A public company that misses a periodic filing deadline without filing Form 12b-25 is delinquent from the moment the original deadline passes. That delinquency can trigger consequences that extend well beyond the missed report: loss of S-3 or F-3 eligibility, loss of WKSI status, exchange delisting notices, and in cases of repeated or egregious delay, SEC enforcement action. Form 12b-25 commonly referred to in EDGAR as the "NT" (notification of late filing) is the mechanism the SEC provides to preserve a company's filing timeliness record when a report cannot be completed by its original due date.

But Form 12b-25 is not a procedural formality. The SEC has brought enforcement actions against companies for incomplete or inaccurate Form 12b-25 disclosures, imposing penalties ranging from $35,000 to $60,000 per company, with the violations characterised as strict liability meaning no evidence of bad intent is required. What goes on the form, and specifically what the disclosure of the delay reason says, carries legal consequences that compliance teams need to understand before the next deadline crisis arrives.

This post maps the entire Form 12b-25 process precisely, in the sequence your team encounters the questions when a filing deadline is approaching and the report is not ready.

What Is Form 12b-25 and When Is It Required?

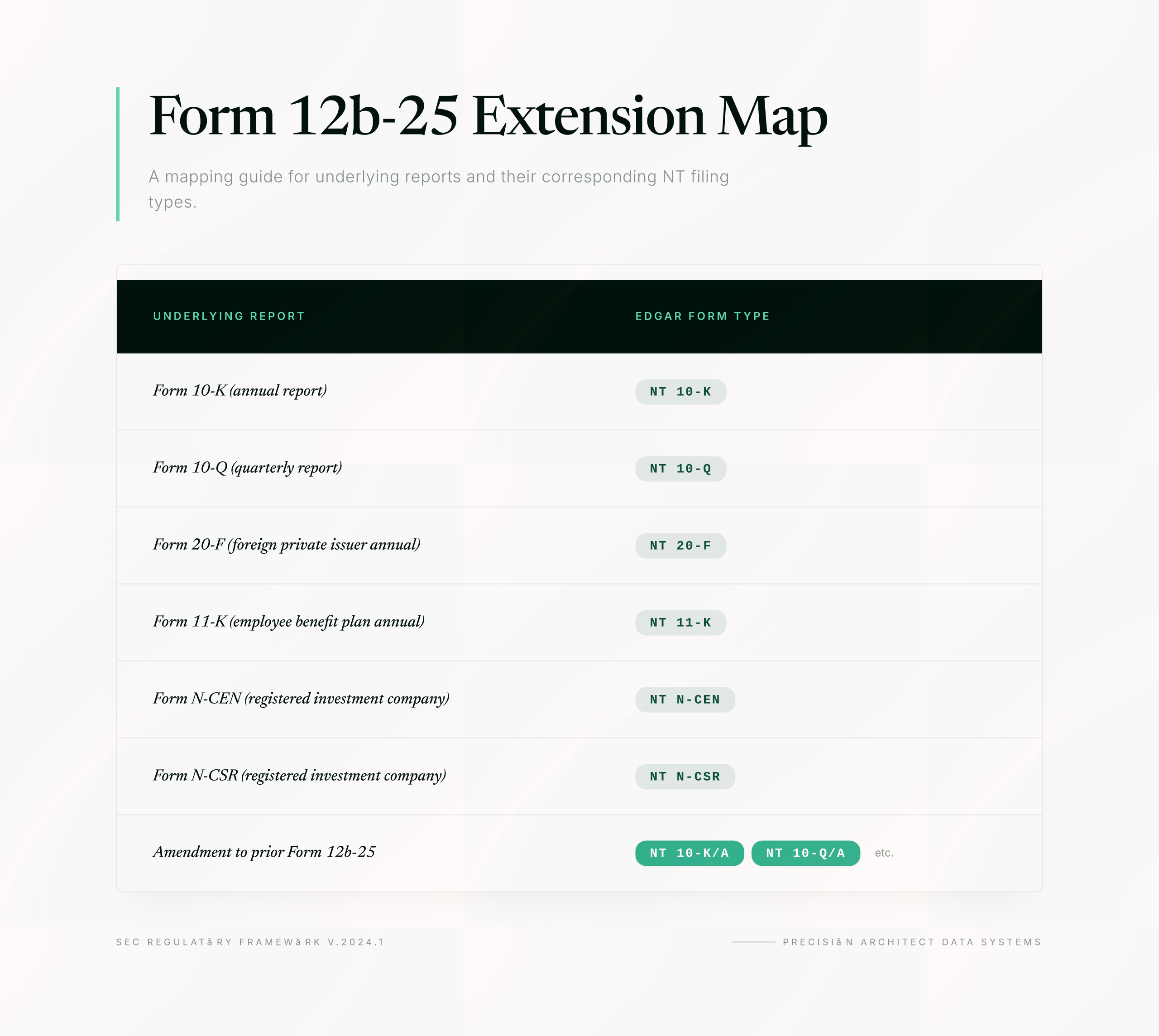

Form 12b-25 is an SEC form filed under Exchange Act Rule 12b-25 that notifies the SEC of a public company's inability to file a required periodic report by its original deadline. It is commonly called a "Form NT" because EDGAR designates the filings as NT 10-K, NT 10-Q, NT 20-F, NT 11-K, or NT N-CEN depending on which underlying report is delayed.

