The United States had approximately 8,090 companies listed on public stock exchanges in 1996. As of 2024 it has approximately 3,929. Over the same period, US nominal GDP nearly tripled, the population grew by roughly 30%, and entirely new industries emerged in cloud computing, biotech, fintech, and AI. The number of public companies fell by half anyway.

That number should bother you regardless of your political views on regulation. It means that the companies creating value in the American economy over the past three decades have been doing so in a venue most investors cannot access. Retail investors, pension funds, and ordinary savers cannot buy a stake in a company that will never list. They get the exit multiple, if they get anything at all.

On May 19, 2026, the SEC proposed two rulemakings that Chairman Paul Atkins described as "the foundation for my agenda to Make IPOs Great Again." The proposals are real and the direction is right. But they solve about a third of the problem. Here is what they do, what they miss, and what that means for a CFO considering going public in 2027.

Why Did the Number of US Public Companies Fall by Half Since 1996?

The decline from approximately 8,090 listed companies in 1996 to approximately 3,929 in 2024 is the foundational data point behind the current SEC reform agenda. According to research published by the Harvard Corporate Governance Forum (Doidge, Karolyi, and Stulz) and confirmed by SEC reporting issuer data for 2004 through 2024, this represents a 51% decline over a period when the economy expanded substantially.

The SEC's own May 19, 2026 press release acknowledges the connection directly: "Compounding regulatory requirements over recent decades, however, have corresponded with a decrease in the number of public companies."

Three explanations for the decline are most commonly cited in the regulatory and academic literature, and it is worth being precise about each because they point to different remedies.

The compliance cost explanation. The Foley and Lardner cost-of-being-public study found average compliance costs for companies under $1 billion in revenue rose to approximately $2.8 million after Sarbanes-Oxley (SOX), a 171% increase from pre-SOX levels. Korn Ferry put average initial compliance cost at $5.1 million with $3.7 million in ongoing annual cost. The GAO's 2025 study on SOX compliance costs (GAO-25-107500) found that nonexempt companies pay 19% more in audit fees than exempt smaller reporting and emerging growth companies.

For a company doing $50 million in annual revenue, $2.8 million to $5 million in annual compliance overhead represents 5 to 10 cents of every dollar going to the cost of being public. For a company doing $5 billion in revenue, the same fixed cost is a rounding error. The system is structurally regressive: it imposes proportionally heavier burdens on the smaller companies it is theoretically designed to benefit.

The pre-SOX decline explanation. The number of public companies began falling in 1997, five years before Sarbanes-Oxley was enacted. This means the compliance cost explanation, while real, is incomplete. The dot-com bust, merger and acquisition consolidation, and Nasdaq's own listing-standard tightening in 1996 each explain a portion of the early decline. The 'regulation killed IPOs' narrative is partially self-serving.

The private capital abundance explanation. The rise of mega-funds, sovereign wealth capital, growth equity, and continuation vehicles means many companies that would have previously gone public can now stay private indefinitely. The SEC's own data confirms that Regulation A, the simplified public offering pathway created specifically to encourage small-company IPOs, represents less than 1% of Regulation D private capital raised. Companies are not using the existing public pathways primarily because private capital is more accessible, not because the pathways are too difficult.

Each explanation is partially correct. The SEC's reform agenda addresses the first most directly. It acknowledges but does not resolve the second and third.

This matters because the reform is being sold as a comprehensive solution to a structural problem it only partially addresses. Reducing SOX compliance costs will help a company on the margin. It will not persuade a venture-backed company sitting on $400 million in private funding at a $2 billion valuation to go public rather than raise another private round. The compliance cost argument is the easiest one to make politically. It is not necessarily the most important one economically.

What Did the SEC Actually Propose on May 19, 2026?

