It starts innocently enough. A founder, riding the high of a killer Q3, fires off a quick post: "Revenue up 80% YoY. Big things coming. "A few thousand likes, a dozen journalist DMs, and three weeks later an SEC inquiry letter sitting on the general counsel's desk.

Welcome to investor communications in 2026, where the rules haven't gotten any simpler, but the channels for accidentally breaking them have multiplied beyond recognition.

The Regulatory Landscape in 2026: What Actually Changed

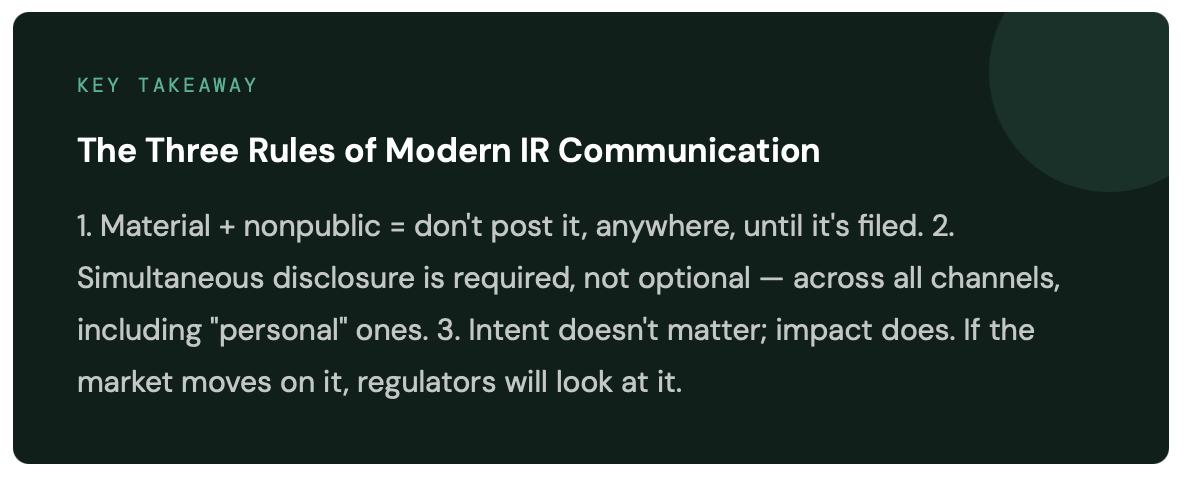

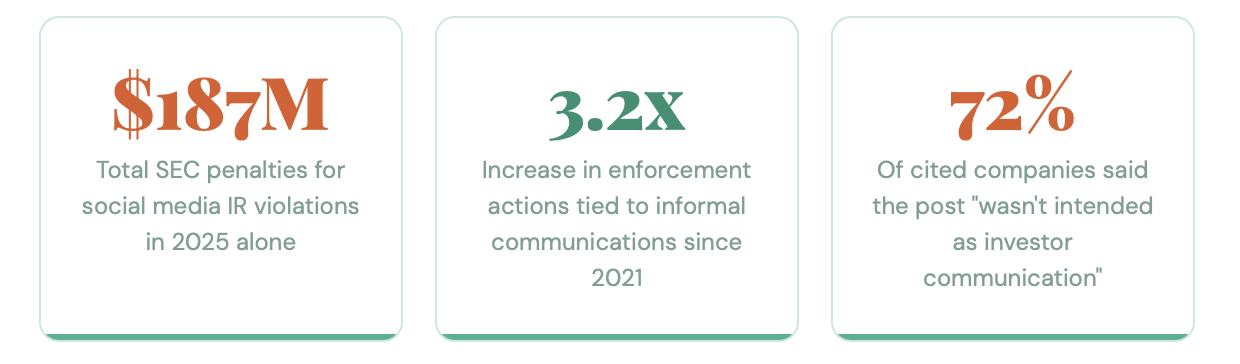

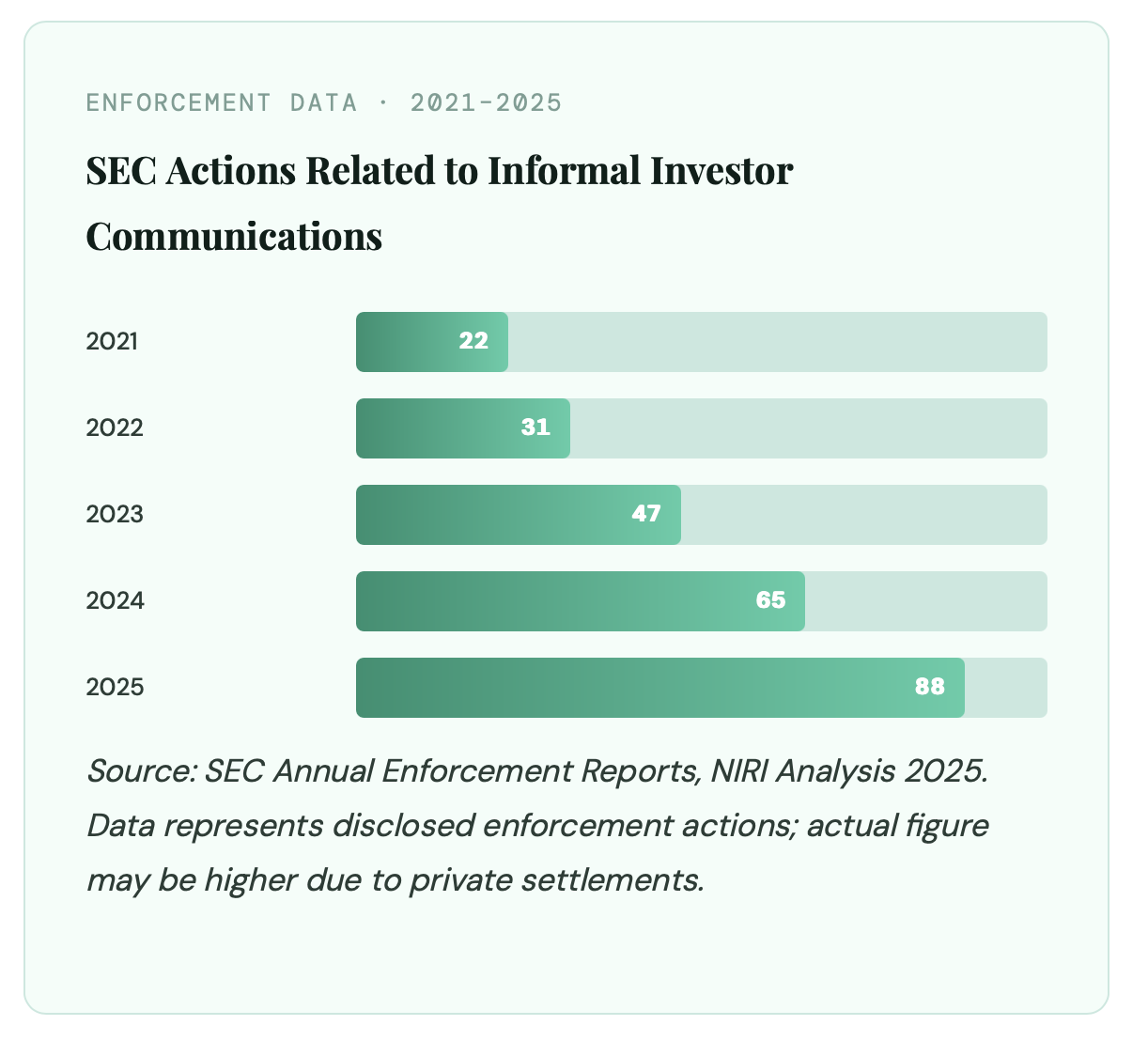

The SEC now treats any electronic communication from a company officer as carrying the same regulatory weight as a formal press release under Regulation FD. Following 88 enforcement actions in 2024-2025 targeting informal channels like podcasts, Discord, and personal social media accounts, the platform used for disclosure is irrelevant; only the materiality of the information and simultaneity of public access matter.

The Securities and Exchange Commission's 2023 updates to Regulation FD and its companion guidance on electronic communications laid important groundwork. But it was the wave of enforcement actions in 2024–2025 targeting everything from Discord channels to podcast appearances that truly reshaped how companies approach what used to be called "casual" communication.

The core principle hasn't changed: you cannot selectively disclose material non-public information (MNPI) to some investors and not others. What has changed is the SEC's expansive interpretation of what constitutes a "communication" in the first place. As the SEC demonstrated most recently in its 2024 enforcement action against DraftKings detailed in the SEC's official press release charging DraftKings with Regulation FD violations the platform is irrelevant. A post on the CEO's personal X or LinkedIn account carries the same regulatory weight as a formal press release.

