The SEC's Office of the Chief Accountant does not issue formal guidance on every accounting question that emerges from changing economic conditions. When it does address a topic at length at a major conference, practitioners treat that as a meaningful signal. At the Practising Law Institute's SEC Speaks conference in March 2026, the OCA addressed tariff-related accounting and disclosure questions at length. Chief Accountant Kurt Hohl and CorpFin Chief Accountant Heather Rosenberger both spoke directly to the tariff question, covering recognition, disclosure, and the non-GAAP treatment that has become a significant point of friction.

This post maps what they said, what the applicable ASC standards require, and how those two things interact in practice for a company with material tariff exposure preparing its Q1 or Q2 2026 filings.

What Did the SEC's Office of the Chief Accountant Actually Say About Tariff Accounting?

At SEC Speaks in March 2026, OCA Chief Accountant Kurt Hohl made three specific observations about tariff accounting that practitioners need to understand as guidance signals rather than informal commentary.

First, Hohl observed that few companies are currently recognising tariff refunds on their financial statements. His stated reason was uncertainty about how refund mechanisms will operate. This is a direct signal that the OCA is watching how companies account for the IEEPA tariff refund question and that the bar for recognition is high. It is not an instruction to avoid recognition in all circumstances. It is a signal that the OCA's expectation aligns with a conservative reading of the applicable gain contingency standard.

Second, Hohl stated that companies with material tariff-related exposures may need to adjust their financial statements and ensure adequate disclosure. The phrase "may need to adjust" is notable. It signals that the OCA does not view tariff accounting as a disclosure-only question for all affected companies. For some, the financial statement recognition question is live and unresolved.

Third, CorpFin Chief Accountant Heather Rosenberger noted that the specificity of tariff disclosures has increased meaningfully over the past year but cautioned that non-GAAP adjustments designed to strip out the impact of tariffs are "likely not appropriate." This is the most operationally significant statement from the conference for most reporting teams, and it is addressed in detail below.

According to the Perkins Coie analysis of SEC Speaks 2026, Rosenberger also reminded registrants that MD&A disclosures should be evaluated on an annual basis considering macroeconomic changes such as tariffs and trade restrictions, and that the COVID-19 disclosure guidance the staff published in 2020 serves as a useful framework for thinking about what specificity is required.

The OCA's comments at SEC Speaks are not Staff Accounting Bulletins and they are not rulemaking. But they represent the interpretive views of the people who review financial statements and send comment letters. Practitioners should treat them as strong signals of where comment letter scrutiny will focus.

How Do Tariffs Enter the Financial Statements Under ASC 330?

The foundational accounting question for most companies is how tariff costs are recognised in the first instance. Under ASC 330, tariffs paid to import goods are part of the cost of putting inventory in a condition and location ready for sale. They are capitalised into inventory cost, not expensed as incurred.

This treatment is not optional. ASC 330-10-30-1 requires that inventory cost include all costs incidental to bringing goods to their existing condition and location. Tariffs paid to U.S. Customs and Border Protection on imported goods meet this definition. They are part of the landed cost of the inventory.

The practical consequence for financial statements is that tariff costs do not flow through the income statement at the time of payment. They remain on the balance sheet as part of inventory until the goods are sold, at which point they flow through cost of goods sold. For a company carrying significant import inventory with elevated tariff rates, the balance sheet carries a higher cost basis than it did under prior tariff rates, and cost of goods sold increases as that inventory turns.

The inventory cost capitalisation treatment creates a secondary accounting question: net realisable value. ASC 330-10-35-1B requires inventory to be measured at the lower of cost or net realisable value. If tariff costs have elevated the cost basis of inventory to a level that exceeds what the inventory can be sold for` either because selling prices cannot be fully passed through to customers or because competitive pressure constrains pricing a write-down is required.

Determining NRV under current conditions requires judgment about selling prices, customer acceptance of price increases, and competitive dynamics. According to EisnerAmper's analysis of tariff accounting implications, once inventory is written down to NRV, the reduced amount becomes the new cost basis and cannot be subsequently marked up, even if market conditions improve. This asymmetry is consequential: a write-down taken in Q1 based on tariff levels prevailing at that time cannot be reversed if tariff rates are subsequently reduced.

How Are Tariff Refunds Recognised Under ASC 450 and ASC 410?

The tariff refund question and the OCA's specific observation that few companies are recognising refunds requires understanding the recognition framework before applying the OCA's signal.

Following the U.S. Supreme Court's ruling on February 20, 2026, holding IEEPA tariffs unconstitutional, companies that paid IEEPA tariffs are potentially entitled to refunds. The accounting question is when a refund receivable can be recognised on the balance sheet.

