Audit season doesn't arrive twice a year anymore. For most public company disclosure teams, internal audit is a rolling process that runs alongside the close cycle, while external audit the PCAOB-registered engagement shows up in the final weeks before filing and expects everything to already be in order.

The problem most teams describe isn't a lack of preparation. It's duplication. The same evidence gets assembled twice: once for internal audit's quarterly review and again for external audit's year-end procedures. The same disclosure sections get reviewed by two separate teams with two different evidence formats, two different tracking systems, and two sets of follow-up questions that often ask for the same underlying support.

This guide covers the practical difference between internal and external audit in the context of SEC disclosure preparation, where the duplication cost is highest, and how disclosure teams are restructuring their evidence and checklist workflows to serve both audit audiences from a single source without building everything twice.

By the end, you'll understand what each audit function actually looks at in a disclosure context, how evidence traceability requirements differ, and how Finrep's Tesseract QA module auto-generates an audit trail per checklist item that satisfies both internal and external reviewers simultaneously.

What Is the Difference Between Internal and External Audit?

Internal audit is an independent function within the company that evaluates the effectiveness of internal controls, risk management, and governance processes including the controls over financial reporting. External audit is the independent PCAOB-registered engagement that issues an opinion on whether the financial statements present fairly, in all material respects, in conformity with GAAP.

For disclosure teams, the distinction matters in three specific ways.

Scope and timing differ. Internal audit typically runs throughout the year testing controls on a rolling basis, issuing findings during the close cycle, and reporting to the audit committee quarterly. External audit concentrates its substantive testing in the weeks surrounding year-end, though most engagements now include interim procedures in Q3. According to the Institute of Internal Auditors (IIA), internal audit's mandate under the International Standards for the Professional Practice of Internal Auditing is to provide independent assurance on governance, risk management, and control processes. The disclosure team interacts with both audit functions, but at different moments and for different purposes.

Evidence standards differ. Internal audit generally accepts management's internal documentation a completed checklist, a prepared reconciliation, a review sign-off as evidence that a control operated. External audit applies a higher standard: auditors need to independently verify that controls operated effectively, which means the evidence must be traceable to an underlying source they can test. A checklist item that says "disclosure reviewed and approved" satisfies internal audit. External audit wants to see the specific EDGAR peer filings that informed the disclosure, the ASC standard the language was checked against, and the named reviewer's sign-off with a timestamp.

Findings carry different consequences. An internal audit finding on a disclosure control is a management issue it triggers a remediation plan and may require a control deficiency disclosure. An external audit finding at the material weakness level triggers a SOX (Sarbanes-Oxley Act) Section 302 and 906 certification issue that affects the filing itself. According to PCAOB inspection data, approximately 40% of audit engagements inspected in 2023 had at least one deficiency related to internal control testing (PCAOB, 2023). The stakes between internal and external audit findings are not equivalent.

Understanding these differences is the first step toward building a disclosure preparation process that satisfies both without running two parallel workflows.

What Does Internal Audit Actually Look at in a Disclosure Context?

Internal audit's disclosure-related procedures typically focus on the design and operating effectiveness of controls over financial reporting not on the content of disclosures themselves. They are testing whether your team followed the right process, not whether the resulting disclosure language is appropriate.

The specific areas internal audit examines in a disclosure context fall into four categories.

Disclosure controls and procedures. These are the controls your company certifies under SOX Section 302 the processes that ensure material information is identified, escalated, and reflected in disclosures accurately and on time. Internal audit tests whether these controls exist, are documented, and operated during the period. A disclosure team that can produce a timestamped, evidence-linked checklist for each disclosure section showing who reviewed what and when passes this test cleanly. A team that relies on email chains and verbal confirmation does not.

ICFR-Internal Control over Financial Reporting. For disclosure teams, the ICFR controls most relevant are those over the preparation of footnotes, MD&A (Management Discussion and Analysis), and critical accounting estimate disclosures. Internal audit tests whether the right people reviewed these sections, whether the review was documented, and whether changes between draft and final were tracked.

