How Diverging Big 4 Guidance on PIK Preferred Created a Real Reporting Problem

The first PIK preferred conversation worth remembering went something like this. Two technical accounting leads at companies in the same sector were reviewing what was effectively the same instrument and arriving at materially different numbers in their EPS calculation. One team was measuring the dividend at fair value. The other was applying the contractual rate to the liquidation preference. Both had a Big 4 interpretive guide on their desk supporting the choice they had made. Neither of them was wrong.

That gap the one that produced two defensible answers to the same question is what FASB closed on April 23, 2026 with Accounting Standards Update No. 2026-01. For fiscal years beginning after December 15, 2026, there is one measurement rule for paid-in-kind dividends on equity-classified preferred stock, and the discretionary versus nondiscretionary analysis that drove most of the prior practice difference no longer applies.

If your company has equity-classified PIK preferred on the balance sheet, this applies to you. The fact pattern shows up most often in post-SPAC technology issuers, biotech and life sciences companies that funded through convertible preferred rounds, energy companies that emerged from Chapter 11 with multiple tranches, and diversified holding companies with NAV-linked accretion mechanics. Your EPS math, your transition footnote, and your disclosure committee briefing for the 2026 and 2027 cycles all change.

This piece is for SEC reporting teams, technical accounting groups, and CFO controllers' offices working through what to do before adoption. It is built around three things that actually move: the new rule and what it costs you, the transition decision you have to make, and the SEC comment-letter pattern most teams will miss.

What Does ASU 2026-01 Actually Require for PIK Preferred Stock Measurement?

