Navigating the Tightrope Between Transparency and Compliance

Imagine you're the CFO of a publicly traded company. You've just finished a productive meeting with a small group of institutional investors, sharing insights about your company's performance. The conversation was engaging, the questions were sharp, and you felt you provided valuable context. Then it hits you—did you just reveal material information that wasn't public? Welcome to the paradox that keeps corporate executives and compliance officers awake at night: the Regulation FD and Form 8-K catch-22.

The Paradox: You must disclose material information to everyone at once (Regulation FD), but you can only know something is "material" after you've potentially already disclosed it selectively. It's like being told you can't step over a line you can't see until after you've crossed it.

Understanding the Regulatory Landscape

Regulation Fair Disclosure (Reg FD), adopted by the SEC in 2000, requires companies to simultaneously disclose material nonpublic information to all investors when sharing it with any select group. Form 8-K is the current report companies must file to announce major events such as mergers, leadership changes, or financial results. Together, these two rules create the framework governing public company disclosure obligations.

Before we dive into the catch-22, let's set the stage. Regulation Fair Disclosure (Reg FD), adopted by the SEC in 2000, was designed to level the playing field in securities markets. Then-SEC Chair Arthur Levitt, who championed Reg FD, described it as essential to ensuring that "all investors have access to an issuer's material disclosures at the same time." The rule is deceptively simple: when a company discloses material nonpublic information to certain people, it must simultaneously disclose that information to the general public. The full text of Regulation FD remains a foundational reference for corporate disclosure obligations.

Form 8-K, on the other hand, is the "current report" companies must file to announce major events that shareholders should know about. These events range from mergers and acquisitions to changes in executive leadership, financial results, and more.

The Catch-22 Unfolds

The core paradox of Regulation FD is that materiality is inherently subjective and context-dependent. A company must disclose material information to everyone simultaneously, yet whether information qualifies as material often cannot be determined until after it has already been shared with a select audience and the market has reacted. This creates an unavoidable compliance gap between real-time conversations and after-the-fact regulatory evaluation.

The materiality of information often exists in shades of gray rather than black and white. Information becomes "material" if there's a substantial likelihood that a reasonable investor would consider it important in making an investment decision, as established in the Supreme Court's landmark TSC Industries v. Northway (1976) decision. But this determination is inherently subjective and context-dependent. A Harvard Law School Forum on Corporate Governance analysis noted that the SEC brought 17 enforcement actions related to Reg FD violations between 2000 and 2023, demonstrating the agency's ongoing focus on selective disclosure (Harvard Law School, 2023).

Real-World Scenario: The Earnings Preview Dilemma

A tech company's IR director receives calls from three analysts on the same day, all asking similar questions about an upcoming product launch. The director provides what she believes is publicly available information, adding some "harmless" color commentary about customer enthusiasm. Two days later, one analyst upgrades the stock based partly on the "insider insights" about customer reception. The company's stock jumps 8%.

The Question: Was the commentary material? Should a Form 8-K have been filed? The company won't know until the SEC potentially investigates.

