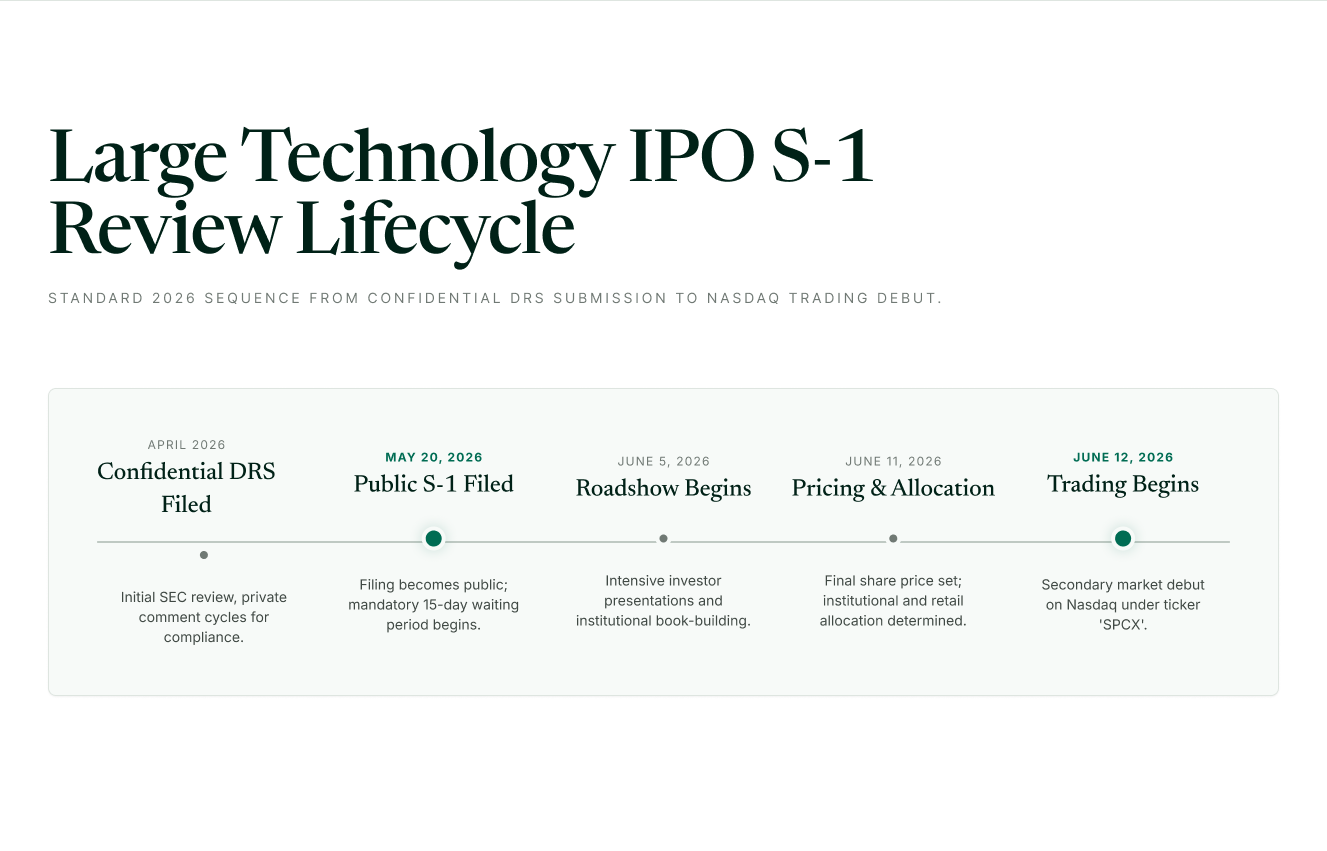

On May 20, 2026, Space Exploration Technologies Corp. filed its public S-1 registration statement with the Securities and Exchange Commission, formally beginning the process of its initial public offering on the Nasdaq under the ticker SPCX. SpaceX had confidentially submitted a draft registration statement to the SEC in April 2026, allowing the company to work through SEC review comments before the public filing, which is standard practice for large IPO candidates under the Jumpstart Our Business Startups Act. The public S-1 filing is required to be available for at least 15 days before the investor roadshow begins.