Form 12b-25 is required not optional when a company cannot file a periodic report on time and wants to preserve its timely filing status and avoid the consequences of delinquency. Filing Form 12b-25 does not guarantee that a company avoids all consequences of a late filing. What it does is preserve the company's ability to have the underlying report treated as timely filed, provided the company files the actual report within the extension period granted under Rule 12b-25.

According to Exchange Act Rule 12b-25 and the SEC's formal instructions, Form 12b-25 is available for delayed filings of Form 10-K, Form 10-Q, Form 20-F, Form 11-K, Form N-CEN, and Form N-CSR. It is not available as an extension mechanism for Form 8-K. A company that cannot file a Form 8-K on time has no Form 12b-25 equivalent and is simply delinquent from the moment the 8-K deadline passes.

Form 12b-25 is also not available to cure delays caused solely by technical difficulties with EDGAR. According to the SEC's Form 12b-25 instructions, electronic filers unable to submit a report within the prescribed time period due to difficulties in electronic filing should comply with either Rule 201 or Rule 202 of Regulation S-T (relating to hardship exemptions and temporary hardship exemptions) or apply for an adjustment in filing date pursuant to Rule 13(b) of Regulation S-T. The Form 12b-25 is designed for substantive delays delays in the preparation or completion of the report itself, not delays in the transmission of a completed report to EDGAR.

When Is Form 12b-25 Due After a Missed Deadline?

Form 12b-25 must be filed with the SEC by 5:30 p.m. Eastern Time no later than one business day after the original due date of the periodic report. This is a hard deadline with no flexibility. A Form 12b-25 filed two business days after the original deadline is itself late and does not preserve the company's ability to claim the Rule 12b-25 extension.

The calculation of the Form 12b-25 due date depends on whether the original report deadline fell on a business day, a weekend, or a federal holiday.

