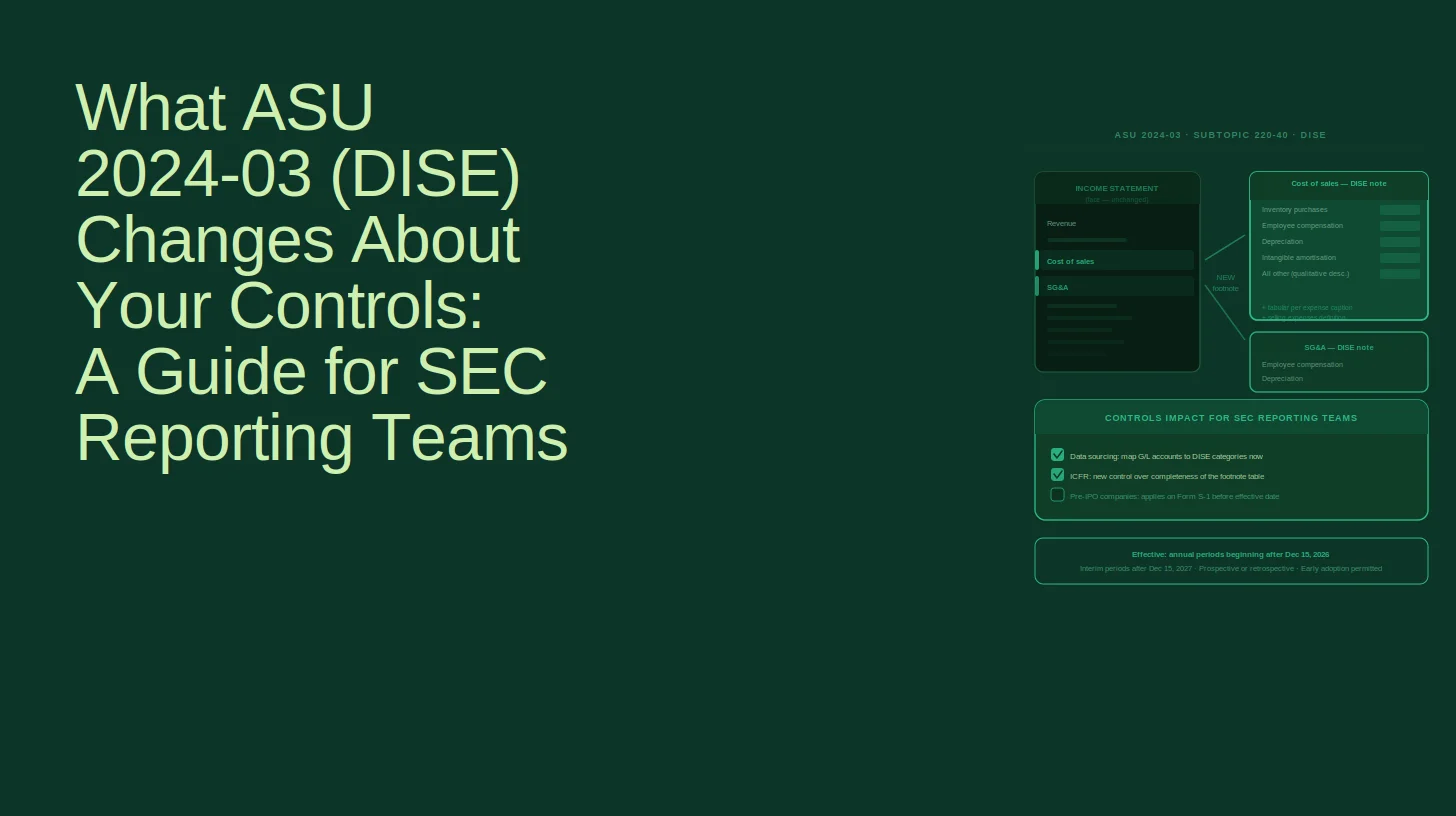

The FASB issued ASU 2024-03 on November 4, 2024. The standard adds ASC 220-40 to require public business entities to disclose, in a tabular footnote, the natural expense components of each relevant income statement caption. For calendar-year-end public companies, the first mandatory annual period is fiscal year 2027. Interim reporting follows one year later, beginning with periods starting after December 15, 2027.

