Did you know that over 1,000 foreign companies from more than 60 countries are currently listed on U.S. exchanges? From household names like Alibaba and Toyota to emerging tech unicorns, these companies collectively represent trillions of dollars in market capitalization. Yet behind every successful foreign listing lies a crucial document that many investors never see but absolutely depend on: Form 20-F.

Consider this: every year, the SEC processes thousands of Form 20-F filings, each one a 200-page-plus document that serves as a financial autobiography of a foreign company. These filings have revealed everything from accounting scandals that wiped out billions in market value to hidden gems that became the next generation's growth stories. The difference between companies that thrive in U.S. markets and those that struggle often comes down to how well they master this single, complex regulatory requirement.

In today's interconnected global economy, foreign companies increasingly seek to access U.S. capital markets to fuel their growth and expansion. However, this opportunity comes with significant regulatory responsibilities, chief among them the requirement to file Form 20-F with the Securities and Exchange Commission. This comprehensive annual report serves as the cornerstone of transparency for foreign private issuers operating in the United States, providing investors with crucial insights into their financial health, operational performance, and strategic direction.

The Birth of Form 20-F: A Regulatory Revolution

Form 20-F originated during the 1930s financial reforms and evolved into its current form in the 1960s as international investing expanded. The SEC designed it to protect American investors in foreign companies by creating a parallel disclosure framework that accommodates differences in international accounting standards, legal systems, and corporate governance practices while maintaining robust investor protections.

Form 20-F didn't emerge in a vacuum—it was born from necessity during the 1930s financial reforms enacted through the Securities Exchange Act of 1934, though it didn't take its current shape until the 1960s when international investing began to surge. The form's creation reflected a regulatory challenge: how do you ensure American investors get the protection they deserve when investing in companies governed by foreign laws, different accounting standards, and varying disclosure traditions?

The SEC's solution was notable for its flexibility. Rather than forcing foreign companies into the exact same mold as domestic issuers, Form 20-F created a parallel framework of disclosure that accommodated international differences while maintaining investor protection. According to the World Federation of Exchanges, foreign companies contribute roughly 20% of total market capitalization on U.S. exchanges (WFE, 2024). Former SEC Chair Mary Jo White emphasized that "cross-border listings strengthen U.S. capital markets by bringing global companies to American investors under robust disclosure standards."

Form 20-F represents far more than a mere compliance obligation. It serves as a vital communication bridge between foreign companies and American investors, ensuring that all market participants have access to the same essential information needed to make informed investment decisions. For foreign private issuers, mastering the 20-F filing process is not just about avoiding regulatory penalties—it's about establishing credibility, building investor confidence, and demonstrating a commitment to the transparency standards that define U.S. capital markets.

