On May 19, 2026, the SEC proposed two rulemakings simultaneously. The first, Release No. 33-11418, addresses registered offering reform. The second, Release No. 33-11419, addresses filer status and Emerging Growth Company accommodations reform. Both proposals are open for public comment for 60 days following publication in the Federal Register. Based on the May 19 announcement, comments are due approximately July 20, 2026.

Neither proposal is a final rule. The thresholds and conditions described in this post are proposed. Final rules, if adopted, would follow a notice-and-comment process that could take 12 to 24 months and could differ materially from the proposals.

That said, both proposals are specific enough to evaluate against your company's current situation right now. This post maps what each proposal would change, which companies are affected, and what the operational effect would be, in the sequence a CFO or compliance team encounters the questions.

What Is the SEC Proposing in the Registered Offering Reform (Release 33-11418)?

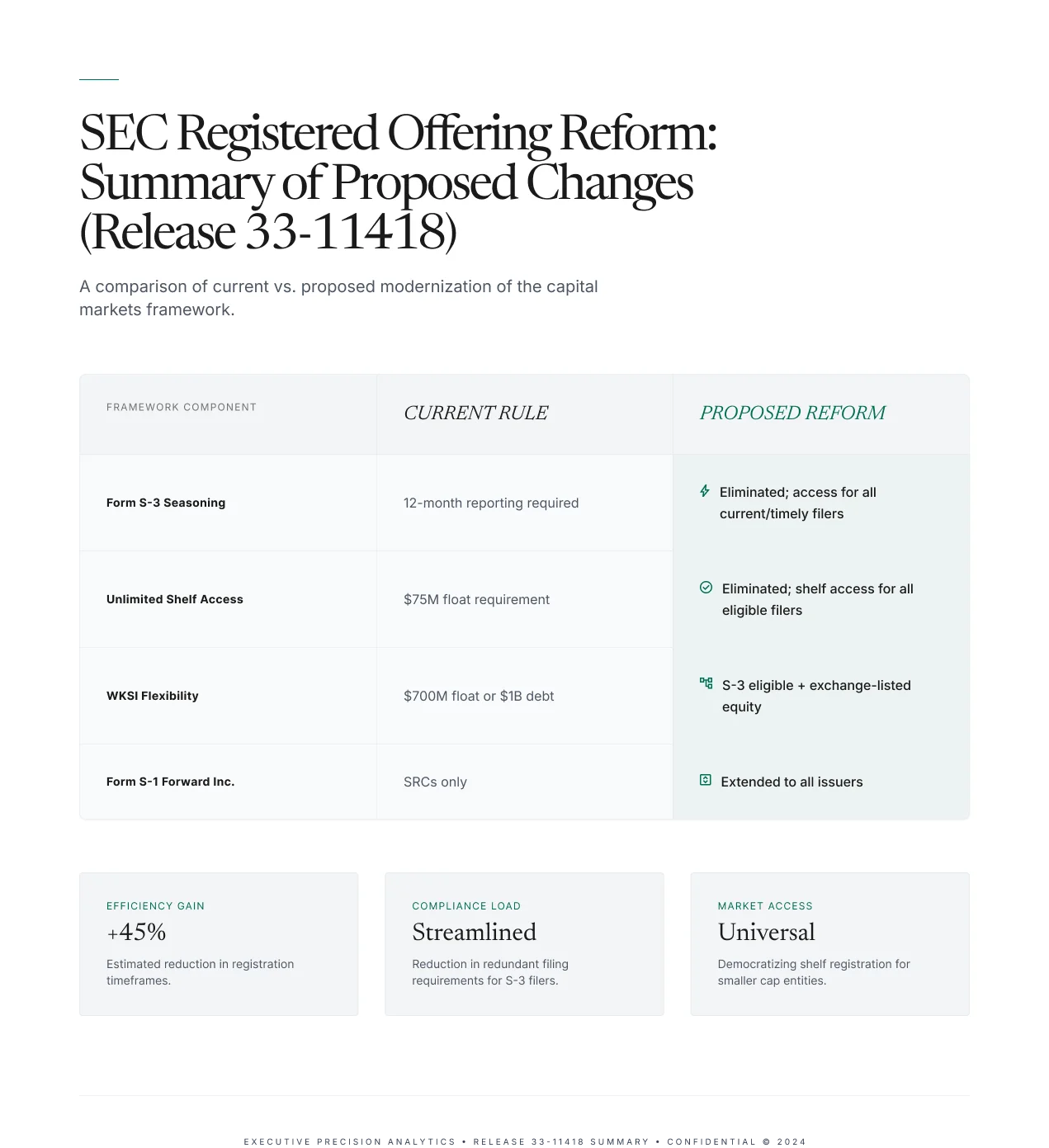

Release No. 33-11418 proposes the most significant modernisation of the registered offering framework in more than 20 years. It addresses four distinct elements of how public companies access the registered capital markets.

Form S-3 eligibility: removing the 12-month seasoning requirement and the $75 million public float requirement.

Under current rules, Form S-3 requires that a company have been subject to Exchange Act reporting requirements for at least 12 months before using the form. It also requires that companies registering an unlimited amount of securities have at least $75 million in public float. Form S-3's significance is that it enables shelf registration, which allows companies to register securities in advance and draw them down quickly when market conditions are favourable, rather than filing a new registration statement for each offering.

The proposed amendments would remove both of these requirements. A company that has been current and timely in its Exchange Act reporting for any period would be eligible to use Form S-3 for a shelf offering, without the 12-month waiting period. The $75 million public float requirement for unlimited registration would be eliminated entirely. According to the fact sheet for Release 33-11418, under the proposed amendments there could be an increase of over 60% in the number of issuers eligible to offer an unlimited amount of securities on Form S-3.

Form S-3 would continue to require that issuers be current and timely in their Exchange Act reporting. Certain ineligible issuers would still be prohibited from using the form.

