When Regulation A was modernised under the JOBS Act and the SEC's 2015 rulemaking, it carried a specific ambition: to create a scaled public offering pathway that gave smaller companies access to the same broad investor base as a registered IPO, at a fraction of the cost and complexity. The pathway was called a mini-IPO, not by statute, but by the practitioners and commentators who saw it as a middle route between a private Regulation D raise and a full S-1 registration.

Ten years of data are now available. The SEC published updated Regulation A statistics in its March 2026 DERA data release covering offerings through the end of 2025. The same month, Chairman Paul Atkins addressed the Small Business Capital Formation Advisory Committee, acknowledged the pathway's limitations directly, and asked what improvements might make it viable. Daniel Forman of Lowenstein Sandler presented a slide deck to the Committee laying out the practical realities of Regulation A from the perspective of practitioners who have run these transactions.

The data, the Chairman's own remarks, and the practitioner slides together tell a consistent story. This post maps that story precisely, without editorial exaggeration in either direction.

What Is Regulation A and What Did It Promise?

Regulation A is an exemption from full Securities Act registration that permits companies to offer securities to the public without filing a full S-1 registration statement. It was available in a limited form before 2015 but was rarely used. The JOBS Act directed the SEC to update it, and in 2015 the SEC adopted rules creating the current two-tier structure.

Tier 1 permits offerings of up to $20 million in a 12-month period. Tier 1 offerings are subject to state securities law review, which means the issuer must comply with the Blue Sky laws of every state in which it offers securities. This is the primary practical constraint on Tier 1: coordinating state-level review across multiple jurisdictions is costly and slow enough to negate much of the cost advantage over a registered offering.

Tier 2 permits offerings of up to $75 million in a 12-month period (raised from $50 million in March 2021). Tier 2 offerings are exempt from state Blue Sky review for initial sales, a meaningful advantage, but they require audited financial statements, an annual report on Form 1-K, semi-annual reports on Form 1-SA, and current event reports on Form 1-U. These ongoing reporting obligations are scaled relative to Exchange Act reporting, but they are not trivial. Tier 2 is also subject to investment limits for non-accredited investors: the greater of 10% of the investor's annual income or net worth per year.

The securities issued in a Regulation A offering are not restricted securities. They can be resold by the investors who purchased them without registration, which is a structural advantage over Regulation D securities. This tradability is one of the principal reasons Regulation A was positioned as a mini-IPO rather than a private placement.

According to the SEC's resources on Regulation A, the pathway is available to US and Canadian issuers, cannot be used by reporting companies or certain investment companies, and requires the offering circular to be filed with and reviewed by the SEC before sales can begin.

What Does the SEC's Own Data Show About How Regulation A Has Actually Performed?

The SEC's March 2026 DERA data release (Press Release 2026-29) updated statistics on Regulation A offerings through the end of 2025. The data covers qualified offerings since the 2015 rules took effect.

The headline numbers that matter for any company evaluating Regulation A as a capital raising pathway are these.

1,531 completed offerings. Across the period since the 2015 rules, 1,531 Regulation A offerings were completed. This is the full population of successful transactions: not initiated filings, not withdrawn attempts, but offerings that qualified and raised capital.

Approximately $13 million average raise. Total capital raised across all 1,531 completed offerings implies an average raise of approximately $13 million per offering. The median is lower. This is the number that most directly contradicts the mini-IPO positioning: the average Regulation A offering raises a fraction of the $75 million Tier 2 ceiling, and far less than the amounts typically raised in the registered IPO market even for small companies.

Less than 1% of Regulation D capital. At his May 6, 2025 SBCFAC remarks, Chairman Atkins stated directly: "the amount raised under Regulation A is less than one percent of the amount of capital raised under rules 506(b) and 506(c) combined." This is the most significant data point in the entire Regulation A policy debate. The pathway exists. Companies are using it. And it is producing less than one cent of capital for every dollar that private placement raises in the same period.

