Every filing cycle, the same question comes up before the 10-K is finalized: are we disclosing more or less than our peers on ESG? The team reviews a handful of competitor filings, makes a few informal comparisons, and either adds language or decides what they have is adequate.

That informal process works until it doesn't. SEC comment letters on climate risk, human capital, and cybersecurity disclosures have increased sharply since 2023. According to Deloitte's 2025 roadmap to SEC comment letter considerations, ESG-adjacent disclosure topics are now among the top five most commented-on areas in annual filings. The teams most frequently targeted share a pattern: their disclosures were thinner than the peer set, and they had no documented process for checking.

ESG disclosure benchmarking is how reporting teams close that gap, systematically, before the comment letter arrives. This guide covers what ESG benchmarking actually involves in an SEC filing context, how to structure a peer comparison that surfaces real coverage gaps, and how Finrep's Grid Reports feature compresses what used to be a multi-day EDGAR research process into a structured output your team can act on.

By the end, you'll have a clear picture of what a complete ESG benchmarking workflow looks like, which disclosure areas carry the highest comment letter risk, and how to build a peer comparison grid that serves both the drafting team and the auditors reviewing your disclosures.

What Is ESG Disclosure Benchmarking in the Context of SEC Filings?

ESG disclosure benchmarking is the process of comparing your company's environmental, social, and governance disclosures in SEC filings against a defined set of peer companies. The goal is to identify where your coverage is thinner than market practice and where the SEC has been issuing comment letters on similar disclosures.

This is different from voluntary ESG reporting frameworks like GRI (Global Reporting Initiative), SASB (now part of the IFRS Foundation), or TCFD (Task Force on Climate-related Financial Disclosures). Those frameworks govern standalone sustainability reports. SEC ESG benchmarking focuses exclusively on what is disclosed in the 10-K, 10-Q, and 20-F, which are the mandatory filings where the SEC's Division of Corporation Finance (CorpFin) has enforcement authority. As SEC Chief Accountant Paul Munter stated in a 2024 address, "the disclosure requirements in Regulation S-K apply to all material risks, including those related to environmental and social matters."

The three disclosure areas under active SEC scrutiny in 2026 are climate risk (Item 1A risk factors and MD&A), human capital (Item 1 business description), and cybersecurity (Item 1C, introduced as a required disclosure in 2023). For each one, the benchmark question is not whether you have a disclosure. Most companies do. The question is whether your disclosure is substantively comparable to peers in depth, specificity, and coverage of the topics the SEC has flagged as priorities.

Teams that run a structured ESG disclosure benchmark before finalizing their 10-K are doing two things at once: improving disclosure quality, and building a documented record that the review was performed. That record matters when the SEC asks.

Why Has SEC ESG Disclosure Enforcement Increased Since 2023?

SEC ESG disclosure enforcement has increased since 2023 due to three converging factors: the 2023 cybersecurity disclosure rule requiring material incident reporting and program descriptions, continued enforcement of existing climate risk disclosure obligations under MD&A, and the SEC pushing for greater specificity in human capital disclosures including headcount, turnover rates, and training investment. In each case, the SEC compares filer disclosures against peer practice.

SEC comment letter activity on ESG topics, particularly climate, human capital, and cybersecurity, has risen materially since 2023 for three specific reasons. According to KPMG's 2024 SEC comment letter analysis, ESG-related comments now represent approximately 15% of all CorpFin comment letters, up from less than 5% in 2020.

The first is the 2023 cybersecurity disclosure rule, which took effect for most filers in December 2023. The SEC's cybersecurity disclosure rules require companies to disclose material cybersecurity incidents within four business days of determining materiality, and to describe their cybersecurity risk management program in the annual 10-K. The SEC's CorpFin staff began reviewing these disclosures immediately and has issued comment letters on their specificity and completeness since early 2024.

