SEC Semiannual Reporting Proposal 2026: The Complete Form 10-S Decision Guide

On May 5, 2026, the SEC formally proposed Release No. 33-11414, giving every public company currently required to file Form 10-Q the option to switch to one semiannual report on new Form 10-S. The rule is not final, the comment period closes July 6, 2026, and quarterly reporting remains the default. But the decision your disclosure team makes now, before adoption, will shape your IR strategy, insider trading policies, and debt covenant review for years.

This guide goes beyond what the rule says. It explains how to decide whether to elect, what the operational traps are, and what you should be doing before the ink is dry.

Key takeaway: The SEC semiannual reporting proposal reduces the number of periodic filings from four to two per year. It does not reduce the substantive disclosure burden, and for many companies, the hidden costs of electing Form 10-S will outweigh the compliance savings.

What the SEC Is Actually Proposing

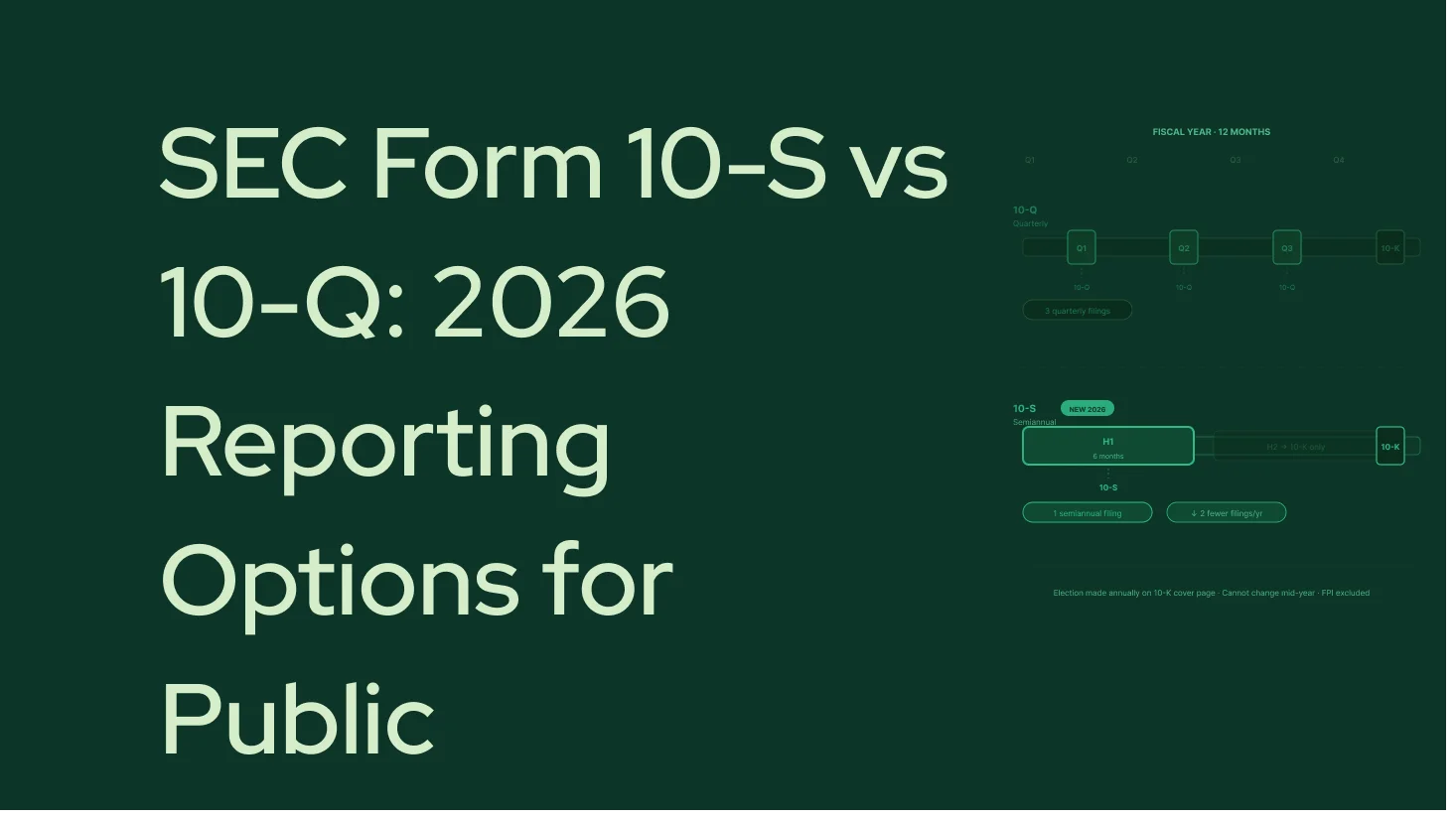

The proposal amends Exchange Act Rules 13a-13 and 15d-13 to permit any domestic reporting company to elect to file one semiannual report on new Form 10-S plus one annual Form 10-K, instead of three Form 10-Qs plus one Form 10-K. The quarterly framework has been in place since 1970, semiannual reporting preceded it from 1955 to 1970, and this is the first formal proposal to revisit it in over five decades.

Chairman Atkins framed the proposal explicitly as part of his "Make IPOs Great Again" agenda: "Today's proposal is just the first step of the larger, comprehensive effort to review and reshape the current SEC rules governing public companies."

Key mechanics at a glance:

- Eligibility: All domestic reporting companies currently required to file Form 10-Q. No market cap, revenue, or filer-status filter.

- Election mechanism: A check box on the cover page of Form 10-K for existing reporters. New registrants elect via the cover page of Forms S-1, S-3, S-4, S-11, or Form 10.

- Annual lock-in: The election applies to the entire following fiscal year and cannot be changed mid-year (except to correct an inadvertent error by filing a Form 10-K/A no later than the due date of the first Form 10-Q that would otherwise be required).

- Re-election required: Leaving the box unchecked on the next Form 10-K defaults back to quarterly reporting.

