Most CFO teams have a month-end financial close checklist. The problem is that most of those checklists were built for speed, not for the SEC.

A checklist that gets your books closed on time is not the same as a checklist that holds up to SEC scrutiny, auditor review, or a comment letter from the Division of Corporation Finance. The gap between those two versions is exactly where reporting errors, review loops, and late filings live.

In this post, you'll learn the specific steps that experienced SEC reporting teams miss most often, how those gaps create downstream risk, and how mapping your checklist items to the right Accounting Standards Codification (ASC) guidance closes that gap before it costs you.

What Is a Month-End Financial Close Checklist for SEC Reporting Teams?

A month-end financial close checklist is a structured sequence of tasks that ensures all financial transactions are recorded, reconciled, and reviewed before period-end reporting is finalized. For SEC reporting teams, the checklist goes further: it must also verify that every disclosure is accurate, consistent with prior periods, benchmarked against peer filings, and defensible under SEC review.

For SEC registrants, a standard accounting close checklist is a starting point, not a finish line. The additional layer required for public company reporting covers disclosure integrity, ASC standard compliance, MD&A (Management Discussion and Analysis) consistency, and audit-readiness of supporting documentation.

Teams that treat close and reporting as sequential---close first, then worry about SEC---consistently run into the same problems at filing time. According to the SEC's Division of Corporation Finance, the most common comment letter topics in 2024 were MD&A, revenue recognition, and non-GAAP measures---all areas that require attention during the close cycle, not after it (SEC, 2024). SEC Chief Accountant Paul Munter stated in a 2024 speech that "the quality of financial reporting begins long before the filing date; it starts with the close process itself."

Why Standard Close Checklists Fail SEC Reporting Teams

Most month-end close checklists in circulation today are adapted from general accounting practice. They cover reconciliations, journal entry sign-offs, subledger-to-GL ties, and intercompany eliminations. Those are necessary, but they are not sufficient for an SEC registrant.

A KPMG survey of SEC reporting teams found that 67% of controllers at public companies said their close checklist had not been updated in the prior two years to reflect new SEC guidance or ASC standard changes (KPMG, 2024). Here is what a standard checklist typically misses:

Disclosure consistency across periods. A reconciliation confirms your numbers tie. It does not confirm that the language describing those numbers in your MD&A is consistent with what you said last quarter. The SEC frequently issues comment letters specifically about unexplained quarter-over-quarter changes in MD&A language, not the numbers themselves.

ASC standard applicability checks. If your lease portfolio changed, ASC 842 (Leases) implications need to be reviewed. If you recognized a new revenue stream, ASC 606 (Revenue from Contracts with Customers) disclosure requirements apply. Most checklists don't include a standing prompt to assess which standards were triggered by activity in the period.

Peer benchmarking of key disclosures. The SEC evaluates your disclosures in the context of what your industry peers are saying. A disclosure that is technically accurate but materially thinner than what comparable companies are filing can generate a comment letter asking you to expand it.

Comment letter history review. If the SEC has previously issued your company a comment letter about a specific disclosure area, segment reporting, goodwill impairment, cybersecurity risk factors, that area needs heightened review every period. Standard checklists don't include this item.

XBRL tagging accuracy. Your EDGAR (Electronic Data Gathering, Analysis, and Retrieval) submission requires XBRL-tagged financial data. Tagging errors are flagged by the SEC's automated review systems before a human reviewer ever looks at your filing. This step belongs in the close checklist, not as an afterthought at submission time.

The 10 Checklist Items SEC Reporting Teams Consistently Miss

The following items are not theoretical gaps. They are the items that generate SEC comment letters, cause audit review loops, and create last-minute filing pressure. According to Audit Analytics, the SEC issued over 2,200 comment letters to public company registrants in fiscal year 2024 (Audit Analytics, 2024). PCAOB Chair Erica Williams noted in her 2024 annual report address that "we continue to see audit deficiencies tied to areas where preparers did not adequately evaluate the applicability of evolving accounting standards." For each item below, the relevant ASC guidance or regulatory reference is included.

