by SIC code ensures your research reflects what the relevant industry group is actually focusing on, not what a different group is asking companies in a different sector.

Select 8 to 12 peer companies of comparable size, business model, and capital markets activity. Companies that recently completed an IPO, a significant acquisition, or a debt offering are particularly good research targets because those events often trigger heightened SEC filing review.

Step 3: Read the Exchange Using a Three-Column Tracker

For each relevant comment letter exchange, read all three documents: the SEC's letter, the company's CORRESP response, and any follow-up letter. Build a simple three-column tracker as you go:

Column 1: What the SEC asked, in one sentence. Column 2: What the company said in response. Column 3: What disclosure change, if any, resulted.

You are building a pattern library, not a document archive. After reviewing 8 to 10 exchanges on a given topic, patterns become clear: the specific language constructions that trigger questions, the disclosure depth that satisfies the SEC, and the response approaches that resolve comments without follow-up letters.

Step 4: Pull Your Own Company's Comment Letter History

Search EDGAR for your own company's correspondence files using your CIK (Central Index Key) number. Your CIK is visible on any EDGAR filing page for your company.

Filter for UPLOAD form type to see the SEC's letters to your company, and CORRESP to see your responses. Read every exchange from the past five years using the same three-column framework.

Any disclosure area the SEC has previously questioned is a high-priority target for your pre-filing review. If you made a disclosure change in response to a prior comment, confirm that the revised approach is consistent and fully reflected in your current draft. Inconsistency between a prior response commitment and current filing language is one of the fastest ways to generate a repeat comment.

Step 5: Apply the Pattern Library to Your Draft

Take your three-column tracker from Steps 3 and 4 and run each pattern against the equivalent section of your current filing draft. For each high-risk disclosure area, ask three questions:

First: does your current disclosure explain the reasons behind material changes, or does it describe them? Description says what happened. Explanation says why it happened and what it means going forward. The distinction between those two things is the core of most MD&A comment letters.

Second: if the SEC sent your company the same question they sent to your peer, would your current disclosure answer it? Read your draft through the lens of the SEC's question, not through the lens of your own knowledge of the business. The disclosure must stand on its own for a reader without your context.

Third: is your disclosure depth comparable to what your peers are filing on this topic? Thin disclosure in a high-attention area stands out. If your peer group uses three paragraphs to describe their revenue recognition methodology and your draft has one, that gap is visible to CorpFin staff even without a formal comparison tool.

Revise where the answer to any of these questions is no. Document the review and the revisions made. That documentation supports your Section 302 disclosure controls certification under the Sarbanes-Oxley Act and gives your audit committee a basis for pre-filing sign-off.

How Finrep's Comment Letters Explorer Does This in Minutes

The five-step process above is thorough. It is also time-intensive when done manually. During close cycle, two to three days of EDGAR research competes directly with every other filing deadline on your calendar.