- Comment deadline: July 6, 2026. Earliest realistic adoption: first half of 2027. Calendar-year companies could first elect semiannual reporting for fiscal year 2028.

- FPIs: Not affected by the proposal if filing on FPI forms. FPIs that voluntarily file on domestic forms may also elect semiannual reporting.

The proposal also introduces two new defined terms, "quarterly filer" and "semiannual filer," into Exchange Act Rule 12b-2 and Securities Act Rule 405, creating a formal regulatory taxonomy for the two regimes.

Form 10-S vs. Form 10-Q: What Actually Changes

The short answer: the period covered changes. The disclosure depth does not.

| Feature | Form 10-Q | Form 10-S |

|---|---|---|

| Period covered | Fiscal quarter (3 months) | First six months of fiscal year |

| Financial statements required | Quarter-to-date AND year-to-date | Year-to-date (semiannual) only |

| Auditor involvement | Review (PCAOB AS 4105) | Review (PCAOB AS 4105) |

| MD&A | Required | Required |

| Inline XBRL tagging | Required | Required |

| CEO/CFO certifications | Required | Required |

| Disclosure controls and procedures | Required | Required |

| ICFR change disclosures | Required | Required |

| Filing deadline (accelerated/large accelerated filers) | 40 days after quarter end | 40 days after semiannual period end |

| Filing deadline (non-accelerated filers) | 45 days after quarter end | 45 days after semiannual period end |

| Voluntary quarterly data within the filing | N/A | Permitted (subject to auditor review if included in financial statements) |

| Annual filings per year | 4 (3 x 10-Q + 1 x 10-K) | 2 (1 x 10-S + 1 x 10-K) |

Sources: PwC In Brief; Sullivan & Cromwell / Harvard Law Forum

One important difference: Form 10-Q requires both quarter-to-date and year-to-date financial statement periods. Form 10-S requires only the year-to-date (six-month) presentation. Voluntary quarterly data may be included inside Form 10-S, but if it appears within the financial statements, it becomes subject to auditor review.

Key takeaway: Practitioners at Gladstone Place Partners put it plainly: "Semiannual filing does not mean semiannual disclosure or less work." Form 10-S still requires a robust six-month MD&A and the full suite of certifications. The burden shifts, it doesn't disappear.