Segregation of duties in the drafting and review process. The person who drafts a disclosure section should not be the only person who reviews and approves it. Internal audit checks that your disclosure workflow enforces this separation that there is a documented second-reviewer step with evidence the review actually occurred.

Completeness of the disclosure checklist. Internal audit will often review the disclosure checklist itself specifically whether it covers all required disclosures for the period, whether each item is mapped to the relevant standard or SEC requirement, and whether any items were signed off without adequate supporting evidence. As former SEC Chief Accountant Paul Munter stated in a 2023 speech, "Effective internal controls over financial reporting remain the foundation upon which reliable financial statements are built."

The PCAOB's auditing standards on internal control specifically AS 2201 on auditing internal control over financial reporting set the framework external auditors use to evaluate what internal audit has already covered. Internal audit teams that align their procedures to AS 2201 create a cleaner handoff to external auditors.

What Does External Audit Focus on That Internal Audit Doesn't?

External audit goes further than internal audit in two dimensions: independence of evidence and sufficiency of substantive testing. Where internal audit tests whether controls exist and operated, external audit tests whether the financial statements and disclosures are actually correct and whether the evidence supporting them would withstand regulatory scrutiny.

The disclosure-specific procedures external auditors run that go beyond internal audit's scope include the following.

Independent verification of disclosure sources. External auditors do not accept management's assertion that a disclosure is consistent with peer practice. They want to see the specific peer filings the team used for benchmarking, with dates, company names, and section references. If your team used Finrep's Tesseract QA module to benchmark disclosure language against EDGAR peer filings, the citation links embedded in each checklist item give auditors exactly what they need without the team having to assemble a separate binder.

ASC standard mapping. Every material accounting policy disclosure should be traceable to the specific ASC paragraph that governs it. External auditors check this mapping not just that the disclosure exists, but that it reflects the correct standard application. A checklist that shows "revenue recognition disclosure reviewed" without a reference to ASC 606-10-50 (Revenue Recognition disclosures) is not sufficient for external audit purposes.

Tie-out of financial statement figures. Every number in the financial statements and footnotes must tie to a source document the auditor can independently inspect a subledger report, a trial balance, a bank statement. This is different from the disclosure language review; it is a numerical accuracy check that is external audit's exclusive domain.

Going concern assessment. Under ASC 205-40 (Presentation of Financial Statements Going Concern), management is required to assess whether conditions raise substantial doubt about the entity's ability to continue as a going concern. External auditors evaluate this assessment independently. For disclosure teams, this means maintaining documented evidence of management's going concern analysis not just the resulting disclosure, but the underlying analysis itself.

The SEC's Division of Corporation Finance comment letter process often surfaces issues that external auditors have already identified internally. A well-maintained audit trail one that shows both the disclosure language and the evidence behind each item is the most effective protection against both SEC comment letters and external audit findings on the same topic.

Where Does the Duplication Happen and What Does It Cost?

Audit preparation duplication concentrates in three areas: evidence assembly, where the same source documents are packaged separately for each auditor; checklist completion, where overlapping disclosure checklists are maintained in parallel; and reviewer documentation, where identical sign-off records are pulled from different systems. This duplication costs mid-size public company teams 3-5 days of incremental work per filing cycle.

The duplication between internal and external audit preparation is concentrated in three activities that most disclosure teams perform twice: evidence assembly, checklist completion, and reviewer documentation.

Evidence assembly is the highest-cost duplication. Internal audit requests evidence of control operation typically a completed checklist, review sign-offs, and documentation that the disclosure was checked against the relevant standard. External audit makes a separate request for evidence of disclosure accuracy the source documents behind the disclosure, the peer filings used for benchmarking, and the ASC mapping for each accounting policy. Most disclosure teams maintain two separate evidence packages because the requests come from different people at different times in different formats. The underlying evidence is often the same; the assembly cost is duplicated.