Understanding Form 20-F: The Foundation of Foreign Issuer Compliance

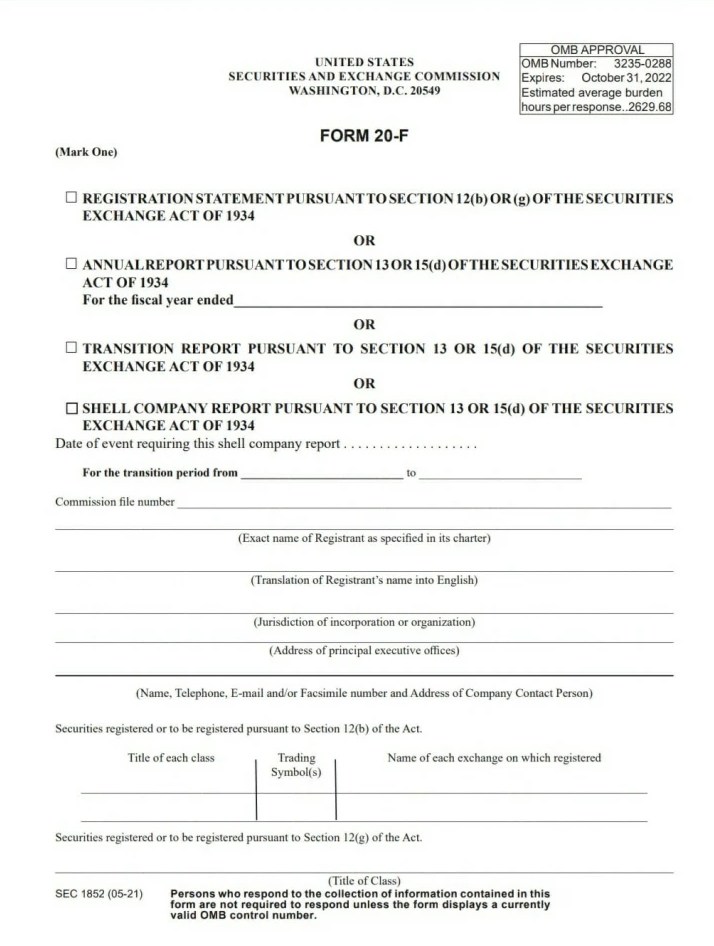

Form 20-F is the annual report that foreign private issuers must file with the SEC, serving as the international equivalent of the domestic Form 10-K. It applies to companies with securities registered under Section 12 of the Securities Exchange Act of 1934, typically those listed on the NYSE or NASDAQ. A company qualifies as a foreign private issuer through ownership and management tests defined by the SEC.

A notable distinction that even seasoned professionals sometimes overlook: Form 20-F is more comprehensive than its domestic counterpart, Form 10-K, in several key areas. Foreign companies must provide additional disclosures about their home country's regulatory environment, explain differences in corporate governance practices, and often present financial information in multiple formats to accommodate different accounting standards.

Form 20-F functions as the foreign equivalent of the Form 10-K that domestic U.S. companies must file annually, but with crucial differences that reflect the international nature of the filers. This comprehensive document provides a detailed snapshot of a company's business operations, financial condition, and results of operations over the preceding fiscal year. The SEC designed this form specifically to accommodate the unique circumstances of foreign companies while maintaining the transparency standards that protect American investors.

The requirement to file Form 20-F applies to foreign private issuers whose securities are registered under Section 12 of the Securities Exchange Act of 1934. This typically includes companies with securities listed on major U.S. exchanges such as the New York Stock Exchange or NASDAQ, as well as those that have conducted registered public offerings in the United States.

The SEC defines a foreign private issuer through what's known as the "50% test" and the "management test"—a company qualifies as foreign if either less than 50% of its outstanding voting securities are held by U.S. residents, or if the majority of its executive officers and directors are non-U.S. residents and the majority of its assets are located outside the United States. This seemingly simple definition has spawned countless legal analyses and strategic corporate restructurings, as companies sometimes reorganize their ownership or management structures to maintain their preferred regulatory status.

Critical Deadlines and Timing Considerations: The Four-Month Marathon

Foreign private issuers must file Form 20-F within four months after their fiscal year end. First-time filers have 90 days from their registration statement's effective date. Missing the deadline triggers a six-month compliance window during which the company loses access to Form S-3 for subsequent offerings. Coordination across time zones, languages, and legal systems makes meeting these deadlines significantly more complex than domestic filings.

One of the most interesting aspects of Form 20-F timing involves what practitioners call the "international coordination challenge." Unlike domestic companies that typically have their accounting teams, auditors, and legal counsel all in the same time zones, foreign issuers often must coordinate across continents, languages, and legal systems to meet their filing deadlines.

The SEC requires foreign private issuers to file their annual reports within four months after the end of their fiscal year, per Rule 13a-1 under the Securities Exchange Act. This deadline was extended from the previous three-month requirement in recognition of coordination challenges. This extension came after years of lobbying from foreign companies and their advisors, who argued that the shorter timeframe put them at a competitive disadvantage compared to domestic issuers.