The Reg S-X Staleness Rule Change (What Almost Nobody Is Explaining)

This is the part of the proposal that most coverage glosses over, and it has direct consequences for any company with an active shelf registration or M&A pipeline.

Current rule: Regulation S-X Rule 3-12 sets fixed financial statement staleness thresholds of 129 days for accelerated filers and 134 days for non-accelerated filers. If your financial statements are older than those thresholds at the time a registration statement goes effective, you must update them.

Proposed rule: Rule 3-12 would be eliminated and consolidated into Rule 3-01. The fixed day counts would be replaced with a model tied to the most recently required periodic report filing deadline. For a quarterly filer, that anchor is the most recently completed fiscal quarter. For a semiannual filer, it is the most recently completed semiannual period.

What this means in practice:

- A semiannual filer would not be required to produce interim quarterly financial results in a registration statement or proxy statement. The staleness clock runs from the semiannual period end, not from a fixed 129/134-day count.

- Rules 10-01 and 8-03 would be amended so that "interim" means a fiscal quarterly period for quarterly filers and a fiscal semiannual period for semiannual filers.

- For shelf takedowns and Form S-3 eligibility, the financial statement currency requirements would differ between quarterly and semiannual filers. A semiannual filer's financial statements could be "current" for a longer window after the semiannual period end than a quarterly filer's would be after a quarter end, but the flip side is a longer gap between required updates.

Companies that run frequent shelf takedowns or conduct registered M&A transactions should model this change carefully before electing semiannual reporting. The interaction between the semiannual election and WKSI status, Form S-3 eligibility, and the timing of capital markets windows is not fully resolved in the proposal and warrants a comment letter or legal analysis.

For more on how registration statement requirements work, see Finrep's guide to S-1 vs S-11 vs S-4 registration statements.

The Three Hidden Operational Traps

These are the risks that most coverage mentions briefly and then moves on. Your disclosure team needs to work through each one before the rule is finalized.

Trap 1: Your Debt Covenants May Already Require Quarterly Financials

This is the most underappreciated operational constraint in the entire proposal. Many credit agreements and bond indentures include affirmative covenants requiring the borrower to deliver quarterly financial statements to lenders, regardless of what the SEC requires.

If your company elects semiannual SEC reporting but your credit agreement requires quarterly financials, you will still prepare quarterly financials, just without the rigor and public accountability of Form 10-Q. You get the governance cost without the compliance relief.

Before electing Form 10-S, your treasury and legal teams need to:

- Pull every credit agreement, term loan, revolving facility, and bond indenture.

- Search for financial reporting covenants, specifically any requirement to deliver quarterly financial statements or comply with SEC reporting obligations.

- Assess whether a semiannual SEC election would trigger a technical default or require lender consent.

- Model the cost and timeline of renegotiating or refinancing debt to remove quarterly financial delivery requirements.

For investment-grade companies with broadly syndicated credit facilities, renegotiating these covenants at scale is not a trivial exercise. For many, it will make the semiannual election impractical regardless of what the SEC permits.

Trap 2: MNPI and Insider Trading Windows Get Significantly More Complex

Under quarterly reporting, the pattern is familiar: blackout period before the quarter closes, Form 10-Q filed, trading window opens. The cycle repeats four times a year.

Under semiannual reporting, your company will generate quarterly internal financial data that is never publicly filed. That data is almost certainly material nonpublic information (MNPI). As Gladstone Place Partners noted in their Harvard Law Forum analysis: "The MNPI question becomes trickier, too, when you have quarterly internal data that isn't publicly filed and longer durations of quiet periods to manage."

The practical consequences:

- Blackout periods may extend to cover the quarters where internal data exists but is not publicly disclosed.

- Rule 10b5-1 plan adoption and modification windows become harder to schedule.

- Share repurchase programs face longer periods of restricted activity.

- Insider transactions, including equity award exercises and sales, require more careful coordination.

Your insider trading policy will need a full redesign if you elect semiannual reporting. Compliance officers should not assume the current policy translates to a six-month cycle.