The SpaceX S-1 is the most significant technology company IPO filing in history by several measures. It is the first complete public disclosure of SpaceX's financial statements since the company was founded in 2002. It covers three business segments Space, Connectivity (Starlink), and AI (xAI, following a February 2026 merger) that collectively produced $18.674 billion in revenue in 2025. The filing targets a valuation range of $1.75 trillion to $2 trillion.

But the significance of the SpaceX S-1 extends beyond the specific company. It is the opening filing in what 2026 is shaping up to be: the most consequential year for technology IPO activity since 2021, with OpenAI, Anthropic, Discord, and Revolut all at various stages of the public filing process. Each of these filings will establish disclosure precedents, face SEC comment letter scrutiny, and present ICP practitioners CFOs, bankers, disclosure counsel, and investors with the most complex IPO documents in a generation.

This post analyses what the SpaceX S-1 actually contains, what it reveals about how the largest technology companies approach the public markets, and what the 2026 pipeline signals about the future of tech IPO disclosure.

What Is an S-1 and Why Does It Matter for Tech Companies Going Public?

An S-1 is a registration statement filed under the Securities Act of 1933 that a company must submit to the SEC before it can offer securities to the public in the United States. For a domestic company conducting an initial public offering on a U.S. exchange, the S-1 is the foundational disclosure document. It is required to contain audited financial statements, a business description, risk factors, management discussion and analysis, executive compensation, and a description of the offering terms and use of proceeds.

For technology companies, the S-1 is particularly significant because it is frequently the first time audited financial data, revenue breakdowns, unit economics, and customer concentration information are disclosed publicly. Private technology companies are not required to file periodic reports with the SEC. When they file an S-1, they make the transition from a company that discloses nothing publicly to one that discloses everything in a single document, under the full antifraud liability of the Securities Act of 1933.

The S-1 process has two stages for large companies. Under the JOBS Act of 2012, companies that qualify as Emerging Growth Companies (EGCs) those with less than $1.235 billion in annual gross revenue may file a Draft Registration Statement (DRS) confidentially with the SEC. The confidential DRS process allows the company to receive SEC staff comments and revise the filing before it becomes public. Once the public S-1 is filed, it must be available for at least 15 calendar days before the roadshow begins.

Most large technology companies including SpaceX, Discord, and Revolut in the current cycle use the confidential filing process even if they do not qualify as EGCs, because the SEC extended confidential submission eligibility to all issuers in 2017. For a company of SpaceX's scale and complexity, the confidential stage serves a specific purpose: it allows SEC staff to review the financial statement presentation, segment reporting structure, use of proceeds, and risk factor adequacy before the company is under public scrutiny and market pressure.

The S-1 is, as one analysis correctly observes, the most honest document a company ever produces about itself. It is a legal disclosure obligation, not a marketing document. The antifraud provisions of Section 11 of the Securities Act create civil liability for material misstatements in a registration statement, and Section 12 creates additional liability for material omissions. Every disclosure in an S-1 is made under those liability standards.

What Does the SpaceX S-1 Actually Disclose?

The SpaceX S-1, filed on May 20, 2026, is the primary data source for understanding how the largest private technology company in the world has structured its business, its financials, and its approach to public market disclosure.