WKSI qualification: extending enhanced registration benefits to a broader population.

Currently, the most expansive registration and communication flexibility (including automatic shelf registration, free-writing prospectuses with fewer restrictions, and the ability to conduct certain communications before filing) is reserved for Well-Known Seasoned Issuers (WKSIs). To qualify as a WKSI, a company must have at least $700 million in public float or have issued at least $1 billion of non-convertible securities in registered offerings in the prior three years.

The proposed amendments would eliminate both of those metrics as qualifying conditions for the enhanced registration and communication benefits, with one exception: the automatic shelf registration statement itself would still require 12 months of Exchange Act reporting. Instead, issuers would qualify for these enhanced benefits if they are eligible to use Form S-3 and have at least one class of common equity securities listed on a national securities exchange.

According to the fact sheet, under the proposed amendments there could be an increase of over 200% in the number of issuers eligible for all of the enhanced registration and communication benefits. This means companies with floats far below $700 million could access registration and communication flexibility currently available only to the largest public companies.

State Blue Sky preemption for all registered offerings.

Under current rules, federal preemption of state securities law registration and qualification requirements applies to registered offerings where the securities are listed or approved for listing on a national securities exchange. It does not apply to registered offerings of unlisted securities. Companies offering unlisted securities in registered offerings must comply with each state's separate registration or qualification requirements, which adds cost and complexity to multi-state offerings.

The proposed amendments would extend federal preemption to all registered offerings by defining "qualified purchaser" under Section 18(b)(3) of the Securities Act to cover all registered offering purchasers. This would eliminate the cost of complying with state-by-state registration requirements for registered offerings of unlisted securities.

Form S-1 modernisation: forward incorporation by reference extended beyond SRCs.

Currently, the ability to incorporate information by reference into a Form S-1 filed after the registration statement's effective date (forward incorporation) is limited to issuers that are Smaller Reporting Companies. Non-SRC issuers using Form S-1 must file post-effective amendments for each update rather than incorporating periodic reports by reference.

