From Sanctions to Scrutiny: How OFAC Violations Create Immediate SEC Disclosure Triggers

Share

When a company discovers it has violated sanctions enforced by the Office of Foreign Assets Control (OFAC), the immediate concern is obvious: What will the penalty be? But there's a second, often more consequential question that many companies fail to ask quickly enough: Do we have to tell our investors?

The answer is frequently yes—and the timeline for that disclosure is shockingly tight. This intersection of international sanctions law and securities regulation has become one of the most treacherous areas of corporate compliance, catching even sophisticated companies off guard.

The OFAC Landscape: More Than Just Rules

OFAC, housed within the U.S. Treasury Department, enforces economic and trade sanctions against countries, individuals, entities, and foreign economic sectors. Its jurisdiction extends to all U.S. companies, citizens, and any party conducting transactions in U.S. dollars through U.S. financial institutions, regardless of where in the world the transaction occurs. Sanctions programs are dynamic, with the SDN List updated multiple times per week.

The Office of Foreign Assets Control operates as the enforcement arm of U.S. economic and trade sanctions policy. Housed within the Treasury Department, OFAC maintains multiple sanctions programs targeting countries, individuals, entities, and even specific sectors of foreign economies. According to the Treasury Department's 2024 Sanctions Review, OFAC administered over 30 active sanctions programs and imposed $1.5 billion in civil penalties in fiscal year 2023.

What makes OFAC particularly formidable is the breadth of its jurisdiction. If you're a U.S. company, U.S. citizen, or anyone conducting business in U.S. dollars through U.S. financial institutions, OFAC's rules apply to you—regardless of where in the world the transaction occurs.

The Evolving Sanctions Landscape

OFAC's sanctions programs are dynamic, not static. New entities are added to the Specially Designated Nationals (SDN) List regularly—sometimes multiple times per week. Sanctions programs expand and contract based on geopolitical events. Entire sectors can be designated overnight in response to international crises.

This fluidity creates constant compliance challenges. A business relationship that's perfectly legal today could become a sanctions violation tomorrow if your counterparty gets added to the SDN List. And in the interconnected global economy, it's not just your direct relationships that matter—OFAC can penalize you for indirect dealings with sanctioned parties, even if you didn't know they were involved.

The SEC's Materiality Standard: When Violations Must Be Disclosed

An OFAC violation becomes a mandatory SEC disclosure when it meets the materiality standard, meaning it could affect an investor's decision-making. Materiality is assessed through both quantitative factors like penalty size relative to income and qualitative factors such as evidence of systemic compliance failures, broader sanctions exposure, or potential criminal prosecution. Even small penalties can be material if they signal deeper organizational risk.

The Securities and Exchange Commission requires public companies to disclose "material" information that could affect an investor's decision-making, as established under SEC Regulation S-K and the Supreme Court's TSC Industries v. Northway standard. But what makes an OFAC violation "material"? The answer isn't always straightforward.

Courts have established that materiality isn't purely quantitative, as the SEC reaffirmed in Staff Accounting Bulletin No. 99. A $100,000 penalty might not seem material for a multi-billion dollar company, but if that violation suggests systemic compliance failures, broader exposure to sanctions risks, or potential criminal prosecution, it could easily cross the materiality threshold. As former SEC Chair Gary Gensler emphasized, "materiality is not just about the dollar amount; it's about what the information tells investors about the company's risk management and governance."

