A CFO preparing for an IPO will hear all four terms in the first 30 days of engaging securities counsel. They will hear them from bankers, from external auditors, from the underwriter's counsel, and from the exchange listing team. In almost every case, at least two of the four will be used interchangeably by someone in the room who should know the difference.

The conflation is understandable. All four terms are associated with smaller companies. All four convey some sense of reduced regulatory burden, and the overlap between them is genuine, a company can simultaneously qualify under three of the four. But they are governed by different statutes, defined by different metrics, carry different obligations, and apply at different points in a company's lifecycle.

Getting the categorisation wrong at the time of an IPO produces two types of error. Over-qualification means the company prepares disclosures it was not required to prepare, pays for audits it was not required to obtain, and files on deadlines tighter than its obligations required. Under-qualification means the company misses required disclosures, receives SEC comment letters, and must remediate in subsequent filings. Both errors are preventable. The definitions are precise.

What Does Micro-Cap Actually Mean and Who Defines It?

Micro-cap is the only one of the four terms that is not a defined regulatory category. The SEC does not define micro-cap. No statute creates it. No rule governs it.

Micro-cap is a market convention used by exchanges, index providers, data vendors, and the financial press to describe public companies within a certain market capitalisation range. The most commonly used definition in market practice treats micro-cap as companies with a total market capitalisation between approximately $50 million and $300 million, though different providers apply different boundaries. Some use $50 million to $250 million. Others use $50 million to $500 million. The SEC's own investor education materials on its Investor.gov site use the term in a general sense to describe smaller public companies without providing a precise definition.

The reason micro-cap matters to a pre-IPO CFO is not regulatory. It matters commercially. Micro-cap stocks are disproportionately associated with thin float, limited analyst coverage, and elevated manipulation risk. The SEC's Investor.gov site explicitly flags micro-cap stocks as an area of heightened fraud concern. Exchanges have been tightening their continued listing standards specifically in response to micro-cap market quality issues, as reflected in the NYSE American and Nasdaq rule proposals of early 2026.

A company that is a micro-cap by market convention may simultaneously be an SRC, an EGC, and a NAF under SEC rules. It may be none of them. The market convention and the regulatory categories are independent.

The practical implication for a pre-IPO CFO: micro-cap describes where your company will sit in the market. SRC, EGC, and NAF describe what you are required to disclose and when. Confusing the market description with the regulatory definition is the most common source of misinformation in pre-IPO planning discussions.

What Is an SRC and What Does SRC Status Actually Change?

Smaller Reporting Company (SRC) is an SEC filer category defined in Exchange Act Rule 12b-2 and Securities Act Rule 405. It is a disclosure-scaling category, not a filing-deadline category and not an IPO-specific category. A company can be an SRC whether it is newly public or has been filing for twenty years.

The qualification test. Under the SEC's 2018 amendments to the SRC definition, a company qualifies as an SRC if it meets either of two tests:

The public float test: public float of less than $250 million as of the last business day of its most recently completed second fiscal quarter.

The revenue test: annual revenues of less than $100 million during the most recently completed fiscal year for which audited financial statements are available, and either no public float or a public float of less than $700 million.

Both tests are measured annually. A company that qualifies on one test qualifies as an SRC regardless of whether it would qualify on the other.

The re-entry threshold. A company that loses SRC status because it exceeded a threshold does not immediately regain it when it falls back below that threshold. Re-entry requires meeting 80% of the threshold on which it previously failed: public float below $200 million (80% of $250 million) or annual revenue below $80 million (80% of $100 million).

What SRC status changes. SRC status provides scaled versions of, or complete exemptions from, specific Regulation S-K and Regulation S-X disclosure requirements. The most significant accommodations include scaled executive compensation disclosures under Item 402 (SRCs are exempt from the full proxy compensation tables required of non-SRCs), two years of audited financial statements rather than three in registration statements, reduced MD&A requirements, and exemption from the CEO pay ratio disclosure under Item 402(u).