The second is the continued enforcement of existing climate risk disclosure obligations under Item 1A and Item 7 (MD&A). Even without a final mandatory climate rule, the SEC has consistently enforced the requirement that known trends and uncertainties be disclosed. Climate-related risk qualifies. Comment letters asking companies to "explain why you have not disclosed quantitative information about your climate-related risks" have become common. They tend to target companies whose disclosures are qualitative only while direct peers provide quantitative estimates.

The third is human capital disclosures under Item 1. Since 2020, public companies have been required to provide a description of their human capital resources material to an understanding of the business, as mandated by the SEC's 2020 modernization of Regulation S-K. The SEC has been pushing for more specificity, including headcount by geography, turnover rates, and training investment metrics. As former SEC Chair Gary Gensler stated, "investors need reliable information about the human capital that drives a company's value." Companies whose human capital section is thinner than peers have increasingly received comments requesting enhancement.

The pattern in each case is the same: the SEC compares your disclosure to peers. If your peers disclose more, you may receive a comment letter asking why. Benchmarking against those peers before filing is the most reliable way to anticipate and address gaps.

What Should a Peer Set for ESG Disclosure Benchmarking Include?

An SEC ESG benchmarking peer set should include eight to twelve companies selected using four filters: SIC code for industry comparability, revenue range within one order of magnitude, filing recency within 18 months, and similar regulatory exposure such as accelerated filer status. The peer set must reflect SEC filing comparability, not ESG reporting reputation, because the SEC compares disclosures within SIC codes and revenue bands.

A peer set for ESG disclosure benchmarking should include eight to twelve companies comparable to yours in industry, size, and geographic footprint. The key is selecting them for SEC filing comparability, not for their ESG reporting reputation.

This is an important distinction. ESG peer sets for voluntary framework benchmarking often include best-in-class reporters regardless of industry comparability. SEC filing peer sets must reflect what the SEC would consider genuinely comparable companies when reviewing your disclosures. An SEC comment letter on your climate risk disclosure will implicitly compare you to companies in the same SIC (Standard Industrial Classification) code and revenue range, not to sustainability leaders in other industries.

The four filters for building a defensible SEC filing peer set:

Industry comparability. Use SIC code as the primary filter, not industry description text. For a cloud software company, SIC 7372 (Prepackaged Software) is more precise than "technology" or "software." Peer disclosures from the same SIC carry more weight in an SEC comment response.

Revenue range. Companies in a meaningfully different revenue band face different materiality thresholds and disclose accordingly. A $500M company's human capital section is not a meaningful benchmark for a $10B company. Keep your peer set within one order of magnitude of your revenue.

Filing recency. ESG disclosure practice is evolving rapidly, particularly on climate and cybersecurity. Peer filings from more than 18 months ago may reflect a prior standard. Prioritize the most recent 10-K filed by each peer company.

Regulatory exposure similarity. If you are an accelerated filer, benchmark against other accelerated filers. If you have international operations that trigger additional environmental disclosure requirements, include peers with similar geographic exposure.

Deloitte's 2025 roadmap to SEC comment letter considerations confirms that MD&A, segment reporting, and now ESG-adjacent disclosures are among the most commented-on areas. A well-constructed peer set is your first line of defence.

How Do You Run an ESG Disclosure Benchmark Against EDGAR Peer Filings?

An ESG disclosure benchmark against EDGAR filings follows five steps: define specific disclosure topics like climate transition risk or cybersecurity governance, build a peer universe filtered by SIC code and filing type in EDGAR, extract relevant sections from each peer's 10-K covering Items 1, 1A, 1C, and MD&A, build a comparison grid showing coverage levels per topic per peer, and identify gaps where your disclosure falls below peer median for targeted remediation.

Running an ESG disclosure benchmark against EDGAR peer filings involves five steps. Done manually, this process takes 3 to 5 days per filing cycle. According to a PwC 2024 SEC reporting survey, 82% of SEC reporting teams spend more than two full business days on peer benchmarking per topic area. Done with Finrep's Grid Reports, it produces a structured comparison output in under an hour.