The effective date is specific: ASU 2025-01, issued January 7, 2025, clarified the original ASU's effective date language to confirm that all public business entities must adopt in annual reporting periods beginning after December 15, 2026, not in an earlier interim period. For calendar-year-end companies, mandatory adoption begins with the December 31, 2027 annual report. Early adoption is permitted.

Most commentary on DISE has focused on what the disclosure looks like. This post focuses on what has to be true about your underlying data and controls before the disclosure can be produced accurately and consistently.

What Does ASU 2024-03 Actually Require and What Does It Leave Unchanged?

The face of the income statement does not change under DISE. The expense captions a company currently presents on the income statement — cost of goods sold, selling general and administrative expense, research and development, and whatever other captions the company uses — remain exactly as they are. ASU 2024-03 does not require new line items on the face of the income statement and does not change the recognition or measurement of any expense.

What changes is the footnote. The standard requires public business entities to disclose, in a tabular format in the notes to the financial statements, the amounts of specified natural expenses that are included within each relevant income statement expense caption at each interim and annual reporting period.

A relevant expense caption is any caption on the face of the income statement that contains any of the five required natural expense categories. If a company's SG&A caption includes any amount of employee compensation, depreciation, intangible asset amortization, purchases of inventory, or DD&A, SG&A is a relevant expense caption and must be disaggregated. For most companies, cost of goods sold, SG&A, and R&D will each be relevant expense captions. The disclosure obligation applies to each one independently.

The tabular disclosure for each relevant expense caption must show:

The amount of each of the five specified natural expense categories included in that caption.

The amounts of any other items required to be disclosed by other GAAP standards that are included in that caption and that are not already captured in the five natural categories.

The amount of remaining expenses within the caption that do not fall into any of the specified categories, described qualitatively as "other."

The total of the tabular disclosure must reconcile to the relevant expense caption on the face of the income statement.

In addition to the per-caption tabular disclosure, the standard requires separate disclosure of total selling expenses for the period. In annual periods, the company must also disclose its definition of selling expenses. DISE does not define selling expenses for the company; the company defines them, applies that definition consistently, and discloses it annually.

The FASB acknowledged in the Basis for Conclusions of ASU 2024-03 that producing the information necessary to comply may require detailed recordkeeping and that the process may be challenging for some entities. This acknowledgment is the most useful framing of what the standard actually demands: it is not a disclosure design challenge. It is a data capture challenge.

What Are the Five Required Natural Expense Categories and Where Do Companies Typically Have Data Gaps?

The five natural expense categories that must be disclosed within each relevant expense caption are defined precisely in ASC 220-40. Understanding each definition and the data it requires is the prerequisite for assessing whether your current chart-of-accounts and system configuration can produce the disclosure.

Category 1: Purchases of inventory. This category includes only amounts within the scope of ASC 330 (and applicable industry-specific inventory guidance). It covers costs associated with acquiring inventory that will be expensed through cost of goods sold or cost of revenues. It does not include all materials costs — specifically, materials purchased under over-time contracts recognised as cost of revenues under ASC 606 and ASC 340-40 are not purchases of inventory under DISE. This distinction creates a data gap in companies with a mix of inventory-based and contract-based cost structures, including manufacturing, aerospace and defence, and construction companies. The Deloitte analysis of this issue confirms that the line between ASC 330 inventory costs and ASC 340-40 contract costs requires careful mapping before the disclosure can be produced.