The 2021 cap increase did not move the needle. The SEC raised the Tier 2 offering limit from $50 million to $75 million in March 2021. In his same remarks, Chairman Atkins noted that "there has not been a significant number of Regulation A offerings seeking to take advantage of the increased limit." The cap increase was intended to make the pathway more attractive to larger issuers. It did not produce a measurable increase in offering size or volume.

Offering volume has declined in the two most recent years. Atkins confirmed that "the overall number of Regulation A offerings has declined the past two years, after increases the prior three years." The pathway peaked in volume terms before the 2021 cap increase and has been contracting since.

Geographic concentration in six states. Regulation A use is heavily concentrated in California, Florida, Nevada, New York, Texas, and Washington. Atkins noted that most other states did not have more than two Regulation A offerings. The geographic distribution reflects both where small growth companies are concentrated and where the legal and financial infrastructure to support Regulation A transactions is available.

Why Did the 2021 Cap Increase Fail to Expand Regulation A Use?

The 2021 increase from $50 million to $75 million in the Tier 2 offering limit addressed a supply-side constraint: the maximum amount any single offering could raise. It did not address the demand-side and structural constraints that actually limit Regulation A use. Understanding why the cap increase failed to move the needle requires understanding what those structural constraints are.

Constraint 1: Upfront costs are high relative to capital raised. Daniel Forman's slides presented to the SBCFAC on May 6, 2025 identified "relatively high upfront costs for amount of capital raised" as the first practical reality of Regulation A. An offering circular must be prepared and reviewed by the SEC before sales can begin, audited financial statements are required for Tier 2, and legal and accounting fees for a qualified offering are comparable to those for a smaller registered offering. For a company targeting a $10 million raise, the upfront costs as a percentage of proceeds are significantly higher than they would be for a company targeting $50 million. The $75 million ceiling does not help the company targeting $10 million. It is irrelevant to them.

Constraint 2: Marketing infrastructure does not exist for Regulation A issuers. Forman's slides noted that "marketing a Reg A offering is difficult and lacks the infrastructure of the traditional IPO market." A registered IPO has an underwriting syndicate, a roadshow process, analyst coverage, and institutional investor relationships. A Regulation A offering has none of these. The issuer must market directly to retail investors, which requires either a strong brand and existing customer base or significant marketing expenditure. Neither is free, and neither is available to most companies at the stage where Regulation A is typically considered.

Constraint 3: Secondary market liquidity is severely limited. Regulation A securities are not restricted, but unrestricted does not mean liquid. The absence of an exchange listing, a market maker, or analyst coverage means that secondary trading is thin or nonexistent for most Regulation A securities. Forman's slides identified navigating secondary sales as a complex system for investors. Atkins referenced a 2022 SBCFAC recommendation that the Commission provide federal preemption from state regulation for secondary resales by investors of Tier 2 securities, noting that the Commission had not acted on this recommendation as of May 2025.

Constraint 4: Successful offerings may complicate future capital raising. Forman's slides noted that "successful offerings under Regulation A may complicate capital raising down the road and often don't go as planned." A company that has conducted a Regulation A offering has hundreds or thousands of small shareholders on its cap table. This creates complexity in future venture rounds, where institutional investors typically want clean cap tables, and in potential M&A transactions. The mini-IPO framing implies a stepping-stone to the public markets. In practice, it can be a detour that makes the eventual path harder.

Constraint 5: Private placement remains easier and cheaper for most issuers. Atkins acknowledged in his SBCFAC remarks that Regulation A "has not been a viable regulatory framework for widespread use by all issuers." The comparison is implicit: a Regulation D 506(b) or 506(c) raise requires no SEC review, no audited financials if the company does not already have them, no ongoing reporting, and can close in weeks rather than months. For a company that has access to accredited investors, the private placement pathway is faster, cheaper, and imposes fewer ongoing obligations. Regulation A only makes sense when the company needs to reach retail investors and cannot, or does not want to, restrict its investor base to accredited investors.

For Which Company Profiles Does Regulation A Still Make Economic Sense?