SRC status does not affect filing deadlines. A company that is simultaneously an SRC and a large accelerated filer still files on the 60-day 10-K and 40-day 10-Q deadlines. SRC status affects what the filing contains, not when it must be filed.

What Is an EGC and How Is It Different From an SRC?

Emerging Growth Company (EGC) is a category created by the Jumpstart Our Business Startups Act of 2012, codified in Securities Act Section 2(a)(19) and Exchange Act Section 3(a)(80). It is an IPO-specific on-ramp category. It applies to companies for a defined period after their first sale of equity securities under an effective Securities Act registration statement, subject to four termination triggers.

The qualification test. A company qualifies as an EGC at its IPO if it had total annual gross revenues of less than $1.235 billion during its most recently completed fiscal year. This threshold was adjusted for inflation from the original $1 billion in September 2022. The SEC is required by statute to adjust it every five years.

The four EGC status termination triggers. A company loses EGC status on the earliest of:

The last day of the fiscal year in which total annual gross revenues are $1.235 billion or more.

The last day of the fiscal year following the fifth anniversary of the IPO. This is the maximum duration of EGC status regardless of revenue.

The date on which the company has issued more than $1 billion in non-convertible debt in the previous three years.

The date on which the company becomes a large accelerated filer: the end of the fiscal year during which the company has been subject to Exchange Act reporting for 12 calendar months and has a public float of $700 million or more as of the last business day of its most recently completed second fiscal quarter.

What EGC status changes. EGC accommodations are more extensive than SRC accommodations in several respects. EGCs may submit a draft registration statement for confidential nonpublic SEC review (the DRS process). EGCs need provide only two years of audited financial statements in their IPO registration statement rather than three. EGCs may provide reduced executive compensation disclosure. EGCs are exempt from the auditor attestation on internal control over financial reporting required by SOX Section 404(b) while they remain EGCs. EGCs may take advantage of the extended transition period for adopting new or revised financial accounting standards, deferring adoption until non-public company effective dates.

How SRC and EGC differ. The two categories are independent and a company can qualify for both simultaneously. The key distinctions are:

EGC is time-limited from IPO. SRC is perpetual if the thresholds are met.

EGC is IPO-specific. It applies to companies that have not previously conducted a public offering of common equity. SRC applies to any public company meeting the size test, regardless of IPO history.

EGC accommodations apply to the IPO registration statement itself, including the DRS process and the two-year financial statement requirement. SRC accommodations apply to periodic filings after the company is public.

EGC status terminates when the company becomes a large accelerated filer. SRC status does not terminate automatically on the basis of float. It terminates when the company exceeds the $250 million float test or the revenue test on its annual measurement date.

A company that qualifies as both an EGC and an SRC may generally elect to use the accommodations of either category, whichever is more favourable for a given disclosure item.

What Is a NAF and Why Does It Govern Filing Deadlines Rather Than Disclosure?

Non-Accelerated Filer (NAF) is an Exchange Act filer category defined in Exchange Act Rule 12b-2. It is a filing-deadline category and an audit obligation category. It governs when you must file your 10-K and 10-Q and whether you are subject to the SOX 404(b) external auditor attestation on internal control over financial reporting.

The qualification test. A company is a non-accelerated filer if it does not qualify as a large accelerated filer or an accelerated filer. The current categories are:

Large Accelerated Filer (LAF): public float of $700 million or more, has been subject to Exchange Act reporting for at least 12 calendar months, has filed at least one annual report, and is not eligible to use Forms 10-KSB or 10-QSB.

Accelerated Filer (AF): public float of $75 million or more but less than $700 million, has been subject to Exchange Act reporting for at least 12 months, and has filed at least one annual report.

Non-Accelerated Filer (NAF): does not meet the LAF or AF thresholds. This category typically covers a company with a public float below $75 million, or a newly public company that has not yet been subject to Exchange Act reporting for 12 months.

What NAF status changes. NAF status provides two specific benefits. First, extended filing deadlines: NAFs file their 10-K within 90 days of fiscal year-end (versus 75 days for accelerated filers and 60 days for large accelerated filers) and their 10-Q within 45 days of quarter-end (versus 40 days for accelerated and large accelerated filers).