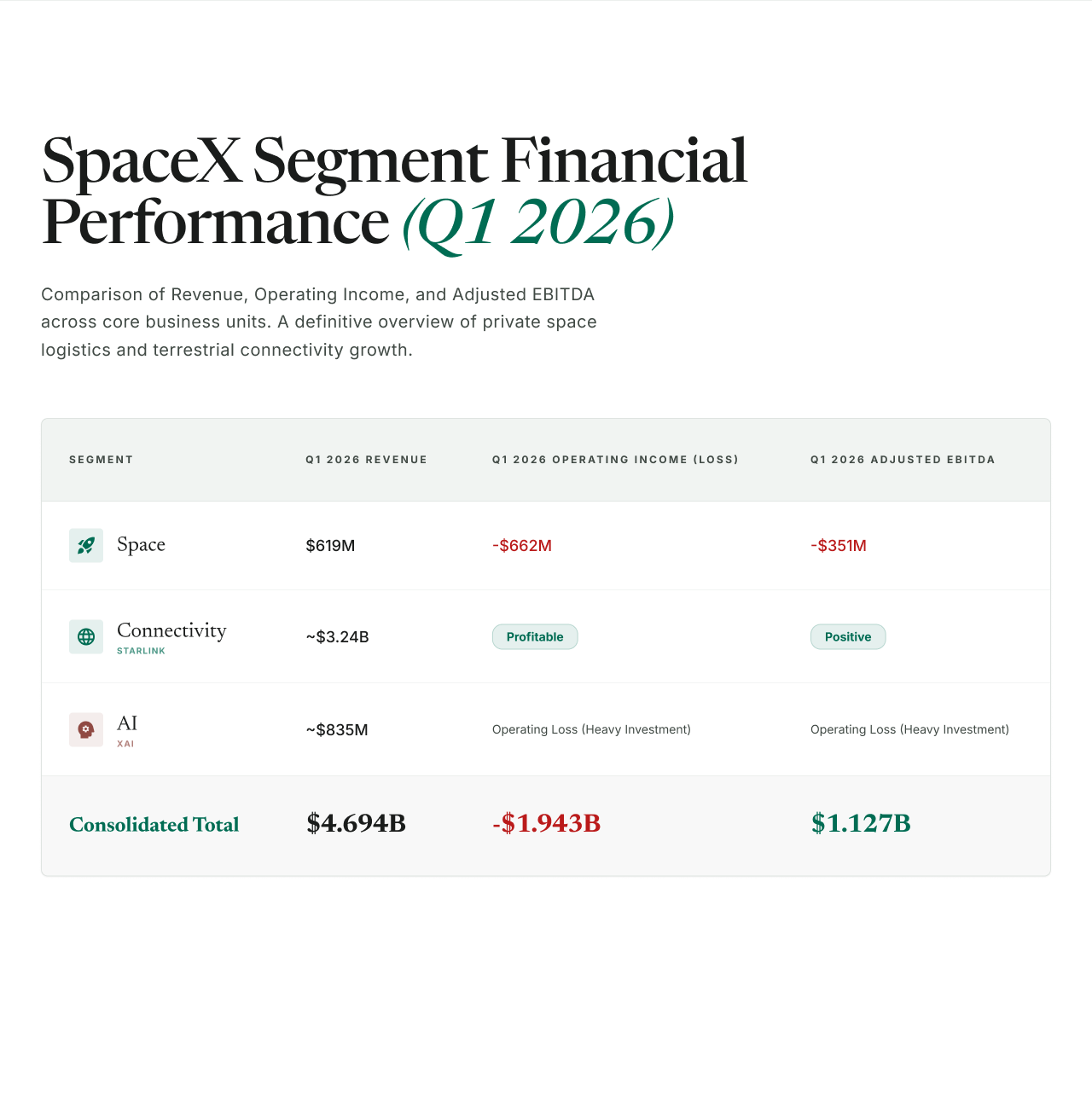

Revenue and segment structure. SpaceX reported revenues of $10.387 billion, $14.015 billion, and $18.674 billion for fiscal years 2023, 2024, and 2025, representing a compound annual growth rate of approximately 34%. The company operates three segments: Space (the rocket launch business), Connectivity (Starlink satellite internet), and AI (xAI, consolidated following the February 2026 merger at a combined valuation of $1.25 trillion).

The Connectivity segment, driven by Starlink, is the sole profitable segment, accounting for 69% of Q1 2026 revenue. The Space segment generated $619 million in Q1 2026 revenue but reported a $662 million operating loss. The AI segment, which was only consolidated for the first time in Q1 2026, is in heavy investment mode and is driving the majority of the operating loss at the consolidated level.