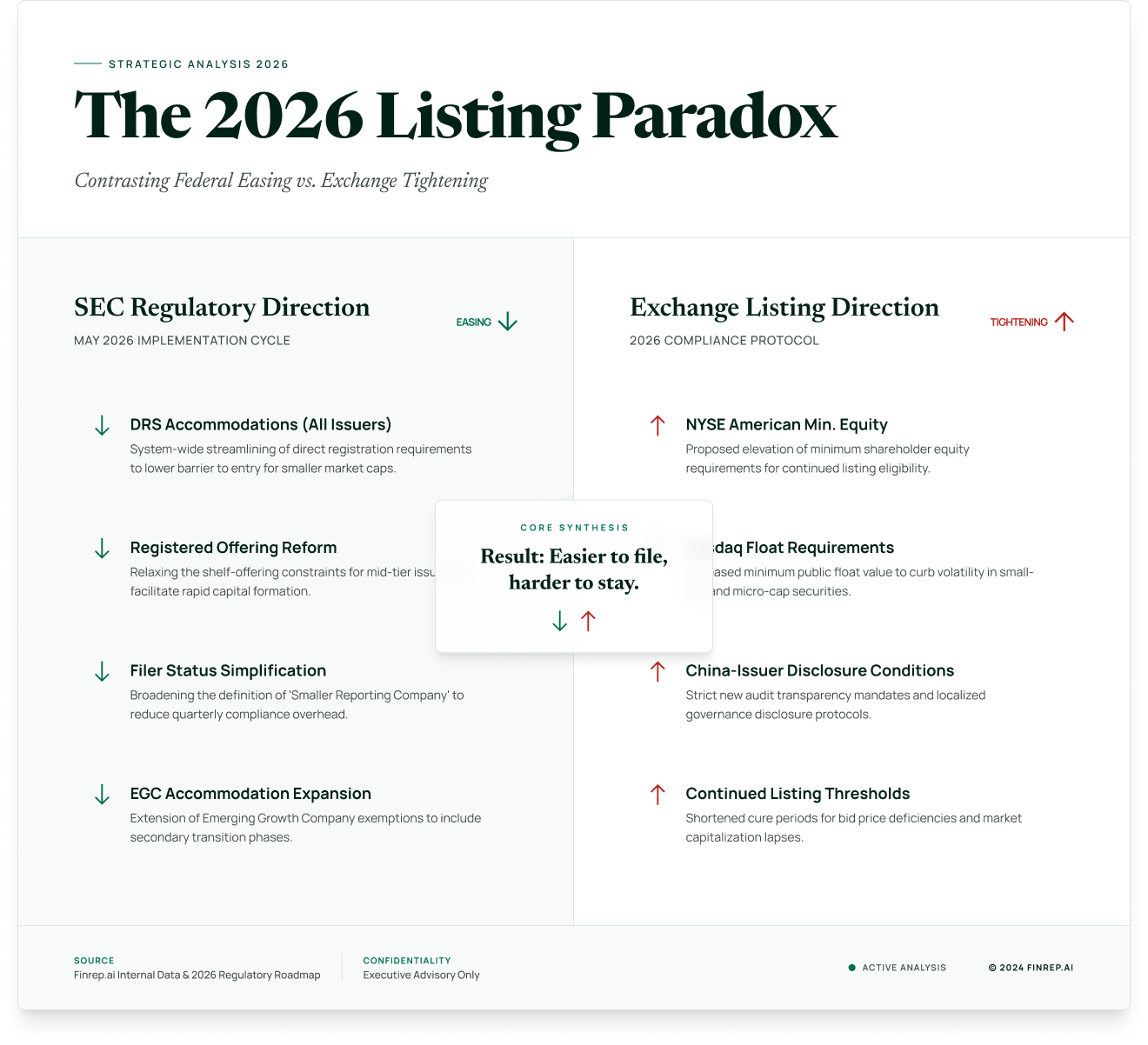

On May 19, 2026, the SEC proposed two rulemakings under Chairman Atkins's stated objective of making IPOs more accessible, particularly for small and mid-sized companies. The proposals are open for comment through July 20, 2026.