Step 1: Define your disclosure topics. Before searching EDGAR, define the specific ESG topics you are benchmarking. Not "ESG" as a broad category, but specific disclosure areas: climate physical risk, climate transition risk, Scope 1 and 2 emissions methodology, human capital headcount metrics, employee turnover disclosure, cybersecurity governance structure, and material incident disclosure. Each topic becomes a column in your comparison grid.

Step 2: Build your peer universe in EDGAR. Search EDGAR's company database filtered by SIC code and filing type (10-K or 10-K/A). Add date range constraints to retrieve only the most recent annual filings. For each peer company, note the CIK (Central Index Key), which is the identifier you'll use to retrieve their filings directly. EDGAR Full-Text Search is the starting point for this retrieval.

Step 3: Extract the relevant sections. For each peer filing, extract the sections covering your benchmark topics: Item 1 (business description and human capital), Item 1A (risk factors covering climate and cybersecurity), Item 1C (cybersecurity), and MD&A Item 7 (climate risk discussion). Manual extraction from a 120-page 10-K PDF for twelve peer companies is the step that consumes most of the time. Finrep's Grid Reports feature performs this extraction simultaneously across all peers, returning section-level text linked to the source filing.

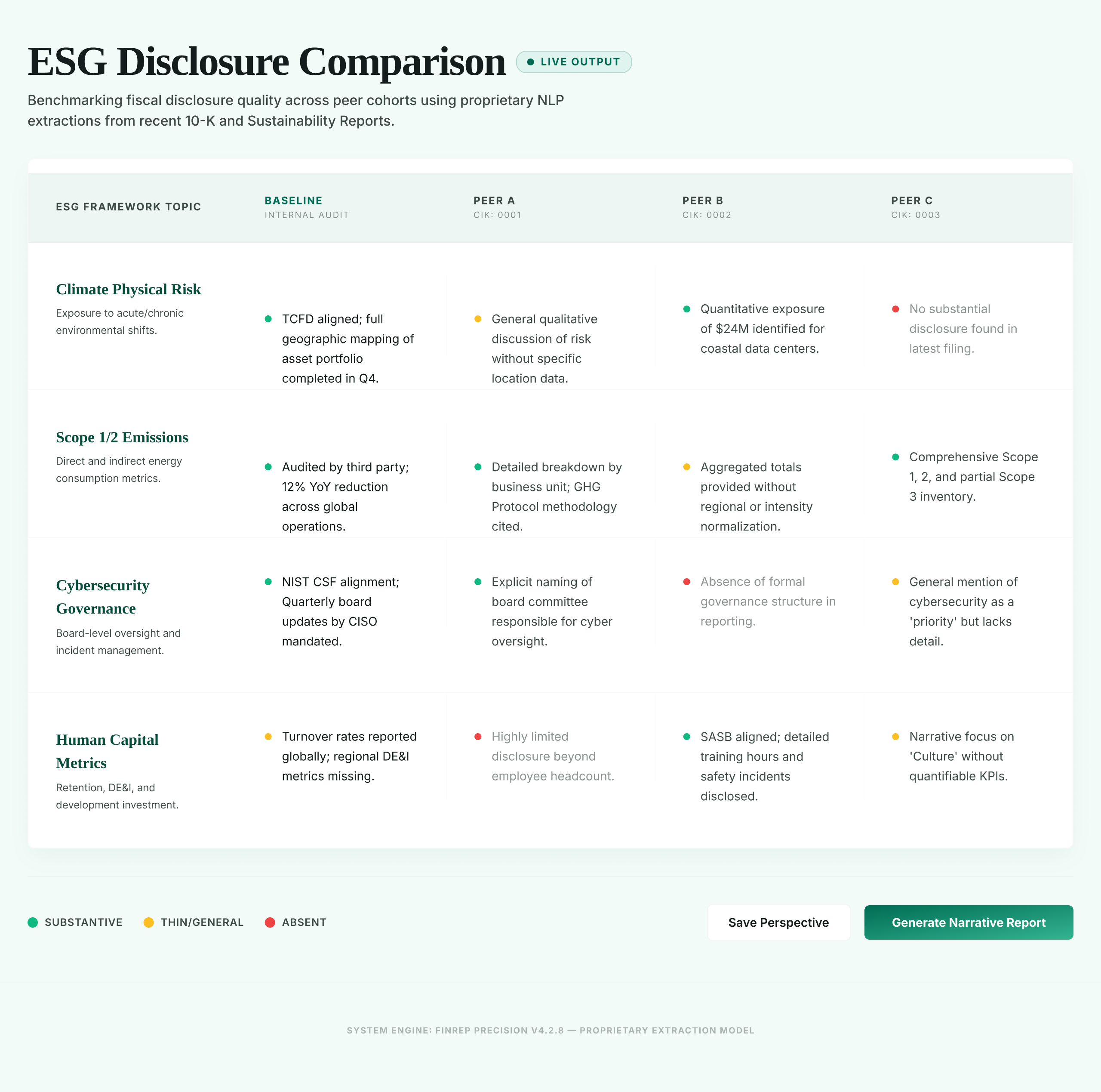

Step 4: Build the comparison grid. Structure the output as a matrix with peers as rows and disclosure topics as columns. For each cell, record whether the disclosure is present, whether it is qualitative or quantitative, and whether it references a specific framework (TCFD, SASB, GRI). The grid immediately surfaces which topics your disclosure is thinner on than the majority of peers.

Step 5: Identify and close gaps. For each gap, which is a topic where you disclose qualitatively while most peers disclose quantitatively, or a topic present in most peer disclosures but absent from yours, draft a remediation note. This should cover what additional disclosure is warranted, what the source language from peers looks like, and what the risk of leaving the gap open is given current SEC comment letter activity.