Profitability and operating losses. For the three months ended March 31, 2026, SpaceX reported revenue on a consolidated basis of $4.694 billion, a loss from operations of $1.943 billion, and adjusted EBITDA of $1.127 billion. At the annual level, in 2025, SpaceX generated revenue on a consolidated basis of $18.674 billion, and a loss from operations of $2.589 billion and adjusted EBITDA of $6.584 billion.

The operating loss is driven substantially by the xAI investment. SpaceX's operating loss is largely being driven by the AI segment; the legacy SpaceX segments (Space and Connectivity) are profitable on both an operating and EBITDA basis.

Research and development. Research and development expenses for fiscal years 2023, 2024, and 2025 were $2.105 billion, $3.464 billion, and $8.643 billion, representing a compound annual growth rate of 60.01%. The R&D growth rate significantly exceeds the revenue growth rate, reflecting the company's investment in the xAI data centre infrastructure, Starship development, and next-generation satellite constellation expansion.

Governance structure. The company will issue two classes of common stock, with Elon Musk holding 85.1% of the voting power. The dual-class structure concentrates control entirely in the founder, a governance approach that investors in the current filing cycle must price into their assessment of the company.

Key contractual disclosures. In March 2026, SpaceX's Colossus 1 data centre secured a deal with Anthropic worth $1.25 billion per month through May 2029. The facility houses 220,000 Nvidia GPUs across 300MW of power and was built in 120 days. Either party can terminate with 90 days' notice. This termination provision is a material risk that investors must weigh against the headline contract value.

Operational metrics. As of March 31, 2026, SpaceX had launched a total mass to orbit of approximately 7,400 metric tons with an over 99% mission success rate across its Falcon rockets.

How Does the SpaceX S-1 Compare to Prior Tech IPO Disclosure Standards?

The SpaceX S-1 establishes several disclosure precedents that differ from the conventions that dominated the last major tech IPO cycle in 2020 and 2021.

Profitable segment disclosure in a loss-making consolidated entity. The SpaceX filing is structured around a three-segment disclosure where the consolidated entity reports operating losses but the core legacy business (Connectivity) is profitable. This segment presentation is technically required by ASC 280 when the CODM views performance at the segment level, but the specific challenge it creates for investors is understanding the cross-subsidy dynamic. The S-1 is transparent about which segment is generating the operating loss (AI and to a lesser extent Space), which is a higher standard of segment-level transparency than many loss-stage technology IPOs have historically provided.

Dual-class governance at an unprecedented scale. The prior-cycle controversy around dual-class share structures which was a significant point of tension in the Snap IPO (2017) and was adopted in various forms by Google, Facebook, and most major tech companies reaches its most extreme form in the SpaceX filing. An 85.1% voting concentration in a single founder is without direct precedent in a company of this scale. The governance risk factor disclosure around founder concentration will be one of the most closely scrutinised sections of the filing.

AI segment disclosure as a new category. The inclusion of xAI as a consolidated segment in the SpaceX S-1 is significant because it is the first time a major AI company has appeared inside a public registration statement as a consolidating entity. This creates a disclosure template for revenue recognition, R&D capitalisation versus expensure, computing infrastructure as a capital investment, and customer concentration in AI compute contracts that will influence how OpenAI and Anthropic present their own financials when they file.

Government contract disclosure and national security risk factors. SpaceX's exposure to government contracts through its Starshield military satellite business creates a category of risk factor disclosure that most technology IPOs do not face: the intersection of commercial business operations with national security classifications. The S-1's risk factor section addresses launch failure rates, founder dependence, regulatory exposure for Starlink spectrum rights across multiple countries, and Starshield programme classification in ways that have no direct precedent in the consumer and enterprise software IPOs that defined the prior cycle.

What SEC Scrutiny Patterns Are Emerging for Tech IPOs in 2026?

The SEC's review of large technology IPO filings focuses on several recurring areas that practitioners preparing or analysing S-1 filings need to understand.