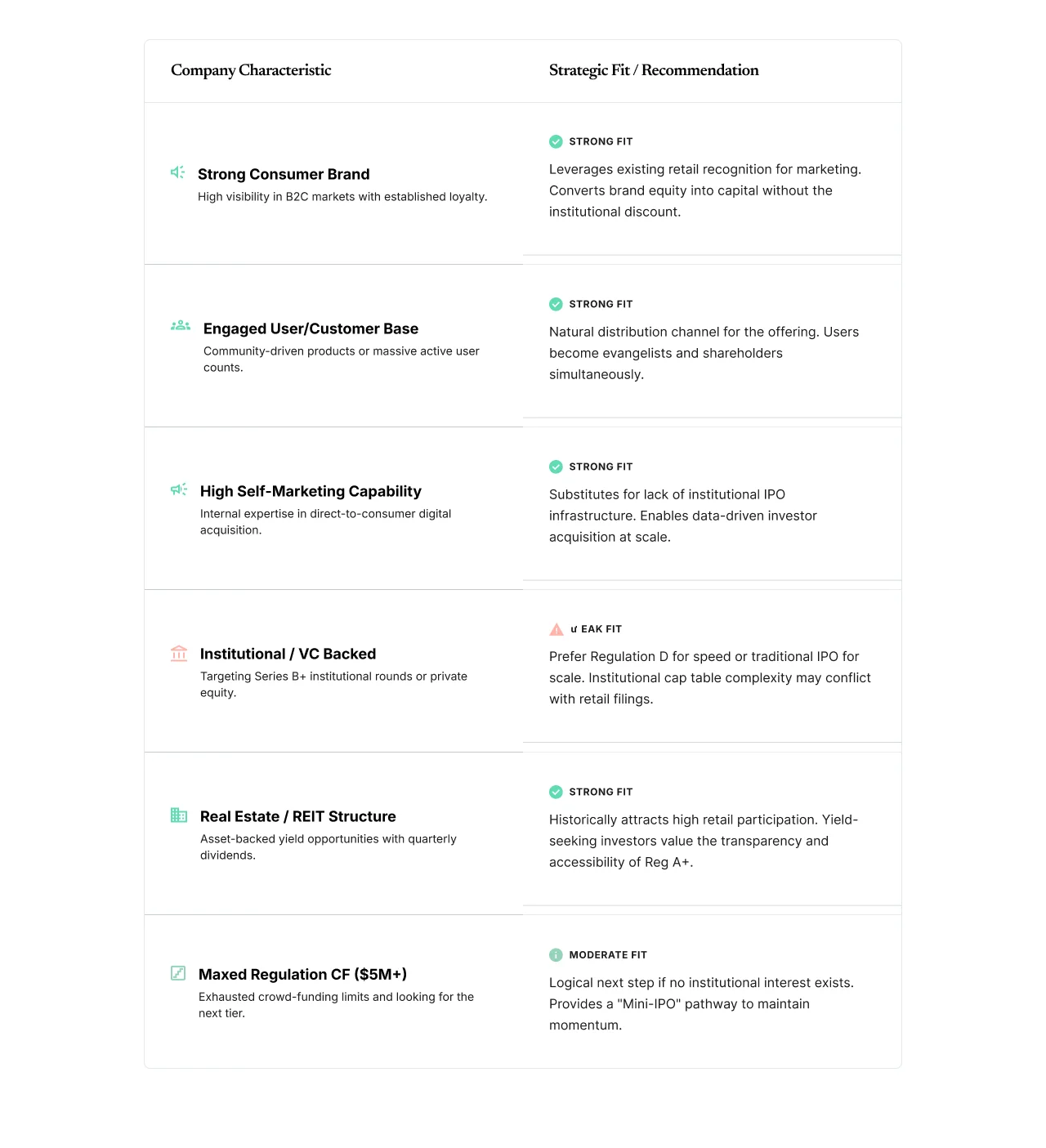

Forman's slides identified the specific company profiles for which Regulation A remains a legitimate capital raising option. These are not generic characterisations. They reflect the structural features of Regulation A that actually differentiate it from private placement.