First-time filers face different timing considerations, with companies registering securities for the first time having 90 days from their registration statement's effective date to submit their initial Form 20-F. This shorter timeframe creates what lawyers call a "baptism by fire" scenario, where companies must simultaneously learn U.S. disclosure requirements while managing their first public offering process.

The consequences of missing these deadlines can be severe. If a company fails to file this form, it is given a 6-month window to come into compliance, but during this grace period, the company cannot use Form S-3 for subsequent offerings, effectively cutting off access to the capital markets that initially motivated their U.S. listing.

Case Study: When Timing Goes Wrong - The Luckin Coffee Lesson

Luckin Coffee's 2019 Form 20-F illustrates how filing compliance extends beyond meeting deadlines to the quality and honesty of disclosures. The company's risk factors and internal control sections, while technically compliant, contained language that securities attorneys later identified as warning signs of the fabricated transactions that triggered the company's collapse and delisting from U.S. exchanges.

The dramatic rise and fall of Luckin Coffee provides a cautionary tale about the importance of robust Form 20-F processes. While Luckin's ultimate downfall stemmed from accounting fraud rather than filing delays, the company's 2019 Form 20-F, filed just months before the scandal broke, contained warning signs that careful readers could have detected.

Luckin's risk factors section mentioned "intense competition" and "challenges in maintaining quality control," but failed to adequately disclose the pressure-cooker environment that ultimately led management to fabricate transactions. The company's internal control disclosures, while technically compliant, used language that securities attorneys now recognize as potentially problematic. The lesson: Form 20-F isn't just about meeting deadlines—it's about creating a comprehensive, honest portrait of your business that can withstand intense scrutiny.

Essential Components and Content Requirements: The Anatomy of Transparency

Form 20-F comprises three main parts: Part I covers company identity, directors, key financial data including five-year summaries, risk factors, and use of proceeds; Part II addresses operational and financial disclosures; and Part III covers financial statements. The SEC reviews approximately 20% of all 20-F filings annually, with particular attention to sections reflecting current enforcement priorities.

The structure of Form 20-F reflects decades of regulatory evolution and comprises three main parts, each serving distinct purposes in the overall disclosure framework. What many companies don't realize is that the SEC reviews approximately 20% of all 20-F filings each year, with certain sections receiving particular attention based on current market conditions and enforcement priorities.

Part I contains the core information required in the annual report, beginning with the identity of directors, senior management, and advisers. This seemingly mundane section has occasionally sparked major controversies when companies failed to disclose that key executives held dual citizenship or had undisclosed conflicts of interest. The SEC's focus on this section intensified after several high-profile cases where foreign executives' backgrounds weren't adequately vetted or disclosed.

The key information section represents one of the most critical components of Form 20-F, encompassing selected financial data spanning five years, exchange rate information, comprehensive risk factors, and details about the use of proceeds from any securities offerings. The five-year financial summary requirement often catches companies off guard during their first filing, as they must present data in a format that may differ significantly from their home country requirements.

Exchange rate disclosures have become increasingly complex as currency volatility has increased. Companies must not only present exchange rate information but also explain their currency risk management strategies and quantify the impact of currency fluctuations on their results. Some companies have discovered that their choice of presentation currency can significantly affect how investors perceive their performance trends.

The Art and Science of Risk Factor Disclosure

Risk factor disclosure in Form 20-F requires company-specific, material risks rather than generic boilerplate language. The SEC enforcement division increasingly scrutinizes "copy-and-paste" risk factors, demanding specificity in areas such as cybersecurity incidents and remediation costs, geopolitical risks including sanctions and trade tensions, and regulatory changes in the issuer's home country. Foreign issuers face unique challenges balancing honest disclosure with avoiding unnecessary investor alarm.