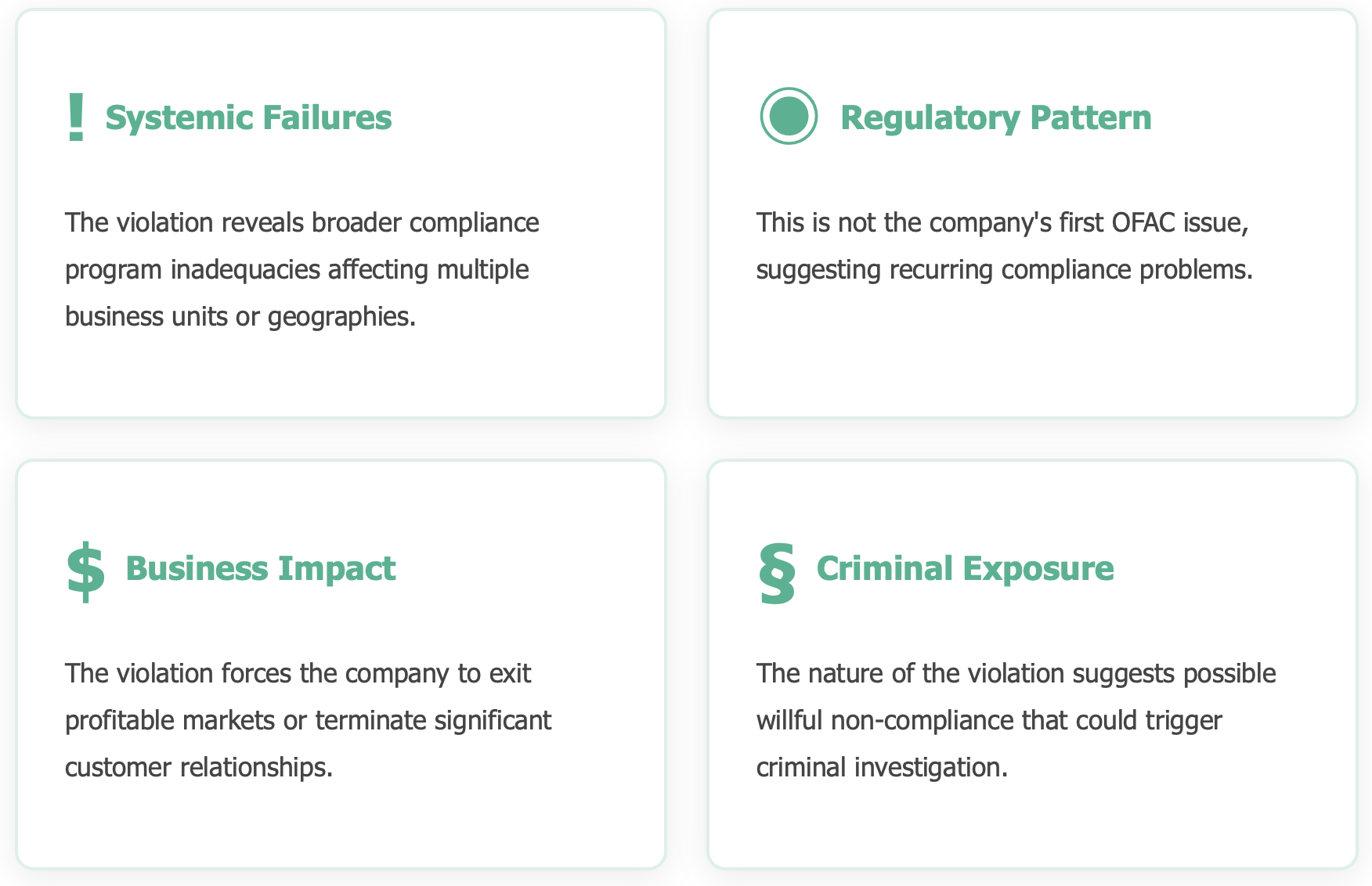

Quantitative vs. Qualitative Materiality

Companies often focus on quantitative factors: Is the penalty more than 5% of income? Will it affect our earnings per share? But qualitative factors can be equally or more important in the OFAC context. Consider these qualitative red flags that can make even small violations material:

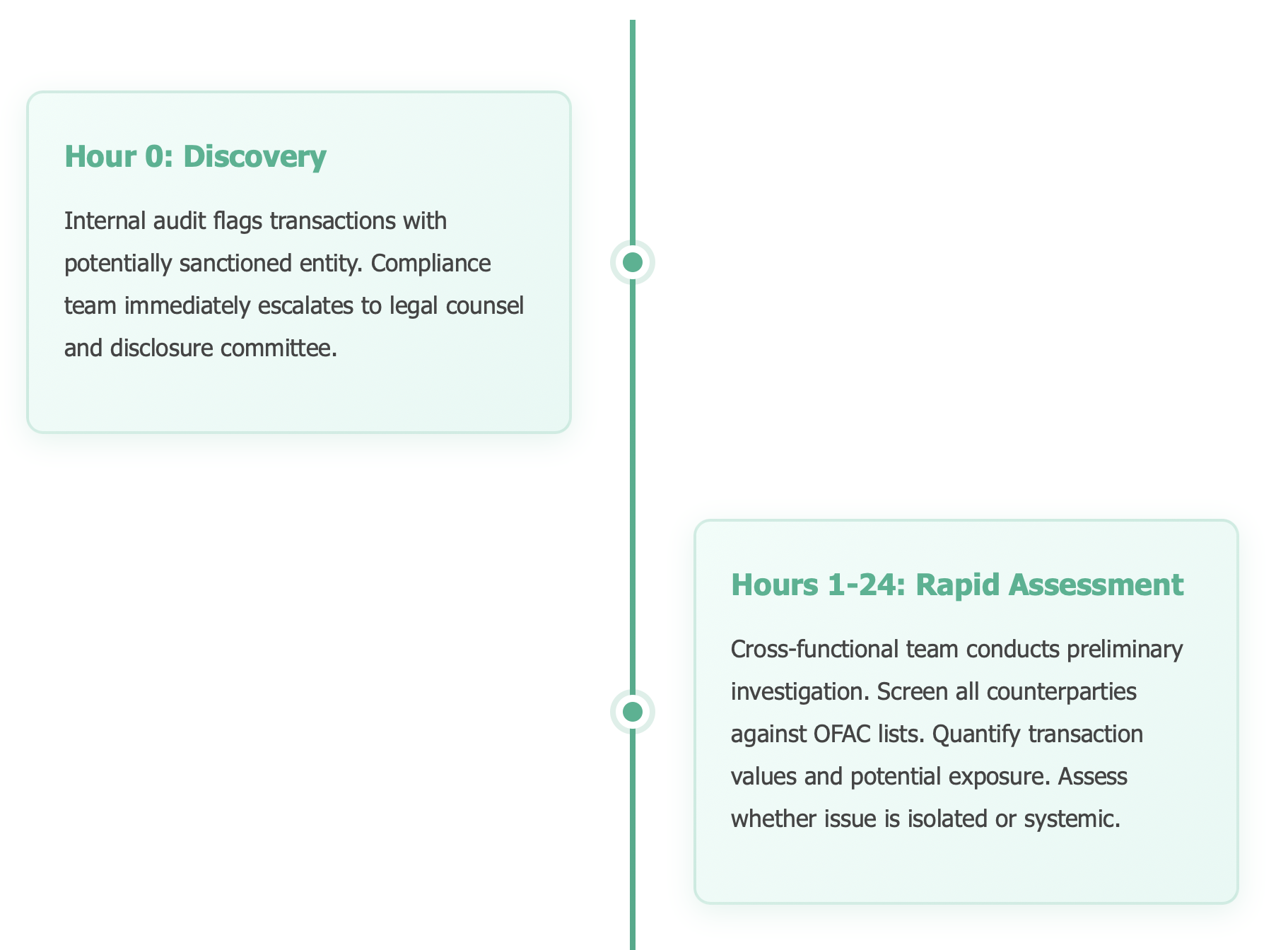

The Disclosure Timeline: Four Business Days to Crisis Management

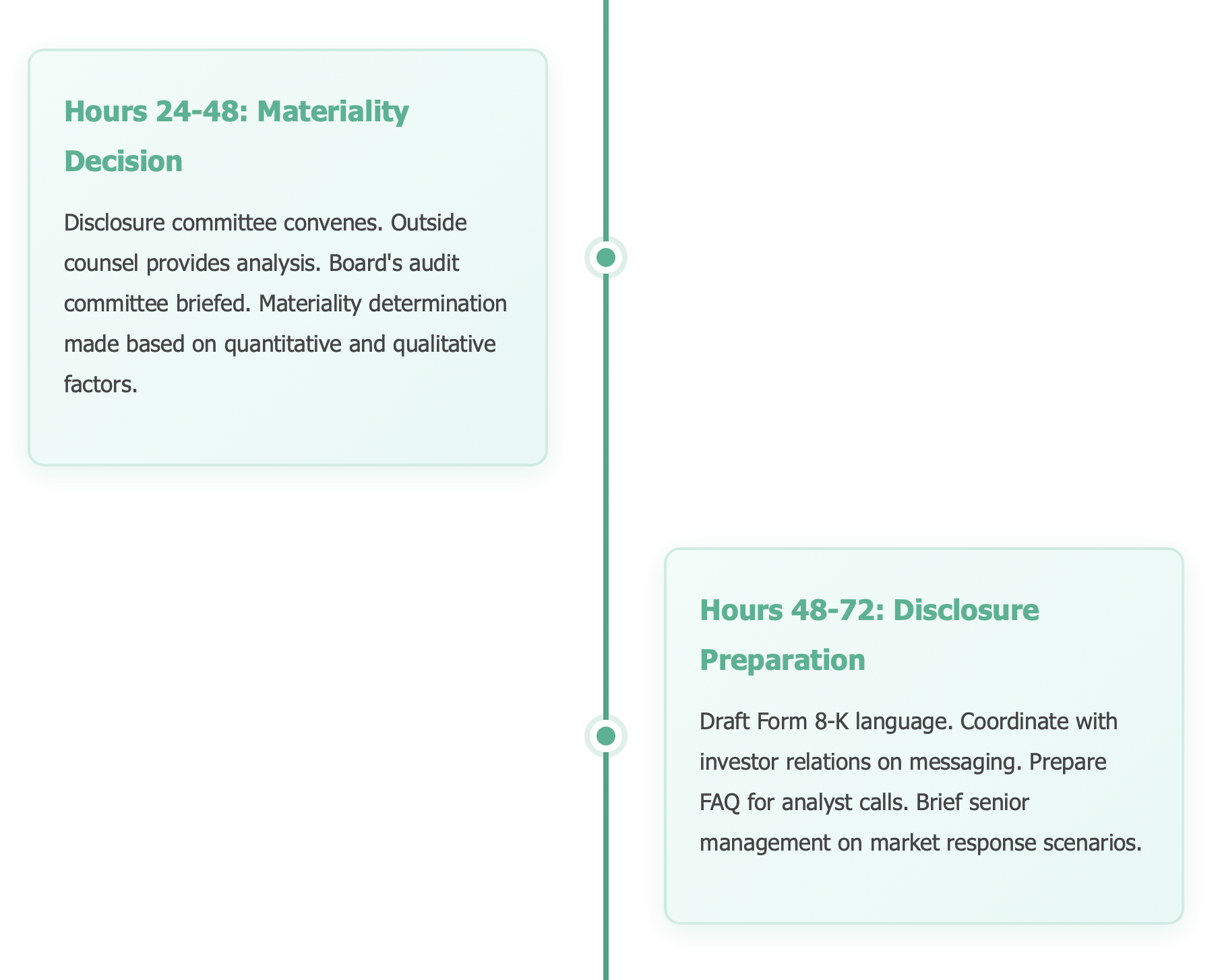

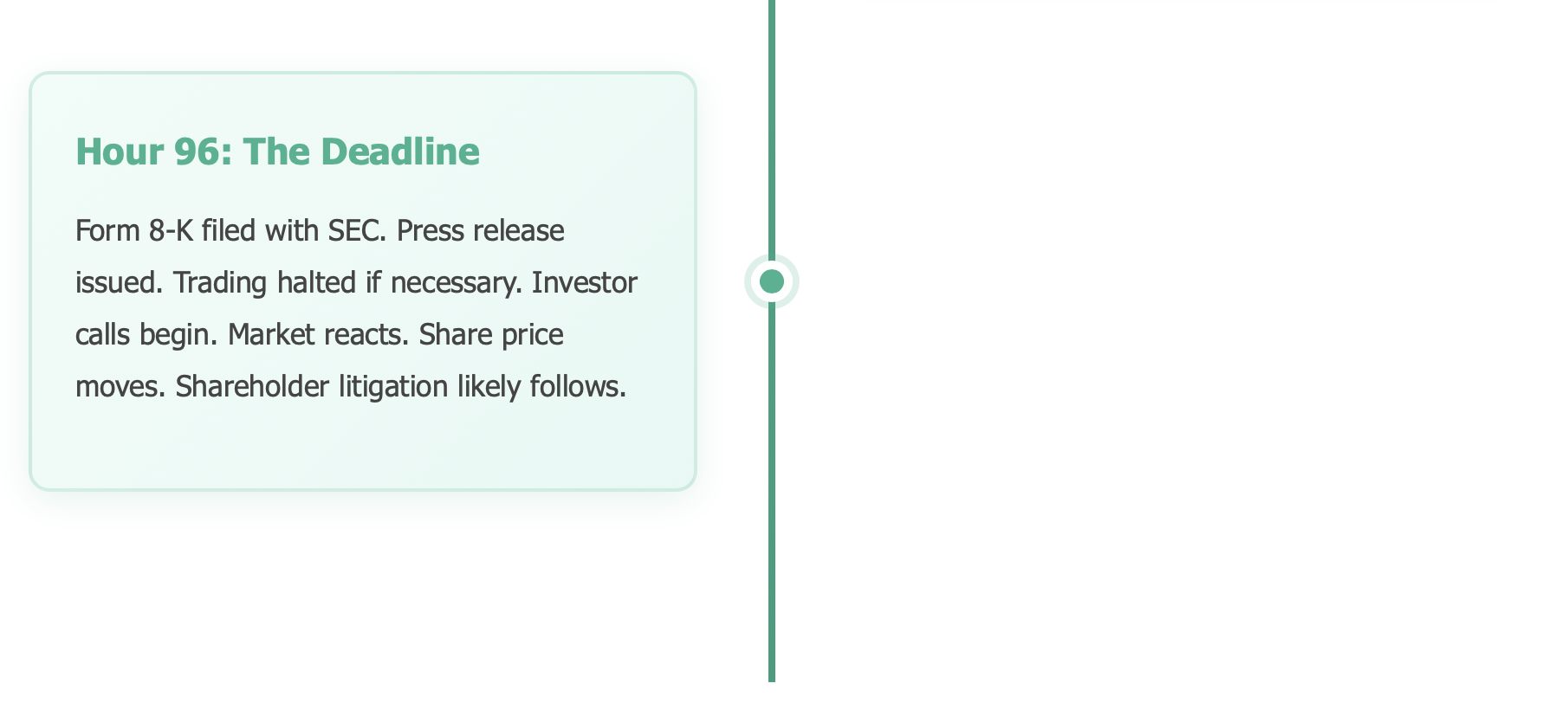

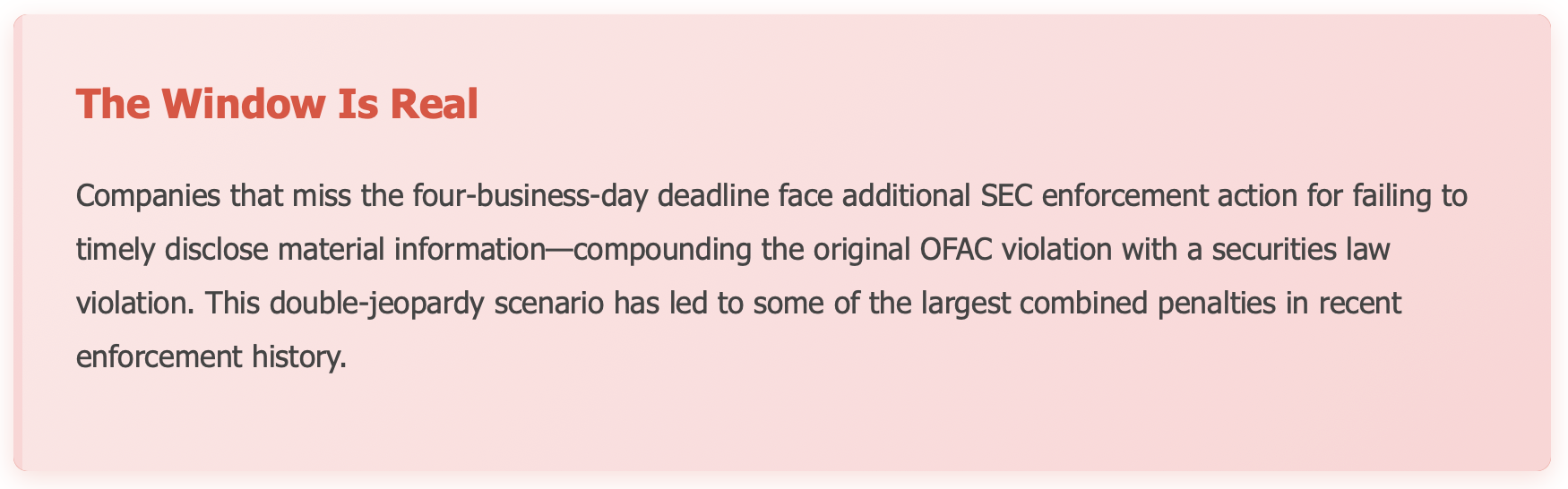

When a public company determines an OFAC violation is material, Form 8-K must be filed with the SEC within four business days. However, significant ambiguity exists around when the triggering "event" occurs — whether at discovery, completion of internal investigation, receipt of an OFAC inquiry, or proposal of penalties. This timeline uncertainty creates intense pressure for rapid internal assessment and disclosure decision-making.

Once a public company determines that an OFAC violation is material, the disclosure clock starts ticking—loudly. Form 8-K, the SEC's "current report" mechanism, requires companies to disclose material events within four business days of their occurrence.

But here's where it gets tricky: When does the "event" occur? Is it when the company discovers the violation? When it completes its internal investigation? When OFAC sends an inquiry? When penalties are proposed? The ambiguity in this timeline creates tremendous pressure and risk.

What Must Be Disclosed: Walking the Tightrope

An OFAC-related Form 8-K must typically include the nature of the sanctions violation, the financial magnitude including estimated penalties and remediation costs, the discovery timeline, remedial actions taken, cooperation status with OFAC, and the operational impact on ongoing business. Companies must balance providing sufficient investor information against creating unnecessary liability exposure for plaintiffs' litigation.