1. MD&A Language Consistency Review

What it is: A line-by-line comparison of your current period MD&A draft against the prior period filing, flagging any substantive language changes that are not explained by quantitative changes in the results.

Why teams miss it: MD&A review is treated as an editorial step, not a compliance step. Writers focus on updating the numbers. The SEC focuses on the narrative.

What the SEC looks for: According to the SEC's Division of Corporation Finance guidance on MD&A, the discussion must explain the reasons behind material changes, not just the changes themselves. Comment letters frequently cite MD&A sections that describe results without analysis.

Checklist item to add: Compare current MD&A draft to prior period filing paragraph by paragraph. Flag every narrative change. For each flagged change, confirm either (a) a corresponding quantitative change exists and is explained, or (b) a disclosure note explains the narrative shift.

2. ASC Standard Applicability Assessment

What it is: A standing agenda item that asks: which ASC standards were triggered by business activity in this period?

Why teams miss it: ASC applicability is assumed to be a one-time setup task at the beginning of the fiscal year. In practice, business events, acquisitions, new contracts, lease modifications, debt restructurings, can trigger new ASC standard applicability at any period-end.

Standards most commonly triggered mid-year:

- ASC 842: triggered by lease modifications, new leases, or sale-leaseback transactions

- ASC 606: triggered by new contract structures or variable consideration arrangements

- ASC 350: triggered by goodwill impairment indicators (stock price decline, reporting unit underperformance)

- ASC 280: triggered by changes in segment structure or management reporting changes

The FASB Accounting Standards Codification is the authoritative source for all ASC standard requirements and applicability criteria.

Checklist item to add: Review the period's significant transactions against an ASC trigger matrix. Document the assessment. If a new standard is triggered, initiate the disclosure draft before close sign-off.

3. SEC Comment Letter History Check

What it is: A review of your company's historical SEC comment letters, specifically identifying any disclosure areas the SEC has previously flagged.

Why teams miss it: Comment letter history is treated as a one-time legal matter rather than an ongoing compliance input. Once a comment letter is resolved, teams move on, until the next one arrives about the same disclosure area.

What the data shows: According to Deloitte's 2025 Roadmap to SEC Comment Letter Considerations, the most frequently commented disclosure areas in 10-K filings are MD&A, segment reporting, non-GAAP financial measures, and revenue recognition. These are not random, they are areas where the SEC consistently finds disclosure gaps across registrants.

Checklist item to add: At the start of each close cycle, pull your company's EDGAR comment letter history. Flag any previously raised disclosure areas. Elevate those areas to a heightened review step in the current period's checklist.

4. Non-GAAP Financial Measure Reconciliation and Compliance Check

What it is: Verification that every non-GAAP measure disclosed, Adjusted EBITDA, Free Cash Flow, Adjusted EPS, includes a GAAP reconciliation and complies with SEC Regulation G and the updated C&DI guidance.

Why teams miss it: Non-GAAP measures are often drafted by investor relations teams and reviewed by finance separately from the formal close process. The SEC's updated compliance and disclosure interpretations (C&DIs) on non-GAAP measures have become progressively more specific, and teams using guidance from 2022 or earlier may be out of step.

The SEC's current position: The SEC has increasingly scrutinized non-GAAP measures that exclude recurring charges, present non-GAAP measures more prominently than GAAP measures, or lack sufficient explanatory context. The SEC's C&DI on non-GAAP financial measures is the controlling document.

Checklist item to add: For every non-GAAP measure: (a) confirm a GAAP reconciliation is present, (b) confirm the GAAP measure appears with equal or greater prominence, (c) confirm the description of excluded items is accurate for the current period.

5. Segment Reporting Review Under ASC 280

What it is: A documented assessment of whether your reportable segment structure still reflects how the chief operating decision maker (CODM) views and manages the business.