Risk factors represent perhaps the most challenging aspect of Form 20-F preparation. The SEC's Division of Corporation Finance has increasingly focused on what they call "copy-and-paste" risk factors—generic disclosures that could apply to any company in an industry. SEC Chief Accountant Paul Munter has stated that "boilerplate disclosures do not serve investors and may indicate a lack of rigor in the company's risk assessment process." The agency expects risks that are specific, material, and genuinely relevant to the particular company's circumstances.

Consider the evolution of cybersecurity risk disclosures. Early foreign issuers often included boilerplate language about cyber threats, but recent SEC guidance demands specific information about actual incidents, remediation costs, and prevention strategies. Companies that failed to adequately disclose cybersecurity risks have faced SEC comments and, in some cases, enforcement actions when incidents occurred that were not properly flagged in their risk factors.

Geopolitical risks have also evolved dramatically. What once might have been a generic mention of "political instability" now requires detailed analysis of specific regulatory changes, trade tensions, and sanctions risks. Foreign companies operating in politically sensitive regions must walk a careful line between honest disclosure and not unnecessarily alarming investors about risks that may be manageable or unlikely to materialize.

Case Study: The Alibaba IPO - A Master Class in Risk Disclosure

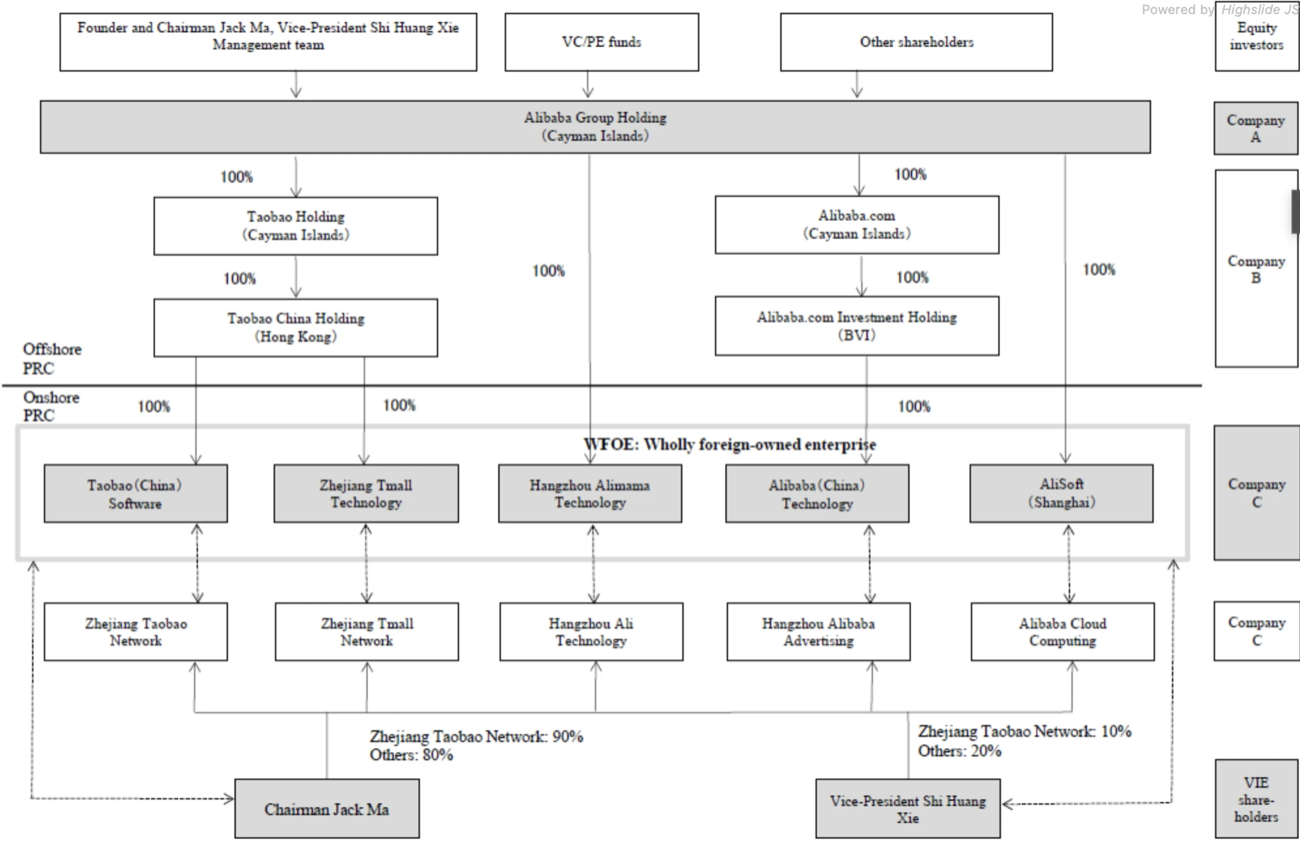

Alibaba's Form 20-F for its 2014 IPO devoted over 20 pages to explaining its Variable Interest Entity (VIE) structure, the contractual arrangements allowing foreign investors to participate despite Chinese legal restrictions on foreign ownership, and detailed scenarios where investor rights could be affected. This comprehensive approach to risk disclosure became a template for other Chinese companies navigating similar cross-border listing challenges.

When Alibaba filed its initial Form 20-F in connection with its record-breaking 2014 IPO, the company faced a unique challenge: how to explain the complex Variable Interest Entity (VIE) structure that allowed foreign investors to participate in Chinese internet companies despite Chinese law restrictions.

- The solid lines show the equity relationship.

- The dotted lines, which indicate the contractual relationship, include an exclusive technical services agreement as well as a loan agreement, an exclusive call option agreement, a proxy agreement, and an equity pledge agreement, etc., between the WFOEs and Chairman Jack Ma and Vice-President Shi Huang Xie.