Second, and most consequentially, NAFs are exempt from the SOX Section 404(b) external auditor attestation on internal control over financial reporting. This exemption is separate from the EGC exemption. A company that has lost EGC status but still qualifies as a NAF based on its public float retains the 404(b) exemption on that basis.

Why NAF and SRC are frequently confused. Both NAF and SRC are associated with smaller public companies. Both provide relief from certain compliance burdens. But they operate on different metrics and provide relief in different areas:

NAF is determined by public float and Exchange Act reporting history. It governs filing deadlines and SOX 404(b).

SRC is determined by public float or revenue. It governs the content of disclosures in the filings.

A company with a $150 million public float is an accelerated filer (not a NAF) for filing deadline purposes but qualifies as an SRC for disclosure scaling purposes. It files on accelerated filer deadlines and uses SRC disclosure accommodations. Getting this wrong in either direction is costly.

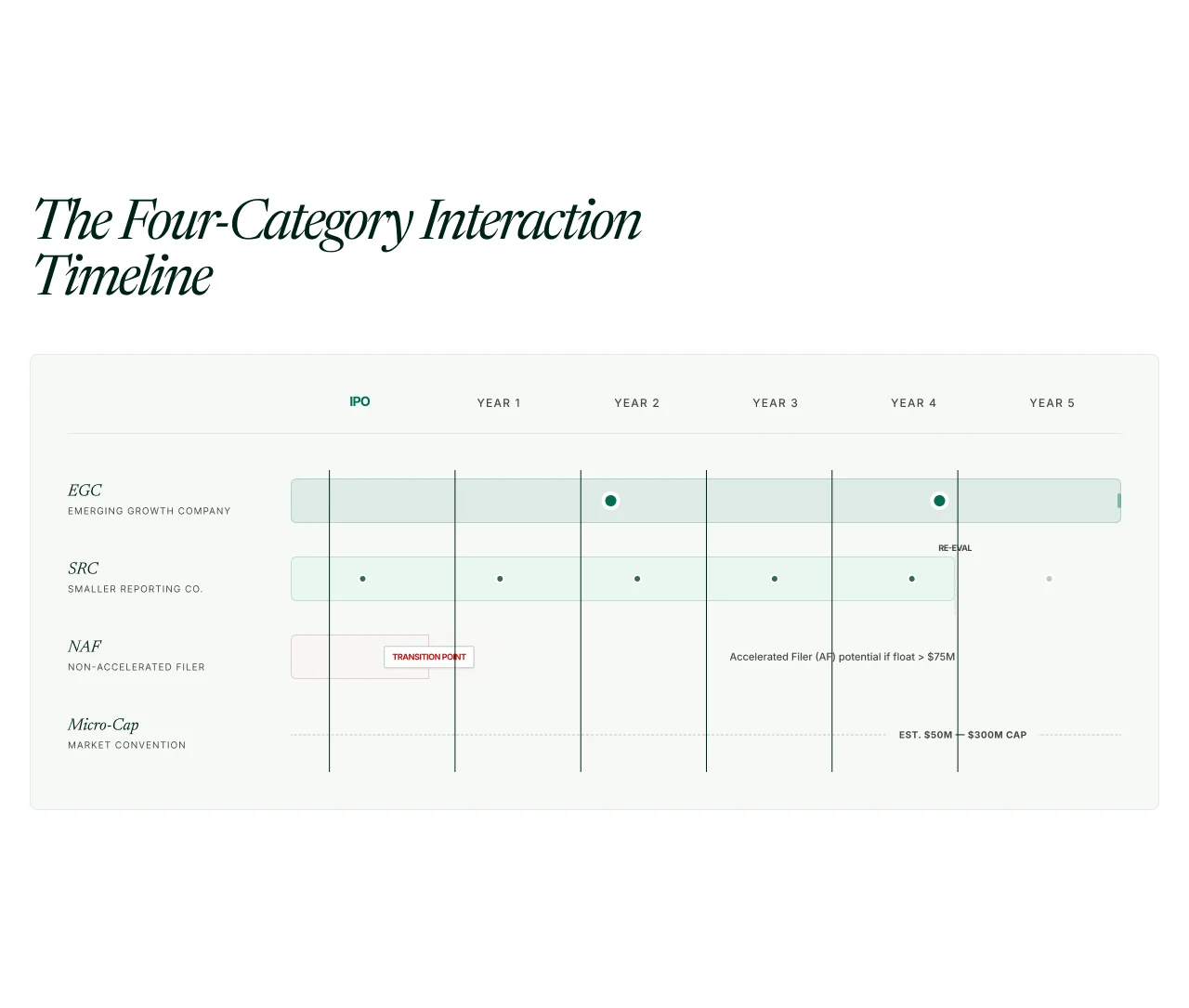

How Do the Four Categories Interact for a Typical Pre-IPO Company?

For a company conducting its IPO in 2026 with $80 million in annual revenue and an anticipated post-IPO public float of $150 million, the categorisation at the time of IPO and in the years immediately following looks like this.

At the time of IPO: The company qualifies as an EGC because its annual revenue is below $1.235 billion and it has not previously conducted a registered public offering of common equity. It is also an SRC because its revenue is below $100 million and its anticipated float is below $700 million. It is a NAF for its first year as a public company because it has not yet been subject to Exchange Act reporting for 12 months. All three regulatory categories apply simultaneously.

In Year 2: Assuming the float has grown to $150 million, the company is no longer a NAF. It has been subject to Exchange Act reporting for 12 months and its float exceeds $75 million, making it an accelerated filer. Its 10-K is now due 75 days after fiscal year-end rather than 90. It retains EGC status because its revenue has not crossed $1.235 billion and five years have not passed since IPO. It retains SRC status because its float is below $250 million. The company has moved from NAF to accelerated filer but is still both an EGC and an SRC.