When drafting an OFAC-related Form 8-K, companies face competing pressures. Provide too little information and you risk inadequate disclosure that could trigger SEC enforcement or mislead investors. Provide too much detail and you create a roadmap for plaintiffs' lawyers, damage business relationships, and potentially compromise ongoing negotiations with OFAC.

Essential Disclosure Elements

While each situation is unique, certain elements are typically necessary for adequate disclosure of material OFAC violations:

Critical Components of OFAC Disclosure

✓ Nature of the Violation: Which sanctions program was violated? What type of prohibited activity occurred (transactions with SDNs, exports to embargoed countries, provision of services to sanctioned sectors)? Provide sufficient detail for investors to understand the conduct without creating unnecessary liability exposure.

✓ Financial Magnitude: Estimated or actual penalties from OFAC. Potential range if settlement negotiations are ongoing. Lost revenue from terminated relationships. Costs of remediation and enhanced compliance measures.

✓ Timeline and Discovery: When did the violations occur? When were they discovered? What triggered the discovery (internal audit, OFAC inquiry, third-party notification)? This timeline helps investors assess management's diligence.

✓ Remedial Actions: Steps already taken to address the violation. Changes to compliance programs, screening systems, or personnel. Third-party audits or reviews commissioned. This demonstrates management accountability.

✓ Status and Cooperation: Whether the company has self-disclosed to OFAC. Status of any investigation or settlement discussions. Company's cooperation posture. This affects both penalty exposure and investor perception.

✓ Operational Impact: Whether violations affect ongoing operations, future business plans, or strategic relationships. Any markets or customers being exited. Potential collateral consequences like banking relationship issues.