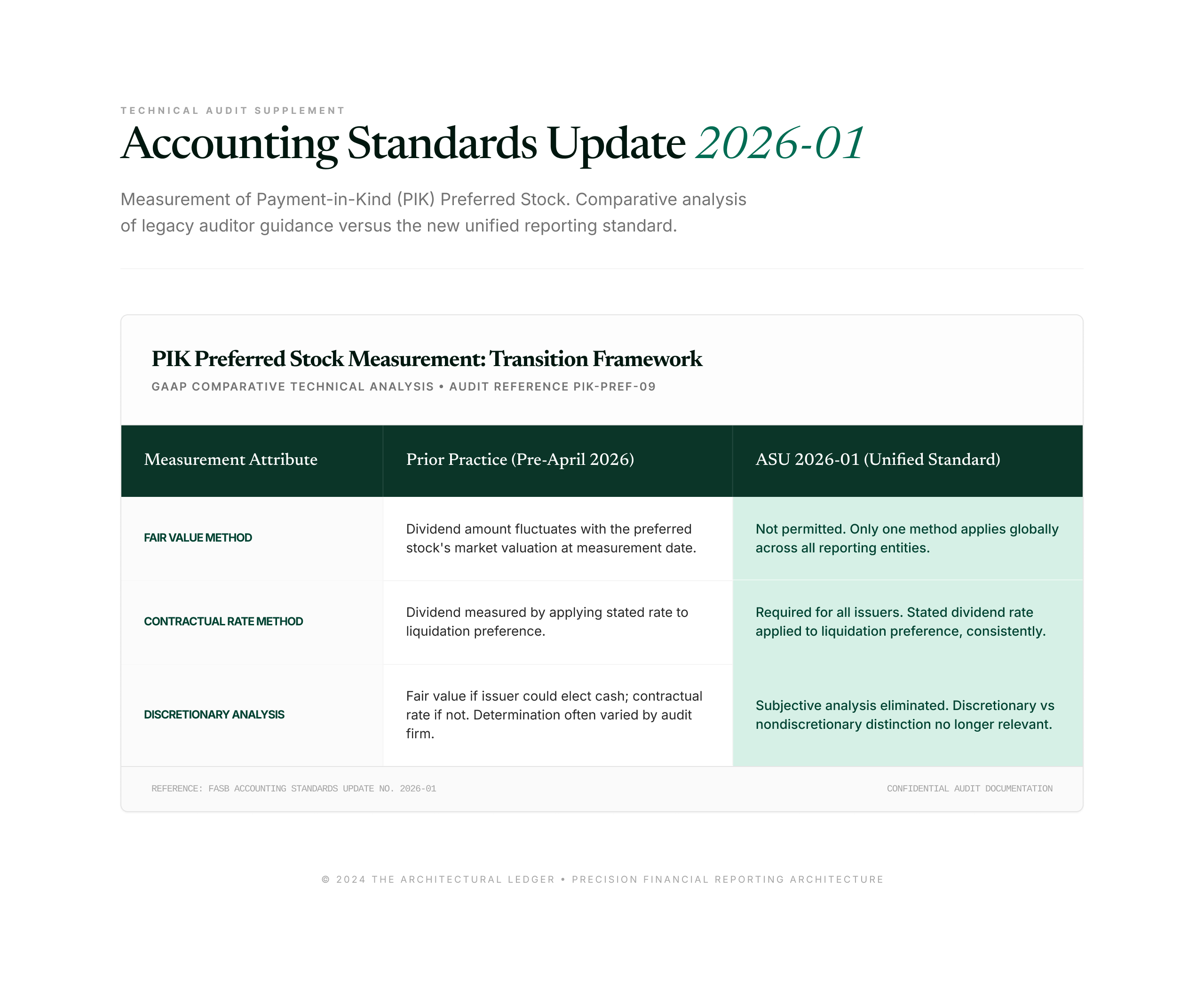

An issuer must measure paid-in-kind dividends on equity-classified preferred stock by applying the dividend rate stated in the preferred stock agreement to the stock's liquidation preference. That is the entire rule. Here is what that means in numbers. Take a company with one million shares of convertible preferred outstanding. Liquidation preference is $10 per share, so $10 million total. The agreement states a 6% annual PIK dividend rate, paid quarterly. At quarter end, the company recognizes a PIK dividend of $150,000, calculated as $10 million times 1.5%. That $150,000 reduces income available to common shareholders for EPS purposes, and it increases the carrying amount of the preferred on the balance sheet. The number is the same regardless of whether the preferred is currently trading at $8 or $12 in a recent third-party valuation.

Before ASU 2026-01, that last point was the source of the entire problem. Some issuers measured at fair value, which meant the dividend amount fluctuated with the underlying preferred's market valuation. Others measured at the contractual rate against liquidation preference. A third group split the answer based on whether the issuer had discretion to pay in cash instead of stock. After ASU 2026-01, only one answer remains.

Why Did FASB Need to Issue New Guidance on PIK Preferred Dividends?

Until April 2026, U.S. GAAP had no authoritative guidance on initial measurement of PIK dividends on equity-classified preferred stock. The vacuum was filled by the Big 4 firms' interpretive literature, and the four firms did not agree.

PwC's Viewpoint guide at FG 7.7 split the answer based on issuer discretion. If the issuer could elect cash instead of stock, the PIK dividend was measured at fair value. If not, the contractual rate applied. Deloitte's Roadmap on Distinguishing Liabilities From Equity prescribed fair value at a commitment date that itself depended on the discretion analysis. EY's Financial Reporting Developments on debt and equity financings allowed an accounting policy election between fair value and contractual rate. KPMG's handbook generally tracked the discretionary versus nondiscretionary split.

The practical consequence was the gap that opened this article. Two companies could write economically identical preferred stock agreements, hire different audit firms, and report materially different EPS to investors. As FASB Chair Richard Jones said in the issuance announcement, the new rule "will enhance the comparability of financial information reported among companies that issue PIK dividends on equity-classified preferred stock." That sentence is doing more work than it looks.

What Changes in Your EPS Calculation and Filing Under ASU 2026-01?

The EPS denominator math is unchanged. The numerator may not be. PIK dividends reduce net income in arriving at income available to common shareholders, the figure that drives basic and diluted EPS. KPMG's Defining Issues alert made the consequence explicit: the measurement change "may affect earnings per share calculations to the extent it alters income available to common shareholders." If your company previously measured PIK dividends at fair value, and your preferred's fair value diverges from its liquidation preference, your EPS resets when you adopt. Whether that reset is material or trivial depends entirely on the size of the gap, which most teams have not yet quantified.

The discretionary versus nondiscretionary analysis disappears entirely. Under prior practice, your technical accounting team had to evaluate whether the issuer or holder had any election to pay in cash versus stock, and whether contingent rights to elect cash made the dividend discretionary in periods when no cash payment was actually available. Deloitte's Heads Up on the new ASU confirmed: "Under the ASU, no such distinction is necessary since both are treated in the same manner." That is one judgment call permanently retired from the technical accounting file.

The third change is more subtle, and it matters most for growth-stage capital structures. When preferred is issued together with warrants, or below liquidation preference for any other reason, the preferred sits on the balance sheet at a carrying value below its liquidation amount. The PIK dividend continues to accrue against the full liquidation preference, not the discounted carrying value. For preferred-with-warrants structures common in PIPE and growth equity financings, the disconnect between carrying value and dividend basis is now codified rather than negotiated case by case.

Are You in Scope for ASU 2026-01?

The "yes" list is broader than the FASB's note about PIK preferred being more common at private entities suggests.