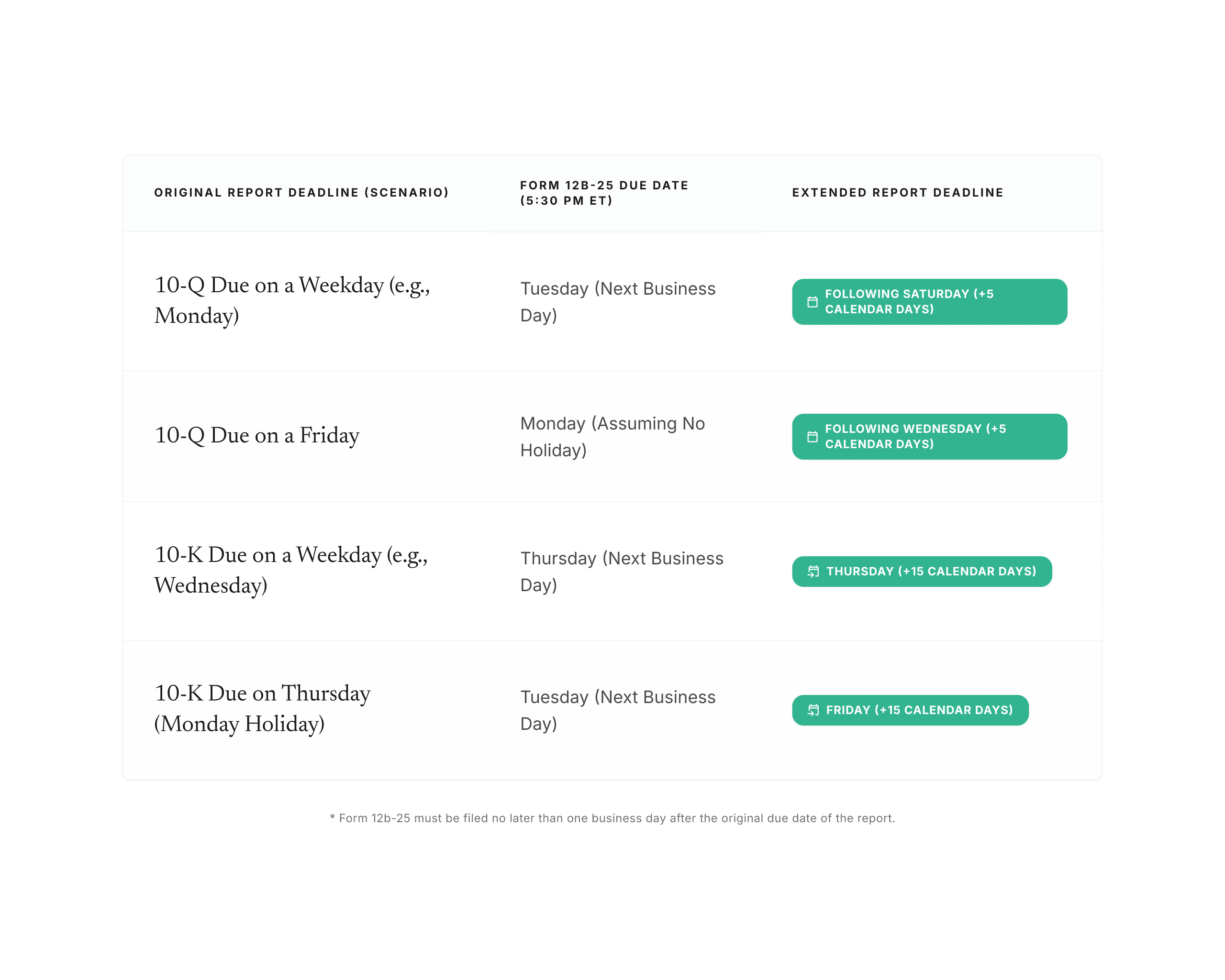

When the original report deadline is a business day. The Form 12b-25 is due the next business day after that deadline. For example, if a Form 10-Q is due on a Friday, the Form 12b-25 must be filed by 5:30 p.m. ET on the following Monday (assuming Monday is not a federal holiday).

When the original report deadline falls on a Saturday, Sunday, or federal holiday. Under Exchange Act Rule 0-3, a periodic report due on a Saturday, Sunday, or federal holiday is considered timely filed on the next business day. The Form 12b-25 is then due no later than the second business day after the original due date. According to PwC's SEC Volume guidance on Form 12b-25, if a Form 10-Q is originally due on a Saturday, the Form 10-Q would be considered timely filed on Monday, and the Form 12b-25 would be due no later than Tuesday. This is because the Form 12b-25 must be filed within one business day after the effective due date, not one business day after the original calendar deadline.

The 5:30 p.m. ET cut-off. EDGAR accepts filings around the clock, but SEC rules specify that the Form 12b-25 must be filed by 5:30 p.m. ET on the required filing day. A Form 12b-25 filed at 6:00 p.m. ET on the due date is technically a next-day filing and may be treated as late. Compliance teams should target submitting the Form 12b-25 well before the 5:30 p.m. cut-off to avoid any time-of-day issues.

What Extension Does Form 12b-25 Actually Provide?

Filing Form 12b-25 does not grant an open-ended extension. Rule 12b-25 provides a fixed extension period that varies by report type. The extension period is measured in calendar days from the original due date of the report, not from the date the Form 12b-25 is filed.