Why teams miss it: Segment reporting is reviewed annually for the 10-K and assumed to be unchanged for interim periods. But management reporting changes, new P&L views, reorganizations, changes in how performance is measured, can change what ASC 280 requires in the very quarter they occur.

The ASC 280 test: Under ASC 280, reportable segments are determined by how the CODM allocates resources and assesses performance. If that changed during the period, your segment disclosures must change too, regardless of when your annual reporting cycle occurs.

Checklist item to add: Confirm with the finance leadership team that the CODM's internal management reporting view is unchanged. If any reorganization, reallocation, or reporting change occurred, initiate an ASC 280 reassessment before close sign-off.

6. Earnings Per Share (EPS) Dilution Check Under ASC 260

What it is: Verification that your diluted EPS calculation captures all potentially dilutive securities, options, RSUs, warrants, convertible debt, under the correct treasury stock or if-converted method.

Why teams miss it: EPS calculations are assumed to be routine. The complexity comes from securities issued or modified during the period, particularly equity awards with performance conditions and convertible instruments issued or retired during the quarter.

What the SEC flags: EPS is consistently among the top five comment letter topics according to the PCAOB's annual inspection findings and Deloitte's comment letter roadmap. Common issues include failure to include antidilutive securities in the disclosure of excluded securities, and incorrect application of the if-converted method for convertible debt.

Checklist item to add: Run diluted EPS calculation through a dedicated review step. For any securities issued or modified in the period, document the dilution methodology applied and confirm it is consistent with ASC 260.

7. Related Party Transaction Disclosure Review

What it is: A review of all transactions between the registrant and related parties, executives, directors, significant shareholders, affiliates, to confirm they are fully disclosed under ASC 850.

Why teams miss it: Related party disclosures are often treated as annual boilerplate. Material related party transactions that occur during interim periods are sometimes captured in the annual filing but not disclosed in the 10-Q where they first occur.

The standard:ASC 850 requires disclosure of material related party transactions in each period they occur, not just annually. The SEC has issued comment letters citing registrants for incomplete or delayed related party disclosures.

Checklist item to add: Confirm with legal and compliance that all related party transactions in the period have been identified, that ASC 850 materiality has been assessed, and that disclosure language is current.

8. Cybersecurity Incident Assessment for Disclosure Purposes

What it is: A standing review item confirming whether any cybersecurity incident occurred during the period that meets the SEC's materiality threshold for disclosure under the 2023 cybersecurity disclosure rules.

Why teams miss it: Cybersecurity incidents are managed by IT and legal. Finance and SEC reporting teams are not always included in the materiality assessment, and SEC rules require disclosure in the 10-Q for material incidents that occurred during the quarter.

The rule: Under the SEC's cybersecurity disclosure rules (effective December 2023), registrants must disclose material cybersecurity incidents on Form 8-K within four business days of determining materiality, and include a summary in the relevant 10-K or 10-Q. The SEC CorpFin Division guidance on cybersecurity disclosure provides the current interpretive framework.

Checklist item to add: Include a standing agenda item for SEC reporting leadership to confirm with IT security and legal whether any cybersecurity incident occurred, and whether a materiality assessment was completed.

9. Going Concern Assessment Under ASC 205-40

What it is: A documented management assessment of whether there is substantial doubt about the company's ability to continue as a going concern for the 12-month period following the financial statement date.

Why teams miss it: Going concern is treated as an annual assessment. Under ASC 205-40, it is required for every annual and interim reporting period, which means it belongs in the quarter-end checklist, not only at year-end.

The standard: ASC 205-40 requires management to evaluate going concern conditions at every reporting date. The evaluation must be documented. If conditions raise substantial doubt, disclosure is required even if that doubt is ultimately alleviated by management's plans.

Checklist item to add: Confirm that a going concern assessment was completed for the period, documented by management, and reviewed by the audit committee. Confirm disclosure status matches the assessment outcome.