This five-step process is the structure Finrep's Grid Reports workflow follows. The Disclosure Comparison module presents the grid output with peer language visible per cell, SEC comment letter frequency data per topic, and a gap summary that flags the highest-risk omissions for the drafting team's immediate attention.

Which ESG Disclosure Topics Carry the Highest SEC Comment Letter Risk in 2026?

The ESG disclosure topics with the highest SEC comment letter risk in 2026 are cybersecurity risk management program specificity, climate risk quantification in MD&A, and human capital metrics detail, in that order. Each has a documented pattern of SEC comment letters requesting more specific disclosure from companies whose peers provide greater detail.

Cybersecurity risk management program (Item 1C). The 2023 SEC cybersecurity rule requires companies to describe their processes for assessing, identifying, and managing material cybersecurity risks. Comment letters on Item 1C have primarily targeted disclosures that describe a cybersecurity program in generic terms, such as "we have policies and procedures to manage cybersecurity risk," without specifying the framework used (NIST, ISO 27001, SOC 2), the board oversight structure, or how the company assesses materiality of incidents. As PCAOB Chair Erica Williams has noted, cybersecurity controls are increasingly relevant to the integrity of financial reporting systems. If your peers are naming their frameworks and describing board-level oversight mechanisms, the SEC will compare their disclosures against yours.

Climate risk in MD&A (Item 7). The SEC's longstanding guidance on MD&A disclosures requires companies to discuss known trends, events, or uncertainties that have materially affected or are reasonably likely to affect results. Climate-related costs and regulatory exposure qualify. Comment letters have targeted companies that describe climate risk in Item 1A (risk factors) but do not discuss it in MD&A as a business impact. The SEC's position is that if climate risk is material enough to warrant a risk factor, it is material enough to warrant MD&A discussion. Companies in carbon-intensive sectors or with significant real estate or supply chain exposure receive more scrutiny.