Two analytical frameworks have emerged in practice.

The gain contingency model under ASC 450. Under ASC 450-30, a tariff refund is a gain contingency. Gain contingencies cannot be recognised in financial statements until the gain is realised or virtually certain. This is a deliberately conservative standard. Unlike loss contingencies, which require accrual if probable, gain contingencies require near-certainty before recognition. Until CBP formally approves and liquidates a specific refund amount for specific entry summaries, most companies cannot conclude that recognition is appropriate under this model.

The loss recovery model under ASC 410-30 by analogy. The second framework treats the expected tariff refund as a recovery of a previously recognised loss, applying ASC 410-30 by analogy. Under this approach, a receivable may be recognised when recovery is probable, subject to a cap at the carrying amount of the previously recognised loss. This threshold is lower than the gain contingency standard, and it is why some companies have been able to support earlier balance sheet recognition for IEEPA refunds.

According to Grant Thornton's analysis of SCOTUS tariff ruling accounting implications, entities may reasonably apply either of these two approaches when determining whether to recognise an asset related to future refunds of previously paid IEEPA tariffs. The choice between frameworks is an accounting policy decision that must be applied consistently and disclosed.

The OCA's observation at SEC Speaks that few companies are currently recognising refunds is consistent with the conservatism built into both frameworks particularly the gain contingency model, which is the more commonly applied default. Companies applying the loss recovery model with documented support for a probable conclusion can support earlier recognition, but the evidential bar remains high and documentation of the probability conclusion is essential.

Where refunds are not recognised, disclosure is still required under ASC 450-30 if the amount involved is material and the probability assessment indicates the refund is at least reasonably possible.