10. XBRL Tagging Review Before EDGAR Submission

What it is: A pre-submission review of the iXBRL-tagged financial statements to confirm tag accuracy, completeness, and consistency with prior period tagging.

Why teams miss it: XBRL tagging is treated as a mechanical step handled by the filing team at the end of the process, after all other review is complete. In practice, errors in XBRL tagging generate automated flags from the SEC's EDGAR system, can cause filing processing errors, and in some cases trigger comment letters about data quality.

The requirement: The SEC requires inline XBRL (iXBRL) tagging for all financial statements in periodic reports filed by domestic registrants. The EDGAR Full-Text Search shows the volume of XBRL-related correspondence between the SEC and registrants, it is not a negligible issue.

Checklist item to add: Run a structured XBRL review at least 48 hours before planned submission. Compare tags to prior period submission for any unexplained inconsistencies. Use the SEC's EDGAR Inline XBRL Viewer to visually confirm the rendered output matches the financial statements.

How to Map Your Checklist Items to ASC Standards

The ten items above each connect to one or more ASC standards maintained by the FASB. The challenge for most reporting teams is that this mapping lives in no single place---it requires cross-referencing the codification, your company's accounting policies, and your current period transaction activity. A Deloitte Center for Board Effectiveness survey found that 58% of audit committee members said they lacked visibility into how close checklist items mapped to specific ASC standards (Deloitte, 2024).