Trap 3: Voluntary Quarterly Earnings Releases Create Shadow Reporting Risk

Form 8-K requirements are unchanged by the proposal. A semiannual filer may still furnish quarterly earnings releases on Form 8-K under Item 2.02. Sullivan & Cromwell practitioners expect many semiannual adopters to do exactly that, at least initially, to support trading windows, capital markets access, and investor dialogue.

But voluntary quarterly earnings releases without the rigor of Form 10-Q create a disclosure controls problem. A Form 10-Q is subject to CEO/CFO certifications, disclosure controls and procedures review, and auditor involvement. A voluntary quarterly 8-K earnings release is not.

If a voluntary quarterly update contains information that is later contradicted by or inconsistent with the Form 10-S, you have a disclosure integrity problem. Your disclosure committee and external auditors need to agree, in advance, on what governance applies to voluntary quarterly releases under a semiannual filing regime.

For a deeper look at how to structure disclosure controls for this kind of complexity, see Finrep's guide on how disclosure teams can master evidence and audit traceability.

Who Should and Should Not Elect Form 10-S

The proposal is available to every domestic reporting company, regardless of size, filer status, or industry. That doesn't mean it makes sense for everyone. Here is a structured view by company profile.

| Company Profile | Elect Form 10-S? | Key Reasoning |

|---|---|---|

| Pre-revenue biotech or clinical-stage company | Likely yes | Investors focus on milestones, not quarterly financials. Analyst coverage is thin. Debt covenants are minimal. Compliance cost savings are material relative to size. |

| Small or micro-cap with limited analyst coverage | Likely yes | Quarterly reporting imposes high fixed costs relative to market cap. Investor base may be concentrated and tolerant of semiannual cadence. |

| Emerging growth company (EGC) post-IPO | Possibly yes | Already benefits from scaled disclosures. Semiannual reporting aligns with the broader Atkins reform agenda for new public companies. |

| Mid-cap with investment-grade debt and active shelf | Likely no | Debt covenants almost certainly require quarterly financials. Shelf takedown timing depends on financial statement currency. Capital markets access is a core business need. |

| Large-cap with broad sell-side analyst coverage | Almost certainly no | Analysts will demand quarterly data regardless. Comparability with peers is critical. Activist risk from perceived reduced transparency. Debt and capital markets constraints are binding. |

| Controlled company or founder-led private-to-public | Possibly yes | Reduced short-termism pressure aligns with long-term focus. But investor relations and analyst coverage still matter for liquidity. |

| Company with active M&A program | No | Registration statement staleness rules under the new Reg S-X model create uncertainty for deal timing. Quarterly financial data is often required in proxy statements and S-4s. |

| Dual-listed company (US + UK/EU) | Evaluate carefully | UK and EU half-year reporting models differ from Form 10-S in important ways. IAS 34 interim reports and UK DTR 4.2 requirements have their own standards. Cross-border investor base may have different expectations. |

Freshfields partner Jenny Hochenberg offered a more optimistic take: "Half-year reporting could have the benefit of encouraging companies to be thoughtful about the quality and materiality of information in a less routinized system, as well as bring the US in line with the EU, UK, and Australia." That alignment argument is real, but it matters most for companies whose investor base already operates in those markets.

The Companion May 19 Proposal: How It Interacts

The semiannual reporting proposal does not exist in isolation. On May 19, 2026, the SEC released a companion registered offering reform proposal that would:

- Raise the large accelerated filer threshold from $700 million to $2 billion in public float.

- Extend disclosure accommodations to approximately 81% of all current public companies.

- Protect new public companies from large accelerated filer status for a minimum of five years post-IPO, regardless of public float.

- Create a subcategory of small non-accelerated filers (the smallest 18% of public companies by assets) with an additional 30 days to file Form 10-K and five extra days to file Form 10-Q.

- Allow information to be incorporated by reference into Form S-1.

The interaction with the semiannual proposal is direct. If the large accelerated filer threshold rises to $2 billion, many companies currently classified as large accelerated filers would become accelerated or non-accelerated filers. That reclassification changes their Form 10-S filing deadline from 40 to 45 days and, critically, may change their auditor attestation obligations under SOX Section 404(b).