Companies with strong brand recognition. A brand that retail consumers already know and trust is the most valuable asset in a Regulation A marketing campaign. The marketing infrastructure of a traditional IPO does not exist for Regulation A, which means the company must substitute its own brand for the underwriting syndicate's distribution. Companies with nationally or regionally recognised brands can substitute effectively. Companies without brand recognition cannot.

Companies with loyal and engaged customer or user bases. The most successful Regulation A offerings have been conducted by companies whose customers became investors because they believed in the product. This investor-customer overlap reduces marketing costs and produces a shareholder base that is likely to be supportive. It also creates a natural distribution channel: the company's customer communications platform becomes the offering's marketing channel.

Companies that excel in self-marketing. Forman's slides distinguished this from brand recognition. Self-marketing capability means the issuer has the internal content, community, and distribution capability to reach and convert retail investors without relying on institutional infrastructure. Companies with large social media followings, podcast audiences, email lists, or platform communities have demonstrated this.

Companies not ready for a traditional IPO. The company must be at a stage where the ongoing reporting obligations of Regulation A are manageable and where the capital target is achievable without institutional anchor investors. A company targeting $5 million to $20 million from a large retail investor base, with a compelling consumer narrative and without institutional investors on the cap table, is closer to the ideal Regulation A profile than a company targeting $50 million with an institutional investor base already in place.

Real estate platforms, smaller REITs, and digital asset adjacent companies. Forman's slides specifically identified these sectors. Real estate investment structures have historically attracted retail investor participation in a way that most operating companies have not. Digital asset companies have similarly found retail investor interest in Regulation A structures. These sectors have built some of the secondary market infrastructure and investor familiarity that other sectors lack.

Companies that have used Regulation CF and need more capital. Forman noted companies that have "maxed out Regulation CF but don't have VCs or other institutional investors on equity cap table." Regulation CF allows up to $5 million in a 12-month period. A company that has raised $5 million under Regulation CF and needs $10 to $20 million more, without access to institutional capital, faces a genuine gap that Regulation A is positioned to fill.

Atkins used his May 2025 SBCFAC remarks to ask the Committee for input on specific potential improvements. The questions he posed are the most direct indication of what the SEC is considering. None of these changes has been proposed as a formal rulemaking as of June 2026.

Federal preemption for secondary resales. The 2022 SBCFAC recommendation that secondary resales of Tier 2 securities be federally preempted from state regulation has not been acted on. If adopted, this would reduce the complexity of secondary trading significantly by eliminating the state-by-state analysis currently required for secondary sales. Forman's slides identified this as the first "where to next" priority. Without secondary market liquidity, Regulation A securities are difficult to value and difficult to sell, which reduces their attractiveness to retail investors regardless of the offering's merits.

Eliminating the prohibition on at-the-market offerings. Atkins specifically raised whether eliminating this prohibition would provide a more effective capital raising mechanism. At-the-market (ATM) offerings allow an issuer to sell shares continuously into the open market at prevailing prices rather than through a fixed-price offering. This mechanism is standard for listed public companies. For Regulation A issuers, allowing ATM offerings would require a trading market to exist for the securities, which brings the secondary liquidity problem back into focus.

Addressing geographic concentration. Atkins raised the question of why use is concentrated in six states and whether decreasing that concentration would make the rules more viable. The concentration likely reflects both where eligible companies are located and where the legal and financial advisers who understand Regulation A are concentrated. A broader ecosystem of Regulation A practitioners would reduce the geographic dependence, but building that ecosystem requires deal flow to justify the investment in expertise.

Building a stronger market ecosystem. Forman's slides called for work to "build a stronger market and ecosystem to support Reg A issuers and offerings." This is the structural improvement that no single regulatory change can produce. An ecosystem includes broker-dealers willing to distribute Regulation A securities, secondary trading platforms, legal advisers familiar with the process, and investor familiarity with the asset class. None of these develop without deal flow, and deal flow has declined in the two most recent years.

Frequently Asked Questions

What is Regulation A and how does it differ from a traditional IPO?