Beyond Form 8-K: The Cascade of Ongoing Disclosures

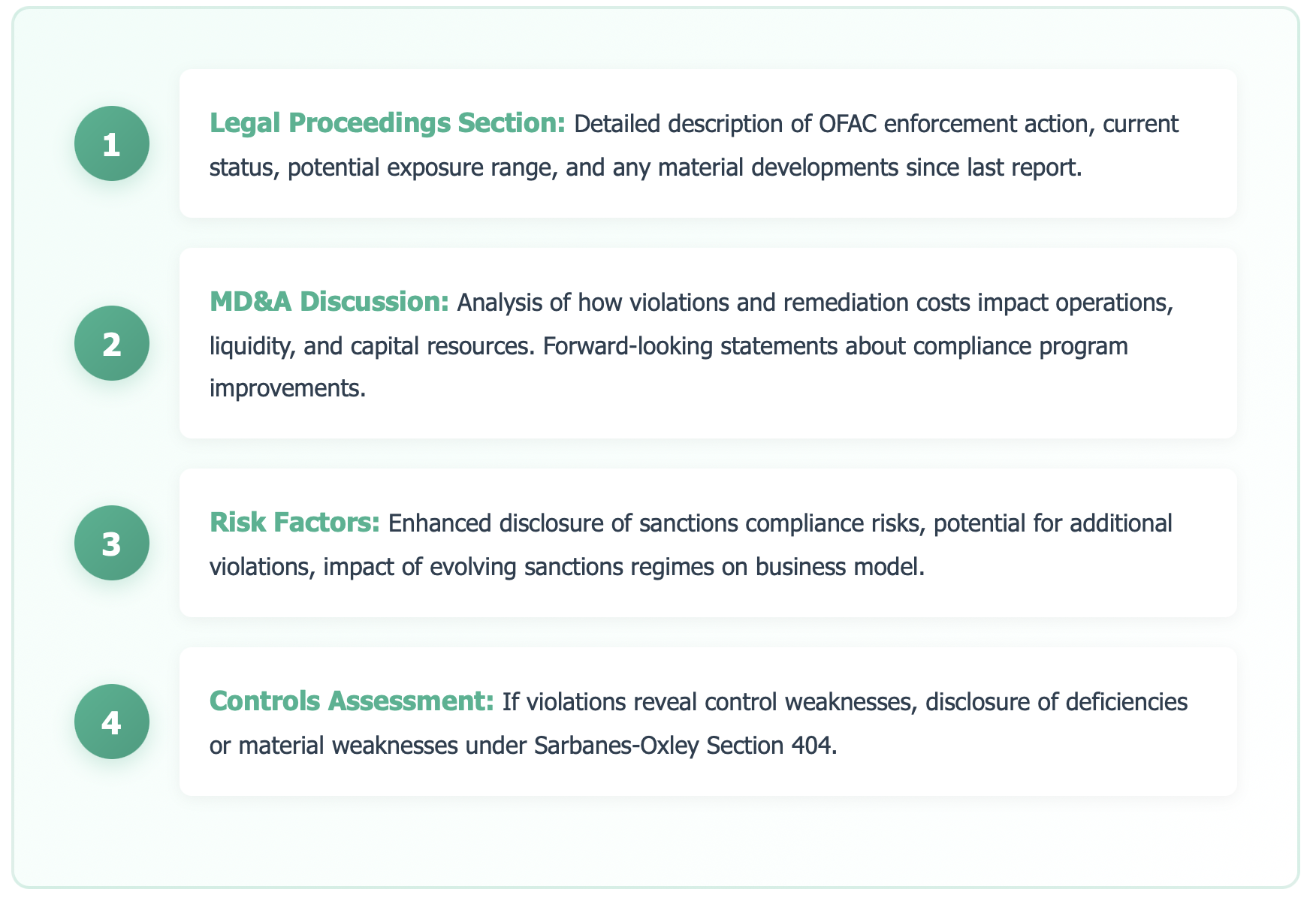

OFAC violations create ongoing disclosure obligations that extend well beyond the initial 8-K filing, persisting through quarterly 10-Q and annual 10-K reports for years. Companies must provide updates on legal proceedings, revise risk factors, and address material uncertainties in the MD&A section. The ripple effect often includes material weakness disclosures, shareholder lawsuits, and sustained market capitalization declines.

Filing a Form 8-K is just the beginning. OFAC violations create ongoing disclosure obligations that persist throughout quarterly and annual reporting cycles, sometimes for years after the initial event. According to Deloitte's 2024 annual review of SEC enforcement trends, sanctions-related disclosures remain in a company's filings for an average of 2.5 years following the initial violation disclosure.

Quarterly and Annual Report Updates

In Forms 10-Q and 10-K, companies must provide updates on material legal proceedings, including OFAC enforcement actions. The Management Discussion and Analysis (MD&A) section becomes particularly critical—companies must discuss known trends, events, and uncertainties that could materially affect financial condition or results.

Real-World Impact: The Ripple Effect

A major financial services firm disclosed OFAC violations in 2021 related to processing transactions for sanctioned entities. The initial Form 8-K was followed by updates in six consecutive quarterly reports and two annual reports. The company revised risk factors three times, disclosed two material weaknesses in internal controls, and ultimately settled with OFAC for $32 million. But the real cost? Market capitalization declined by over $800 million in the quarter following disclosure, and the company faced five separate shareholder class action lawsuits.