- Alibaba Group Holding has many other subsidiaries in China and overseas, but they are omitted here for the sake of simplification.

Source: Compiled by the author based on the listing prospectus of Alibaba (August 12, 2014).

Alibaba's risk factors section devoted over 20 pages to explaining the VIE structure, regulatory uncertainties, and potential scenarios where foreign investors could lose their rights. This comprehensive disclosure, while potentially scary to some investors, actually enhanced Alibaba's credibility by demonstrating transparency about complex legal arrangements.

The disclosure strategy paid off. Despite the risks outlined in the filing, investors appreciated the thoroughness and honesty of the disclosures, contributing to the IPO's success. Alibaba's approach became a template for other Chinese companies navigating similar disclosure challenges.

Financial Statement Requirements: The International Accounting Maze

Foreign private issuers filing Form 20-F can choose from three accounting frameworks: U.S. GAAP, IFRS as issued by the International Accounting Standards Board, or home country GAAP with a full reconciliation to U.S. GAAP. Companies using IFRS must use the IASB version rather than any local variant, and the home country GAAP option requires detailed explanations and quantified impacts of material differences from U.S. GAAP.

The financial statement requirements for Form 20-F create a notable compromise between standardization and flexibility. According to the IFRS Foundation, over 140 jurisdictions now require or permit IFRS Standards (IFRS Foundation, 2024). Foreign private issuers can choose from three accounting frameworks: U.S. GAAP, IFRS as issued by the IASB, or home country GAAP with reconciliation to U.S. GAAP, as specified in Item 17 and Item 18 of Form 20-F.

This choice isn't as simple as it might appear. Companies using IFRS must ensure they're using the standards as issued by the International Accounting Standards Board, not their local country's version of IFRS, which may include modifications or carve-outs. This distinction has trapped several companies that assumed their local IFRS implementation would satisfy SEC requirements.

The home country GAAP option, while seeming like the path of least resistance, often proves most complex due to reconciliation requirements. Companies must provide detailed explanations of material differences between their home country standards and U.S. GAAP, along with quantified impacts on key financial metrics. These reconciliations can span dozens of pages and require expertise in both accounting frameworks.