Human capital metrics (Item 1). The 2020 human capital disclosure rule requires material information about your human capital resources. What counts as "material" has been clarified through comment letters. The SEC has pushed for total headcount, turnover rates where material, and workforce development metrics. Companies reporting only headcount totals while peers disclose turnover, diversity metrics, and training investment consistently receive enhancement requests. The SEC's Division of Corporation Finance human capital guidance makes clear that "material" is assessed relative to what a reasonable investor would consider significant.

For each of these topics, the remediation path is the same: benchmark against direct peers in EDGAR, identify the median disclosure level for your SIC code and revenue range, and bring your disclosure to or above that median before filing.

How Does Finrep's Grid Reports Feature Work for ESG Benchmarking?

Grid Reports is an EDGAR-native tool that automates ESG peer disclosure comparison by extracting section-level text from up to 15 peer 10-K filings, mapping extracts to benchmark topics, and presenting results in a color-coded matrix showing coverage levels per peer per topic. The output includes citation links to source filings and a gap summary ranked by SEC comment letter frequency for the filer's SIC code.

Finrep's Grid Reports is an EDGAR-native peer comparison feature that builds a structured ESG disclosure benchmark grid from a defined peer set. Section-level text extraction, coverage status indicators, and gap analysis are all built into the output.

The five-step workflow in Grid Reports:

Step 1: Define peers. Enter your peer universe (up to 15 companies) by company name or CIK. Finrep queries EDGAR to retrieve the most recent 10-K filing for each company automatically.

Step 2: Select topics. Choose the ESG disclosure topics to benchmark from the topic library, which includes climate physical risk, climate transition risk, Scope 1/2 emissions, human capital headcount, turnover, DEI metrics, cybersecurity framework, incident disclosure, and board oversight. You can also define custom topics by entering the specific language to search for.

Step 3: Run the extraction. Fina extracts the relevant section text from each peer filing simultaneously, covering Item 1, Item 1A, Item 1C, and MD&A, and maps each extract to the benchmark topic it covers. Extraction across 12 peers takes under 3 minutes.

Step 4: Review the grid. The Grid Reports output presents a matrix where each peer filing is a row and each benchmark topic is a column. Each cell shows the coverage level (absent, qualitative only, quantitative, or framework-referenced) with the source text accessible by clicking the cell. Coverage levels are color-coded: green (present and substantive), amber (present but thin), and red (absent or materially below peer median).

Step 5: Export the gap summary. The gap summary identifies the topics where your disclosure, entered as a baseline row at the top of the grid, falls below the peer median. For each gap, it shows the peer with the strongest disclosure on that topic as a reference point, and the SEC comment letter frequency for that topic in your SIC code.

The output is citation-linked to EDGAR source filings at the section level. Every peer comparison cell links to the exact paragraph in the source filing it draws from. This makes the Grid Reports output audit-ready: both internal and external reviewers can verify every benchmark data point independently.

For teams that currently run this process manually, the Grid Reports workflow reduces ESG benchmarking time from 3 to 5 days to under two hours per filing cycle (Finrep client data, 2025).

What Does a Coverage Gap in ESG Disclosure Actually Look Like?

A coverage gap in ESG disclosure is a specific topic that your peers disclose at a level of detail the SEC considers adequate, that is absent or materially thinner in your filing. Coverage gaps are not about having different disclosures from peers. They are about disclosing less on topics where the SEC has established expectations through comment letter patterns.

Three concrete examples of coverage gaps that commonly appear in ESG benchmarking:

Gap 1: Qualitative-only climate risk while peers disclose quantitative exposure. Your Item 1A states that climate-related regulatory changes "could" increase operating costs. Your five direct peers all quantify the potential financial impact of carbon pricing in their MD&A, citing a range of $X million to $Y million under specific regulatory scenarios. The SEC has commented on this gap in multiple filings in your SIC code. Closing the gap means adding a quantitative estimate of your climate-related cost exposure to MD&A, with the scenarios and methodology disclosed.