Form 10-Q extensions. Filing a Form 12b-25 for a delayed quarterly report on Form 10-Q provides an additional five calendar days from the original due date. If the Form 10-Q was due on a Monday, the extended deadline is the following Saturday. If that Saturday is not a business day, the extended deadline remains Saturday the extension period is five calendar days, not five business days, and the calendar days count from the original due date regardless of weekends.

Form 10-K and Form 20-F extensions. Filing a Form 12b-25 for a delayed annual report on Form 10-K or Form 20-F provides an additional fifteen calendar days from the original due date.

Form 11-K extensions. Filing a Form 12b-25 for a delayed annual report on Form 11-K also provides fifteen calendar days.

The extension period start date matters. According to PwC's analysis, if the original due date of the periodic report was not a Saturday, Sunday, or holiday, the extension period begins to run from the day the periodic report was originally due. If the original due date was a Saturday, Sunday, or holiday (so that the report was considered timely filed on the next business day under Rule 0-3), then the extension period begins to run from that next business day.

The extension is not renewable. Rule 12b-25 provides one extension and one extension only. There is no mechanism to file a second Form 12b-25 to extend the extended deadline. If the company cannot complete and file the delayed report within the Rule 12b-25 extension period, no further extensions are available under Rule 12b-25 and the company will be considered delinquent as of the original filing due date.

The condition for timely deemed filing. The Form 12b-25 does not itself cause the late report to be deemed timely filed. The late report is deemed to have been filed as of the original due date only if two conditions are both met: the Form 12b-25 was timely filed (by 5:30 p.m. ET on the business day after the original deadline), and the actual report is filed within the extension period. If the actual report is filed one day after the extension period ends, the deemed-timely-filed treatment is lost and the report is delinquent from the original due date.

What Must Form 12b-25 Contain?

Form 12b-25 is a substantive disclosure document, not a bare notification checkbox. The SEC's enforcement history makes clear that incomplete or misleading Form 12b-25 disclosures carry their own legal consequences. Here is precisely what the form requires.

Identification of the report and registrant. The form must identify the report that cannot be filed timely (by form type: 10-K, 10-Q, 20-F, etc.), the period covered by the report, and the full legal name and SEC file number of the registrant. The form must also indicate the subject company's exchange listing or the fact that it is an unlisted OTC registrant.

The reason for delay the most consequential element. Rule 12b-25 requires the registrant to explain in reasonable detail why it is unable to file the report within the prescribed time period. The explanation must be specific. Vague statements such as "additional time is needed to complete the financial statements" without any additional context are insufficient. The SEC has specifically charged companies for inadequate delay reason disclosures, including for failing to disclose that an anticipated restatement or correction of prior financial reporting was a principal reason for the delay.

According to the Public Company Advisory Blog's analysis of SEC enforcement of Form NT disclosure requirements, the SEC instituted and settled proceedings against five public companies for failing to disclose in Form 12b-25 that their request for a delayed filing was caused by an anticipated restatement or correction of prior financial reporting, with penalties ranging from $35,000 to $60,000 per company. These are strict liability violations. The SEC does not need to prove bad intent. It only needs to establish that a material disclosure was omitted from the Form NT.

The unreasonable effort or expense representation. Form 12b-25 requires the registrant to represent that the report cannot be filed without unreasonable effort or expense. This representation is a condition to the deemed-timely-filed treatment. If the reasons for the delay could have been eliminated without unreasonable effort or expense, the Rule 12b-25 extension is not available and the representation would be false.

Anticipated changes in results of operations. Form 12b-25 requires the registrant to indicate whether it anticipates any significant change in its results of operations from the comparable prior period. If the registrant does anticipate a significant change, it must either provide a narrative description and quantitative estimate of the change, or explain why a reasonable estimate cannot be made. The SEC's enforcement actions confirm that this disclosure is taken seriously: companies that omitted anticipated changes in results of operations from their Form NT filings while simultaneously announcing restatements or corrections within weeks of the filing have been charged under strict liability standards.

Changes in corporate structure or management. Form 12b-25 asks whether the registrant has had any changes in its corporate structure or management that are relevant to the inability to file timely. This requires affirmative consideration, not merely a boilerplate negative answer.

Amendments. Form 12b-25 instructions clarify that amendments to a previously filed Form 12b-25 must also be filed on Form 12b-25, clearly identified as an amendment. An amendment need not restate information that was correctly furnished in the original filing.