Non-GAAP financial measures in IPO filings. The SEC has been increasingly focused on the appropriate presentation of non-GAAP measures in registration statements. The SpaceX S-1 uses Adjusted EBITDA as its primary non-GAAP metric, which is standard, but the treatment of the xAI AI segment's operating losses and the reconciliation from GAAP operating loss to Adjusted EBITDA will receive scrutiny. Under Regulation G and Item 10(e) of Regulation S-K, non-GAAP measures in registration statements must be presented with equal or lesser prominence than the GAAP measure, and adjustments must be described with specificity.

Revenue recognition for AI compute contracts. The $1.25 billion per month Anthropic contract disclosed in the SpaceX S-1 raises a specific revenue recognition question: how does SpaceX recognise revenue from a compute-as-a-service arrangement where the customer can terminate with 90 days' notice? Under ASC 606, the pattern of revenue recognition from a contract is determined by the performance obligations and the variable consideration framework. For a contract of this size that carries a material termination right, the allocation of consideration and the constraint on variable consideration will be closely scrutinised by the SEC staff in the comment letter process.

Segment reporting and CODM determination. For companies with complex business structures like SpaceX, the SEC staff routinely reviews how the chief operating decision maker (CODM) is identified and how the segments are defined. The inclusion of xAI as a separate segment following the February 2026 merger requires the S-1 to demonstrate that the CODM views xAI as a separate operating segment with discrete financial information reported to and used by the CODM. The segment determination directly affects what financial information must be disclosed and at what level of detail.

Dual-class share structure and corporate governance disclosure. The SEC has required progressively more detailed disclosure of dual-class voting arrangements following proxy advisory firm pressure and institutional investor focus on governance standards. The SpaceX S-1's founder voting concentration at 85.1% will require robust risk factor and prospectus cover page disclosure of the practical consequences for minority shareholders.

What Does the 2026 Tech IPO Pipeline Reveal About Where the Market Is Going?

The SpaceX S-1 is the highest-profile filing in a 2026 tech IPO pipeline that is the broadest since 2021 and qualitatively different from that cycle in several respects.

OpenAI is preparing to file a confidential draft of its IPO prospectus with the SEC, with Goldman Sachs and Morgan Stanley leading the process, targeting a public market debut in September 2026. Its current private market valuation sits at approximately $852 billion. Rival Anthropic has indicated it is targeting an October 2026 IPO, potentially at a valuation above $900 billion based on its current funding round.

Discord filed a confidential S-1 with the SEC on January 6, 2026, working with Goldman Sachs and JPMorgan Chase, targeting a $15 billion IPO in Q2 2026. Revolut filed a confidential S-1 with the SEC in early 2026 and has reportedly chosen Nasdaq over its home London market for the listing, targeting a $75 billion valuation, which would make it the largest fintech IPO of the current cycle.

Several structural characteristics distinguish this pipeline from prior cycles.

AI revenue models will face their first public disclosure test. OpenAI and Anthropic have generated tens of billions of dollars in private funding based on projected AI revenue trajectories that have never been publicly disclosed. Their S-1 filings will be the first time audited revenue figures, cost structures, customer concentration data, and the unit economics of API and enterprise AI subscription revenue are available for public scrutiny. The SpaceX S-1's xAI segment disclosure is a preview of what that analysis will require.

Valuation compression is a structural feature, not a temporary condition. The SpaceX private market valuation has remained flat for five years (Discord's private valuation has been flat since 2021 at $15 billion). These flat private valuations mean the IPO is not a valuation step-up but a liquidity event at or near the last private mark. The S-1 disclosures for these companies will need to justify current-cycle valuations to a public market investor base that was not present when the private valuations were set.

Customer concentration at the AI compute layer is a systemic risk. The Anthropic compute contract disclosed in the SpaceX S-1 illustrates a concentration pattern that will appear across multiple filings in this cycle. AI companies are both customers of each other (OpenAI, Anthropic, and other AI labs buy compute from infrastructure providers like SpaceX's Colossus) and competitors in the same application markets. This creates customer concentration and related-party disclosure questions that the SEC has not previously had to address at this scale.