The first rulemaking addresses registered offering reform and the conditions under which companies can access Form S-3 and other shelf registration mechanisms. The proposals are designed to increase efficiency, flexibility, and cost savings for public companies while maintaining investor protections, according to the SEC's May 19 press release.

The second rulemaking addresses filer status simplification. recalibrating disclosure obligations based on company size and maturity. The SEC's stated objective is to extend to more companies the accommodations that have proven successful for Emerging Growth Companies under the JOBS Act of 2012.

These proposals build on a series of earlier actions under the Atkins agenda. In March 2025, the Division of Corporation Finance expanded the accommodations available for draft registration statement (DRS) submissions, allowing all issuers. not just Emerging Growth Companies. to submit registration statements for nonpublic SEC review before going public. The March 2025 expansion specifically extended nonpublic review to Exchange Act Section 12(b) and 12(g) registrations, permitted issuers to omit underwriter names from initial draft submissions, and expanded DRS eligibility for de-SPAC transactions.

The May 19 proposals are described by Atkins as "among the first important steps toward transforming the SEC's regulatory framework for public companies." They are proposals, not final rules. The comment period closes July 20, 2026. Final rules, if adopted, would follow a subsequent rulemaking process.

The honest assessment is that these proposals are meaningful but incremental. They reduce friction at the margins. They do not address the aftermarket infrastructure problem, the analyst coverage collapse, or the exchange listing standards that are tightening simultaneously. A company that could not economically justify going public in 2025 will not automatically be able to justify it in 2027 because Form S-3 eligibility conditions have changed.

What Is Chairman Atkins's Position on Capital Formation and Why Does It Matter?

Chairman Paul Atkins has been consistent and specific about his views across public statements from February through May 2026. Three direct quotes from his statements establish the framework.

On the role of public markets: "Public markets are the anchor of American capital formation because they combine liquidity, transparency, price discovery, and accountability in a way that private markets cannot fully replicate.", SEC Statement, May 19, 2026

On who should be able to access an IPO: "Raising capital through an IPO should not be a privilege reserved for those few 'unicorns.' Our regulatory framework should provide companies in all stages of their growth with the opportunity for an IPO, particularly one that represents a capital raising mechanism for the company, instead of a liquidity event for insiders.", SEC Small Business Forum, March 10, 2026

On accumulated regulation: "Decades of accretive rulemaking have made the path to becoming a public company narrower. and the experience of remaining one encumbered with rules that can introduce more friction than benefit. reams of paperwork that can do more to obscure than to illuminate.", SBCFAC Remarks, April 28, 2026

From his remarks on the INVEST Act, February 25, 2026, Atkins has identified three specific reform pillars: re-anchoring disclosures in materiality so investment decisions turn on economic signals rather than regulatory volume; de-politicising shareholder meetings to restore focus to significant corporate matters; and developing litigation alternatives that protect genuinely innovative companies from frivolous suits.

Understanding Atkins's position matters for a specific practical reason: these are not aspirational statements from a new chairman. The March 2025 DRS expansion was a concrete regulatory action. The May 19 proposals are two more. The comment period closes July 20, 2026. If you have views on how these proposals would affect your company's ability to access public markets, this is the window to express them.

What Is the 44% and 3% Data Telling the SEC About the Current IPO Market?

In 2024, small-company IPOs represented 44% of all IPOs by count but raised only 3% of the total IPO capital raised that year. According to Commissioner Mark Uyeda's remarks at the SEC's Small Business Capital Formation Advisory Committee on April 28, 2026, Uyeda characterised the current IPO market recovery as an "uneven recovery."