Checklist completion is the second major duplication point. Many disclosure teams maintain one checklist for internal audit's quarterly DC&P testing and a separate disclosure preparation checklist for the external audit process. Both cover overlapping territory whether each required disclosure is complete, reviewed, and sourced but the formats differ, the ownership differs, and the completion timestamps are recorded separately.

Reviewer documentation. When internal audit asks "who reviewed this section and when?", and external audit asks the same question six weeks later, most teams pull the same information from two different sources an email chain for internal audit's request and a sign-off log for external audit's. The review happened once; documenting it takes twice the effort.

An AICPA survey on audit efficiency found that duplicative audit preparation activities account for 15-20% of total close-cycle hours at mid-size public companies (AICPA, 2024). The aggregate cost of this duplication for a mid-size public company disclosure team runs to 3-5 days of incremental work per filing cycle time spent reassembling evidence that was already assembled in a different format. Teams that eliminate this duplication by building an audit trail that satisfies both audiences simultaneously recover that time for substantive work. Finrep's Tesseract QA module is designed specifically for this: every checklist item auto-generates a timestamped, evidence-linked audit trail as the item is completed so the same record serves both internal and external reviewers without re-assembly.

How Should Disclosure Teams Structure Evidence to Satisfy Both Auditors?

A disclosure evidence structure that satisfies both auditors requires four components per checklist item: a mapping to the governing ASC standard or SEC requirement, embedded source document links such as EDGAR peer filings, a timestamped reviewer sign-off with name and role, and a documented record of any changes between draft and final versions. Building these into the checklist eliminates separate evidence assembly at audit time.

The evidence structure that satisfies both internal and external audit simultaneously has four components. Each must be present for a checklist item to be considered fully evidenced.

1. The checklist item itself, mapped to a standard or requirement. Each disclosure checklist item should reference the specific SEC form requirement, ASC standard, or internal policy that governs it. "Climate risk disclosure reviewed" is insufficient. "Climate risk disclosure reviewed against SEC guidance on climate-related disclosures and benchmarked against Item 1A of 10 peer filings" is traceable. The mapping is what allows both auditors to verify completeness independently.

2. The source documents used to prepare the disclosure. These are the EDGAR peer filings, the ASC codification sections, the PCAOB standards, or the SEC guidance that informed the disclosure language. Source links embedded directly in the checklist item not in a separate binder allow auditors to follow the evidence chain without additional requests.

3. A timestamped reviewer sign-off. Both internal and external audit require evidence that a qualified person reviewed the disclosure, not just that the disclosure was drafted. The sign-off should include the reviewer's name, role, and the date and time of review. This is the evidence that the control operated not just that the process was designed.

4. A record of changes between draft and final. Any material change to a disclosure section between the initial draft and the filed version should be documented what changed, who approved the change, and why. This satisfies both internal audit's ICFR control testing and external audit's tie-out procedures simultaneously.

When these four components are embedded in the checklist item itself rather than maintained in separate systems the audit trail is auto-generated as the disclosure is prepared. There is no assembly step at audit time because the evidence was collected in real time. This is the core design principle behind Finrep's evidence traceability feature: every checklist action opening a peer filing, marking a section reviewed, adding a sign-off is timestamped and linked to the item that triggered it, producing a complete audit trail without additional effort from the disclosure team.

How Does Tesseract QA Connect the Internal and External Audit Workflows?