The proposed amendments would extend forward incorporation by reference on Form S-1 to all issuers, regardless of SRC status. The fact sheet states there could be an increase of up to 106% in the number of issuers eligible to forward incorporate on Form S-1. This change reduces the administrative burden of maintaining a Form S-1 registration statement on an ongoing basis for companies that do not qualify as SRCs.

Release No. 33-11419 proposes to restructure the public company filer category system and extend disclosure scaling accommodations to a substantially larger proportion of public companies. The proposal contains three substantive changes.

Raise the large accelerated filer threshold from $700 million to $2 billion.

Under current rules, a company with $700 million or more in public float is a large accelerated filer. This status triggers the shortest permitted filing deadlines (60 days for the 10-K, 40 days for the 10-Q), the requirement to obtain an external auditor attestation on internal control over financial reporting under SOX Section 404(b), and the full set of Regulation S-K disclosure obligations including pay-versus-performance and CEO pay ratio.

The proposal would raise the threshold to $2 billion. Every public company with a float below $2 billion would be categorised as a non-accelerated filer and would retain access to scaled disclosure accommodations. According to the SEC's May 19 press release, the proposed amendments would extend disclosure scaling and other accommodations to approximately 81% of all current public companies.

A mandatory five-year IPO on-ramp regardless of company size.

Under the current EGC framework, new public companies receive scaled disclosure accommodations for up to five years following their IPO, but EGC status terminates early if the company's public float crosses $700 million. A fast-growing technology company can lose EGC accommodations within one to two years of its IPO.

The proposed amendments would establish a mandatory minimum 60-month period before any new public company can become a large accelerated filer, regardless of how quickly its float grows. This provides a predictable five-year period of scaled accommodations for all new public companies and removes the uncertainty that currently affects rapidly growing companies approaching the $700 million float threshold.

A new Small Non-Accelerated Filer subcategory with extended filing deadlines.

The proposal establishes a new subcategory of small non-accelerated filers, defined as the smallest 18% of public companies by total assets (specifically those with $35 million or less in total assets), that would receive an additional 30 days to file their Form 10-K annual reports and an additional five days to file their Form 10-Q quarterly reports compared to the standard non-accelerated filer deadlines.

The proposal also extends the ICFR auditor attestation exemption under SOX Section 404(b) to all non-accelerated filers. Under current rules, the 404(b) exemption applies to non-accelerated filers and to SRCs with less than $100 million in annual revenues. Under the proposal, if the large accelerated filer threshold moves to $2 billion, the SOX 404(b) exemption applies to every public company below that threshold.

Which Companies Are Most Directly Affected by the Registered Offering Reform?

The registered offering reform proposal affects three distinct groups of public companies in materially different ways.

Companies with floats between $75 million and $700 million that currently cannot access Form S-3 for unlimited shelf registration. These companies currently must register each offering separately on Form S-1, which is slower and more expensive than a shelf registration. Under the proposal, these companies gain shelf registration access without the $75 million float floor, allowing them to register securities in advance and draw them down when market conditions are favourable.

Companies with floats below $700 million that are excluded from WKSI benefits. These companies currently cannot use automatic shelf registration, cannot distribute free-writing prospectuses with the same flexibility as large issuers, and face more communication restrictions in the offering process. Under the proposal, companies eligible for Form S-3 with an exchange-listed class of equity securities gain access to most of these benefits without the $700 million float requirement.

Companies conducting registered offerings of unlisted securities that currently must comply with state Blue Sky requirements. These companies face the cost and administrative burden of multi-state securities law compliance for each offering. Under the proposal, federal preemption extends to all registered offerings, eliminating state-level registration and qualification costs.

For most of these companies, the practical effect of the registered offering reform is faster and cheaper access to capital. A company that currently needs six to eight weeks to complete a registered offering on Form S-1 can complete a shelf takedown on Form S-3 in days once an effective shelf is on file.