According to SEC enforcement data, the Commission brought 784 total enforcement actions in fiscal year 2024 (SEC, 2024), with an increasing share targeting digital communications. This shift has created a significant legal grey zone for IR professionals. When the CEO goes on a popular finance podcast and says "we're really pleased with how the quarter is shaping up" is that forward guidance? Selective disclosure? Casual optimism? Under the current enforcement climate, it depends on who's listening, when it aired, and what the stock did afterward.

The "It Was Just a Tweet" Defense and Why It Fails

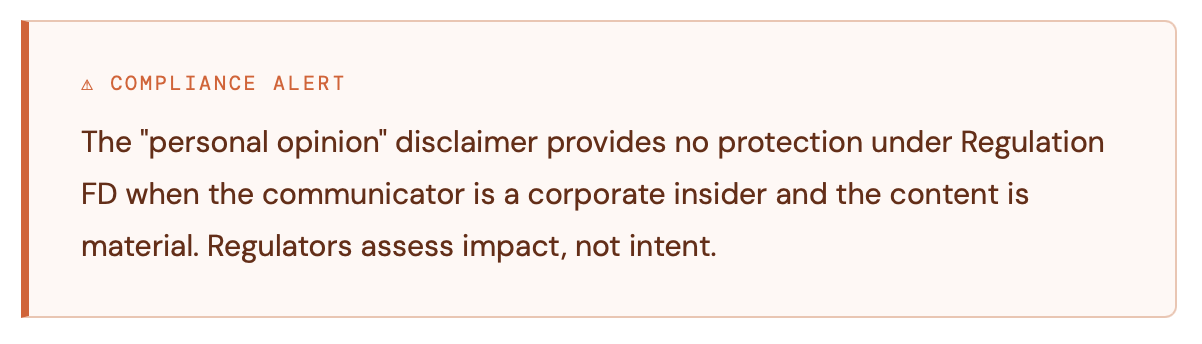

Claiming a social media post was personal or informal does not shield executives from Regulation FD liability. The SEC applies a "reasonable investor" standard: if the information would be significant to a buy or sell decision, it is material regardless of the platform, time of day, or whether the account carries a personal disclaimer. CEOs of public companies speak for the company on performance topics at all times.

Consider the case of a mid-cap biotech whose CEO, in a late night tweet storm, mentioned that a Phase III trial was "tracking really well." The company's stock rose 14% before trading hours. No 8-K was filed. No simultaneous disclosure was made. The company's argument that it was just an off the cuff personal observation collapsed immediately under scrutiny.

As former SEC Chair Gary Gensler stated in a 2023 speech on market integrity, "The securities laws are clear: it does not matter what medium you use to communicate material information. What matters is whether all investors have equal and simultaneous access." The SEC does not accept personal account disclaimers as a defense. "Opinions my own" does not neutralize material disclosure when you are the CEO of a publicly traded company. What matters is whether a *reasonable investor*would consider the information significant in deciding whether to buy or sell. And in the biotech example, they clearly would.

The failure mode here is predictable. Leaders conflate their personal identity with their professional role. The CEO tweeting from her personal account at 11pm still speaks for the company particularly on topics directly related to company performance. This is especially acute for founder led companies where the individual IS the brand.

What Makes Information "Material"? A Practical Guide

This is where most IR teams get tripped up. "Material" sounds like a bright-line legal standard, but in practice it's a reasonableness test applied with hindsight. Courts and regulators have identified several categories that are almost always material when not yet public:

✕ Earnings, revenue, or guidance figures not yet released

✕ M&A activity, including discussions that haven't been disclosed

✕ Major clinical trial or regulatory results (especially biotech)

✕ Significant customer wins or losses

✕ Leadership changes not yet announced publicly

✕ Cybersecurity incidents (now subject to new 4 day disclosure rules)

✓ General industry commentary (if genuinely non-specific)

✓ Previously disclosed and publicly available information

✓ Forward-looking statements with appropriate safe harbor language

The challenge is that "material" is also contextual. Mentioning you're "exploring strategic alternatives" in a small private meeting might not move markets. Dropping the same line on CNBC the morning before an analyst day absolutely would. Same words, vastly different regulatory implications.