Category 2: Employee compensation. This category includes wages, salaries, bonuses, benefits, stock-based compensation, and other amounts paid or accrued as compensation to employees. The ASU requires separate disclosure of one-time employee termination benefits within this category if applicable. The data gap here is most common in companies where payroll systems, stock compensation systems, and benefits systems feed expense in ways that do not align with the income statement caption structure. Employee compensation that flows into cost of goods sold, SG&A, and R&D simultaneously must be captured and attributed to each caption separately. Many companies currently aggregate total compensation expense without clean attribution to income statement captions at the natural expense level.

Category 3: Depreciation. This category includes charges for the allocation of the cost of tangible assets over their useful lives. It includes amortisation of right-of-use assets and lease incentives under ASC 842. The data gap is most common in companies where depreciation is allocated across multiple expense captions through allocations that are not captured at the source ledger level. If depreciation is allocated from a fixed asset subledger to multiple cost centres and then rolled up into multiple income statement captions through an allocation methodology, the DISE disclosure requires that the depreciation amount within each relevant caption be traceable. That traceability is only possible if the allocation methodology is documented and the allocation outputs are retained at the caption level.

Category 4: Intangible asset amortisation. This category covers the amortisation of intangible assets recognised under ASC 350 and related guidance. The data gap is typically not in the identification of the amount but in the attribution to income statement captions. For companies that have completed acquisitions and carry significant intangible assets, amortisation may be presented in a single caption or allocated across multiple captions. The DISE disclosure requires the amortisation amount within each relevant caption to be separately identified and reported.

Category 5: Depreciation, depletion, and amortisation (DD&A) for oil and gas activities. This category is specific to extractive industries. For non-oil-and-gas companies, this category is not applicable, though the general depletion category extends to other types of depletion.

Why Is DISE an Evidence Problem Before It Is a Disclosure Problem?

The central implementation error that companies are making in their DISE preparation is treating it as a disclosure design exercise. They are working backward from the footnote template to the data. The correct approach is forward from the data to the disclosure.

The reason this matters is audit and consistency. The DISE table must reconcile to the income statement. Every number in the table must trace to a defined source. If the employee compensation amount in the SG&A disaggregation does not tie to a specific, documented, controlled source, the reconciliation will break under audit scrutiny in two directions: the auditor will test whether the amount is complete (all employee compensation in SG&A is captured), and the auditor will test whether it is accurate (no non-compensation amounts are included). A number produced from a spreadsheet lookup or a one-time calculation cannot survive that testing without a documented, repeatable methodology.

The FASB's own acknowledgment in the Basis for Conclusions — that producing the required information may require detailed recordkeeping — is a direct signal that the board understood the disclosure would expose data infrastructure weaknesses that pre-existing disclosures had not. DISE is the first US GAAP standard in several years to require natural expense category data at the income statement caption level simultaneously. Prior disclosures of depreciation (under ASC 360) and amortisation (under ASC 350) are total-period amounts; DISE requires them attributed to each relevant caption.

Three specific control infrastructure questions determine whether a company can produce the DISE disclosure from existing data or needs to build new controls.

Question 1: Does the chart of accounts capture natural expense categories at the point of entry? If employee compensation costs are coded to a single compensation account and then allocated across cost centres and income statement captions through a period-end allocation, the DISE disclosure requires either that the allocation methodology is sufficiently granular to produce caption-level attribution, or that the chart of accounts is restructured to capture the natural expense category at the point of entry. For most companies, the latter is more reliable.

Question 2: Do the allocation methodologies produce caption-level output that is auditable? Many companies use headcount-based or revenue-based allocation keys to distribute shared costs across business units and income statement captions. These allocations may be appropriate for financial reporting purposes, but if the allocation output is not retained at the caption level with the allocation key and the base data documented, the DISE disclosure cannot be reconciled back to source. The allocation must be a controlled process with documented output, not an ad hoc calculation.

Question 3: Are the source system extracts from which the DISE amounts are drawn subject to IT general controls? The PCAOB's AS 1105 amendments effective December 15, 2025 require auditors to evaluate the reliability of electronic data used as audit evidence. For external auditors testing the DISE table, this means evaluating the IT general controls over the systems producing the payroll extract, the fixed asset subledger report, and the intangible asset amortisation schedule. ITGC weaknesses in those source systems create a DISE audit risk that is independent of whether the disclosure itself looks correct.