Which Companies Are Most Directly Affected by the Filer Status Reform?

The filer status reform proposal's most significant impact concentrates in two groups.

Companies with public floats between $700 million and $2 billion that are currently large accelerated filers.

These companies currently pay for an external SOX 404(b) auditor attestation, prepare pay-versus-performance tables and CEO pay ratio disclosures, and file on the shortest permitted deadlines. Under the proposal, they would be reclassified as non-accelerated filers. The SOX 404(b) attestation, which costs $500,000 to $2 million or more annually depending on company complexity, would no longer be required. The pay-versus-performance table and CEO pay ratio would be scaled or eliminated. Filing deadlines would extend from 60 to 90 days for the 10-K and from 40 to 45 days for the 10-Q.

New public companies that currently risk losing EGC accommodations quickly after their IPO.

Under the current framework, a company that goes public and grows rapidly, such as a technology company whose float crosses $700 million within 18 months of its IPO, can lose EGC accommodations before it has fully built the compliance infrastructure of a large public company. The proposed 60-month floor removes this risk and gives every new public company a predictable period to build its reporting function before facing the full large accelerated filer disclosure and audit burden.

What Does the SPAC-IPO Equivalence Provision in the Registered Offering Reform Mean?

The registered offering reform proposal contains a provision specifically addressing SPAC transactions. As part of the broader expansion of Form S-3 eligibility and shelf registration access, the proposal treats de-SPAC transactions consistently with the expanded framework for IPO-equivalent transactions.

This is consistent with the March 2025 Corp Fin DRS expansion, which treated de-SPAC registration statements as the functional equivalent of an IPO for purposes of nonpublic draft review eligibility. The May 2026 registered offering reform proposal extends that equivalence principle to the registered offering framework, giving de-SPAC target companies access to the same registration flexibility that would be available to a company conducting a traditional IPO under the proposed rules.

For practitioners advising SPAC targets, this provision is relevant to how the S-4 or proxy is structured and what flexibility exists in the registration process. It does not alter the underlying 2024 SPAC disclosure and liability requirements, which remain in effect.

What Should a Small Issuer Do Before the Comment Period Closes on July 20, 2026?

The comment period on both proposals closes approximately July 20, 2026. Three actions are worth taking before that date.

Assess which proposals affect your company's current capital markets programme. For the registered offering reform: determine whether your company currently qualifies for Form S-3 shelf registration and, if not, whether the proposed removal of the 12-month seasoning and $75 million float requirements would make you eligible. Calculate the cost differential between your current S-1 offering process and the shelf registration process you would gain access to under the proposal.

Assess which filer status proposals affect your company's current disclosure and audit obligations. Calculate your most recent public float measurement against the proposed $2 billion large accelerated filer threshold. If your float is below $2 billion, determine what your SOX 404(b) attestation costs annually, and identify which Regulation S-K disclosure items (pay-versus-performance, CEO pay ratio, and executive compensation narrative) would change under non-accelerated filer scaled accommodations.

Submit a comment letter if the proposals materially affect your company. The SEC's public comment process is the formal mechanism through which companies influence whether and how proposed rules are adopted. Comments are submitted through the SEC's online comment system at sec.gov and become part of the public rulemaking record. For companies that would materially benefit or be adversely affected by specific thresholds or conditions in either proposal, a comment letter describing the company's specific experience is the appropriate form of engagement.

The key reminder at this stage is that neither proposal is a final rule. Companies should not restructure their offering programmes or compliance frameworks around these thresholds until final rules are published. The proposals may change materially based on comment feedback.

Frequently Asked Questions

What does the SEC's registered offering reform proposal change about Form S-3?