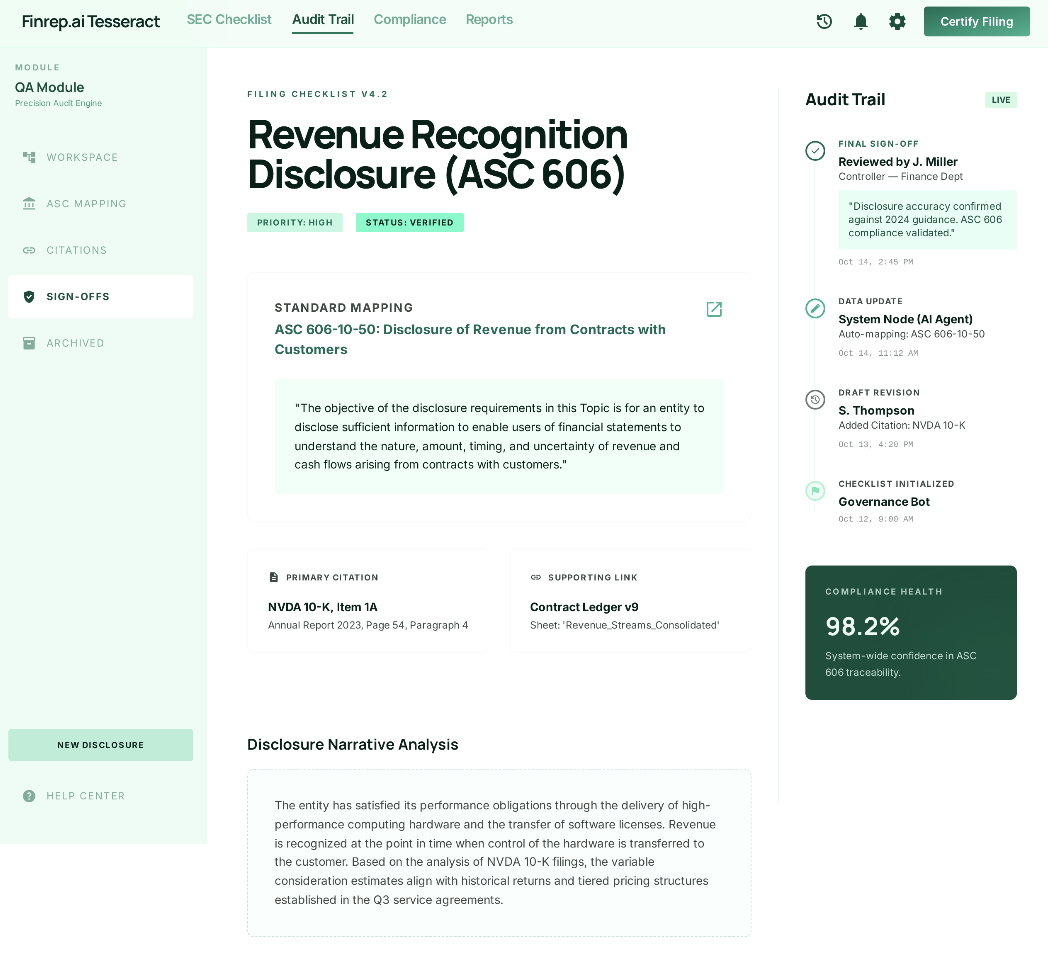

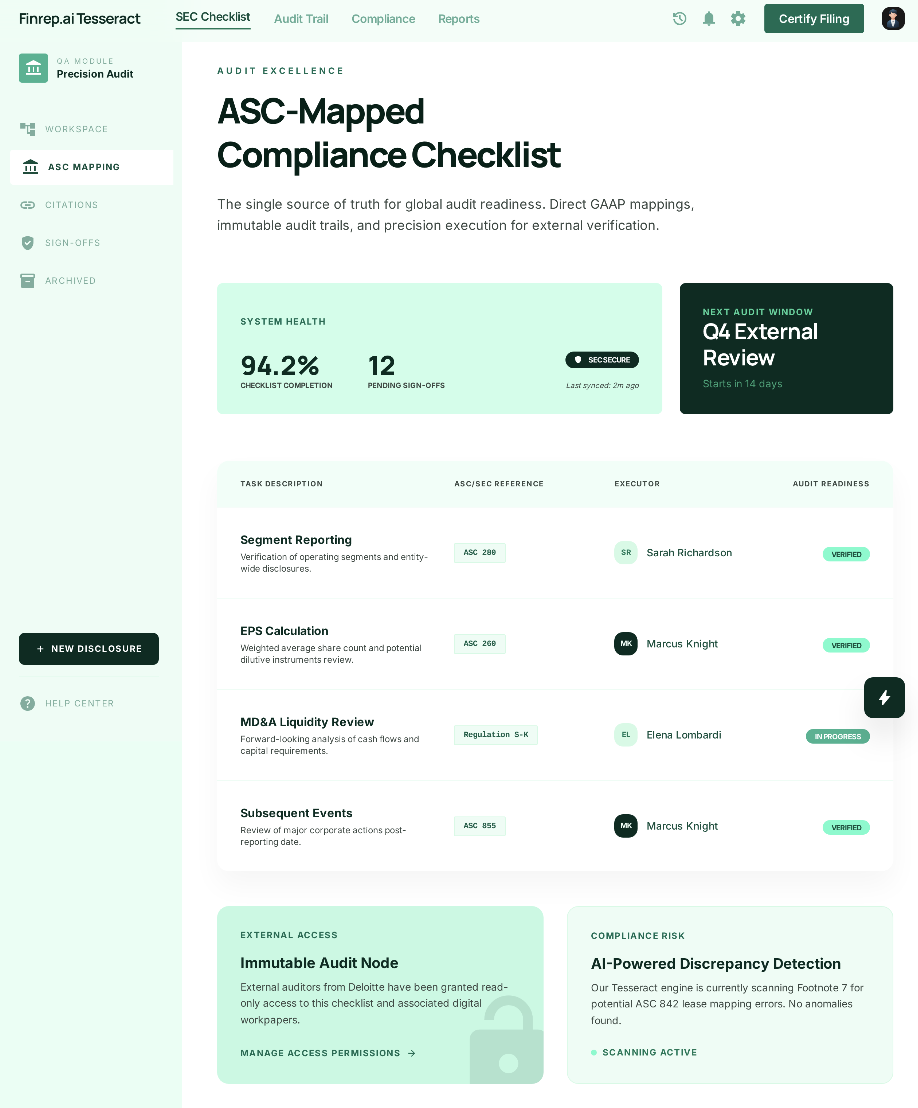

Tesseract QA is Finrep's disclosure quality assurance module a structured checklist environment where each item is mapped to the relevant ASC standard or SEC requirement, linked to source evidence, and tracked through the review and sign-off process. The audit trail it generates is designed to satisfy both internal and external audit requests from a single completion record.

The workflow in practice: a disclosure team member works through the Tesseract QA checklist for a given disclosure section say, the revenue recognition footnote. As they benchmark the language against peer EDGAR filings using Fina, the citations are automatically embedded in the checklist item. When they mark the section reviewed and add their sign-off, the timestamp and reviewer identity are recorded. When a manager approves the final language, that approval is linked to the specific version of the disclosure that was approved.

The resulting record contains everything both auditors need. Internal audit sees: the control operated (checklist item completed), by a qualified reviewer (named sign-off with timestamp), with documented evidence that the process was followed. External audit sees: the specific EDGAR peer filings used for benchmarking, the ASC standard the language was checked against (standard mapping), and who approved the final language (reviewer sign-off chain).

Neither auditor needs to make a separate evidence request. The disclosure team doesn't assemble a separate evidence package for each engagement. The audit trail was built in real time, as the disclosure was prepared.

For teams managing both quarterly 10-Q cycles and the annual 10-K simultaneously, Tesseract QA's ASC-mapped checklist covers the full disclosure universe roll-forwards, new standard adoptions, and required disclosures that must be present even when there is nothing new to say. The ASC-mapped checklist demo shows how each item maps to its governing standard and what a complete evidence record looks like before audit season begins.

What Are the Most Common Audit Findings on Disclosure Controls ?

The disclosure control findings that appear most frequently in both internal audit reports and SEC comment letters share a common root cause: evidence that a control operated was documented after the fact, in response to an audit request, rather than in real time as the control was executed.