The use of confidential submission has become the universal standard. Every major company in the 2026 pipeline SpaceX, Discord, Revolut, and reportedly OpenAI and Anthropic is using the confidential DRS process before filing a public S-1. This is now the expected practice rather than the exception. The confidential stage allows companies to negotiate SEC comment letter responses before market exposure, and it means the public S-1 is a more polished document than the one originally submitted for SEC review.

What Should Practitioners Read in an S-1 First?

For CFOs, bankers, investors, and disclosure counsel reading a technology company S-1, the document's structure rewards a non-linear reading approach. The sections that contain the most decision-relevant information are not necessarily the ones that appear first.

Risk factors: the most legally precise section. The risk factors section of an S-1 is drafted under the closest SEC scrutiny and the highest antifraud liability. It is where the company is required to describe the specific, material risks that could adversely affect the investment. Generic risk factors are consistently commented on by the SEC staff, who require that risk factors be specific to the company rather than applicable to any company in the same industry. The SpaceX risk factors covering launch failure rates, founder dependence, Starlink spectrum regulatory exposure across multiple countries, and the termination right in the Anthropic compute contract are specific and material. They are the sections where the company has told investors exactly what could go wrong.

MD&A: where the segment economics become visible. The Management Discussion and Analysis section is where the S-1 discloses the period-over-period changes in each segment's revenue and profitability, the factors driving those changes, and the forward-looking trends and uncertainties that management believes are likely to affect results. For a multi-segment company like SpaceX, the MD&A segment discussion is the primary location where the cross-subsidy between Connectivity and the Space and AI segments is explained analytically rather than just presented numerically.

Use of proceeds: what the company intends to do with IPO capital. The use of proceeds section reveals how management prioritises capital allocation at the moment of the IPO. For SpaceX, the use of proceeds will reflect the relative priority among Starship development, Starlink satellite constellation expansion, and xAI data centre investment. These priorities are the concrete expression of the strategic plan the IPO is financing.

Capitalization table: who owns what and what governance rights they hold. The cap table, combined with the description of the share classes, is where the governance structure of the post-IPO company becomes concrete. The 85.1% founder voting concentration in the SpaceX filing means that public shareholders purchasing SPCX shares will have economic participation but no effective governance influence. This is a material fact that belongs in the risk factor reading alongside the financial disclosures.

Audited financial statements: the only section the S-1 cannot spin. The financial statements are prepared under US GAAP, audited by a registered public accounting firm subject to PCAOB oversight, and certified by the CEO and CFO under Sarbanes-Oxley. They are the most verifiable section of the S-1 and the one where the actual economics of the business are most reliably presented. For SpaceX, the revenue breakdown, the R&D expense trajectory, and the segment-level operating income data are all in the financial statements. The narrative sections of the S-1 explain those numbers. The numbers themselves are the ground truth.

Frequently Asked Questions

What is an S-1 filing and when must a company file one?

An S-1 is a registration statement filed with the SEC under the Securities Act of 1933 that a company must submit before conducting an initial public offering of securities in the United States. The S-1 must contain audited financial statements, a business description, risk factors, MD&A, executive compensation disclosure, a capitalisation table, and the terms of the offering. For large companies, the process typically begins with a confidential Draft Registration Statement submitted to the SEC for private review, followed by the public S-1 filing, which must be available for at least 15 calendar days before the investor roadshow.

What did SpaceX disclose in its May 2026 S-1 filing?

SpaceX's S-1, filed May 20, 2026, disclosed three operating segments: Space (rocket launch), Connectivity (Starlink), and AI (xAI, consolidated following the February 2026 merger). The company reported $18.674 billion in 2025 revenue, a $2.589 billion operating loss, and $6.584 billion in Adjusted EBITDA for 2025. R&D expenses reached $8.643 billion in 2025, reflecting aggressive investment in xAI infrastructure and Starship development. The Connectivity (Starlink) segment is the sole profitable segment. Elon Musk holds 85.1% of voting power through a dual-class share structure. The Anthropic compute contract $1.25 billion per month through May 2029, terminable with 90 days' notice is a material disclosed customer relationship.