How Do You File Form 12b-25 on EDGAR?

Form 12b-25 is filed electronically through EDGAR. The EDGAR form type designation depends on which underlying report is delayed:

Step 1: Access EDGAR. Log in to the EDGAR filing system at edgar.sec.gov using the company's EDGAR account credentials. If the company does not have EDGAR access, the filing can be submitted by a filing agent, but the form must still be filed under the company's own CIK number.

Step 2: Select the correct form type. Navigate to the filing submission area and select the appropriate NT form type from the list above. Selecting the wrong form type for example, filing an NT 10-K for a delayed 10-Q is an error that must be corrected by filing an amendment.

Step 3: Complete the form fields. Fill in all required fields: registrant name, CIK number, period of report, exchange listing information, the reason for delay (in sufficient detail), the unreasonable effort or expense representation, anticipated changes in results of operations, and any relevant corporate changes. Every field should be reviewed by the company's legal counsel before submission.

Step 4: Attach the narrative explanation. The narrative explanation of the reason for delay should be attached as a document exhibit to the EDGAR filing, not merely entered in a text box. A clearly labelled, complete narrative is more defensible in an SEC review than a compressed text field entry.

Step 5: Submit by 5:30 p.m. ET on the required day. Submit the completed filing before the 5:30 p.m. ET deadline. After submission, EDGAR generates an acceptance confirmation and a filing date and time stamp. Save the confirmation. The timestamp is the evidence that the Form 12b-25 was filed on time.

Step 6: File the actual report within the extension period. After the Form 12b-25 is accepted, the clock for the extension period is running from the original report due date. The actual Form 10-Q, 10-K, or other delayed report must be filed within five calendar days (10-Q) or fifteen calendar days (10-K) of the original due date to receive deemed-timely-filed treatment.

What Are the Consequences of Filing Form 12b-25 or Missing the Extended Deadline?

Filing Form 12b-25 has consequences beyond the extension itself that every SEC reporting team and CFO needs to understand before using it.

S-3 and F-3 eligibility. Form S-3 and Form F-3 require that the registrant have timely filed all required Exchange Act reports during the preceding 12 months. A Form 12b-25 filed in a timely manner, where the underlying report is filed within the Rule 12b-25 extension period, preserves the deemed-timely-filed status of that report. If the underlying report is not filed within the extension period, the report is delinquent from the original due date, and S-3 or F-3 eligibility is lost for 12 full calendar months from the original filing due date.

According to Winston and Strawn's Late SEC Filings Guide, a company that misses its 10-K deadline on March 16 but files all subsequent periodic reports on time will not be eligible to use Form S-3 or Form F-3 until April 1 of the following year. During that 12-month period, the company cannot conduct registered shelf offerings or file effective registration statements on Form S-3 or F-3, absent a waiver from the SEC.

WKSI status. Well-Known Seasoned Issuers (WKSIs) benefit from automatic shelf registration and other simplified registration procedures. WKSI status requires meeting the S-3 or F-3 eligibility requirements. A company that loses S-3 eligibility due to a late filing also loses WKSI status. A company that relied on WKSI status for a pending or planned offering must reassess its offering plan immediately upon losing that status.

Capital markets access during the Rule 12b-25 grace period. During the Rule 12b-25 extension period (between the original filing deadline and the extended deadline), an already effective registration statement remains operative. However, a registration statement cannot generally be filed or declared effective during this grace period. According to the Troutman Pepper 2026 SEC filing deadlines guide, the SEC typically allows filing or effectiveness of a registration statement during the gap period for timely filers who have filed a Form 12b-25, subject to confirmation that the quarterly report will be timely filed and that there have been no material adverse developments since the balance sheet date.

Exchange listing notices. Companies listed on the NYSE and Nasdaq are required by applicable stock exchange listing standards to issue a press release when a Form 12b-25 is filed. The press release must be issued not later than the day on which the Form 12b-25 is filed. Failure to issue the required press release is a separate listing standards violation. Both NYSE and Nasdaq may issue deficiency notices to companies that file Form 12b-25, particularly where the delay suggests a potential material issue with the company's financial reporting.