In Year 5: If revenue has grown to $400 million and the float to $500 million, the company has lost SRC status on its annual measurement date because its float exceeds $250 million and its revenue exceeds $100 million. EGC status terminates at the end of the fiscal year following the fifth anniversary of the IPO. The company has also become an accelerated filer. What it is not is a large accelerated filer. Its float is below $700 million, so it is not subject to the SOX 404(b) auditor attestation yet.

This progression illustrates why the four categories cannot be tracked as a single status. A company can transition out of NAF status while retaining EGC and SRC status. It can lose SRC status while retaining EGC status. Each category has its own measurement date and its own termination trigger.

The SEC's May 19, 2026 proposed rule release 33-11419 (Public Company Reporting Framework) proposes to restructure the filer category system in a way that directly affects how NAF, SRC, and EGC interact.

The three proposed changes most relevant to a pre-IPO CFO are:

Raising the large accelerated filer threshold from $700 million to $2 billion. Under the proposal, a company with a public float below $2 billion would be a non-accelerated filer. This means the transition from NAF to accelerated filer under the current framework disappears for most mid-cap companies. The compliance cost differential between NAF and accelerated filer, principally the SOX 404(b) attestation, would be eliminated for all companies below $2 billion in float.

A guaranteed 60-month IPO on-ramp. Under the proposal, a new public company would not become a large accelerated filer for at least 60 months following its IPO regardless of float growth. Under the current EGC framework, a fast-growing company can lose EGC status within one to two years if its float crosses $700 million. The proposed 60-month floor removes that uncertainty and decouples the on-ramp duration from float performance.

These are proposals, not final rules. The comment period closes approximately July 20, 2026. Until final rules are published, companies should use the current thresholds for planning purposes. A company that incorrectly applies proposed thresholds as if they were in effect will either over-disclose or under-disclose relative to its current obligations.

The SRC definition is not changed by the May 2026 proposal. The current $250 million float test and $100 million revenue test for SRC qualification remain in place under the proposed framework.

Frequently Asked Questions

What is the difference between micro-cap and SRC?