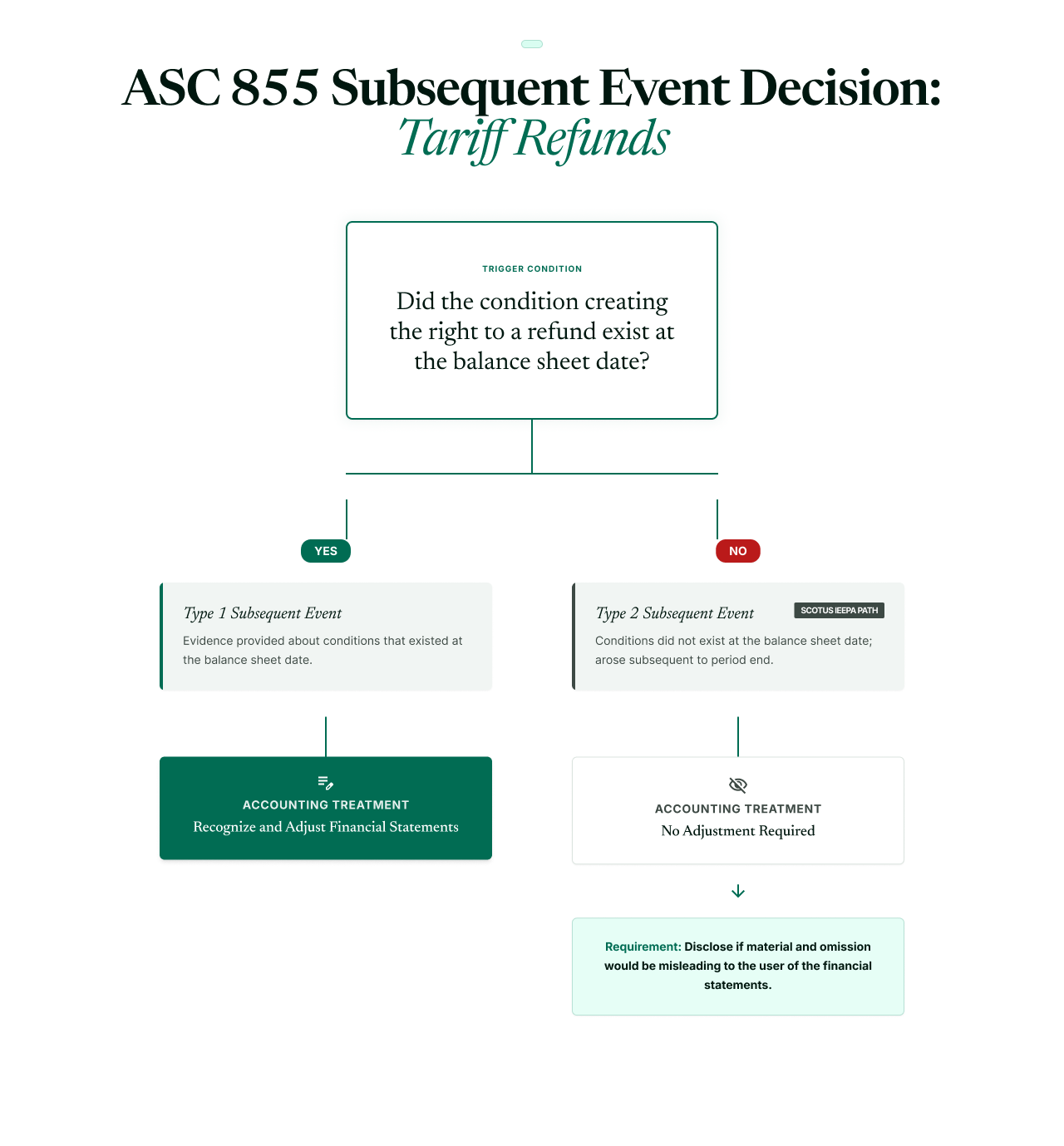

What Does the SCOTUS Ruling Require Under ASC 855 for Balance Sheet Date Filers?

For companies with December 31, 2025 fiscal year-ends, the SCOTUS ruling of February 20, 2026 is a subsequent event under ASC 855. The analysis requires determining whether it is a Type 1 (recognised) or Type 2 (non-recognised) subsequent event.

A Type 1 subsequent event provides additional evidence about conditions that existed at the balance sheet date and requires adjustment to the financial statements. A Type 2 subsequent event relates to conditions that arose after the balance sheet date and does not require adjustment, but requires disclosure if the event is material and its omission would render the financial statements misleading.

According toTheCorporateCounsel.net's analysis of the SCOTUS tariff ruling as a subsequent event, it is acceptable to treat the Supreme Court's decision as a non-recognised (Type 2) subsequent event in financial statements that have not yet been issued as of February 20, 2026. The condition creating the right to a refund did not exist at December 31, 2025.

The consequence is that December 31, 2025 financial statements do not require balance sheet adjustment for expected tariff refunds as a result of the SCOTUS ruling, but they do require disclosure if the ruling is expected to have a material effect on the financial statements when ultimately recognised, or if non-disclosure would otherwise result in the omission of material information.

Under ASC 855-10-50-2, disclosure of a non-recognised subsequent event must include the nature of the event and an estimate of its financial effect, or a statement that an estimate cannot be made. For companies with material IEEPA tariff exposure, this means providing a description of the ruling and its implications, and either quantifying the expected refund amount or explaining why quantification is not possible at this stage.

Companies should also assess whether the subsequent event disclosure requires supplemental analysis under ASC 275 (risks and uncertainties) and ASC 450 (contingencies) to address the full scope of tariff-related uncertainty in the financial statement footnotes.

What Does the SEC Expect in MD&A Tariff Disclosures?

The OCA's signal at SEC Speaks that tariff disclosure specificity has increased meaningfully over the past year creates an important benchmark question: what does adequate specificity look like under Regulation S-K?

Under Regulation S-K Item 303, MD&A must address known trends and uncertainties that are likely to have a material effect on financial condition, results of operations, and liquidity. Tariffs qualify as a known trend or uncertainty for any company with material import exposure, and the disclosure obligation is not satisfied by a generic statement that tariffs may affect costs.

Based on the OCA's signals at SEC Speaks 2026 and the framework published by Grant Thornton from the December 2025 AICPA conference, a company with material tariff exposure should consider addressing five specific elements in MD&A.

First, the magnitude of the business affected. What portion of the company's procurement, cost of goods sold, or revenue base is subject to tariff exposure? Generic risk factor language that acknowledges tariff risk without quantifying its scale is increasingly insufficient.

Second, the company's ability to mitigate the impact. Can the company shift sourcing, renegotiate supplier terms, or otherwise reduce tariff exposure? If so, what progress has been made and what is the timeline?

Third, the ability to pass increased costs through to customers. Can pricing absorb the tariff increase? What is the evidence for that conclusion? What is the competitive context?

Fourth, the resulting effects on profitability, financial condition, and liquidity. This is where the quantitative specificity the OCA flagged as having improved becomes the expectation rather than the aspiration. How much did tariffs affect gross margin in the reporting period? What is the forward-looking sensitivity?

Fifth, potential impairments or increased allowance for credit losses. For companies carrying tariff-exposed inventory at elevated cost basis, or companies with customers whose financial position is affected by tariff conditions, these secondary effects belong in the MD&A risk assessment.