SEC enforcement risk. The SEC's enforcement actions demonstrate that Form 12b-25 is an active monitoring target. The SEC has charged companies not only for failing to file Form 12b-25 when required but also for inadequate disclosures within Form 12b-25. Enforcement is on a strict liability basis. The SEC has also suspended trading in securities of companies with recurring or egregious late filing patterns and has instituted administrative proceedings seeking revocation of Exchange Act registration, though these more severe remedies are reserved for the most serious violations.

No extension for Form 8-K. Form 8-K does not have a Form 12b-25 equivalent. A company that cannot file a Form 8-K on time (current event reporting within four business days of a triggering event) has no formal extension mechanism and is delinquent from the moment the deadline passes. The Form 12b-25 is available only for periodic reports, not for current event reports.

What Should the Reason for Delay Disclose?

The reason for delay is the most legally significant element of Form 12b-25. Based on the SEC's published enforcement history, here is a practical framework for what the disclosure must include and what it must not omit.

Disclose the specific operational cause. The disclosure should identify the specific factual reason the report cannot be completed: the departure of a key finance executive, a complex valuation requiring additional specialist input, a material acquisition that requires preparation of target financial statements, a system failure affecting financial data extraction, or an identified error in previously reported financial information that requires analysis before the current period can be completed. General statements like "additional time is needed" are inadequate.

Disclose anticipated restatements or corrections. If the delay is caused in whole or in part by an anticipated restatement, correction of financial statements, or material error in prior period reporting, that cause must be disclosed in the Form 12b-25. The SEC's enforcement actions against multiple companies for omitting anticipated restatement disclosures from Form NT filings establish that this is a mandatory disclosure, not a judgment call. The fact that the restatement has not yet been finalised, quantified, or publicly announced does not excuse the omission if it is a principal reason for the delay.

Disclose anticipated significant changes in results. If the company anticipates that results for the period will differ significantly from the comparable prior period, that information must be disclosed on the Form 12b-25. Companies that were in the process of recording material write-downs, impairment charges, or other adjustments that will affect the reported results for the quarter have been charged for failing to disclose those anticipated changes in their Form NT filings.

Do not misrepresent the filing timeline. Form 12b-25 asks the registrant to state whether it expects to file the delayed report within the extension period. If the company knows at the time of filing that the report cannot be completed within five or fifteen calendar days, representing otherwise on the Form 12b-25 is a misrepresentation. The company should file the Form 12b-25, represent what is accurate about the expected timeline, and plan for the consequences of missing the extended deadline if that outcome is likely.

Legal review before submission. Every Form 12b-25 should be reviewed by outside securities counsel before submission. The form's legal consequences for what it says, what it omits, and what it represents about the registrant's financial reporting situation exceed those of most routine compliance filings. The cost of that review is insignificant relative to the cost of an SEC enforcement investigation.

What Is the Waiver Process If the Extended Deadline Cannot Be Met?

If a company cannot file the delayed report within the Rule 12b-25 extension period and wants to preserve its S-3 or F-3 eligibility, it may apply to the SEC for a waiver of the S-3 or F-3 timeliness requirement.

According to Winston and Strawn's analysis, the waiver request must be in writing and addressed to the SEC's Office of the Chief Counsel. It is not submitted through EDGAR. The waiver request should describe the company's situation including whether it has an existing Form S-3 or F-3, the circumstances of the late filing, the reason the company was unable to file on time, and the plan and timeline for filing the delayed report.

The waiver request is evaluated by SEC staff on a case-by-case basis. There is no guaranteed outcome. Companies that have a history of timely filing and can demonstrate a genuine extraordinary circumstance causing the delay are more likely to receive favorable consideration than companies with a pattern of late filings or those whose delay is attributable to internal control failures or financial restatements. The SEC staff notifies the company of its determination by phone. The waiver process itself is not public and does not appear on EDGAR.

For companies that lose S-3 eligibility due to a late filing without a waiver, the 12-month waiting period begins from the original filing due date of the delayed report. After 12 full calendar months of timely filing following that date, the company regains S-3 eligibility provided it otherwise meets all other S-3 requirements.

Frequently Asked Questions

What is Form 12b-25 and what does filing it do?