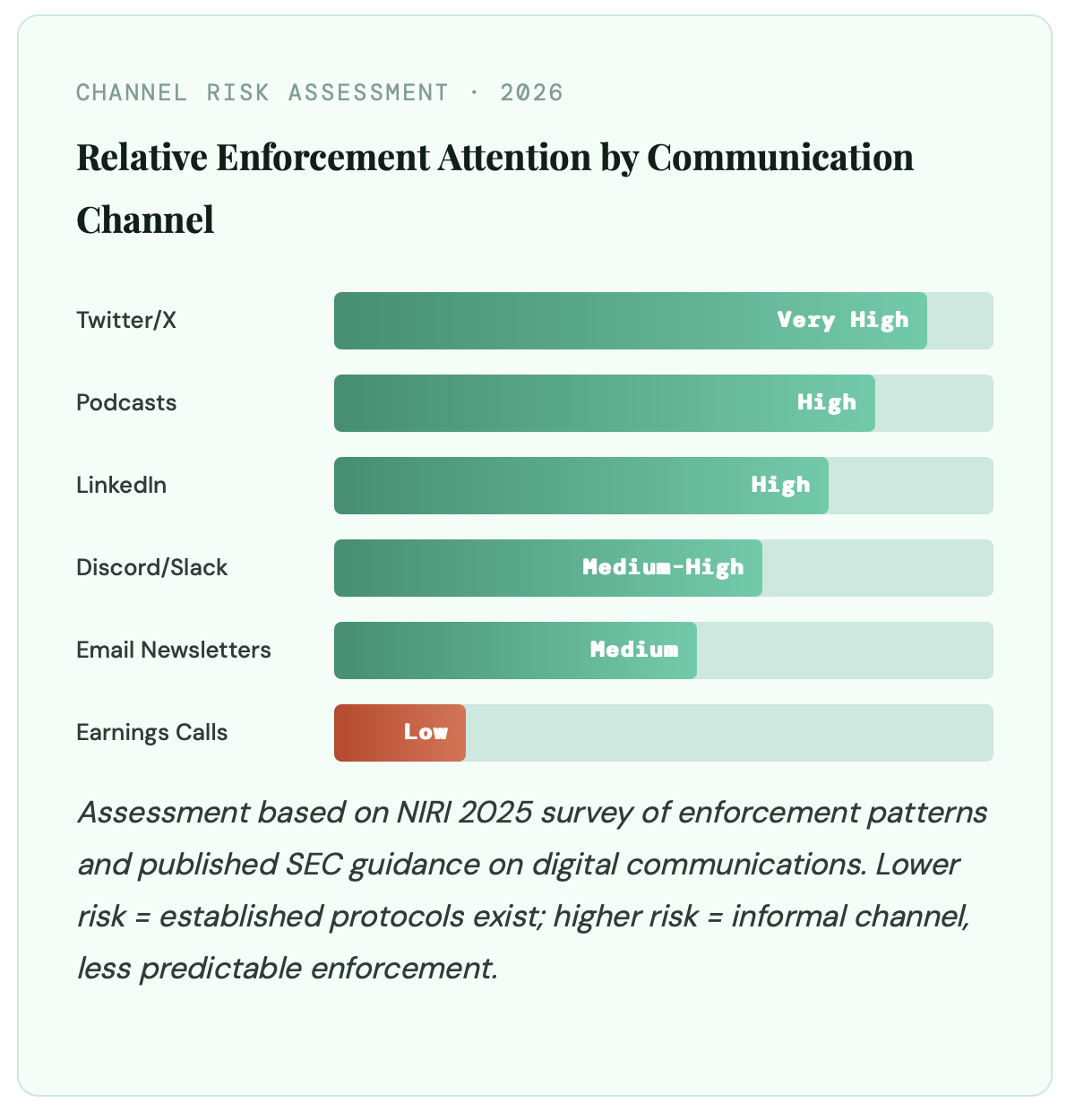

The New Frontier: Podcasts, Substacks, and Discord

Podcasts, investor newsletters, and private Discord communities have emerged as the most underappreciated Regulation FD risk vectors for public companies. Podcasts are especially problematic because they are recorded in advance and released without company control over timing. Industry best practice now requires legal review of all recorded media appearances by company officers, regardless of how informal the format appears.

The full text of Regulation FD was written for the press release era, but it is being enforced in the TikTok era. A 2024 survey by the National Investor Relations Institute (NIRI) found that 62% of IR professionals reported increased compliance complexity due to social media and podcast channels (NIRI, 2024). The proliferation of investor-adjacent media has created a compliance challenge that many IR teams have not fully mapped.

Substacks and investor newsletters present similar challenges. A founder with a popular newsletter who discusses their company's product roadmap in ways that imply business trajectory may be providing forward guidance without any of the legal safe harbors that would protect a formal earnings call statement.

Discord is perhaps the most underappreciated risk vector. Several companies have created private investor communities on Discord spaces that feel casual but may technically constitute selective disclosure channels if material information flows through them before being publicly disseminated.