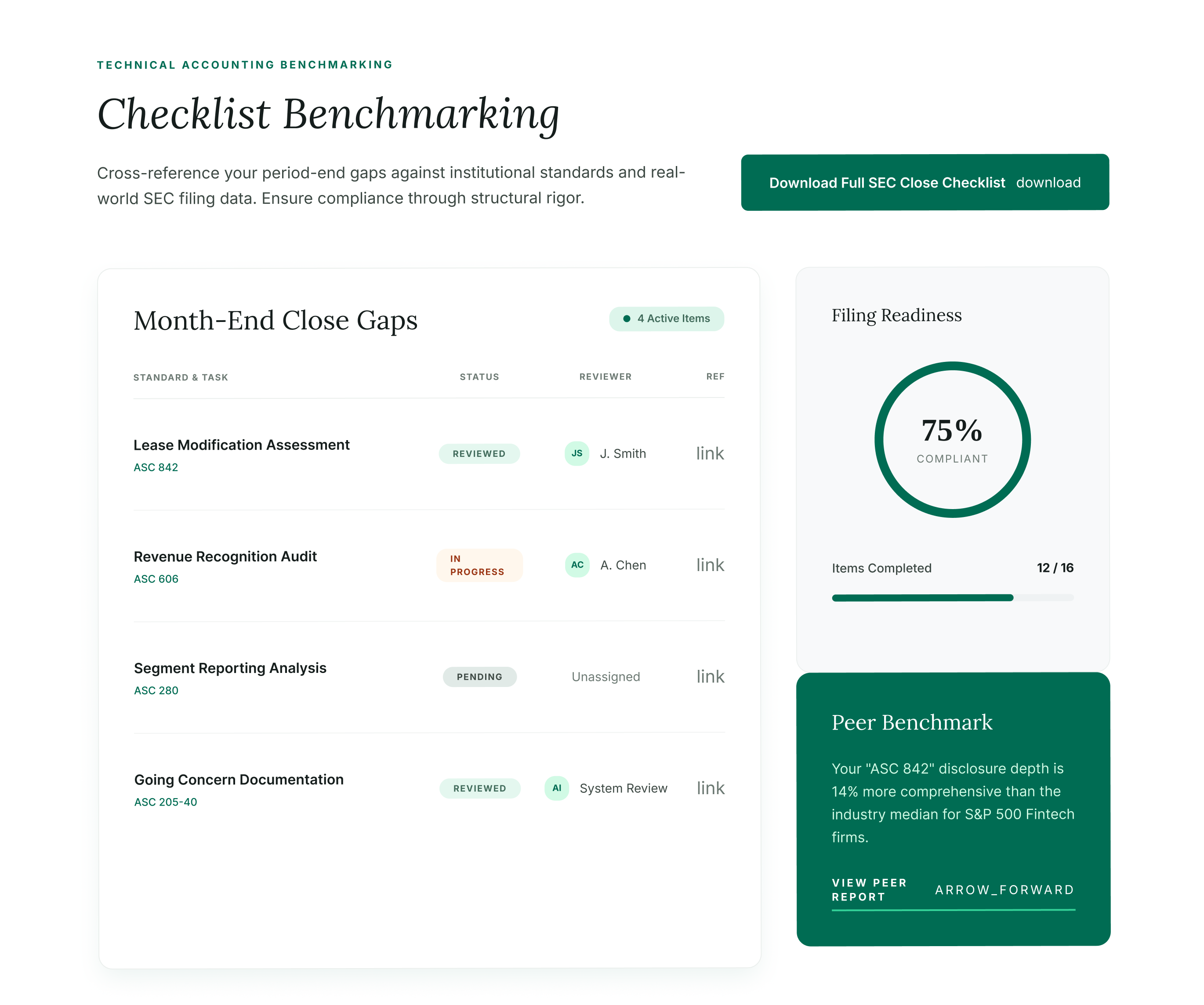

Finrep's Checklist Benchmarking feature addresses this directly. It maps each checklist item to the applicable ASC guidance, pulls relevant peer disclosure examples from EDGAR, and flags items where your current draft deviates from what comparable registrants are disclosing. Instead of manually cross-referencing ASC 280 or searching EDGAR for segment reporting peers, your team gets a structured view of where your disclosures stand relative to the standard and relative to the market.

The ASC guidance module within Finrep provides plain-language summaries of the applicable standard alongside the codification reference, so your team can review disclosure requirements without switching between the ASC, EDGAR, and your draft simultaneously.

CFO teams using Finrep's checklist benchmarking reduce month-end prep time from 10 days to 3–4 days, with 60–70% fewer review loops with auditors, according to Finrep client data, 2025.

What a Complete SEC Reporting Close Checklist Looks Like

Here is a structured, SEC-focused month-end financial close checklist that incorporates the ten items above alongside the standard close steps. This is the framework your team should be working from.

Week 1 of Close: Financial Close

- Subledger-to-GL reconciliation (AR, AP, Fixed Assets, Inventory)

- Intercompany elimination and reconciliation

- Journal entry completeness review and approval

- Bank and investment account reconciliations

- Accruals review and sign-off

Week 2 of Close: Disclosure Preparation

- ASC standard applicability assessment for period transactions

- MD&A draft initiated with prior period comparison

- Non-GAAP measure reconciliation drafted and reviewed

- Segment reporting review (ASC 280 applicability confirmed)

- Related party transaction disclosure review (ASC 850)

- Going concern assessment documented (ASC 205-40)

- Cybersecurity incident assessment confirmed with IT and legal

Week 3: Review and SEC Alignment

- MD&A language consistency review against prior period filing

- SEC comment letter history review, flagged areas elevated for heightened review

- EPS dilution calculation reviewed and documented (ASC 260)

- Peer benchmarking of key disclosures completed

- Audit committee pre-read package prepared

Week 4: Filing Preparation

- XBRL tagging review completed 48 hours before submission

- Final disclosure review against ASC checklist

- Sign-off chain confirmed (CFO, Controller, Disclosure Committee)

- EDGAR submission dry run completed

- Search Console or submission portal notification confirmed

Frequently Asked Questions

What is a month-end financial close checklist for SEC reporting?

A month-end financial close checklist for SEC reporting is a structured list of tasks covering both the accounting close, reconciliations, journal entries, subledger ties, and the disclosure integrity steps required for SEC filings. For public companies, the checklist must also include ASC standard applicability reviews, MD&A consistency checks, peer benchmarking, comment letter history review, and XBRL verification. A close checklist that stops at the accounting layer is insufficient for SEC registrants.