Trivia: The Multi-Billion Dollar Footnote

The most expensive footnote in SEC filing history appeared in a foreign issuer's Form 20-F when a European telecommunications company's GAAP reconciliation revealed an undisclosed pension obligation exceeding $3 billion. The disclosure immediately wiped out nearly 20% of the company's market value, demonstrating that technical reconciliation requirements can surface material information with significant valuation consequences.

Here's a remarkable piece of Form 20-F trivia: the single most expensive footnote in SEC filing history appeared in a foreign issuer's 20-F. A European telecommunications company's reconciliation from local GAAP to U.S. GAAP revealed a previously undisclosed pension obligation that exceeded $3 billion, immediately wiping out nearly 20% of the company's market value when the filing was published.

The lesson: those "technical" reconciliation requirements aren't just paperwork—they can reveal material information that significantly affects company valuations.

Navigating the Filing Process: A Strategic Approach

A successful Form 20-F filing requires three to six months of preparation, a coordinated international team spanning auditors, legal counsel, and internal staff across time zones, and a continuous-cycle approach where planning for next year's filing begins immediately after the current submission. Companies should maintain year-round documentation files capturing significant events, management changes, and strategic decisions as they occur.

Successfully filing Form 20-F requires orchestrating what amounts to an international symphony, with musicians (team members) scattered across time zones, playing from different sheet music (regulatory requirements), and performing for an audience (investors and regulators) that has zero tolerance for wrong notes.

The preparation phase should commence at least three to six months before the filing deadline, but experienced practitioners know that truly successful filers begin their next year's filing immediately after submitting the current year's document. This continuous cycle approach allows companies to capture issues and improvements while they're fresh, rather than trying to reconstruct events months later.

Assembling the right team represents a critical first step that goes beyond simply hiring qualified professionals. The team needs chemistry—auditors who understand the business, lawyers who can translate complex regulations into practical guidance, and internal staff who can coordinate across different functional areas. Some of the most successful Form 20-F filings result from teams that have worked together for multiple years and developed efficient collaboration processes.

The information gathering phase involves much more than collecting financial data. Companies must also gather corporate governance information, material contracts, risk assessments, and forward-looking business analysis. Smart companies maintain "20-F files" throughout the year, capturing significant events, management changes, and strategic decisions as they occur rather than trying to recreate this information months later.

Common Challenges: The Hidden Pitfalls

The most common Form 20-F challenges for foreign issuers include corporate governance disclosure explaining how practices differ from U.S. norms and why, related party transaction reporting in business cultures where such transactions are more prevalent, and the complexity of presenting financial information across multiple accounting frameworks and regulatory systems while maintaining accuracy and investor comprehension.

Foreign private issuers face several unique challenges that don't affect domestic companies, and understanding these pitfalls can mean the difference between a smooth filing process and a regulatory nightmare.

Corporate governance disclosure represents one of the most nuanced challenges. Companies must explain not just how their practices differ from U.S. norms, but why these differences exist and how they protect or affect shareholder interests. This isn't about declaring one system superior to another—it's about helping American investors understand how decisions get made and rights get protected in different corporate cultures.

Related party transactions create particular complexity for foreign companies, which often operate in business environments where such transactions are more common and accepted. The challenge isn't necessarily avoiding these transactions—it's explaining them in a way that American investors can understand and evaluate. Companies must provide context about industry norms, business rationales, and safeguards that protect minority shareholders.

Case Study: The Samsung Succession Saga

Samsung's Form 20-F evolution over the past decade demonstrates how foreign issuers can improve governance disclosures progressively. The company moved from minimal detail about the Lee family control structure to comprehensive explanations of governance safeguards, independent director roles, and succession planning. Samsung's handling of the Lee Jae-yong legal issues showed that transparency about adverse developments serves companies better than minimal disclosure.