What is the confidential S-1 submission process and why do large tech companies use it?

The confidential submission process, also called a Draft Registration Statement (DRS) submission, allows a company to file a draft S-1 with the SEC for private review before making it public. The SEC staff reviews the draft, issues comment letters, and the company responds and revises. The public S-1 is filed after that iterative process is complete. Large technology companies use confidential submissions because it allows them to negotiate SEC comment letter responses without market and media scrutiny, and ensures the public filing is a polished document that has already addressed SEC staff concerns.

What is the 2026 tech IPO pipeline and who is expected to go public?

The major technology companies at various stages of the 2026 IPO process include SpaceX (public S-1 filed May 20, 2026, targeting Nasdaq listing under SPCX in June 2026), Discord (confidential S-1 filed January 2026, targeting $15 billion valuation), Revolut (confidential S-1 filed early 2026, targeting $75 billion valuation on Nasdaq), OpenAI (confidential DRS reportedly being filed, targeting September 2026 debut at approximately $852 billion valuation), and Anthropic (targeting October 2026 IPO at above $900 billion valuation). 2026 is on track to be the most significant year for large technology IPO activity since 2021.

What SEC scrutiny areas apply to technology company S-1 filings?

The SEC staff's review of technology IPO registration statements consistently focuses on several areas: the presentation and reconciliation of non-GAAP financial measures, particularly EBITDA and adjusted profitability metrics; revenue recognition policies for complex arrangements including SaaS, API usage, and compute-as-a-service contracts; segment reporting and the basis for CODM determination; dual-class share structure disclosure; risk factor specificity; and customer concentration disclosure where a small number of customers represent a material share of revenue.

What are the most important sections to read in a technology company S-1?

The risk factors section is the most legally precise and specifically tailored to the company's actual risks. The MD&A section contains the segment-level financial analysis and forward-looking trend disclosure. The use of proceeds section reveals capital allocation priorities. The capitalisation table and share class description clarify governance rights. The audited financial statements are the most reliable section because they are prepared under GAAP and audited by a PCAOB-registered firm. Reading these five sections before the business description and the underwriter narrative gives a more accurate picture of the company's actual economics and risks.

Key Takeaways

- The SpaceX S-1, filed May 20, 2026, is the largest and most complex technology company IPO filing in history. It discloses $18.674 billion in 2025 revenue across three segments, with Starlink (Connectivity) as the only profitable segment funding investment in the Space and AI (xAI) segments. R&D expenses grew at 60% CAGR from 2023 to 2025, reaching $8.643 billion in 2025.

- The dual-class share structure in the SpaceX S-1 concentrates 85.1% of voting power in Elon Musk, which represents the most extreme founder control concentration in any major technology IPO to date. Public shareholders will have economic participation but no effective governance influence.

- 2026 is the most significant year for large technology IPO activity since 2021. SpaceX, Discord, Revolut, OpenAI, and Anthropic are all at various stages of the SEC filing process. OpenAI and Anthropic will make their financials publicly available for the first time when they file, creating the largest single transparency event the AI industry has produced.

- The confidential DRS process is now the universal standard for large technology IPOs. Every major company in the 2026 pipeline used confidential submission before the public S-1 filing, which means the public document has already been through SEC comment letter review.

- SEC scrutiny of technology S-1 filings in 2026 is concentrated on non-GAAP measure presentation, revenue recognition for AI compute contracts, segment reporting, dual-class governance disclosure, and customer concentration. The Anthropic compute contract in the SpaceX S-1, which is terminable with 90 days' notice at $1.25 billion per month, is an example of a disclosure that will generate specific SEC review.

- For practitioners reading an S-1, the risk factors, MD&A segment discussion, use of proceeds, cap table, and audited financial statements are the five sections that contain the most decision-relevant information. The business description and underwriter narrative sections should be read second.