Gap 2: Cybersecurity framework not named while peers specify it. Your Item 1C describes your cybersecurity risk management process in general terms. Nine of your twelve peers name the specific framework governing their program (NIST CSF, ISO 27001, SOC 2). The SEC has commented on Item 1C disclosures that are less specific than peer practice. Closing the gap means naming the framework your program follows and describing how the board receives cybersecurity risk information.

Gap 3: Human capital section with headcount only while peers disclose turnover and training. Your Item 1 human capital section states total headcount. Six of your twelve peers disclose annual voluntary turnover rate, total learning and development investment, or both. The SEC has issued enhancement requests on human capital sections that provide only headcount for companies whose peers disclose more. Closing the gap means adding the metrics your peers are providing. Start with voluntary turnover rate if that is the most common additional disclosure in your peer set.

In each case, the gap is identified by the benchmark and quantified by the peer comparison grid. The remediation is targeted and documentable. You can show exactly which peer disclosures informed your update and why.

The Harvard Law School Forum on Corporate Governance tracks SEC comment letter patterns on ESG topics, including the specific language CorpFin has been using in climate and human capital comment letters since 2023. It is the best secondary source for understanding where the SEC's expectations currently sit.

How Do You Respond to an SEC Comment Letter on ESG Disclosures?

An SEC comment letter on an ESG disclosure requires the same response structure as any other comment letter. There is one additional challenge: the SEC's question is often implicitly comparative. It may ask why your disclosure does not include something that your peers disclose. The best response requires demonstrating that you reviewed peer practice and made a considered disclosure decision.

The SEC's Staff Legal Bulletin No. 4 provides general guidance on the comment letter process. The response structure for an ESG comment letter on disclosure adequacy has four components.

Acknowledge the comment and describe your review process. The response should explain that you reviewed peer disclosures in EDGAR for companies in your SIC code and revenue range before preparing your filing. Naming the specific peer companies and filings you reviewed strengthens the response. It demonstrates that your disclosure decision was informed, not inadvertent.

Explain the disclosure decision. If you disclosed qualitatively while peers disclosed quantitatively, explain the basis for the difference. Valid bases include: the information was not reasonably estimable at the time of filing, the disclosure would constitute forward-looking guidance requiring safe harbor language, or the quantitative difference between your exposure and peers' exposure is not material given your business model.

Commit to enhanced disclosure in future filings. In most cases, the most efficient path is to agree to enhance the disclosure in the next filing and provide a sample of the proposed enhanced language. The SEC generally accepts prospective remediation for first-time comments on disclosure adequacy.

Use peer filings as the reference point. The response is strengthened by referencing the specific EDGAR filings that establish peer practice, including company names, filing dates, and the specific section containing the disclosure you are benchmarking against. Finrep's Disclosure Comparison module surfaces these references automatically as part of the Grid Reports output.

Comment letter correspondence, including both the SEC's initial letters and company responses, is public in EDGAR under form types UPLOAD and CORRESP. Before drafting your response, search EDGAR for responses from peers who have received similar comments on the same ESG topic. Their response language and the SEC's follow-up (or lack of it) tells you what the staff considers an adequate response.

Frequently Asked Questions: ESG Disclosure Benchmarking

What is ESG disclosure benchmarking for SEC reporting teams?

ESG disclosure benchmarking is the process of comparing your company's environmental, social, and governance disclosures in mandatory SEC filings (the 10-K, 10-Q, and 20-F) against a defined peer set. The goal is to identify where your coverage is thinner than peer practice and where the SEC has been issuing comment letters. It is different from voluntary ESG framework benchmarking and focuses on the disclosures subject to SEC enforcement: climate risk (Item 1A and MD&A), human capital (Item 1), and cybersecurity (Item 1C).

Which SEC filing sections require ESG-related disclosures?