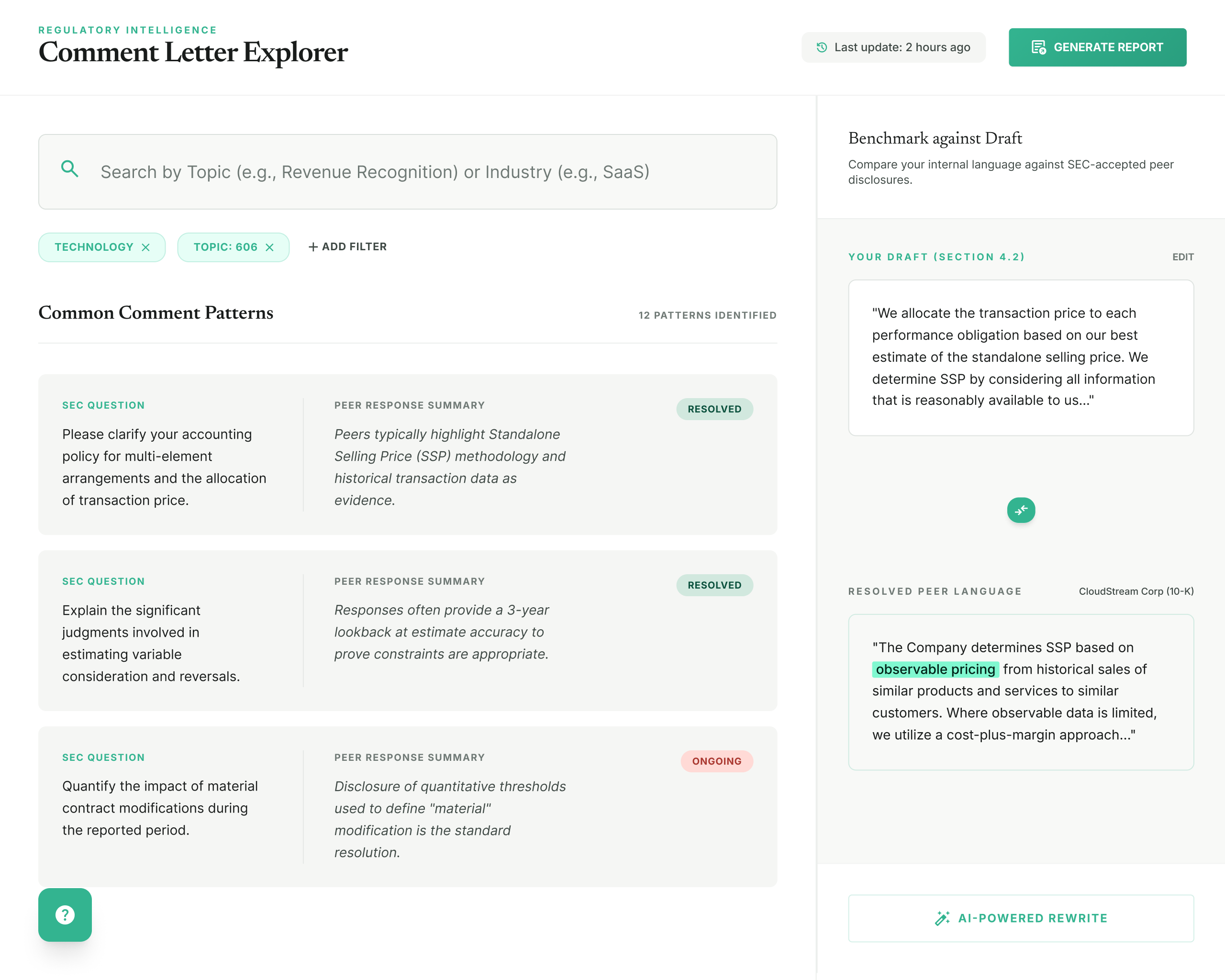

Finrep's Comment Letters Explorer automates the research layer of this process. Here is what using it looks like in practice.

Step 1: Topic and industry search

You open the Comment Letters Explorer and enter your disclosure topic and industry category. Finrep queries EDGAR's comment letter correspondence archive and returns a structured list of relevant exchanges, organised by recency, industry match, and comment type. You are not navigating individual company filing pages. You are looking at a filtered, relevant result set in seconds.

Step 2: Comment pattern view

For each result, Finrep surfaces the SEC's question, the company's response summary, and the resolution outcome, presented as structured data rather than raw document text. You can see at a glance: what the SEC asked, what the company said, and whether the comment resolved in one exchange or required follow-up. Patterns across multiple companies become visible immediately without building your own tracker from scratch.

Step 3: Peer benchmarking against your draft

You paste your current disclosure draft for the section under review. Finrep compares your disclosure language and depth against the peer group's resolved disclosures from the comment letter research. The output shows where your disclosure is consistent with market practice and where it falls short of the depth that has satisfied the SEC in comparable exchanges.

Step 4: Guidance alignment check

For any disclosure area connected to a specific accounting standard, Finrep surfaces the relevant guidance alongside the comment letter pattern. You see the standard's requirement, what the SEC asked peers about, and how your draft compares, all in one view. No switching between EDGAR, the FASB Accounting Standards Codification, and your draft document simultaneously.

Step 5: Export and audit trail

Finrep generates a structured summary of the pre-filing review: which disclosure areas were researched, which peer comment patterns were identified, and what revisions were made. This export serves as your documented evidence that disclosure controls and procedures were applied before filing, which is directly relevant to Section 302 and Section 906 certifications.

The time saving is material. Research that takes two to three days manually takes under an hour with Finrep. According to Finrep client data, 2025, teams using Finrep's disclosure intelligence tools reduce their month-end SEC reporting preparation time from 10 days to 3 to 4 days, with 60 to 70% fewer review loops with auditors.

Finrep is an AI-powered SEC reporting and financial disclosure intelligence platform for the Office of the CFO. SOC2 Type II and ISO 27001 certified. Zero data residency. Your data is never retained or used to train models.

Ready to run a pre-filing pressure-test using live EDGAR comment letter data? Request access to Finrep's Comment Letters Explorer.

What Good Pre-Filing Disclosure Looks Like: The Standard Your Review Should Meet

Running the research is one thing. Knowing when your disclosure has passed the test is another. Here is a practical benchmark for each layer of the review.

On MD&A: Your discussion explains the business reasons behind every material variance, not just the direction and magnitude. If revenue declined, the disclosure identifies which segment, product line, or customer drove the decline and what management expects going forward. A reader with no prior knowledge of your company should be able to understand the story from the MD&A alone.

On non-GAAP measures: Every non-GAAP measure has a clearly labelled GAAP reconciliation. The GAAP measure appears with at least equal prominence. Any item excluded from the non-GAAP calculation is described specifically and consistently with how it was described in prior periods. If a definition changed, that change is disclosed explicitly with an explanation of why. The SEC's C&DI guidance on non-GAAP financial measures is the controlling reference.