Samsung's Form 20-F filings over the past decade provide a fascinating case study in how to handle complex corporate governance issues. The company faced the challenge of explaining the Lee family's control structure, succession planning, and various legal challenges while maintaining investor confidence.

Samsung's approach evolved over several years, with early filings providing minimal detail about family control structures and later filings offering comprehensive explanations of governance safeguards, independent director roles, and succession planning processes. The evolution of Samsung's disclosures shows how companies can improve their Form 20-F communications over time, building investor understanding and confidence even around sensitive topics.

The company's handling of the Lee Jae-yong legal issues demonstrates another important principle: when facing adverse developments, transparency and comprehensive explanation often serve companies better than minimal disclosure that leaves investors guessing about potential impacts.

Technology and XBRL: The Digital Revolution in Financial Reporting

XBRL (eXtensible Business Reporting Language) tagging transforms Form 20-F financial statements into searchable, machine-readable data that institutional investors use for automated comparative analysis. Foreign issuers must make substantive decisions about tagging complex transactions, unusual items, and industry-specific metrics, as these choices directly affect how the company appears in database searches and analytical tools used by investors and analysts.

The SEC's XBRL requirements represent one of the most significant changes in financial reporting since the creation of EDGAR, but many companies still approach XBRL as a technical compliance issue rather than recognizing its strategic implications.

XBRL tagging transforms traditional financial statements into searchable, analyzable data that sophisticated investors can use for detailed comparative analysis. Companies that excel at XBRL implementation often gain advantages in analyst coverage and investor relations, as their data becomes more accessible to automated analysis tools that institutional investors increasingly rely upon.

The implementation challenges go beyond software and technical requirements. Companies must make substantive decisions about how to tag complex transactions, unusual items, and industry-specific metrics. These decisions affect how the company's financial performance appears in database searches and comparative analyses that investors conduct.

Building a Sustainable Compliance Framework: The Long Game

Sustainable Form 20-F compliance requires investment in what practitioners call SEC reporting infrastructure: systems, processes, and expertise that make quality disclosure repeatable rather than an annual scramble. This includes mapping workstream interdependencies, managing document versions across time zones, verifying translation accuracy, and rotating section responsibility among team members to catch issues that a single reviewer might miss.

Excellence in Form 20-F filing extends far beyond meeting annual deadlines. The companies that consistently produce high-quality, timely filings typically invest in what professionals call "SEC reporting infrastructure"—systems, processes, and expertise that make excellent disclosure a repeatable capability rather than an annual scramble.

Project management excellence in the Form 20-F context requires understanding the interdependencies between different workstreams. Auditors can't complete their testing until accounting teams finish their analysis, legal counsel can't finalize disclosures until business teams provide operational updates, and translation services can't begin work until content is locked. Successful project managers map these dependencies and build buffers that accommodate the inevitable delays and iterations.

Quality control processes must account for the international nature of the exercise. Document versions must be managed across time zones, translation accuracy must be verified, and cultural differences in communication styles must be navigated. Some companies have found that rotating primary responsibility for different sections among team members helps catch issues that the same person might miss year after year.

The Strategic Value of Excellence: Beyond Compliance

Companies that treat Form 20-F as a strategic exercise rather than a compliance burden often discover operational benefits beyond regulatory adherence. Comprehensive risk factor analysis identifies operational vulnerabilities proactively, clear business descriptions improve internal communication, and consistently excellent filings enhance relationships with credit rating agencies, improve debt market access, and strengthen credibility with strategic partners and acquisition targets.

While Form 20-F represents a regulatory requirement, companies that approach it strategically often discover that the discipline required for excellent SEC reporting improves their overall business operations. The process of preparing a comprehensive risk factor analysis often identifies operational vulnerabilities that management can address proactively. The requirement for clear, accessible business descriptions forces companies to articulate their strategies in ways that benefit internal communication as well as external disclosure.