Your company is in scope if it is a public reporting entity with equity-classified preferred outstanding that satisfies dividends through additional preferred shares, or through accretion of the original liquidation preference. Post-SPAC technology companies that raised PIPE financing carrying PIK dividend mechanics to defer cash burn during the post-merger ramp. Biotech and life sciences issuers that funded through convertible preferred rounds with cumulative accrual into liquidation preference. Energy companies that restructured out of Chapter 11 and emerged with multiple tranches of preferred securing the new capital structure. Diversified holding companies whose capital structures include convertible participating preferred, often with NAV-linked accretion mechanics INNOVATE Corp. is one public example, with its FY2025 Form 10-K disclosing Series A-3 and A-4 Convertible Participating Preferred Stock with quarterly accretion at adjustable annualized rates. And pre-IPO companies on an active S-1 timeline whose historical PIK preferred accounting needs to align with the new standard before financials lock.

The "no" list matters too, because the scope question is where most early misclassification happens. ASU 2026-01 does not apply to PIK interest on debt instruments, which sits in ASC 470 and ASC 835. It does not apply to PIK dividends on preferred classified as a liability under ASC 480. It does not apply to preferred dividends payable in shares of common stock or in equity with terms that differ from the original instrument. It does not apply to deemed dividends or to nonmonetary distributions accounted for under ASC 845.

Prospective or Modified Retrospective: How Should Your Team Choose the Transition Method?

You have one decision to make before adoption. Apply the new rule prospectively, or apply it on a modified retrospective basis to preferred outstanding as of the initial application date.

Prospective is the lighter path. New ASC 505-10-65-1 lets you apply the new measurement only to PIK dividends recognized on or after the initial application date, regardless of when the underlying preferred was issued. The disclosure burden is light too: the nature of the change in accounting principle, including an explanation of the new principle, and the method of applying it.

Modified retrospective is more involved. You recast prior reporting periods presented and book a cumulative-effect adjustment to retained earnings, or other appropriate components of equity, as of the beginning of the earliest period presented. The recast applies only to PIK dividends previously recognized on preferred stock that is still outstanding as of the initial application date. Disclosures expand accordingly: cumulative effect on retained earnings, effect on income available to common shareholders, effect on other affected line items, and per-share amounts for each restated period.

The decision turns on whether your prior measurement gap is material. If your company previously measured at fair value and the gap to stated rate against liquidation preference is meaningful, modified retrospective preserves comparability for sell-side analysts working off historical EPS. If the gap is immaterial or zero, prospective is the cheaper path. The work to make this call is the gap analysis itself, and the gap analysis has to happen either way.

There is no longer-runway carve-out for private companies. Grant Thornton's comment letter requested an additional year for non-public business entities consistent with FASB's Private Company Decision Making Framework. The Board declined.