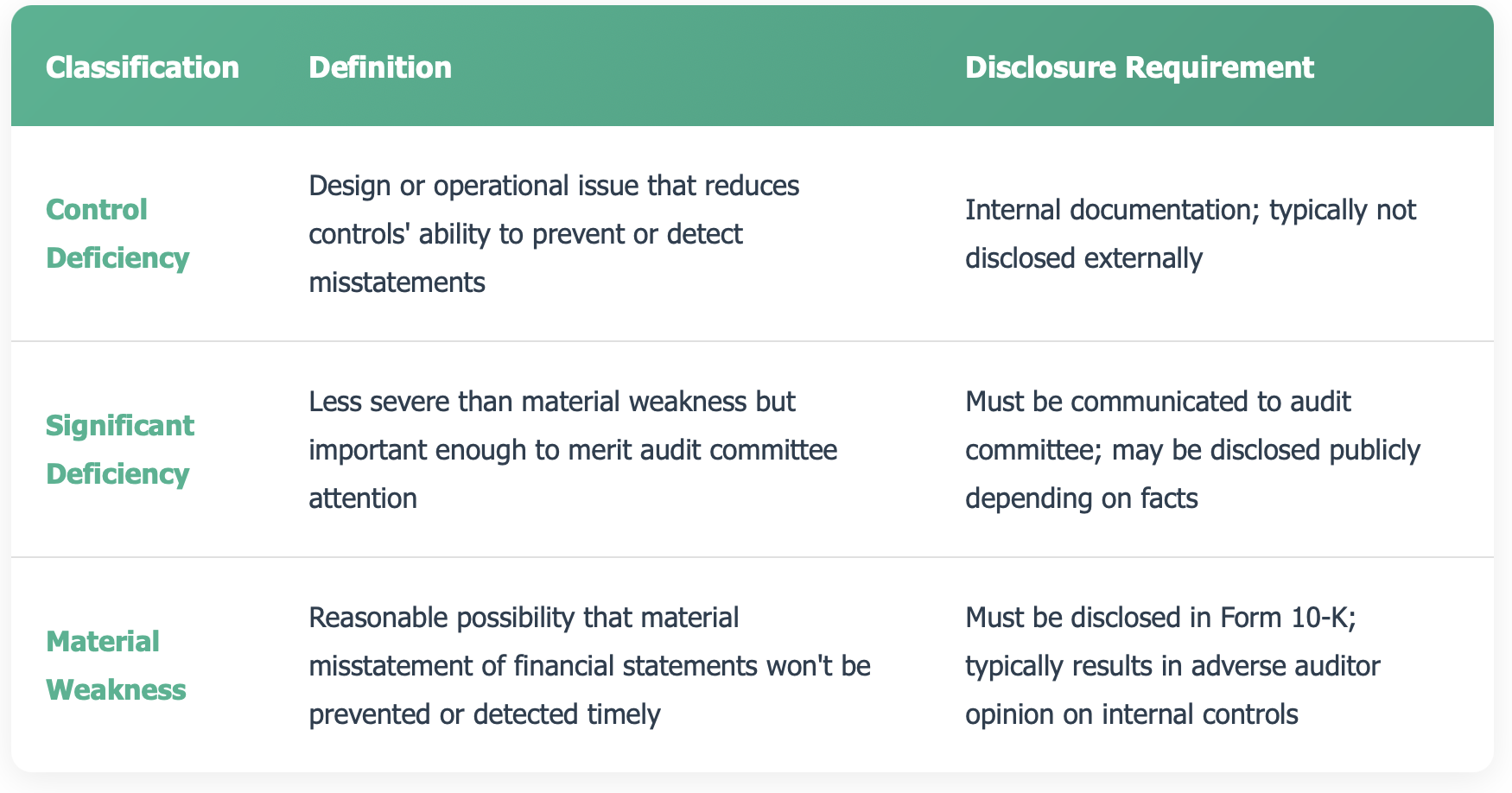

Internal Controls and the Sarbanes-Oxley Connection

OFAC violations can trigger Sarbanes-Oxley Section 404 internal control disclosures when they suggest that controls failed to prevent or detect prohibited financial transactions. If the failure rises to a material weakness, companies face consequences including potential delisting threats, loss of investor confidence, increased audit fees, stock price declines, and vulnerability to class action litigation.

OFAC violations can also trigger Sarbanes-Oxley internal control disclosures, a dimension many companies overlook. If a violation suggests that controls failed to prevent or detect prohibited transactions, management may need to disclose a material weakness. According to PCAOB inspection data, internal control deficiencies related to sanctions compliance screening have appeared with increasing frequency in inspection findings since 2022.

Under Section 404 of Sarbanes-Oxley, public companies must assess and report on the effectiveness of internal controls over financial reporting. OFAC violations that involve financial transactions can directly implicate these controls.

Control Deficiency Hierarchy

The consequences of disclosing a material weakness are severe: potential delisting threats, loss of investor confidence, increased audit fees, stock price decline, and vulnerability to class action litigation. Yet failure to disclose a material weakness when one exists creates even greater liability exposure.