The five most common findings and their prevention:

Finding 1: Disclosure checklist items signed off without adequate supporting evidence. The checklist shows completion, but the reviewer cannot produce the source documents that informed the review. Prevention: embed source links in each checklist item at the time of completion not in a separate filing system that gets assembled later.

Finding 2: ASC standard references missing or incorrect. A disclosure is present but not mapped to the specific ASC paragraph that governs it. External auditors flag this because they cannot verify the accounting treatment without knowing which standard was applied. Prevention: build ASC mapping into the checklist structure itself as Tesseract QA does so the standard reference is required before an item can be signed off.

Finding 3: Review sign-offs from the wrong level of reviewer. SOX documentation requires that the reviewer have sufficient seniority and technical knowledge to evaluate the disclosure. A sign-off from a junior staff member doesn't satisfy this requirement even if the disclosure is accurate. Prevention: configure the checklist to require role-specific sign-offs first-level review by a senior reporting professional, approval by the Controller or VP Finance.

Finding 4: No documentation of changes between draft and final. Internal audit finds a difference between the draft disclosure and the filed version with no record of who approved the change. This is an ICFR control failure even if the change itself was appropriate. Prevention: track version history within the checklist every change to a disclosure section after initial sign-off requires a documented reason and re-approval.

Finding 5: Peer benchmarking not documented. External audit asks what peer filings the team reviewed when drafting the disclosure and finds no record. The disclosure may be accurate, but the process cannot be verified. Prevention: citation-link peer filings directly in the checklist item when the benchmarking is performed as Fina's EDGAR research outputs do automatically.

Deloitte's 2025 roadmap to SEC comment letter considerations identifies the disclosure areas most frequently flagged in both comment letters and audit findings MD&A, segment reporting, and EPS are the top three. These are the sections where documentation gaps are most likely to surface.

How Does the Audit Trail Requirement Differ Between SOX and the SEC?

SOX Sections 302 and 906 require certification that disclosure controls operated effectively, while SOX Section 404 requires documented evidence of ICFR design and operating effectiveness. The SEC's Division of Corporation Finance, by contrast, evaluates the substantive accuracy and completeness of disclosures through comment letters, not the controls behind them. A comprehensive audit trail can satisfy all three requirements simultaneously.

The SOX audit trail requirement and the SEC's evidence expectations are related but distinct. Understanding both matters for disclosure teams building a documentation system.

SOX Section 302 and 906 require the CEO and CFO to certify that the filing does not contain material misstatements, that the financial statements fairly present the company's financial condition, and that they have disclosed all significant deficiencies and material weaknesses in internal control. The audit trail that supports these certifications is the documentation that disclosure controls operated effectively the evidence that each required disclosure was reviewed, sourced, and approved by qualified personnel.

SOX Section 404 requires management's assessment of ICFR effectiveness, and for accelerated filers an external auditor's attestation on that assessment. The documentation requirements here are more granular: each key control must be documented with evidence of design effectiveness (the control exists and is designed to prevent or detect errors) and operating effectiveness (the control actually worked during the testing period).

The SEC's evidence expectations are different from SOX's control documentation requirements. The SEC's Division of Corporation Finance, through the comment letter process, evaluates the accuracy and completeness of disclosures not the controls behind them. An SEC comment letter asking a company to "tell us how you determined that your segment reporting meets the requirements of ASC 280" is asking for the substance of the analysis, not the control documentation. The answer must include the actual ASC 280 analysis, not just proof that a review process was followed.

A well-maintained disclosure audit trail satisfies all three: SOX 302/906 certifications (the disclosure process was controlled), SOX 404 testing (the ICFR controls operated), and SEC comment letter responses (the accounting analysis was performed). The FASB Accounting Standards Codification is the authoritative reference for the substantive accounting analysis the audit trail documents that the analysis was performed against this source. According to EY's 2024 Global Board Risk Survey, 68% of audit committee chairs identified disclosure control documentation as a top-three governance priority (EY, 2024).