Companies that consistently produce exceptional Form 20-F filings often report improved relationships with credit rating agencies, better access to debt markets, and enhanced credibility with strategic partners and acquisition targets. The investment in disclosure excellence pays dividends that extend well beyond the immediate regulatory compliance requirement.

Case Study: The Spotify Model - Innovation in Disclosure

Spotify uses its Form 20-F as a strategic communication tool rather than a compliance exercise. The company's risk factors section educates investors about the music streaming industry and competitive dynamics, while its management discussion and analysis reads as a strategic primer explaining not just what happened during the reporting period but why it matters for future performance, earning a reputation for transparent, investor-friendly disclosure.

Spotify's approach to Form 20-F filing demonstrates how companies can use regulatory requirements as opportunities for strategic communication. Rather than treating risk factors as legal boilerplate, Spotify uses this section to educate investors about the music streaming industry, explain the company's competitive advantages, and provide context for business model evolution.

Spotify's management discussion and analysis sections read more like strategic primers than traditional regulatory filings, helping investors understand not just what happened during the reporting period, but why it happened and what it means for future performance. This approach has contributed to Spotify's reputation for transparent, investor-friendly communication.

The Numbers Game: Form 20-F by the Statistics

Form 20-F filings average 200 to 250 pages, with some exceeding 400 pages. Over 1,000 foreign companies from more than 60 countries are listed on U.S. exchanges, with the largest contingents from China, Canada, and the United Kingdom. Their collective market capitalization exceeds $8 trillion. The SEC obtained $8.2 billion in financial remedies in fiscal year 2024, with significant enforcement actions involving foreign issuers who failed disclosure obligations.

Here are some fascinating statistics that illustrate the scope and impact of Form 20-F filings:

The average Form 20-F filing contains approximately 200-250 pages, but some comprehensive filings exceed 400 pages. The longest Form 20-F on record contained over 600 pages and was filed by a diversified industrial conglomerate with operations in more than 50 countries.

Foreign private issuers represent companies from every continent except Antarctica, with the largest contingents coming from China, Canada, and the United Kingdom. The collective market capitalization of foreign companies listed on U.S. exchanges exceeds $8 trillion, making their Form 20-F filings some of the most economically significant documents filed with any regulatory agency worldwide.

The SEC obtained orders for $8.2 billion in financial remedies in fiscal year 2024 (SEC, 2024), with a significant portion of enforcement actions involving foreign issuers who failed to meet their disclosure obligations. These statistics underscore the real consequences of inadequate Form 20-F compliance. As SEC Chair Gary Gensler noted in a 2023 speech, "We will hold foreign issuers to the same standards of transparency that apply to domestic companies."

Conclusion: Mastering Form 20-F for Long-Term Success

Filing Form 20-F successfully requires combining technical expertise with strategic thinking, operational excellence with clear communication, and regulatory compliance with investor relations effectiveness. The companies that master this process don't just survive in U.S. capital markets—they thrive, building the operational capabilities and disclosure disciplines that define world-class public companies.

The key to sustainable success lies in viewing Form 20-F not as an annual burden but as an opportunity to strengthen financial reporting capabilities, enhance investor communication, and demonstrate commitment to the transparency standards that define excellence in public company management. Companies that embrace this perspective often find that their investment in SEC reporting excellence generates returns that extend far beyond regulatory compliance to encompass improved access to capital, enhanced investor confidence, and stronger operational performance.

In our interconnected global economy, the ability to communicate effectively with international investors through vehicles like Form 20-F has become a core competency for ambitious companies seeking to scale across borders. The companies that master this art form don't just comply with regulations—they use transparency as a competitive advantage, building trust that translates into lower capital costs, better strategic partnerships, and sustainable long-term growth.

The Form 20-F process requires international business communication, cross-cultural transparency, and the operational discipline demanded by major capital markets. For foreign companies that treat it as a strategic exercise, the benefits extend beyond meeting filing deadlines to include stronger investor relationships, improved internal processes, and more credible participation in U.S. capital markets.