This data point is significant because it demonstrates that reducing the mechanical barriers to IPO filing (which prior reforms partially accomplished through the JOBS Act EGC accommodations) is not sufficient to produce a functioning small-company IPO market. A company can file an S-1 relatively efficiently. The problem is the aftermarket: without analyst coverage, institutional investor interest, and liquidity, the IPO raises little capital and delivers limited benefit to the issuing company.

The Office of the Advocate for Small Business Capital Formation's 2024 annual report confirmed that 44% of small and mid-cap stocks have zero analyst coverage. Without research, there is no aftermarket. Without an aftermarket, the IPO raises less capital. Without capital, the entire rationale for going public weakens.

The SEC's reform agenda is addressing this ecosystem problem. not just the filing mechanics. The proposals on filer status simplification and registered offering reform are designed to reduce the ongoing cost burden that makes small-company public market participation economically marginal relative to the private alternative. Whether they succeed depends on whether the exchange listing environment simultaneously supports small-company liquidity. which is where the picture complicates.

The 44% and 3% data is the most uncomfortable statistic in this entire debate because it cannot be explained by compliance costs alone. Small companies are filing IPOs. They are just not raising any capital. That is an aftermarket problem, not a filing problem. Fixing the filing requirements will not fix the aftermarket.

What Are Nasdaq and NYSE American Doing to Listing Standards at the Same Time?

This is the paradox the blog title names. At the same moment the SEC is reducing federal filing barriers, the exchanges are tightening their own listing standards. Understanding both sides of this dynamic is essential for a company evaluating whether to go public.

In January 2026, NYSE American filed a proposed rule change with the SEC that would increase minimum equity and float requirements for continued listing. In May 2026, Nasdaq filed a separate rule change relating to China-based issuers, requiring additional disclosures and conditions for companies with principal operations in China. The specific rule filings are available at the SEC: Nasdaq China Rule, May 2026 (SR-NASDAQ-2026) and NYSE American January 2026 proposal (SR-NYSEAMER-2026).

The exchange tightening is happening for separate reasons from the SEC reforms. Exchanges face reputational and regulatory pressure from failures of small listed companies, particularly those with thin floats, minimal analyst coverage, and high manipulation risk. The SEC's Investor.gov site explicitly flags micro-cap stocks as disproportionately associated with fraud and manipulation. Exchanges are responding to that risk by raising the structural requirements for continued listing. minimum float, minimum market value, minimum revenue or shareholder equity. that a company must maintain to stay listed.

The practical consequence of these two simultaneous movements is a bifurcation: the federal regulatory cost of filing is declining, but the structural requirements for sustaining a listed company are increasing. The SEC is making it easier to file. The exchanges are making it harder to stay. The question for a company considering a public offering in 2026 or 2027 is not whether it can satisfy the SEC's filing requirements. it almost certainly can. The question is whether it can sustain the listing requirements, analyst coverage, institutional float, and minimum liquidity standards that make being public economically viable in the years after the IPO.

The exchange tightening is not the villain in this story. It is the rational response to 30 years of micro-cap manipulation and thin-float fraud. The problem is that nobody is coordinating the federal easing and the exchange tightening into a coherent framework for what a viable small-company IPO actually looks like. The SEC and the exchanges are making independent decisions that push in opposite directions, and the company in the middle has to navigate both without a map.

What Are the Five Forces Driving This Reform Agenda Now?

The current reform effort is not happening in isolation. Five specific conditions converged in 2026 to make this the moment for this agenda.

Political alignment. Atkins is a Republican appointee with views aligned with the current administration's deregulatory direction. Free-market SEC leadership historically favors capital formation over disclosure expansion. The window of policy opportunity is open now and may not be in 2028 depending on the election cycle.

The retail investor exclusion problem. When companies stay private until they reach $50 billion or more in market capitalisation, retail investors cannot participate in the value creation years. By the time a company conducts an IPO, venture capital and private equity have already captured the majority of the appreciation. Atkins has explicitly framed this as an equity issue: workers and savers should not be locked out of the next generation of American enterprise.

