If you're a CFO, audit committee member, or financial controller preparing for your annual 10-K or 20-F filing, the SEC's increasing scrutiny of auditors and financial gatekeepers is reshaping how audits are conducted and what finance teams should expect.

The Securities and Exchange Commission has intensified its scrutiny of auditors, audit firms, and other financial gatekeepers over the past few years. This heightened oversight is changing how audits are planned, executed, and documented across all public company engagements.

The SEC intensified its scrutiny of auditors and financial gatekeepers following a series of high-profile audit failures, accounting scandals involving companies like Luckin Coffee, and rising complexity in financial instruments such as SPACs and cryptocurrency valuations. This regulatory pressure directly affects how audit firms approach their engagements, increasing demands on corporate finance teams during audit preparation.

The SEC's renewed focus on gatekeepers did not emerge in a vacuum. A combination of accounting scandals, high-profile audit failures, and the increasing complexity of financial instruments has pushed regulators to take a harder line. From the Luckin Coffee fraud to concerns about SPAC audits and cryptocurrency valuations, regulators have responded by holding auditors to stricter standards. The SEC's Division of Enforcement reported 784 total enforcement actions in fiscal year 2023, with financial fraud and issuer disclosure cases representing a significant portion (SEC, 2023).

Former SEC Chair Gary Gensler was particularly vocal about strengthening the "three lines of defense" in corporate governance, stating, "Gatekeepers serve an important role in our capital markets, and we will hold them accountable when they fail in their obligations." The PCAOB's annual inspection reports have also identified increasing deficiency rates across audit firms, further justifying the heightened scrutiny (PCAOB, 2023).

💡 What Does This Mean for You?

Your auditors are under increased pressure. They face greater scrutiny on methodology, documentation standards, and professional skepticism. That pressure flows directly to your finance team and your audit preparation process.

The New Audit Landscape: What's Changed

Three major shifts define the current audit environment: heightened professional skepticism where auditors question items that previously passed without challenge, significantly more detailed documentation of auditor decision-making processes, and deployment of data analytics tools that test entire transaction populations rather than samples, flagging anomalies that traditional methods would miss.

Today's auditors are applying what the PCAOB calls "enhanced skepticism" — questioning items that may have passed without challenge in prior years. Management representations are being tested more rigorously, and historical precedents carry less weight. PCAOB Chair Erica Williams has stated, "Professional skepticism is not optional — it is the foundation of audit quality, and we expect auditors to apply it consistently."

2. Documentation, Documentation, Documentation

Auditors are now documenting their thought processes, decision trees, and alternative considerations in greater detail — because they know the SEC or PCAOB will review their work papers. According to the Center for Audit Quality (CAQ), audit documentation requirements have expanded significantly in response to PCAOB inspection findings (CAQ, 2024). For finance teams, this means more information requests, more follow-up questions, and more time spent explaining the rationale behind accounting judgments.

3. Technology and Data Analytics

Your auditors are deploying sophisticated data analytics tools to test entire populations of transactions rather than samples. This is generally good news for audit quality, but it means anomalies and outliers that might have slipped through traditional sampling methods are now getting flagged for investigation.