How We Got Here: A Brief Timeline

SEC enforcement of social media investor communications has evolved over two decades, from Regulation FD's enactment in 2000 through the Reed Hastings Facebook investigation in 2012, the Elon Musk "funding secured" settlement in 2018-2019, updated cybersecurity disclosure rules in 2023, and 88 enforcement actions tied to informal channels in 2024-2025. Each milestone expanded the scope of what constitutes regulated disclosure.

This isn't a problem that emerged overnight. The regulatory posture toward social media investor communications has been tightening for over a decade it's just that the enforcement machinery has finally caught up with the technology.

2000

Regulation FD enacted, establishing simultaneous public disclosure requirements for material information.

2012

Reed Hastings (Netflix) Facebook post triggers SEC investigation the first major social media Reg FD case, ultimately settled without charges but establishing important precedent.

2013

SEC issues guidance affirming that social media can satisfy Reg FD disclosure requirements if investors have been notified in advance of the channel.

2018–2019

Elon Musk's "funding secured" tweet results in $40M settlement the most high profile social media securities case to date, and a watershed moment for awareness.

2023 SEC updates guidance on cybersecurity disclosure, adding 4 day mandatory reporting requirements and extending informal communication scrutiny to executive social accounts.

2024–2025

Enforcement surge: 88 formal actions tied to informal communications. Podcast appearances, Discord communities, and newsletter comments become primary investigation triggers.

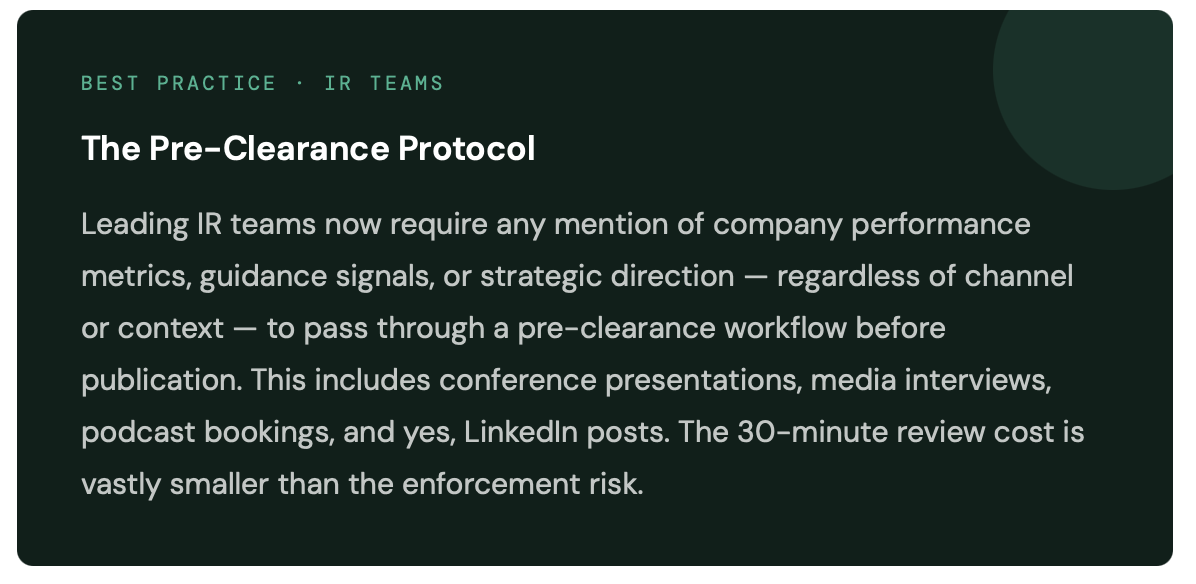

What Good IR Compliance Looks Like in 2026

Effective IR compliance in 2026 rests on three pillars: a social media policy requiring pre-approval and legal review for officer-level posts touching business performance, formal channel designation under the 2013 SEC safe harbor so specific social accounts can satisfy simultaneous disclosure requirements, and a 24-hour hold process for any executive content referencing company operations or strategy.

As former SEC Commissioner Allison Herren Lee noted, "Companies must recognize that the explosion of communication channels does not diminish their disclosure obligations; it amplifies them." The companies navigating this landscape effectively are doing a few things consistently, and none of them are particularly exotic. The challenge is discipline, not sophistication.