The proposed amendments to Form S-3 would remove the requirement that issuers be subject to Exchange Act reporting for 12 months before using the form, and would eliminate the requirement that issuers have at least $75 million in public float to register an unlimited amount of securities. Form S-3 would still require that issuers be current and timely in their Exchange Act reporting. The fact sheet for Release 33-11418 states there could be an increase of over 60% in the number of issuers eligible to offer an unlimited amount of securities on Form S-3.

What is a WKSI and how does the proposal change who qualifies?

A Well-Known Seasoned Issuer (WKSI) currently must have at least $700 million in public float or have issued at least $1 billion in non-convertible securities in registered offerings in the prior three years. WKSIs benefit from automatic shelf registration and enhanced offering communication flexibility. The proposed amendments would extend most WKSI-equivalent benefits to any issuer eligible for Form S-3 with at least one class of exchange-listed common equity, without the $700 million float or $1 billion debt issuance requirement.

What is the proposed large accelerated filer threshold change and what does it affect?

The proposed filer status reform would raise the large accelerated filer threshold from $700 million to $2 billion in public float. Companies below $2 billion would be non-accelerated filers under the proposed framework. Non-accelerated filer status exempts companies from the SOX 404(b) external auditor attestation, provides scaled Regulation S-K disclosure accommodations including reduced executive compensation disclosure, and allows longer filing deadlines (90 days for 10-K, 45 days for 10-Q versus 60 and 40 days for large accelerated filers).

What is the proposed five-year IPO on-ramp and who does it protect?

The proposed five-year IPO on-ramp would prevent any new public company from becoming a large accelerated filer until at least 60 months after its IPO, regardless of how quickly its public float grows. Under the current EGC framework, a fast-growing company whose float crosses $700 million can lose scaled disclosure accommodations within one to two years of its IPO. The proposed 60-month floor removes that uncertainty and gives all new public companies a predictable compliance runway.

What is the new Small Non-Accelerated Filer subcategory?

The filer status proposal creates a new subcategory of small non-accelerated filers defined as the smallest 18% of public companies by total assets, specifically those with $35 million or less in total assets. This subcategory would receive an additional 30 days to file Form 10-K annual reports and an additional five days to file Form 10-Q quarterly reports compared to standard non-accelerated filer deadlines.

When does the comment period close and do these proposals affect my company?

The comment period on both proposals closes approximately July 20, 2026. To determine whether either proposal affects your company: for the registered offering reform, assess whether you currently qualify for Form S-3 shelf registration and what access to WKSI-equivalent benefits would mean for your capital markets programme. For the filer status reform, calculate your public float against the proposed $2 billion threshold and identify your current SOX 404(b) attestation cost and scaled disclosure obligations.

Key Takeaways

- The SEC's registered offering reform (Release 33-11418) would remove the 12-month seasoning requirement and the $75 million public float requirement for Form S-3 shelf registration, extend most WKSI-equivalent registration benefits to all Form S-3-eligible issuers with exchange-listed equity, preempt state Blue Sky requirements for all registered offerings, and extend forward incorporation by reference on Form S-1 beyond SRCs to all issuers.

- The filer status reform (Release 33-11419) would raise the large accelerated filer threshold from $700 million to $2 billion in public float, exempt all non-accelerated filers from the SOX 404(b) auditor attestation requirement, establish a mandatory minimum 60-month IPO on-ramp before any new public company becomes a large accelerated filer, and create a new Small Non-Accelerated Filer subcategory with extended filing deadlines.

- The registered offering reform fact sheet projects a 60% increase in Form S-3-eligible issuers, a 200% increase in issuers eligible for enhanced registration and communication benefits, and a 106% increase in issuers eligible to forward incorporate on Form S-1.

- The filer status reform would extend scaled disclosure accommodations to approximately 81% of all current public companies, up from the proportion currently qualifying under SRC and NAF categories.

- Neither proposal is a final rule. The comment period closes July 20, 2026. Final rules, if adopted, could differ materially from the proposed thresholds. Companies should not restructure their offering programmes or compliance frameworks around these thresholds until final rules are published.