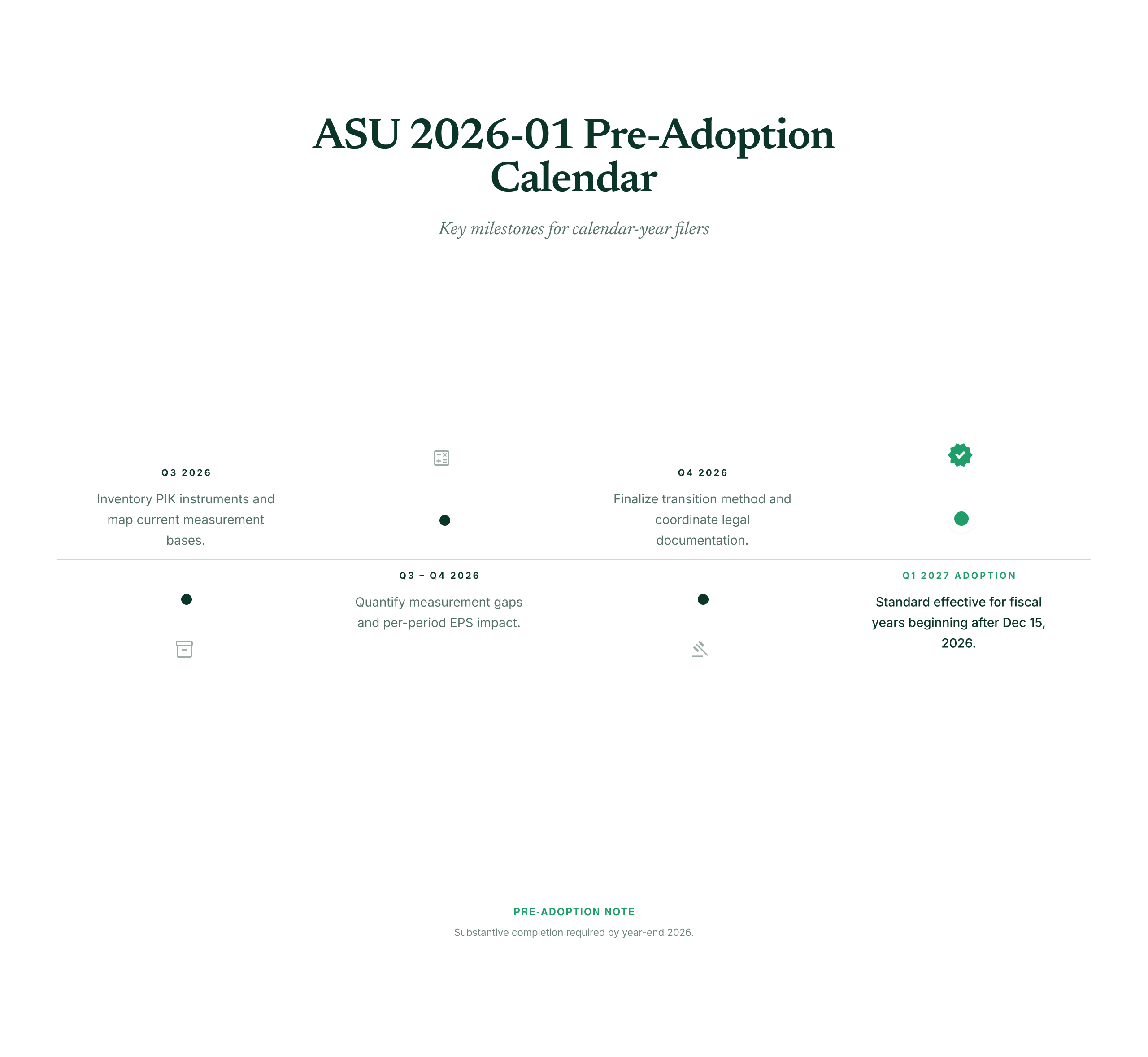

Five Steps Your Team Should Take Before the Adoption Date

Five steps, in order, with the calendar in mind.

- Inventory in-scope instruments. Pull every preferred stock instrument on the balance sheet, including any classified as temporary equity under ASC 480-10-S99-3A. Flag the ones with PIK accrual or in-kind dividend mechanics, whether explicit, optional, or contingent. Q3 2026 at the latest.

- Map current measurement basis. For each instrument, document what method has been applied historically: fair value, contractual rate against liquidation preference, hybrid based on discretion, effective yield, or other.

- Quantify the gap. Where current measurement differs from the new standard, calculate the cumulative difference for the periods that would be presented under modified retrospective, plus the per-period EPS impact. This is the single input that determines your transition decision.

- Make the transition call and document it. Choose prospective or modified retrospective. Walk the rationale through your disclosure committee with the gap analysis attached. SEC staff comment letters have historically focused on whether transition method selection is well reasoned more on that below.

- Coordinate with securities counsel. ASU 2026-01 elevates the dividend rate from accounting estimate to legal text. Drafting ambiguity in the certificate of designations is now an accounting issue. If the rate or the accretion mechanic in any of your designations is unclear, fix the documentation problem before the period of adoption.

For calendar-year filers, the work needs to be substantively complete by Q4 2026 to support a clean Q1 2027 adoption.

What SEC Comment Letter Risk Does ASU 2026-01 Create That Most Teams Will Not See Coming?

Here is where the work actually gets graded.

The transition method selection itself draws SEC comment letter scrutiny. Staff regularly question whether registrants chose the path that produces decision-useful information for investors, whether the cumulative-effect disclosure is complete, and whether the materiality assessment supporting a prospective election is properly documented. The risk pattern is predictable. A registrant adopts prospective without a quantified gap analysis on the file. The staff comment arrives asking why modified retrospective was not selected given the historical PIK recognition involved. The response cycle eats six to twelve months and lives in the comment letter trail that analysts and acquirers read for years.

We track these comment-letter patterns at Finrep, and the transition cycles that followed ASC 606 and ASC 842 told a consistent story. Registrants who walked into a comment letter with a quantified gap analysis and disclosure committee minutes attached resolved the staff cycle in one or two rounds. Registrants who treated the transition method choice as a footnote disclosure rather than a documented decision ended up in much longer cycles. ASU 2026-01 is narrow enough that a lot of teams will be tempted to skip the documentation step. The history of the last two big transitions suggests that is the wrong instinct.

This is the part where disclosure committee minutes matter more than the underlying accounting. The records need to show the gap analysis, the materiality conclusion, and the rationale for the transition path chosen. If those are not in the file when the staff letter arrives, the answer is harder to assemble than it needed to be.

What Your Team Needs to Do Before ASU 2026-01 Takes Effect

ASU 2026-01 replaces years of inconsistent practice with one rule: stated dividend rate against liquidation preference, every time. If your public company has equity-classified PIK preferred outstanding, it resets your EPS math for fiscal years beginning after December 15, 2026, and the transition method you choose will be visible to the SEC, your auditor, and the Street for years. Start with the gap analysis. The number it produces is what makes every other decision easy.