PCAOB Chair Erica Williams emphasized in a 2023 address that "investors depend on reliable, high-quality audits to make informed decisions, and that reliability starts with well-documented evidence supporting every material assertion in the financial statements."

Frequently Asked Questions

What is the difference between internal and external audit for a disclosure team?

Internal audit evaluates whether disclosure controls and procedures are designed and operating effectively it tests the process. External audit evaluates whether the disclosures themselves are accurate and complete it tests the output. For disclosure teams, internal audit is a year-round control testing function; external audit is a concentrated year-end (and increasingly Q3 interim) evidence review. Both require documentation that the right people reviewed the right disclosures with the right evidence, but external audit requires a higher standard of source traceability.

Why do disclosure teams end up doing audit prep twice?

The duplication typically arises because internal audit and external audit make separate evidence requests at different points in the year, in different formats, with different levels of specificity. Most teams respond to each request separately rather than maintaining a single evidence record designed to satisfy both. The solution is to build the audit trail into the disclosure preparation process itself so the evidence is complete and traceable by the time either auditor asks for it.

What evidence does external audit require for disclosure language?

External auditors require: the specific peer filings or authoritative sources used to develop or benchmark the disclosure language, the ASC standard paragraph that governs the accounting treatment being disclosed, documentation that a qualified reviewer approved the final language, and a record of any changes between the initial draft and the filed version. Evidence assembled after the fact in response to an audit request is accepted but is viewed less favorably than documentation that was maintained in real time.

What is evidence traceability in the context of SEC disclosures?

Evidence traceability means that every element of a disclosure can be traced back to the source document that supports it a specific EDGAR filing, an ASC codification section, a subledger report, or an authoritative guidance document. Finrep's evidence traceability feature embeds citation links directly in each Tesseract QA checklist item as the disclosure is prepared, so the source is permanently linked to the item that references it auditors can follow the chain without requesting additional documentation.

How does Tesseract QA help with both internal and external audit?

Tesseract QA auto-generates a timestamped, evidence-linked audit trail for every checklist item as it is completed. The record contains the ASC standard reference, the EDGAR peer citation links used for benchmarking, the reviewer sign-off with timestamp, and the version history of the disclosure. This single record satisfies internal audit's control documentation requirements and external audit's source traceability requirements without the disclosure team assembling separate evidence packages for each engagement.

What are the most common SOX disclosure control deficiencies?

The most common deficiencies in disclosure controls are: checklist sign-offs without embedded source documentation, missing or incorrect ASC standard references, sign-offs from reviewers who lack sufficient seniority or technical qualification, no documentation of changes between draft and final disclosure, and peer benchmarking that was performed but not recorded. Each of these represents a gap between the control as designed and the control as documented and each is preventable with a structured, evidence-linked checklist system.

Key Takeaways

- Internal audit tests whether disclosure controls operated effectively it evaluates the process. External audit tests whether disclosures are accurate and complete it evaluates the output. The evidence requirements are related but not identical.

- The duplication cost between internal and external audit preparation is concentrated in three activities: evidence assembly, checklist completion, and reviewer documentation. Most teams perform each twice because internal and external audit request the same information in different formats at different times.

- The evidence structure that satisfies both auditors requires four components in every checklist item: a standard or requirement mapping, source document links, a timestamped reviewer sign-off, and a change record between draft and final.

- SOX 302/906 certifications, SOX 404 ICFR testing, and SEC comment letter responses can all be served by the same audit trail if that trail is built into the disclosure preparation process rather than assembled in response to audit requests.

- Tesseract QA auto-generates a complete, timestamped, evidence-linked audit trail per checklist item as the disclosure is prepared eliminating the duplicate assembly step and giving both internal and external auditors what they need from a single record.

- The five most common disclosure control findings missing source evidence, incorrect ASC mapping, wrong-level sign-offs, undocumented changes, and unbenchmarked peer research are all preventable with a structured, evidence-embedded checklist.