Companies near the $700 million to $2 billion public float range should model both proposals together before making any disclosure strategy decisions. For context on how IPO reform fits into the broader 2026 agenda, see Finrep's analysis of IPO Reform 2026.

What to Do Before the Rule Is Finalized

The comment period closes July 6, 2026. Final rules are realistically 12 to 18 months away. Calendar-year companies could first elect semiannual reporting for fiscal year 2028. That timeline is short enough to start planning now.

For disclosure teams and CFO offices:

- Audit your debt agreements. Identify every covenant that requires quarterly financial statements or SEC reporting compliance. Quantify the cost of renegotiation.

- Map your trading window policy. Work with legal and HR to understand what a semiannual filing cycle means for blackout periods, 10b5-1 plan windows, and equity award administration.

- Survey your investor base. Your IR team should understand whether institutional holders and sell-side analysts would tolerate or penalize a semiannual cadence. Peer comparability matters.

- Model the Reg S-X staleness impact. If you run shelf takedowns or expect M&A activity, model how the new staleness rules would affect your capital markets calendar.

- Assess audit committee and auditor implications. Shifting from three quarterly reviews to one semiannual review changes the nature, timing, and likely cost of auditor involvement. Ask your auditors now what PCAOB AS 4105 review procedures would look like for a six-month period.

- Consider a comment letter. The SEC is actively seeking input on whether this framework serves investors and issuers. If your company has a clear view, the comment period is the right venue. Commissioner Peirce explicitly asked whether the Commission should slim down Form 10-Q requirements rather than making quarterly reporting optional, signaling that a separate Form 10-Q reform rulemaking may follow.

For companies that use EDGAR benchmarking to inform disclosure decisions, Finrep's guide on how disclosure teams use SEC EDGAR for benchmarking covers how to track peer filing patterns as the semiannual option rolls out.

FAQ

Is the SEC semiannual reporting proposal final? No. The SEC proposed Release No. 33-11414 on May 5, 2026. The comment period closes July 6, 2026. Final rules are not expected before the first half of 2027 at the earliest. Quarterly reporting remains the default and is not changing until a final rule is adopted.

Can a company switch back to quarterly reporting after electing Form 10-S? Yes, but not mid-year. The election locks in for the full fiscal year. A company can revert to quarterly reporting by leaving the semiannual check box unchecked on its next Form 10-K. An inadvertent election can be corrected by filing a Form 10-K/A before the due date of the first Form 10-Q that would otherwise be required.

Does electing Form 10-S eliminate the need for quarterly earnings releases? No. Form 8-K requirements are unchanged. A semiannual filer may still furnish quarterly earnings releases under Item 2.02 of Form 8-K. Many companies are expected to continue doing so to support trading windows and investor relations, which means the investor-facing disclosure cadence may not change even if the SEC filing cadence does.

How does Form 10-S affect foreign private issuers? The proposal does not change interim reporting requirements for FPIs filing on FPI forms. FPIs that voluntarily file on domestic forms would be permitted to elect semiannual reporting.

Will investors penalize companies that elect semiannual reporting? The risk is real for larger companies with broad analyst coverage. Analysts depend on quarterly data to model earnings and maintain coverage. Companies that differ from peers in reporting cadence create comparability challenges. Activist investors could also use reduced disclosure frequency as a governance attack vector. The risk is lower for smaller companies, pre-revenue issuers, and companies in sectors where investors focus on non-financial milestones.

What is Form 10-S and how does it differ from Form 10-Q? Form 10-S is a new SEC form proposed to replace three quarterly Form 10-Qs with one semiannual report. It requires the same substantive disclosures as Form 10-Q, including MD&A, auditor-reviewed financials, Inline XBRL, and CEO/CFO certifications, but covers a six-month period rather than a quarter. For a full breakdown of the form itself, see Finrep's dedicated explainer on what Form 10-S is and whether your company should switch.

The quarterly reporting framework has survived for 56 years because it serves a real market function. The semiannual proposal does not eliminate that function. It gives companies a choice. For most established public companies, the choice will be to stay quarterly. For a meaningful subset, particularly smaller, pre-revenue, or founder-led companies, Form 10-S could represent a genuine reduction in compliance friction. The work is figuring out which category you are in, before the rule is adopted.