Red Flags That Will Trigger Extra Scrutiny

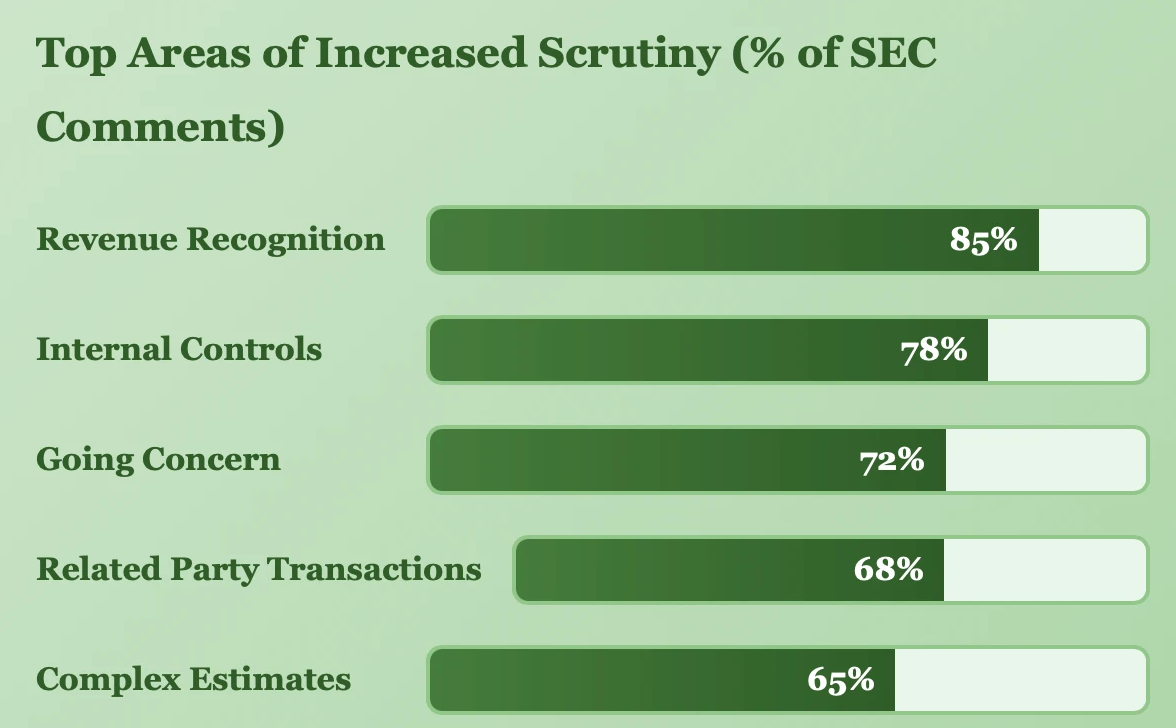

Areas most likely to draw heightened audit scrutiny include late adjustments to material financial statement items, complex fourth-quarter transactions, significant management estimates lacking robust documentation, related-party transactions without clear business purpose, revenue recognition deviations from industry norms, and unexplained changes in accounting policies or estimates.

Be especially mindful of these areas that are likely to draw heightened attention:

- Late adjustments to financial statements, especially in material areas

- Complex or unusual transactions in the fourth quarter

- Significant management estimates without robust supporting documentation

- Related party transactions that lack clear business purpose

- Revenue recognition patterns that deviate from industry norms

- Changes in accounting policies or estimates without clear justification

How to Prepare for Your Next Audit in This New Environment

Finance teams should start audit preparation well before year-end, strengthen internal controls over financial reporting, document significant accounting judgments contemporaneously, pre-clear complex transactions with auditors, invest in technical accounting expertise, and schedule regular auditor touchpoints throughout the year rather than only during the formal audit period.

Proactive Steps for Finance Teams

- Start earlier: The days of cramming audit prep into the final weeks are over. Begin documentation and analysis well before year-end.

- **Strengthen internal controls: **The SEC is heavily focused on ICFR (Internal Control over Financial Reporting). Any material weaknesses will draw extra scrutiny.

- Document your judgments: For any significant accounting judgment or estimate, create contemporaneous documentation of your analysis, alternatives considered, and rationale.

- Pre-clear complex transactions: Don't surprise your auditors with novel structures or unusual transactions. Involve them early in the accounting assessment.

- Invest in your technical accounting team: Having deep expertise in-house for complex areas (revenue recognition, leases, derivatives) pays dividends.

- Enhance communication: Schedule regular touchpoints with your auditors throughout the year, not just during the audit period.

The Impact on Audit Committees

Audit committees face increased pressure to exercise independent oversight of both management and auditors. Effective committees are allocating more meeting time to review significant accounting judgments before finalization, conducting more frequent private sessions with auditors, requesting additional reporting on internal controls quality, and ensuring adequate funding for both internal and external audit functions.

Audit committees are finding themselves in a delicate position. On one hand, they need to support management and maintain efficient operations. On the other, they're expected to exercise independent oversight and be prepared to challenge both management and auditors when necessary.

Smart audit committees are adapting by allocating more meeting time to understand significant accounting judgments before they're finalized, not after. They're also engaging in private sessions with auditors more frequently to understand areas of audit emphasis and concern. Additionally, they're requesting additional reporting on the quality of internal controls and the company's financial reporting process, and they're ensuring adequate resources for both internal audit functions and external audit fees—underfunding audits creates risks that ultimately blow back on the committee.

Looking Ahead: The Long-Term Implications

Companies that adapt to heightened audit scrutiny often experience improved financial reporting processes, stronger internal controls, and better documentation practices. Research indicates that companies with clean audit histories and robust controls trade at premium valuations compared to peers with audit issues or control weaknesses, making compliance investment a long-term value driver.

While the current environment requires additional investment, companies that adapt to this higher-scrutiny environment often find that their financial reporting processes improve significantly. Better documentation, stronger controls, and more rigorous analysis are good business practices that can prevent costly errors and strengthen investor confidence.

The market also rewards companies that demonstrate audit quality. Research published in the Harvard Law School Forum on Corporate Governance indicates that companies with clean audit histories and strong internal controls trade at premium valuations compared to peers with audit issues or control weaknesses. According to a Deloitte CFO Signals survey, 85% of CFOs view strong internal controls as a competitive advantage rather than merely a compliance requirement (Deloitte, 2024).

Key Takeaways

The era of casual audit preparation is definitively over. The SEC's heightened scrutiny of auditors has created a ripple effect that touches every public company's financial reporting process. But rather than viewing this as purely a compliance burden, forward-thinking finance leaders are using it as an opportunity to strengthen their financial infrastructure and enhance the reliability of their reporting.

Your next 10-K or 20-F audit will likely be more thorough, more time-consuming, and more challenging than previous years. But with proper preparation, transparent communication with your auditors, and a commitment to robust financial reporting practices, you can navigate this new landscape successfully.

Remember: in the world of financial reporting, surprises are never welcome. Start your audit preparation early, document thoroughly, and when in doubt, seek guidance before the fact, not after.