The Timeline Trap

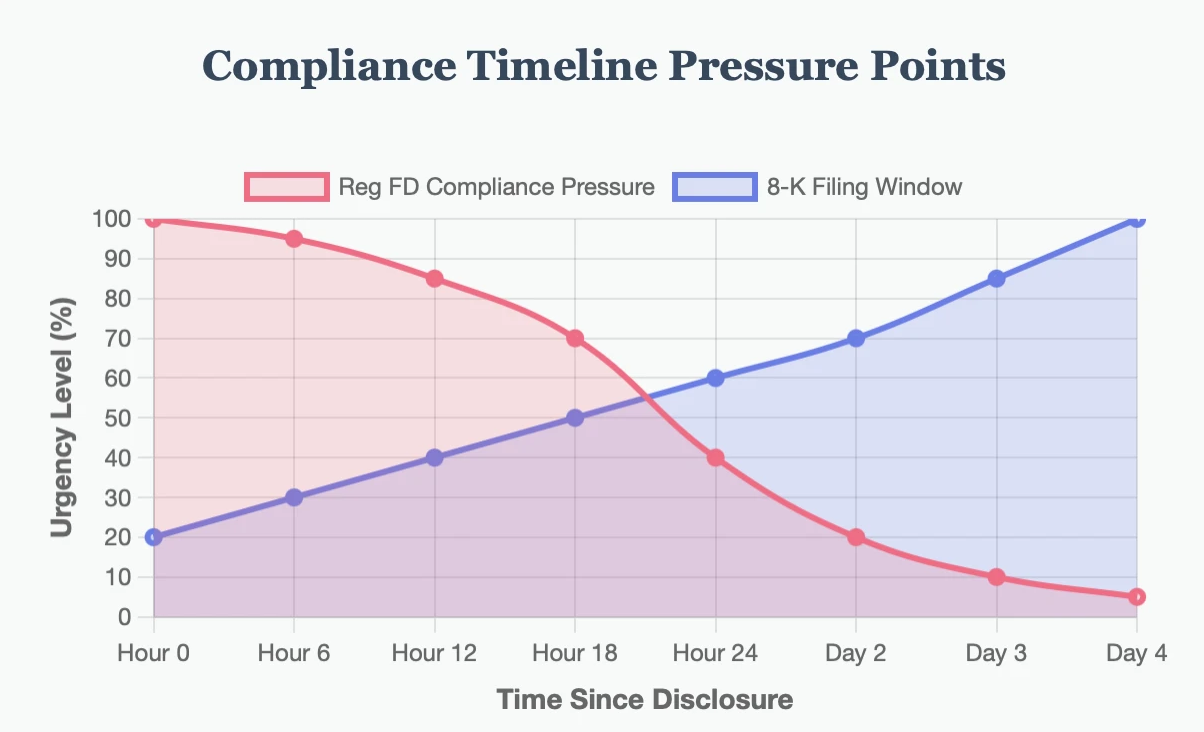

Regulation FD and Form 8-K impose conflicting timelines that create compliance tension. Reg FD requires public disclosure within 24 hours for intentional selective disclosures or as soon as reasonably practicable for unintentional ones, while Form 8-K allows four business days from the triggering event. This mismatch can force companies to file a Form 8-K to cure a Reg FD violation before the 8-K would otherwise have been required.

Adding another layer of complexity is timing. If you inadvertently make a selective disclosure, Regulation FD requires you to make a public disclosure "promptly"—defined as within 24 hours for intentional disclosures or as soon as reasonably practicable for non-intentional ones. But Form 8-K has its own timeline: typically four business days from the triggering event.

This creates a maddening situation: you might need to file a Form 8-K to cure a Reg FD violation before you would have been required to file the Form 8-K for the underlying event itself. You're essentially being forced to publicly disclose information earlier than legally required because you might have accidentally disclosed it to the wrong audience first.

The Materiality Maze

Materiality under securities law involves both qualitative and quantitative assessment of whether information would significantly alter the total mix of information available to investors. The challenge is that executives must make split-second materiality determinations during live conversations, while courts and regulators evaluate those same determinations retroactively with full hindsight, complete information, and unlimited deliberation time.

The concept of materiality is where the catch-22 really tightens its grip. Courts have wrestled with this for decades, and the tests keep evolving. The Supreme Court's definition involves both a qualitative and quantitative assessment: would the information significantly alter the "total mix" of information available to investors?

**The Irony: **Companies are expected to make split-second materiality determinations in live conversations, yet courts and regulators get to evaluate those same determinations with the benefit of hindsight, complete information, and unlimited deliberation time.

Common Pitfalls and How They Happen

The most frequent Reg FD pitfalls include the incremental information problem where individually harmless details combine into material guidance, selective silence where ceasing to share previously routine metrics signals material information, and social media exposure where CEO tweets or LinkedIn posts can trigger disclosure obligations. Each scenario can create Reg FD liability without any single clearly identifiable violation.

The Incremental Information Problem: No single piece of information seems material, but together they paint a revealing picture. An executive mentions that sales in Q3 started "strong," another notes that a key customer is "very satisfied," and a third mentions that manufacturing efficiency has "improved." Individually harmless—collectively, they might be material guidance.