How long should the month-end close take for an SEC reporting team?

For most mid-cap SEC registrants, the full close and disclosure preparation cycle runs 15–25 business days for a 10-Q quarter and 30–45 business days for the 10-K annual period. Teams using AI-powered disclosure tools like Finrep report reducing their SEC reporting preparation time from 10 days to 3–4 days on the research and benchmarking portion, according to Finrep client data, 2025. The largest time savings come from eliminating manual EDGAR research and automating peer benchmarking.

What ASC standards are most commonly triggered during a standard month-end close?

The ASC standards most frequently triggered during interim close cycles are ASC 842 (Leases, lease modifications and new leases), ASC 606 (Revenue, new contract structures or variable consideration), ASC 350 (Goodwill and Intangibles, impairment triggers), ASC 280 (Segment Reporting, management reporting changes), and ASC 260 (EPS, new equity or convertible securities). Teams should assess all five for applicability at each period-end, not only at year-end.

Why do SEC comment letters often cite MD&A even when the numbers are correct?

The SEC's MD&A review focuses on narrative quality, not just numerical accuracy. Comment letters frequently cite MD&A sections that describe results without explaining the reasons behind them, that change language from prior periods without explanation, or that omit discussion of known trends or uncertainties. Correct numbers with insufficient analysis are a common SEC comment letter trigger. The SEC's interpretive guidance on MD&A states that the purpose of the section is analysis, not summary.

How does Finrep help with month-end close checklist management?

Finrep's Checklist Benchmarking feature maps each checklist item to the applicable ASC standard and pulls relevant peer disclosure examples from EDGAR, so your team can see how comparable registrants handle the same disclosure area. The ASC guidance module provides plain-language summaries of each applicable standard alongside codification references. Teams use Finrep to benchmark MD&A language, check non-GAAP disclosure consistency, and surface comment letter patterns from peers, all within a single platform built for the Office of the CFO. Finrep is SOC2 Type II and ISO 27001 certified, with zero data residency.

What is the most common close checklist item that generates SEC comment letters?

Based on Deloitte's 2025 Roadmap to SEC Comment Letter Considerations, the most commonly commented areas are MD&A (especially segment-level discussion), non-GAAP financial measures, revenue recognition disclosure under ASC 606, and EPS. Segment reporting under ASC 280 has been a particular focus in recent SEC review cycles, with comment letters asking registrants to explain why their reportable segment structure reflects CODM decision-making. Adding explicit ASC 280 and MD&A consistency checks to your close checklist directly reduces comment letter exposure in these areas.

Key Takeaways

- A standard accounting close checklist is not sufficient for SEC registrants. The public reporting layer requires ten additional steps that most checklists omit entirely.

- The most common gaps are MD&A consistency review, ASC standard applicability assessment, comment letter history check, non-GAAP compliance verification, and XBRL review.

- Each checklist item maps to a specific ASC standard or SEC regulatory requirement. Documenting that mapping is itself a disclosure controls best practice.

- Peer benchmarking your key disclosures against EDGAR data is not optional for high-scrutiny areas, it is how you know whether your disclosure meets current market standards before the SEC tells you it doesn't.

- Finrep's Checklist Benchmarking feature and ASC guidance module automate the research layer of this process, reducing close cycle time and audit review loops.

Ready to see how your close checklist maps against ASC standards, and against what your peers are filing?

Request access to Finrep's Checklist Benchmarking →

Finrep is an AI-powered SEC reporting and financial disclosure intelligence platform for the Office of the CFO. It lets your team research, benchmark, and draft SEC filings using EDGAR data with cited, audit-ready outputs. SOC2 Type II and ISO 27001 certified. Backed by Accel. Trusted by CFO teams at FOX, Roku, HP, RingCentral, and Infosys.

For further reading on related disclosure topics, see how Finrep compares to Intelligize for EDGAR benchmarking and the Section 16 deadline guide for Foreign Private Issuers