The reference point the OCA staff offered for how to frame these disclosures is the COVID-19 disclosure guidance published in 2020. That guidance emphasised company-specific, quantified, forward-looking disclosure rather than boilerplate risk acknowledgement. The standard being applied to tariff disclosures in 2026 is the same one.

Why Are Tariff Non-GAAP Adjustments "Likely Not Appropriate"?

The OCA's most operationally significant statement from SEC Speaks 2026 on tariffs was Rosenberger's characterisation that non-GAAP adjustments designed to strip out the impact of tariffs are "likely not appropriate." This requires precise interpretation before a reporting team applies it.

The general framework for non-GAAP measure appropriateness under Regulation G and Item 10(e) of Regulation S-K prohibits adjustments that eliminate normal, recurring cash operating expenses. It also prohibits measures that are misleading or present a company's performance in a way that is not consistent with how management actually manages the business.

Tariff costs, once a company is operating in a tariff-affected environment, are a normal cost of doing business for that company. They are not a one-time charge, an acquisition-related item, or a restructuring cost. They are not analogous to the types of items that non-GAAP presentations have traditionally excluded. Stripping tariff costs out of a non-GAAP measure would effectively allow management to present a picture of performance that excludes a recurring cost of importing goods. Rosenberger's "likely not appropriate" signal is consistent with the existing non-GAAP framework and is not new law. It is an application of existing rules to a new fact pattern.

There is a nuance that practitioners should be aware of. The statement targets non-GAAP adjustments designed to strip out the impact of tariffs. It does not prohibit all qualitative or supplemental disclosure of tariff impacts. A company that discloses the tariff impact on gross margin as supplemental information within a GAAP-compliant MD&A discussion without constructing a non-GAAP measure that excludes tariff costs is not in the category Rosenberger was addressing.

The practical test is whether the company is creating a financial measure that presents results as if tariff costs did not exist. If the answer is yes, that measure is the type the OCA characterised as likely not appropriate. If the company is providing additional context about how tariff costs affected GAAP results without creating an alternative performance measure, that supplemental context is within bounds.

According to the Harvard Law Forum's 2026 annual reporting considerations, SEC staff comment letters on non-GAAP measures increased by more than 10% in the most recent year, with the appropriateness of adjustments to eliminate normal, recurring cash operating expenses ranking as the most frequent source of non-GAAP comment. Companies should treat any proposed tariff non-GAAP adjustment as a comment letter risk and ensure robust pre-filing analysis before including such a measure.

What Disclosures Are Required Beyond MD&A?

The MD&A obligation does not exhaust the tariff disclosure requirement. Several additional disclosure frameworks apply to companies with material tariff exposure, and the OCA's signals at SEC Speaks implicitly covered the full scope.

ASC 275 (Risks and Uncertainties). ASC 275-10-50 requires disclosure of concentrations of risk, including concentrations in the geographic location of suppliers. A company that sources a material portion of its inventory from countries subject to elevated tariff rates has a concentration that falls within the scope of ASC 275 disclosure. The disclosure must describe the nature of the concentration and, if it is reasonably possible that the concentration will result in a near-term severe impact, that possibility must be disclosed.

Regulation S-K Item 105 (Risk Factors). Risk factor disclosure should address specific, company-tailored tariff risk rather than generic trade policy risk. The SEC staff has consistently commented on risk factors that are generic and do not reflect the specific risks facing the registrant. A company with material China-sourced import exposure has different tariff risk than a company with minimal import activity, and the risk factor should reflect that specificity.

Regulation S-K Item 303 (MD&A Liquidity). Beyond the results of operations discussion, the liquidity section of MD&A should address whether tariff-related cash outlays have affected or are expected to affect the company's liquidity position, including working capital, cash conversion cycle, and revolving credit availability.

ASC 205-40 (Going Concern). For companies with thin margins where tariff-related cost increases are material, a going concern assessment is required if conditions and events in the aggregate raise substantial doubt about the company's ability to continue as a going concern within one year of the financial statement issuance date. This assessment must consider the cumulative effect of tariff costs on cash flows and projections.

Frequently Asked Questions

What is the SEC OCA's position on tariff accounting for 2026 filings?