Form 12b-25, also called Form NT, is an SEC form filed under Exchange Act Rule 12b-25 that notifies the SEC when a public company cannot file a required periodic report by its original deadline. Filing Form 12b-25 by 5:30 p.m. ET on the business day after the original deadline provides an extension of five calendar days for Form 10-Q and fifteen calendar days for Form 10-K and Form 20-F. If the company files the actual report within that extension period, the report is deemed to have been filed as of the original due date. Filing Form 12b-25 does not eliminate all consequences of a late filing, including exchange listing notice obligations.

When must Form 12b-25 be filed?

Form 12b-25 must be filed by 5:30 p.m. Eastern Time no later than one business day after the original due date of the periodic report. If the original report deadline fell on a Saturday, Sunday, or federal holiday so that the report's effective deadline under Rule 0-3 was the next business day the Form 12b-25 is due no later than the second business day after the original calendar deadline. A Form 12b-25 filed after this deadline does not preserve the company's timely filing status.

What extension does Form 12b-25 provide for a 10-Q versus a 10-K?

Form 12b-25 provides five calendar days from the original due date for a late Form 10-Q. For a late Form 10-K or Form 20-F, it provides fifteen calendar days from the original due date. These are calendar days, not business days, meaning weekends count. The extension cannot be renewed Rule 12b-25 provides one extension period and no mechanism for a second extension.

What happens if the report is not filed within the Form 12b-25 extension period?

If the company does not file the actual report within the Rule 12b-25 extension period, the report is considered delinquent as of the original filing due date. No further extensions are available. The company loses S-3 and F-3 eligibility for twelve full calendar months from the original filing due date and loses WKSI status if applicable. The SEC may issue trading suspension orders for companies with recurring or egregious late filing patterns. If the company wants to try to preserve its S-3 eligibility despite missing the extended deadline, it must apply in writing for a waiver to the SEC's Office of the Chief Counsel.

Does Form 12b-25 need to disclose the reason for the delay?

Yes, and the disclosure must be specific and complete. Rule 12b-25 requires a detailed explanation of why the report cannot be filed without unreasonable effort or expense. Vague explanations are insufficient. The SEC has charged companies under strict liability standards for failing to disclose that an anticipated restatement or material error was a principal reason for the delay, and for failing to disclose anticipated significant changes in results of operations. Every Form 12b-25 should be reviewed by securities counsel before submission.

Is Form 12b-25 available for a late Form 8-K?

No. Form 12b-25 is available only for periodic reports: Form 10-K, Form 10-Q, Form 20-F, Form 11-K, Form N-CEN, and Form N-CSR. There is no Form 12b-25 equivalent for current event reports on Form 8-K. A company that cannot file a Form 8-K within the four-business-day deadline has no extension mechanism and is delinquent from the moment the deadline passes.

Can Form 12b-25 be filed for electronic filing difficulties?

No. Form 12b-25 may not be used by electronic filers who are unable to file solely due to EDGAR technical difficulties. Filers experiencing EDGAR technical problems should seek a hardship exemption under Rule 201 or Rule 202 of Regulation S-T or apply for a filing date adjustment under Rule 13(b) of Regulation S-T.

Key Takeaways

- Form 12b-25 must be filed by 5:30 p.m. ET no later than one business day after the original periodic report deadline. Missing this window means the Form 12b-25 itself is late and the extension is unavailable.

- The extension period is five calendar days for Form 10-Q and fifteen calendar days for Form 10-K and Form 20-F, measured from the original due date. These are calendar days. There is no second extension under Rule 12b-25.

- The reason for delay disclosure on Form 12b-25 is a substantive legal disclosure subject to strict liability enforcement. If an anticipated restatement, correction of financial statements, or anticipated significant change in results of operations is a principal reason for the delay, it must be disclosed. Companies have been charged and penalised for omitting these disclosures.

- If the delayed report is not filed within the extension period, the company loses S-3 and F-3 eligibility for twelve full calendar months from the original filing due date. WKSI status is also lost. A waiver can be sought from the SEC's Office of the Chief Counsel, but is not guaranteed.

- Form 12b-25 is not available for Form 8-K delays and is not available when the delay is caused solely by EDGAR technical difficulties. For technical difficulties, use Regulation S-T hardship exemption procedures.

- NYSE and Nasdaq require a press release to be issued no later than the day a Form 12b-25 is filed. This exchange listing obligation exists independently of the SEC filing obligation.