What Changes in the Close Process to Support DISE?

DISE is an interim and annual requirement for calendar-year companies beginning with periods in fiscal 2028 (annual 2027, then interim Q1 2028 onward). This means the close process must produce the DISE table data consistently at every interim period close, not just at year-end.

Three close process changes are typically necessary.

Change 1: Add a DISE data collection step to the close checklist. At each period close, the relevant systems must produce defined outputs: the payroll system produces a compensation expense by caption report, the fixed asset subledger produces a depreciation expense by caption report, the intangible asset schedule produces an amortisation expense by caption. Each output must reconcile to the general ledger before the period is closed. This is not a year-end exercise; it is a monthly or quarterly control that must operate with the same reliability as the account reconciliation process.

Change 2: Document and control the selling expenses definition. The DISE standard requires disclosure of the company's definition of selling expenses in each annual period. The definition must be established before fiscal 2027 begins, documented in the accounting policies, and applied consistently. If the company's current chart of accounts does not produce a clean selling expenses total — for example, because selling costs are embedded in SG&A without a separate functional classification — the chart of accounts must be restructured or the definition must be built around an allocation methodology that is documented and controlled.

Change 3: Build the DISE reconciliation into the disclosure control environment. The DISE table, once produced, must reconcile to the income statement. This reconciliation should be a designed control in the disclosure controls and procedures framework, not an ad hoc check performed by the preparer. The disclosure committee's review of the DISE table should include a documented review of the reconciliation, confirmation that each natural expense amount ties to a defined source, and confirmation that the "other" qualitative description is consistent with what is not captured quantitatively.

What Does the DISE Footnote Table Need to Look Like to Satisfy the Standard?

The DISE footnote is a tabular disclosure. The structure is defined by ASC 220-40, with implementation examples provided in ASC 220-40-55-3 through 55-25 for a manufacturer, a services provider, and a bank.

Each relevant expense caption gets its own column or section in the table. For a company with cost of goods sold, SG&A, and R&D as relevant captions, the table has three sections. Within each section, the rows are the natural expense categories present in that caption, any other GAAP-required disclosures included in that caption, and an "other" row for the remainder with a qualitative description.

The total of all rows within each caption section must equal the amount of that caption on the income statement face. This is the reconciliation requirement. If the table does not tie, the disclosure is deficient. Because the table appears in the footnotes of an SEC filing, any discrepancy between the table total and the income statement caption is an error that will be identified either in EDGAR inline XBRL review or in an SEC comment letter.

The table must include a qualitative description of amounts included in the "other" row that are not disaggregated quantitatively. This qualitative description is not a catchall. The FASB expects that it will describe specific types of expenses, not generic language like "other expenses not captured above." The description should be specific enough that an investor can understand what types of costs are aggregated in the remainder.

Early adoption data from companies that have voluntarily adopted DISE before the mandatory effective date will begin appearing on EDGAR in fiscal 2026 and 2027 annual reports. Reviewing those early adopter filings on EDGAR is the most direct source of disclosure format benchmarking available to SEC Reporting Leads preparing their own first-time DISE disclosure.

The DISE table is also subject to Inline XBRL tagging under the same requirements that apply to other footnote disclosures in Form 10-K and Form 10-Q. The XBRL taxonomy for DISE data elements will need to be confirmed and mapped in the company's XBRL tagging process before the first mandatory filing.

Frequently Asked Questions

What is ASU 2024-03 DISE and when is it effective?

ASU 2024-03, Disaggregation of Income Statement Expenses (DISE), adds ASC 220-40 to require public business entities to disclose, in a tabular footnote, the natural expense components of each relevant income statement caption. As clarified by ASU 2025-01, the mandatory effective date for all public business entities is annual reporting periods beginning after December 15, 2026. For calendar-year-end companies, mandatory adoption begins with the December 31, 2027 annual report. Interim periods follow one year later. Early adoption is permitted.