**The Selective Silence Issue: **Sometimes what you don't say is as telling as what you do. If you've historically provided certain metrics or commentary and suddenly stop when asked, sophisticated investors might read that silence as material information itself.

The Social Media Minefield: In today's digital age, what counts as "disclosure" has expanded dramatically. A CEO's tweet, a LinkedIn post, even a comment on a podcast can potentially trigger Reg FD concerns.

The Over-Disclosure Response

Many companies adopt a defensive "when in doubt, disclose" approach that has led to Form 8-K inflation, with hundreds of thousands of filings annually for increasingly minor events. This over-disclosure creates its own risks: investor confusion, dilution of genuinely important information, and potential securities fraud exposure if hastily disclosed information later proves inaccurate or incomplete.

Faced with this uncertainty, many companies have adopted a "when in doubt, disclose" approach. This has led to Form 8-K inflation—companies filing reports for increasingly minor events just to be safe. According to SEC EDGAR filing statistics, the SEC received over 300,000 Form 8-K filings in fiscal year 2023 (SEC, 2024), and the meaningful information can get lost in the noise. Former SEC Commissioner Robert Jackson Jr. observed that "over-disclosure can be just as harmful to investors as under-disclosure when it obscures truly material information."

This defensive posture creates its own problems. Over-disclosure can confuse investors, obscure truly important information, and create legal risks if the disclosed information later proves inaccurate or incomplete. You're damned if you don't disclose (Reg FD violation) and potentially damned if you do disclose incorrectly (securities fraud claims).

Best Practices for Navigating the Catch-22

Implement Robust Pre-Clearance Procedures: Require executives to pre-clear talking points before analyst meetings, conferences, or media appearances.

Create Clear Escalation Protocols: Establish a rapid-response team that can evaluate potential Reg FD issues in real-time.

Maintain Detailed Records: Document what was said, to whom, and when. This creates a contemporaneous record that can be invaluable if questions arise later.

Use Safe Harbor Provisions: Take advantage of Regulation FD's exemptions for communications with certain parties like journalists, rating agencies, and customers (in the ordinary course of business).

**Leverage Technology: **Utilize webcasts, press releases, and social media strategically to broadly disseminate information simultaneously.

**Conduct Regular Training: **Ensure that anyone who might communicate with investors understands Reg FD requirements and can recognize potentially material information.

The Path Forward: Lessons from Two Decades of Reg FD

Two decades of Reg FD enforcement have shown that the SEC evaluates the totality of circumstances and focuses on behavioral patterns rather than isolated incidents. Courts have demonstrated pragmatism, recognizing that perfect compliance is nearly impossible and weighing whether companies made good-faith efforts. The fundamental catch-22 remains, but companies that build robust pre-clearance procedures and escalation protocols can manage the inherent uncertainty.

Since Regulation FD's adoption in 2000, the SEC has clarified through enforcement actions that it evaluates the totality of circumstances. The agency recognizes that mistakes happen and generally focuses on patterns of behavior rather than isolated incidents. The SEC's Division of Enforcement has published guidance indicating that good-faith compliance efforts are considered when evaluating potential Reg FD violations.

Courts have also shown some pragmatism, understanding that perfect compliance is nearly impossible. They tend to focus on whether companies made good-faith efforts to comply and whether any selective disclosure was intentional or part of a pattern.

However, the fundamental catch-22 remains: you can't know with certainty whether information is material until after the market has a chance to react to it. This inherent uncertainty means that companies must err on the side of caution while simultaneously avoiding the trap of over-disclosure.

The Bottom Line: The Regulation FD and Form 8-K catch-22 isn't going away. It's a feature, not a bug, of a regulatory system trying to balance multiple competing interests—investor protection, market efficiency, corporate flexibility, and information transparency. The key to navigating it successfully isn't eliminating risk (impossible) but managing it intelligently through robust procedures, clear communication protocols, and a healthy dose of caution. In the end, the companies that thrive are those that embrace transparency as a principle rather than treating it as merely a compliance obligation.

The dance between disclosure and discretion will continue to challenge corporate America. But with thoughtful policies, vigilant compliance, and a commitment to fair dealing, companies can navigate this regulatory tightrope successfully—most of the time, anyway.