The structural regressiveness of fixed compliance costs. The compliance cost data is not politically contested. A system that imposes $3 to $5 million in fixed annual cost on a $50 million revenue company and the same cost on a $5 billion revenue company is structurally regressive. The argument for relief is available from any political direction that accepts the cost data.

The research coverage collapse. With 44% of small and mid-cap stocks carrying zero analyst coverage, the aftermarket infrastructure that makes IPOs viable for small companies has substantially degraded. The SEC has connected the disclosure burden, the research economics, and the listing economics as a system that needs to be addressed together. not as separate problems.

Private capital constraints. Venture funding has been constrained since 2022. Companies that would previously have raised another private round are now reaching the limits of private capital access. Public markets are becoming an alternative again out of necessity, not just opportunity, which gives the reform agenda real market demand behind it rather than purely ideological backing.

What Are the Legitimate Criticisms of This Reform Agenda?

Publishing a post that presents only one side of a regulatory debate is not credible analysis. Four substantive criticisms of the current SEC reform agenda deserve honest engagement.

The decline started before SOX. Public company counts began falling in 1997, five years before Sarbanes-Oxley. The 'regulation killed IPOs' narrative is partially self-serving. The dot-com crash and M&A consolidation also explain a large portion of the early decline, and the regulation-focused explanation tends to be more prominent in industry advocacy than in academic research.

Global exchanges saw similar declines. Tuck School of Business research by Espen Eckbo found that approximately 80% of country-specific stock exchanges globally saw 50% drops in listed companies over similar periods, in different years. When M&A exits are included as a natural market evolution, the 'lost listings' story is considerably weaker than the headline 51% decline suggests.

Companies stay private because private capital is abundant. The SEC's own data. acknowledged by Atkins at the May 2025 SBCFAC meeting. shows Regulation A represents less than 1% of Regulation D capital raised. Companies are not using the simplified public pathway primarily because private capital is faster and easier to raise with less disclosure obligation, not because the federal filing process is too burdensome.

Loosening disclosure requirements risks enabling fraud. Micro-cap stocks are disproportionately associated with manipulation and fraud. Reducing required disclosures, even for legitimate reasons, has real investor protection implications. This is precisely why the exchange listing tightening is occurring simultaneously: it is the necessary counterbalance to federal disclosure reduction. A company cannot simultaneously benefit from reduced federal filing obligations and relaxed exchange standards without increasing investor protection risk.

The correct editorial posture is to acknowledge all four criticisms. The SEC is addressing a real problem with a partial solution that has real risks. The reform agenda is not obviously right or obviously wrong. It is a serious regulatory effort addressing a serious structural problem, with legitimate disagreement about causes, remedies, and consequences.

Frequently Asked Questions

What is the SEC's "Make IPOs Great Again" agenda and what does it propose?

Chairman Paul Atkins's capital formation agenda is a series of regulatory actions designed to make going public cheaper and more accessible, particularly for small and mid-sized companies. The most recent concrete proposals, released May 19, 2026, address registered offering reform and filer status simplification. Earlier actions include the March 2025 expansion of the Draft Registration Statement nonpublic review process to all issuers. The comment period on the May 19 proposals closes July 20, 2026.

Why did the number of US public companies fall from approximately 8,090 in 1996 to approximately 3,929 in 2024?

Multiple causes are documented. Post-Sarbanes-Oxley compliance costs rose by 171% for companies under $1 billion in revenue, making being public proportionally more expensive for smaller companies. The dot-com crash and M&A consolidation drove early declines beginning in 1997, before SOX. The growth of private capital markets reduced the need for many companies to access public markets for financing. Each explanation is partially correct, and the SEC's reforms address primarily the first.

What does it cost a small company to be public under current requirements?