Regulation A is a Securities Act exemption that allows companies to raise up to $75 million from the public without a full S-1 registration. It requires an offering circular reviewed by the SEC, audited financial statements for Tier 2, and scaled ongoing reporting obligations. Unlike a traditional IPO, it does not require exchange listing, does not have an underwriting syndicate, does not produce analyst coverage, and does not provide meaningful secondary market liquidity. It permits retail investor participation without accredited investor restrictions, which is its primary structural advantage over Regulation D private placements.

Why did Regulation A fail to become the mini-IPO pathway it was intended to be?

The SEC's own data and Chairman Atkins's May 2025 SBCFAC remarks identify the core reasons: upfront costs are high relative to the capital raised by most offerings, the marketing infrastructure of the traditional IPO market does not exist for Regulation A, secondary market liquidity is severely limited because securities are not exchange-listed, and private placement under Regulation D remains faster, cheaper, and simpler for companies with access to accredited investors. The 2021 cap increase from $50 million to $75 million did not produce a measurable increase in offering size or volume.

How much capital does Regulation A raise compared to Regulation D?

Atkins confirmed at the May 2025 SBCFAC meeting that Regulation A raises less than 1% of the capital raised under Regulation D rules 506(b) and 506(c) combined. Across 1,531 completed offerings since the 2015 rules took effect, the average Regulation A offering has raised approximately $13 million.

What company profiles are best suited for Regulation A?

According to Daniel Forman's SBCFAC slides, the best-fit profiles are companies with strong brand recognition, companies with loyal and engaged customer bases who can become investors, companies that excel in self-marketing without institutional infrastructure, real estate platforms and smaller REITs, digital asset adjacent companies, and companies that have exhausted Regulation CF's $5 million annual limit but lack institutional investors on their cap table.

What changes are being considered to improve Regulation A's viability?

As of June 2026, Atkins has raised but not formally proposed three potential improvements: federal preemption for secondary resales of Tier 2 securities (recommended by the SBCFAC in September 2022 but not yet acted on), elimination of the prohibition on at-the-market offerings, and measures to reduce geographic concentration of use. Forman's slides also called for building a stronger market ecosystem including broker-dealer distribution and secondary trading platforms.

Should a company use Regulation A or Regulation D for its next capital raise?

The answer depends on whether the company needs to reach retail investors who are not accredited. If the company has access to accredited investors and does not need a retail investor base, Regulation D 506(b) or 506(c) is faster, cheaper, and imposes no ongoing reporting obligations. If the company has a strong consumer brand, an engaged customer base, and specifically needs to raise capital from retail investors, and if the marketing infrastructure exists to reach them, Regulation A may be appropriate. The decision should be made with full awareness of the upfront costs, the secondary market liquidity limitations, and the potential cap table complications for future institutional rounds.

Key Takeaways

- The SEC's March 2026 DERA data shows 1,531 completed Regulation A offerings with an average raise of approximately $13 million. Total capital raised under Regulation A represents less than 1% of capital raised under Regulation D 506(b) and 506(c) combined, as confirmed by Chairman Atkins at the May 2025 SBCFAC meeting.

- The 2021 cap increase from $50 million to $75 million did not produce a significant number of offerings seeking to take advantage of the increased limit. Overall Regulation A offering volume has declined in the two most recent years after increasing the prior three.

- The four structural bottlenecks, as identified in Forman's SBCFAC slides, are high upfront costs relative to capital raised, absence of the marketing infrastructure of the traditional IPO market, severely limited secondary market liquidity, and cap table complexity that complicates future institutional rounds.

- Regulation A is not a replacement for the traditional IPO. It is a retail investor access mechanism that requires specific company conditions to work: brand recognition, an engaged customer base, self-marketing capability, and a capital target achievable without institutional anchor investors.

- The company profiles for which Regulation A makes most economic sense are: consumer-facing companies with strong brands, real estate platforms and smaller REITs, digital asset adjacent companies, and companies that have exhausted Regulation CF's $5 million limit.

- The regulatory improvements that would move the needle (federal preemption for secondary resales, elimination of the ATM offering prohibition, and ecosystem building) have been raised by Atkins and the SBCFAC but none has been formally proposed as rulemaking as of June 2026.