Micro-cap is a market convention, not an SEC regulatory category. It refers to companies in a certain market capitalisation range, typically $50 million to $300 million, but has no precise or universal definition. SRC (Smaller Reporting Company) is an SEC-defined filer category under Exchange Act Rule 12b-2 that qualifies based on public float below $250 million or annual revenue below $100 million with a float below $700 million. A micro-cap company may or may not qualify as an SRC depending on its specific float and revenue.

Can a company be both an EGC and an SRC at the same time?

Yes. EGC and SRC are independent categories governed by different statutes and different metrics. An EGC qualifies based on annual gross revenues below $1.235 billion at IPO and loses status on four possible triggers. An SRC qualifies based on public float below $250 million or revenue below $100 million with float below $700 million, measured annually. A company that qualifies as both may generally use the more favourable accommodation for any given disclosure item.

What is the most important practical difference between EGC and NAF status?

EGC status provides IPO-specific accommodations including the DRS confidential review process, two years of audited financial statements in the registration statement, and the SOX 404(b) exemption during the EGC period. NAF status provides extended filing deadlines (90 days for 10-K, 45 days for 10-Q) and the SOX 404(b) exemption based on float, independent of EGC status. A company that has lost EGC status but still has a float below $75 million retains the 404(b) exemption as a NAF. A company with a $150 million float that has lost EGC status is an accelerated filer, is not a NAF, and is subject to 404(b).

When does a company transition from NAF to accelerated filer?

A company transitions to accelerated filer status when it has been subject to Exchange Act reporting for at least 12 calendar months, has filed at least one annual report, and has a public float of $75 million or more as of the last business day of its most recently completed second fiscal quarter. This typically occurs one year after the IPO date if the float has grown to or above $75 million.

How does EGC status terminate and what triggers should a pre-IPO CFO track?

EGC status terminates on the earliest of four events: total annual gross revenues of $1.235 billion or more at fiscal year-end; the fiscal year following the fifth anniversary of the IPO; issuance of more than $1 billion in non-convertible debt in the previous three years; or becoming a large accelerated filer by having a public float of $700 million or more after 12 months of Exchange Act reporting. A fast-growing company should track all four triggers, not only the revenue threshold.

Does the SEC's May 2026 proposal change the SRC definition?

No. The SEC's May 19, 2026 proposed rule release 33-11419 does not change the SRC definition. The $250 million public float test and the $100 million annual revenue test for SRC qualification remain in place under the proposed framework. What the proposal changes is the large accelerated filer threshold (from $700 million to $2 billion) and the IPO on-ramp structure (minimum 60 months). Comments on the proposal are due approximately July 20, 2026.

Key Takeaways

- Micro-cap is a market convention with no regulatory definition. It describes where a company sits in the market. SRC, EGC, and NAF are three separate SEC regulatory categories, each governed by a different statute, each measured on a different metric, and each applicable at a different point in a company's lifecycle.

- SRC (Smaller Reporting Company) is a perpetual disclosure-scaling category. It qualifies based on public float below $250 million or annual revenue below $100 million with float below $700 million, measured annually. It governs the content of what a company discloses, not when.

- EGC (Emerging Growth Company) is an IPO-specific time-limited on-ramp. It qualifies at IPO based on revenue below $1.235 billion and terminates on one of four triggers, the most common being the fifth fiscal year anniversary of the IPO or becoming a large accelerated filer. It governs both pre-IPO process accommodations (DRS, two-year financials) and post-IPO disclosure accommodations.

- NAF (Non-Accelerated Filer) is a filing-deadline and SOX 404(b) category. It qualifies based on public float below $75 million or being in the first 12 months of Exchange Act reporting. It governs when you file and whether external auditor ICFR attestation is required, not what you disclose.

- A company can simultaneously be a micro-cap (market convention), an EGC, an SRC, and a NAF. Each category has its own measurement date and termination trigger. Tracking all four independently is the Controller's responsibility from the IPO date forward.

- The SEC's May 2026 proposal would raise the large accelerated filer threshold to $2 billion and provide a guaranteed 60-month IPO on-ramp. It does not change the SRC definition. Until final rules are published, current thresholds govern. Comments close approximately July 20, 2026.