At SEC Speaks in March 2026, OCA Chief Accountant Kurt Hohl and CorpFin Chief Accountant Heather Rosenberger addressed tariff accounting at length. Hohl noted that few companies are currently recognising tariff refunds due to uncertainty about refund mechanisms, and that companies with material tariff exposures may need to adjust financial statements and ensure adequate disclosure. Rosenberger noted that tariff disclosure specificity has increased but cautioned that non-GAAP adjustments to strip out tariff impacts are "likely not appropriate." These are not formal rulemaking statements but represent strong interpretive signals from the staff who review filings and issue comment letters.

How do tariff costs enter a company's financial statements under US GAAP?

Under ASC 330, tariffs paid to import goods are capitalised as part of inventory cost. They do not flow through the income statement at the time of payment. They remain on the balance sheet until the related inventory is sold, at which point they flow through cost of goods sold. The secondary question is whether capitalised tariff costs have elevated the inventory cost basis above net realisable value, which would require a write-down under ASC 330-10-35-1B.

Can a company recognise a tariff refund receivable on its balance sheet?

Two frameworks apply. Under the gain contingency model (ASC 450-30), a tariff refund can only be recognised when realised or virtually certain. Under the loss recovery model (ASC 410-30 applied by analogy), a receivable may be recognised when recovery is probable, capped at the amount of the previously recognised loss. Most companies with IEEPA tariff refund claims are applying the gain contingency model conservatively, with recognition deferred until CBP formally approves specific refund amounts. The OCA's observation that few companies are currently recognising refunds is consistent with this conservative application.

Is the SCOTUS tariff ruling a Type 1 or Type 2 subsequent event under ASC 855?

For December 31, 2025 filers, the February 20, 2026 SCOTUS ruling holding IEEPA tariffs unconstitutional is a Type 2 (non-recognised) subsequent event. The condition creating the right to a refund did not exist at the balance sheet date. Accordingly, it does not require balance sheet adjustment in December 31, 2025 financial statements, but does require disclosure if material and if omission would render the financial statements misleading. Disclosure must include the nature of the event and an estimate of its financial effect or a statement that an estimate cannot be made.

Why did the OCA say tariff non-GAAP adjustments are likely not appropriate?

The OCA's position applies existing non-GAAP rules to the tariff fact pattern. Regulation G and Regulation S-K Item 10(e) prohibit non-GAAP measures that eliminate normal, recurring cash operating expenses. For a company operating in a tariff-affected environment, tariff costs on imported goods are a recurring cost of doing business, not a one-time or non-recurring item. A non-GAAP measure that strips out tariff costs presents performance as if that cost did not exist. The OCA's signal is that this type of adjustment is likely to attract comment letter scrutiny.

What MD&A disclosures are required for tariff exposure?

Under Regulation S-K Item 303, companies with material tariff exposure must disclose known trends and uncertainties likely to affect financial condition, results of operations, and liquidity. Based on OCA signals and the AICPA conference framework, disclosure should address the magnitude of the affected business, the company's ability to mitigate or pass through costs, the impact on profitability and liquidity, and any potential impairments or credit loss implications. Generic acknowledgement of tariff risk is insufficient. Quantified, company-specific, forward-looking disclosure is the expectation.

Key Takeaways

- The OCA addressed tariff accounting at length at SEC Speaks 2026. OCA Chief Accountant Kurt Hohl noted that few companies are recognising tariff refunds due to uncertainty about refund mechanisms, and that companies with material exposure may need to adjust financial statements. These are signals of where comment letter scrutiny will focus.

- Tariff costs on imported goods are capitalised into inventory under ASC 330, not expensed at the time of payment. The secondary question is NRV: if capitalised tariff costs exceed what inventory can be sold for, a write-down is required and cannot subsequently be reversed.

- Tariff refund recognition requires either the gain contingency standard (realised or virtually certain, under ASC 450-30) or the loss recovery model (probable, capped at prior loss, under ASC 410-30 by analogy). The choice is an accounting policy decision requiring consistent application and disclosure.

- The SCOTUS IEEPA ruling of February 20, 2026 is a Type 2 non-recognised subsequent event for December 31, 2025 filers. It requires disclosure if material, but not balance sheet adjustment. Disclosure must include the nature of the event and an estimate of its financial effect.

- Tariff non-GAAP adjustments that strip out the impact of tariffs are "likely not appropriate," per CorpFin Chief Accountant Rosenberger at SEC Speaks 2026. Tariff costs are recurring operating costs, not the type of item traditionally excluded from non-GAAP measures.

- MD&A disclosure must be company-specific, quantified, and forward-looking. Magnitude of exposure, mitigation steps, pricing pass-through ability, and profitability impact should all be addressed. Additional disclosure under ASC 275, Item 105, and going concern assessment under ASC 205-40 may also be required depending on facts and circumstances.