The Foley and Lardner study found post-SOX compliance costs averaged approximately $2.8 million annually for companies under $1 billion in revenue, a 171% increase from pre-SOX levels. Korn Ferry estimated $5.1 million in initial compliance cost plus $3.7 million in ongoing annual cost. The GAO's 2025 study found nonexempt companies pay 19% more in audit fees than companies with smaller reporting company or emerging growth company exemptions. For a company with $50 million in annual revenue, this represents 5 to 10% of revenue in compliance overhead annually.

What is the 2026 paradox between SEC filing requirements and exchange listing standards?

In 2026, the SEC is reducing the federal regulatory burden for going public. through DRS accommodations, registered offering reform, and filer status simplification. Simultaneously, Nasdaq and NYSE American are tightening their exchange listing standards. increasing minimum float, equity, and disclosure requirements for continued listing. The result is a bifurcation: filing with the SEC is becoming easier, but sustaining an exchange listing is becoming structurally harder. The question for a company considering going public is not whether it can satisfy the SEC's filing requirements. it is whether it can satisfy the exchange's listing standards for years after the IPO.

What does the 44% and 3% data mean for small-company IPOs?

In 2024, small-company IPOs represented 44% of all IPOs by count but raised only 3% of total IPO capital. Commissioner Uyeda characterised this as an "uneven recovery." The data demonstrates that reducing the cost of filing an S-1 is not sufficient to produce a functioning small-company IPO market. The bottleneck is the aftermarket: without analyst coverage (44% of small and mid-cap stocks have zero coverage), institutional interest, and minimum liquidity, the IPO raises little capital and delivers marginal benefit. The SEC's current proposals attempt to reduce the ongoing cost burden that makes small-company public market participation economically marginal.

When does the comment period close and what should companies do before it does?

The comment period on the May 19, 2026 proposals closes July 20, 2026. Companies with views on how the proposed registered offering reform or filer status simplification would affect their ability to access or remain in public markets can submit comments through the SEC's online comment system. This is specifically relevant for companies under $1 billion in revenue for whom the compliance cost differential between exempt and non-exempt status is material.

Key Takeaways

The SEC's May 19 proposals are a serious attempt to address a real structural problem. The problem is real: 51% fewer public companies, a 44%/3% IPO market split, and compliance costs that consume 5 to 10% of revenue for small companies while barely registering for large ones. The direction is right.

But the proposals solve the easiest part of the problem. Reducing the federal cost of filing does not fix the aftermarket. It does not restore analyst coverage to the 44% of small stocks that have none. It does not resolve the simultaneous tightening of exchange listing standards. A company that goes public into a market with no institutional float, no research coverage, and minimum listing requirements breathing down its neck will discover that the filing was the easy part.

The practical verdict for a CFO considering a public offering in 2027: the SEC reforms matter, but they are table stakes, not the thesis. The decision to go public should rest on whether your company can sustain exchange listing standards, generate institutional investor interest, and support analyst coverage in the years after the IPO. If the answer to those questions is yes, the reduced federal compliance burden makes the economics better. If the answer is no, lower filing costs do not change the outcome.

- The US lost 51% of its listed public companies between 1996 and 2024. The SEC's reforms address the compliance cost dimension of this decline. They do not address the private capital abundance or market structure dimensions.

- Compliance costs are documented and regressive: $2.8 million to $5 million annually for companies under $1 billion in revenue, representing 5 to 10% of revenue for a $50 million company. The GAO confirmed in 2025 that nonexempt companies pay 19% more in audit fees than exempt counterparts.

- The 44%/3% data reveals the real problem: it is not that small companies cannot file, it is that they cannot raise meaningful capital when they do. That is an aftermarket and coverage problem, not a filing problem.

- The SEC and exchanges are moving in opposite directions. Federal filing burden is decreasing. Exchange listing standards are tightening. The gap between them is where companies will get hurt if they read only one side of the picture.

- The comment period closes July 20, 2026. If the compliance cost differential is material to your company, submit a comment. This is the best opportunity to influence final rules that will govern the cost of being public for the next decade.