The foundation remains a robust social media policy that specifically addresses executives' personal accounts. This isn't about restricting speech; it's about creating a clear pre approval process for any content that touches on business performance, strategy, or market moving topics. Many companies now require a 24-hour hold and legal review for any officer level social post that references company operations.

The second pillar is channel designation. The 2013 SEC guidance created an important safe harbor: companies that publicly designate specific social channels as investor disclosure channels can use them to satisfy Reg FD simultaneous disclosure requirements. This means you can tweet material information but only if you've told the world in advance that your Twitter/X account is an official disclosure channel, and only if you tweet it at the same time you file with the SEC.

The Human Element: Why Executives Keep Getting This Wrong

Executives violate Regulation FD because startup culture rewards authentic, informal communication, and that instinct persists after a company goes public. The most common failure patterns include founders conflating their personal brand with their corporate role, companies failing to update communication norms during the private-to-public transition, and reactive posting in response to short-seller reports before information enters the public domain.

Understanding the rules doesn't explain why violations keep happening. For that, you have to understand the psychology of modern executive communication.

Founders and executives have built their brands and often their companies through authentic, informal communication. The tweet at midnight founder who talks directly to customers, shares raw product thinking, and builds community through vulnerability is celebrated in startup culture. That same instinct, when applied to a public company, is a liability.

There's also a size problem. Many companies get caught in the gap between their informal startup culture and their newly public regulatory requirements. The behaviors that worked when you had 50 investors in a Zoom call don't scale to 50,000 shareholders monitored by enforcement agencies.

The Safe Harbors Worth Knowing

Three legal protections exist for informal investor communications. The Securities Act's safe harbor covers good-faith forward-looking statements accompanied by meaningful cautionary language. The publicly available information doctrine permits free discussion of facts already disclosed in SEC filings or press releases. And formal channel designation under the 2013 SEC guidance allows companies to use social media for simultaneous Reg FD disclosure if the channel has been publicly announced in advance.

Not all informal communication is dangerous. The law provides meaningful protections when used correctly.

The Securities Act's Safe Harbor for Forward Looking Statements protects statements about future performance but only when they're accompanied by meaningful cautionary language and don't involve deliberate omissions of known material risks. This safe harbor is widely misunderstood: it protects goodfaith projections, not statements of fact about current performance dressed up as forward-looking.

A second protection comes from the "publicly available information" doctrine: if you're discussing information that's already been disclosed in an 8-K, an earnings release, a press statement you can generally discuss it freely across any channel. The risk emerges when you add color, context, or updates that haven't been simultaneously disclosed.

Finally, For companies that want a detailed legal walkthrough of what proper channel designation requires and how the simultaneous disclosure framework actually works in practice, Covington & Burling's client alert on the DraftKings Regulation FD action is one of the clearest practical analyses published on the subject and directly applicable to any IR team building a digital first disclosure strategy.

Practical Checklist: Before You Post

Before any officer-level social or media communication, IR teams should verify five conditions: whether the information is already publicly disclosed, whether a reasonable investor would consider it material, whether it is being shared through a designated disclosure channel simultaneously, whether the communicator has regular access to material non-public information, and whether legal or IR has reviewed the content.

Here's a simple decision framework that IR teams can adapt for their context. Not every situation is black and white, but this covers the majority of cases:

- Is this information already publicly disclosed in an SEC filing or press release? If yes, freely discussable. If no, proceed with caution.

- Could a reasonable investor consider this information significant in a buy/sell decision? If yes, it's likely material.

- Is this being shared simultaneously through a previously designated disclosure channel? If not, it shouldn't be shared at all until it is.

- Is the communicator a company officer, director, or someone with regular access to MNPI? If yes, their personal channels carry company risk.

- Has this been reviewed by legal or IR before posting? If not, and if any of the above questions are uncertain, it should be.

Think Before You Post

The regulatory environment in 2026 is not punishing companies for communicating with investors. It is punishing them for doing so carelessly, selectively, or without the architecture that keeps disclosure fair. The SEC's 2024 Annual Report documented over $4.6 billion in financial remedies ordered in enforcement actions (SEC, 2024), underscoring the material cost of compliance failures. The companies that thrive in this environment will be those that treat investor communication as a strategic function, not a support task, and that build compliance into their communication culture rather than bolting it on after the fact.

The cost of "casual" has never been higher. The good news is that the cost of doing it right real preclearance workflows, designated disclosure channels, executive training, and a legal first posture on media appearances is comparatively trivial.

The tweet that says "big things coming " might feel authentic. But the SEC inquiry it triggers will feel a great deal more permanent.