On forward-looking disclosures: Your risk factors and liquidity disclosures reflect the company's actual current circumstances. Known trends and uncertainties that a reasonable investor would consider material are identified and discussed specifically, not acknowledged in general boilerplate terms carried forward from the prior year.

On peer benchmarking: For every high-attention disclosure area, your disclosure depth is within the range of what comparable registrants are filing. Materially thinner disclosure than your peer group in an area of active SEC focus is a comment letter risk regardless of technical accuracy. Per the Harvard Law School Forum on Corporate Governance, pre-filing peer benchmarking has become a standard practice for disclosure committees at listed companies.

On documentation: Your pre-filing review has a written record. The review was completed before the CFO and Controller signed Section 302 certifications. The audit committee received a summary of the review findings. This documentation is the evidence that your disclosure controls and procedures operated effectively for the period. It is also the foundation of a defensible response if a comment does arrive.

Frequently Asked Questions

What is an SEC comment letter and how does it differ from an SEC investigation?

An SEC comment letter is a routine part of the SEC's filing review process. It is a written request from CorpFin staff for clarification or additional disclosure in a public filing. It is not an allegation of fraud or the beginning of a formal investigation. Most public companies receive comment letters at some point, particularly following significant transactions or changes in financial results. A formal investigation by the SEC's Division of Enforcement is a separate and far less common process initiated when staff have reason to believe securities laws may have been violated.

How do I access my company's own SEC comment letter history on EDGAR?

Go to EDGAR Full-Text Search and search by your company name or CIK number. Filter by form type UPLOAD to see letters the SEC sent to your company, and CORRESP to see your company's responses. All correspondence is publicly accessible. Your CIK number is visible on any EDGAR filing page for your company and on the EDGAR filing search portal.

How far back should I go when researching peer comment letter history?

Focus on the past 24 to 36 months for most disclosure areas. SEC comment focus shifts with regulatory priorities and new accounting standards. For cybersecurity disclosure, focus on letters from 2024 onward, after the SEC's December 2023 cybersecurity disclosure rules took effect. For AI-related risk disclosures, 2025 letters are most relevant given the pace of SEC guidance activity in this area. Per the SEC's filing review process page, staff apply current regulatory priorities when selecting filings for review.

What should I do if my research reveals a gap in a disclosure I have already filed?

Assess materiality with your legal counsel and auditors first. If the gap is material, you may need to file an amendment. If it is not material, document your assessment and revise the disclosure in your next filing. The key is to have a written record of the assessment and the decision made, regardless of the outcome. Undocumented decisions are far harder to defend if the SEC does follow up.

How does Finrep's Comment Letters Explorer differ from manual EDGAR research?

Manual EDGAR research requires navigating individual company filing pages, filtering by form type, reading raw document text, and building your own pattern library by hand. Finrep's Comment Letters Explorer queries EDGAR's correspondence archive and returns structured results organised by topic, industry, recency, and resolution outcome. The peer benchmarking layer compares your draft directly against resolved peer disclosures. The structured export creates an audit trail of your pre-filing review. Total research time drops from two to three days to under an hour for a thorough pre-filing pressure-test.

Can a pre-filing review eliminate the risk of receiving a comment letter entirely?

No pre-filing review eliminates the risk entirely. The SEC may select your filing for review based on rotation, risk indicators, or market events outside your control. What a thorough pre-filing review does is reduce the probability that a review will surface material disclosure gaps. It also means that if a comment does arrive, your team already has documented reasoning behind your disclosure approach, which significantly accelerates the response process and reduces the likelihood of follow-up letters.

Key Takeaways

- The SEC publishes every comment letter and company response on EDGAR. That archive is a pre-filing research tool, not just a post-filing reference. Your team should be using it before you file.

- Reading a comment letter exchange in full, including the SEC's letter, the CORRESP response, and any follow-up, reveals the exact disclosure depth and language the SEC considered sufficient for resolution. That is your benchmark.

- A five-step EDGAR research process covering topic search, SIC-filtered peer selection, structured exchange reading, own-history review, and draft application produces a reliable pre-filing pressure-test. Done manually, it takes two to three days.

- Finrep's Comment Letters Explorer compresses that research to under an hour. It adds peer benchmarking against your draft, surfaces accounting guidance in the same workflow, and exports a structured audit trail for your Section 302 documentation.

- The goal is not to predict every comment. It is to ensure that if the SEC does review your filing, the questions they would ask are ones you have already answered.

See how Finrep's Comment Letters Explorer works on your next filing. Request access here.

Finrep is an AI-powered SEC reporting and financial disclosure intelligence platform for the Office of the CFO. Research, benchmark, and draft SEC filings using EDGAR data with cited, audit-ready outputs. SOC2 Type II and ISO 27001 certified. Backed by Accel. Trusted by CFO teams at FOX, Roku, HP, RingCentral, and Infosys.

For related reading on how to build peer benchmarking into your broader disclosure workflow, see how Finrep compares to Intelligize for EDGAR research and financial disclosure benchmarking and the Section 16 deadline guide for Foreign Private Issuers.