What are the five required natural expense categories under DISE?

The five required categories are: purchases of inventory (within the scope of ASC 330), employee compensation, depreciation (including right-of-use asset amortisation under ASC 842), intangible asset amortisation (under ASC 350), and depreciation, depletion, and amortisation for oil-and-gas producing activities or other depletion. Every relevant income statement caption must be disaggregated into these categories to the extent each is present in that caption.

What makes an income statement caption a relevant expense caption under DISE?

A caption is relevant if it contains any amount that falls within any of the five natural expense categories. Most companies will find that cost of goods sold, SG&A, and R&D are all relevant captions. If a caption is entirely composed of a single natural expense category already presented separately on the face of the income statement, it does not require further disaggregation.

Does DISE change the face of the income statement?

No. ASU 2024-03 does not change the expense captions presented on the face of the income statement. It does not change the recognition or measurement of any expense. What changes is the footnote: a tabular disclosure of the natural expense components of each relevant caption is required at each interim and annual period.

What is the selling expenses disclosure requirement under DISE?

Entities must disclose the total amount of selling expenses for the period in both annual and interim reports. In annual reports only, entities must also disclose their definition of selling expenses. DISE does not define selling expenses; the company defines them, applies the definition consistently, and discloses it annually. Companies that do not currently track a clean selling expenses total will need to establish a definition and build the data infrastructure to support it before fiscal 2027.

What control changes does DISE require?

DISE requires three categories of control change: the chart of accounts must capture natural expense categories at the caption level (or the allocation methodology must produce auditable caption-level output), the close process must include a DISE data collection and reconciliation step at each interim period, and the selling expenses definition must be documented, controlled, and consistently applied. The DISE table must also be incorporated into the disclosure controls and procedures framework as a designed control with a documented reconciliation review.

How does DISE interact with PCAOB AS 1105 and external audit?

The AS 1105 amendments effective December 15, 2025 require external auditors to evaluate the reliability of electronic data used as audit evidence. For DISE, this means auditors will evaluate the IT general controls over the payroll system, fixed asset subledger, and intangible asset schedule that produce the source data for the DISE table. ITGC weaknesses in those systems create a DISE audit risk independent of whether the disclosure looks correct. Companies should assess ITGC coverage for all DISE data source systems before the first mandatory filing.

Key Takeaways

- ASU 2024-03 (DISE) is effective for annual reporting periods beginning after December 15, 2026, and interim periods beginning after December 15, 2027, as clarified by ASU 2025-01. For calendar-year companies, mandatory annual adoption is the December 31, 2027 Form 10-K.

- The face of the income statement does not change. DISE requires a tabular footnote disclosure of the natural expense components of each relevant income statement caption. The table must reconcile to the caption total on the income statement face.

- The five required natural expense categories are: purchases of inventory (ASC 330 scope only), employee compensation, depreciation (including ROU asset amortisation), intangible asset amortisation, and DD&A for oil and gas or other depletion. Each relevant caption must be disaggregated into these categories to the extent present.

- DISE is an evidence-gathering problem before it is a disclosure-drafting problem. The number in the DISE table must tie to a defined, controlled, auditable source. A table built from a spreadsheet lookup or a one-time calculation will not survive auditor testing for completeness and accuracy.

- Three control infrastructure questions determine readiness: does the chart of accounts capture natural expense categories at the caption level? Do the allocation methodologies produce caption-level output that is documented and auditable? Are the source systems subject to IT general controls that will satisfy PCAOB AS 1105 data reliability requirements?

- The close process must add a DISE data collection and reconciliation step at each interim period. The selling expenses definition must be established, documented, and applied before fiscal 2027 begins.

- Early adopter DISE disclosures will begin appearing on EDGAR in fiscal 2026 and 2027 annual reports. Reviewing those filings is the most direct source of footnote format benchmarking available before mandatory adoption.