The Voluntary Self-Disclosure Dilemma

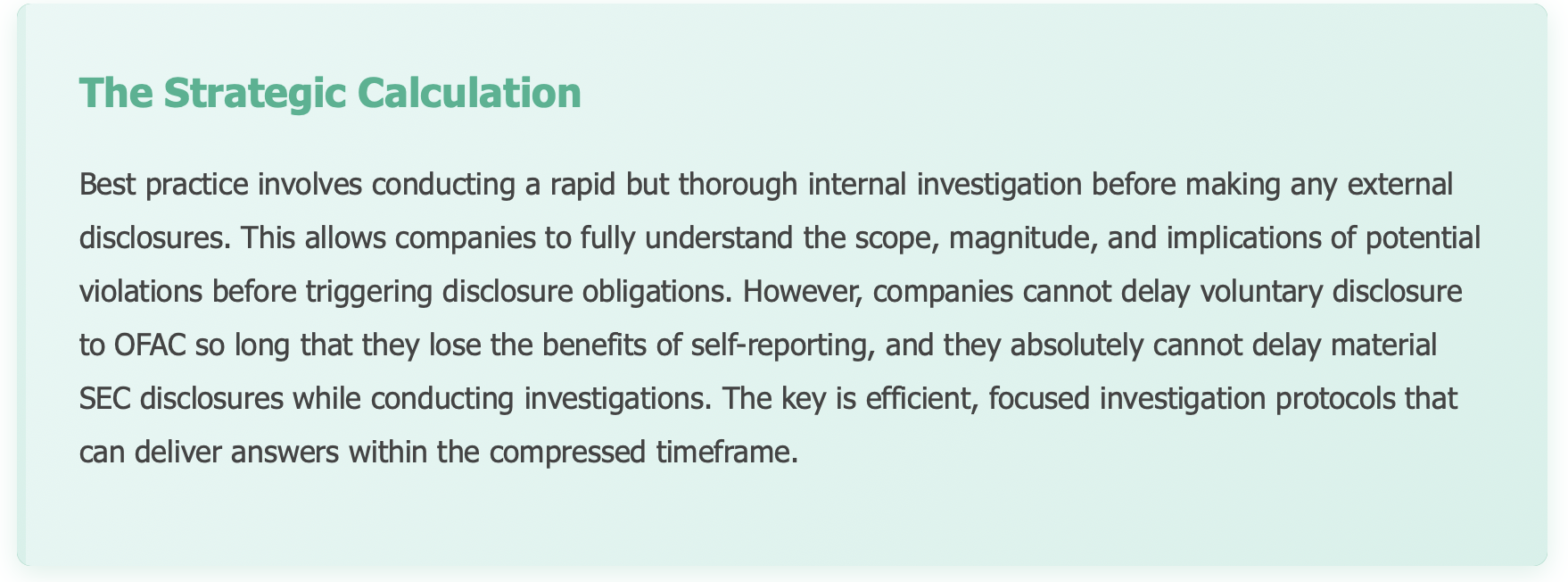

Voluntary self-disclosure to OFAC can significantly reduce penalties but creates an immediate tension with SEC obligations. Once a company acknowledges a violation to OFAC, it possesses material information that may require investor disclosure, even before OFAC formally determines penalties. Attorney-client privilege and work product protections become critical to manage, as securities filing disclosures can waive privilege and expose the company to civil litigation discovery.

OFAC strongly encourages companies to voluntarily self-disclose violations, offering the possibility of significantly reduced penalties. But voluntary disclosure to OFAC creates an immediate tension with SEC obligations.

The moment a company makes a voluntary self-disclosure to OFAC, it has acknowledged that a violation occurred. Even though OFAC hasn't yet determined the penalty or even formally confirmed the violation, the company now possesses material information that may need to be disclosed to investors.

Privilege Considerations

Attorney-client privilege and work product protection become crucial in this context. Companies must carefully structure internal investigations to maintain privilege while gathering information needed for disclosure decisions. Once information is disclosed to the SEC or in securities filings, privilege protection is often waived, potentially exposing the company to additional discovery in civil litigation.

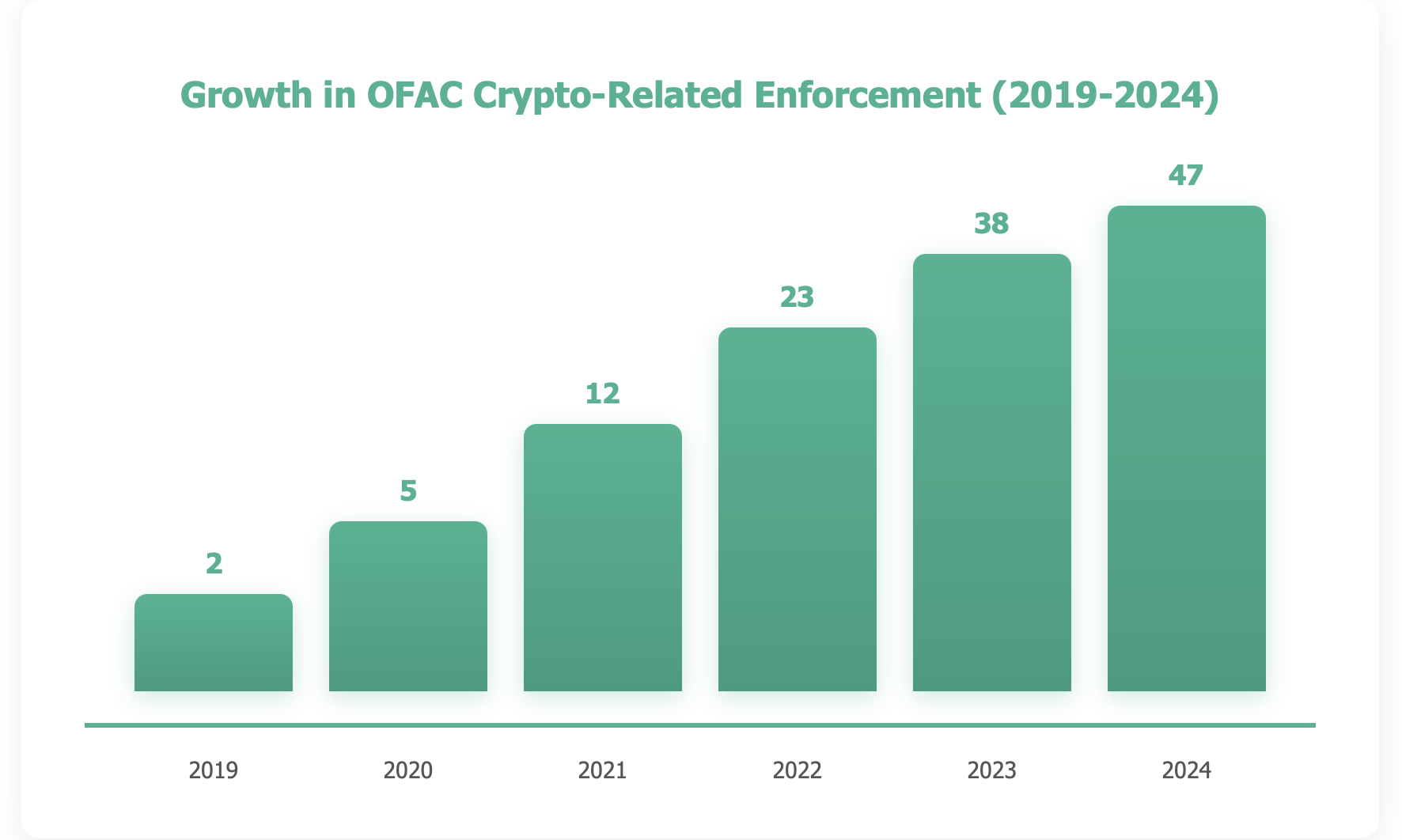

Emerging Challenges in the Digital Age

Cryptocurrency and AI-driven trading are creating new OFAC compliance complexities. OFAC now maintains sanctioned digital currency addresses, yet screening pseudonymous blockchain transactions remains technically challenging. Similarly, when AI systems inadvertently process transactions with sanctioned entities, questions of accountability and control failure disclosure arise, with regulatory frameworks still evolving while disclosure obligations remain immediate.

The intersection of OFAC compliance and SEC disclosure is becoming more complex as new technologies and business models emerge.