Four sections of the 10-K contain ESG-related mandatory or enforcement-active disclosures: Item 1 (business description covering human capital resources), Item 1A (risk factors covering climate risk and cybersecurity risk), Item 1C (cybersecurity risk management program, required since December 2023), and Item 7 (MD&A covering known trends and uncertainties including climate impact on results). The SEC has issued comment letters on all four sections requesting more specific disclosure from companies whose filings are thinner than peers.

How do you find peer ESG disclosures in EDGAR?

Peer ESG disclosures are accessible through [EDGAR Full-Text Search](https://efts.sec.gov/LATEST/search-index?q=%22ESG%22&dateRange=custom&startdt=2024-01-01&forms=10-K), filtered by form type (10-K), SIC code, and date range. To retrieve specific sections like Item 1A, Item 1C, or MD&A, you must open the full filing and navigate manually, or use a tool like Finrep's Grid Reports that performs section-level extraction across multiple peer filings at once. Comment letter correspondence on ESG topics is searchable in EDGAR under form types UPLOAD (SEC letters) and CORRESP (company responses).

What does Finrep's Grid Reports do for ESG benchmarking?

Grid Reports is Finrep's EDGAR-native peer comparison feature. You define the peers and topics. Fina extracts the relevant section text from each peer's most recent 10-K. The output is a color-coded comparison matrix showing coverage level (absent, qualitative, quantitative, or framework-referenced) per peer per topic, with source text and EDGAR citation links accessible per cell. The gap summary identifies where your baseline disclosure falls below peer median, ranked by SEC comment letter frequency for your SIC code.

How long does ESG disclosure benchmarking take without a tool?

Manual ESG benchmarking against EDGAR peer filings, including retrieving twelve 10-K filings, extracting four sections per filing, and building a comparison grid, takes 3 to 5 days of analyst time per filing cycle. With Finrep's Grid Reports, the same benchmark runs in under two hours (Finrep client data, 2025). The time saving comes from automated section extraction and grid population. The judgment work of interpreting the gaps and deciding on remediation still requires your team.

Can ESG benchmarking help prevent SEC comment letters?

It significantly reduces the risk. The SEC's comment letter review process is implicitly comparative. Staff compare your disclosures to peers in the same SIC code and revenue range. Companies whose disclosures are materially thinner than the peer set are more likely to receive comments requesting enhancement. Completing a structured benchmark before filing, and documenting that the benchmark was performed, both improves disclosure quality and provides a defensible process record if a comment letter does arrive.

Key Takeaways

- ESG disclosure benchmarking in an SEC context focuses on 10-K mandatory disclosures: Item 1 (human capital), Item 1A (climate and cybersecurity risk factors), Item 1C (cybersecurity risk management), and MD&A (Item 7). It is not about voluntary ESG reports or sustainability frameworks.

- SEC comment letter activity on ESG topics has increased materially since 2023, driven by the cybersecurity disclosure rule, continued MD&A climate risk enforcement, and human capital specificity requests. The companies most frequently targeted are those whose disclosures are thinner than their SIC peer set.

- A defensible ESG benchmarking peer set uses SIC code, revenue range, filing recency, and regulatory exposure similarity as selection criteria. ESG reputation is not a relevant filter.

- The five-step benchmarking workflow is: define topics, build the peer universe in EDGAR, extract the relevant sections, build the comparison grid, and identify and remediate gaps. Manual execution takes 3 to 5 days. Finrep's Grid Reports compresses it to under two hours.

- The three highest-risk ESG coverage gaps in 2026 are: qualitative-only climate risk in MD&A while peers quantify exposure; unnamed cybersecurity framework in Item 1C while peers specify it; and headcount-only human capital while peers disclose turnover and training investment.

- Grid Reports output is citation-linked to EDGAR source filings at the section level, making every peer comparison cell verifiable by internal and external reviewers without additional documentation requests.