Cryptocurrency and Digital Assets

The rise of cryptocurrency has created new OFAC compliance challenges. OFAC now maintains a list of sanctioned digital currency addresses associated with ransomware attacks, darknet markets, and sanctioned jurisdictions. According to Chainalysis research, sanctioned entities received over $14 billion in cryptocurrency transactions in 2023, underscoring the scale of the compliance challenge. For public companies operating crypto exchanges or processing digital asset transactions, the compliance implications are profound.

How do you screen a blockchain transaction when participants use pseudonymous addresses? What disclosure obligations arise when your platform inadvertently processes transactions involving sanctioned addresses? The regulatory framework is still evolving, but the disclosure obligations are immediate.

AI and Automated Trading

As companies increasingly deploy AI for trading, customer onboarding, and transaction processing, new questions arise about accountability for sanctions violations. If an AI system processes a transaction with a sanctioned entity, who is responsible? How do you disclose control failures in algorithmic systems? These questions are becoming pressing as AI adoption accelerates.

Best Practices: Building a Robust Framework

An effective OFAC-SEC compliance framework integrates sanctions compliance with financial reporting, internal audit, and investor relations through four pillars: cross-functional compliance architecture, enhanced AI-powered screening and monitoring systems, pre-established rapid response protocols with specialized counsel on retainer, and a disclosure committee with clear authority over sanctions-related materiality assessments and timing decisions.

Leading companies have developed integrated approaches to managing the OFAC-SEC interface. A 2024 EY Global Sanctions Compliance Survey found that 78% of Fortune 500 companies now have cross-functional sanctions compliance teams that integrate legal, finance, and disclosure functions. These frameworks share several common elements:

1. Integrated Compliance Architecture

OFAC compliance cannot be siloed in the legal or trade compliance department. It must be integrated with financial reporting, internal audit, investor relations, and disclosure committees. When potential violations are identified, cross-functional teams should immediately assess both OFAC implications and SEC disclosure obligations in parallel.

2. Enhanced Screening and Monitoring

Prevention is always cheaper than remediation. Robust screening of customers, vendors, and transactions against sanctions lists, coupled with ongoing monitoring, is essential. Modern AI-powered screening tools can identify potential matches even when names are transliterated differently or entities use multiple aliases.

Core Components of Effective OFAC Compliance

✓ Risk-Based Assessment: Regular evaluation of sanctions exposure based on products, services, geographic footprint, customer base, and supply chain relationships. Risk profiles should be updated as business evolves.

✓ Automated Screening Systems: Real-time screening of transactions, customers, and vendors against comprehensive sanctions lists. System must handle name variations, transliterations, and aliases effectively.

✓ Escalation Protocols: Clear procedures for reporting potential violations to senior management, disclosure committees, and outside counsel. Pre-established thresholds for escalation based on transaction value and violation type.

✓ Training Programs: Regular, role-specific training for employees who interact with international transactions. Training should cover red flags, escalation procedures, and real-world case studies.

✓ Third-Party Due Diligence: Enhanced vetting of distributors, agents, and intermediaries, particularly in high-risk jurisdictions. Ongoing monitoring of third-party relationships for sanctions exposure.

✓ Independent Auditing: Regular independent review of compliance program effectiveness and transaction monitoring. Audit findings should be reported to audit committee and addressed promptly.

3. Rapid Response Capabilities

When potential violations are identified, speed is essential. Companies need pre-established protocols that allow them to quickly assemble the right team, conduct focused investigations, and make disclosure decisions within compressed timeframes.

This requires having outside counsel on retainer who specialize in both sanctions and securities law, maintaining relationships with forensic accountants and investigators, and ensuring disclosure committee members can be mobilized on short notice—including after hours and on weekends.

4. Disclosure Committee Excellence

The disclosure committee becomes the critical decision-making body when OFAC issues arise. These committees should include representatives from legal, compliance, finance, investor relations, and business operations. They need clear charters that specifically address sanctions-related disclosures and the authority to make rapid decisions about materiality and timing.

Practical Recommendations for Corporate Counsel

Corporate counsel should integrate sanctions compliance into disclosure frameworks proactively, establish clear materiality thresholds before violations occur, document investigation and decision-making processes meticulously, invest in prevention through screening technology, conduct regular crisis simulations, maintain relationships with specialized sanctions and securities counsel, and default to disclosure when materiality is uncertain.

Based on years of enforcement actions and regulatory guidance, and consistent with OFAC's Economic Sanctions Enforcement Guidelines, here are concrete recommendations for companies navigating this complex landscape:

1. Integrate sanctions compliance into your disclosure framework from day one.

Build sanctions considerations into your disclosure committee charter and materiality assessment frameworks before a violation occurs, rather than determining the OFAC-SEC intersection during a crisis.

2. Establish clear materiality thresholds in advance.

Develop quantitative and qualitative criteria for assessing whether OFAC violations are material. Having pre-established frameworks enables faster, more consistent decision-making during crises.

3. Document your investigation and decision-making process meticulously.

Create contemporaneous records of how you discovered violations, investigated them, assessed materiality, and reached disclosure decisions. These records are crucial for defending against both regulatory enforcement and securities litigation.

4. Invest in prevention, not just detection.

Sophisticated screening and monitoring systems are far less expensive than OFAC penalties, SEC enforcement actions, shareholder lawsuits, and reputational damage combined. View compliance technology as critical infrastructure.

5. Conduct crisis simulations regularly.

Run tabletop exercises where your team works through hypothetical OFAC violations and resulting disclosure decisions. These exercises identify gaps in protocols and build organizational muscle memory.

6. Maintain specialized counsel relationships proactively.

Establish relationships with law firms that have deep expertise in both sanctions and securities law before problems arise. The middle of a crisis is the wrong time to be searching for counsel.

7. When in doubt, disclose.

The consequences of inadequate or delayed disclosure consistently exceed the costs of proactive transparency. If you're wrestling with whether something is material, that struggle itself suggests materiality.

8. Focus on your remediation narrative.

When you must disclose violations, emphasize concrete steps you're taking to prevent recurrence. Investors and regulators respond far more favorably to companies that demonstrate accountability and continuous improvement.