SEC FY 2026-2030 Draft Strategic Plan: Filing and Compliance Implications for Registrants

The SEC published its Draft Strategic Plan for FY 2026-2030 on June 2, 2026, opening a 30-day public comment window that closes July 2, 2026. For CFOs, IR teams, ESG officers, and compliance professionals, this is not a background document. It is the agency's five-year operating blueprint, and it signals where SEC staff will focus examination resources, which rules are likely to be revisited, and how enforcement priorities will shift through 2030.

The generic coverage summarises the three goals and moves on. This article does something different: it translates each goal into concrete filing and compliance implications, maps the plan against the Gensler-era FY 2022-2026 plan, and gives you a practical guide to submitting a comment that actually shapes the final document.

Key takeaway: The comment deadline is July 2, 2026. If your company wants to influence the SEC's five-year regulatory direction, you have days, not weeks, to act.

What Are the Three Goals in the SEC's FY 2026-2030 Draft Strategic Plan?

The Atkins plan organises the SEC's work around three goals that represent a sharp philosophical break from the Gensler era. Each goal carries sub-objectives that translate directly into rulemaking signals, examination priorities, and disclosure expectations for registrants.

Goal 1: Renew regulatory policy to support innovation, capital formation, market efficiency, and investor protection. Sub-objectives include modernising and simplifying disclosure practices, expanding access to private markets, enabling new capital-raising pathways, and providing a "rational, coherent, and principled" regulatory foundation for digital assets and distributed ledger technologies.

Goal 2: Shift regulatory practices to increase stakeholder engagement, facilitate compliance, and return enforcement to Congress's original intent. This explicitly repudiates "regulation by enforcement" and commits to policing only established violations such as fraud and manipulation. It also calls for periodic retrospective reviews of existing rules and an assessment of the agency's administrative law framework.

Goal 3: Optimise operational efficiency through technology modernisation, EDGAR overhaul, AI and blockchain adoption, and reformed performance management.

Chairman Paul S. Atkins framed the plan directly: "I encourage market participants and the general public to provide comment on best practices to ensure our regulatory framework upholds the United States as the best and most secure place to do business."

Atkins Plan vs. Gensler Plan: A Side-by-Side Comparison

The plan's deregulatory pivot becomes clearest when you put the two plans next to each other. The statutory basis is identical (the Government Performance and Results Modernization Act of 2010), but the priorities have moved substantially.

DimensionGensler FY 2022-2026Atkins FY 2026-2030Goal 1 focusProtect working families against fraud, manipulation, and misconductRenew regulatory policy for innovation, capital formation, market efficiency, and investor protectionGoal 2 focusDevelop a robust regulatory framework keeping pace with evolving marketsShift to stakeholder engagement, compliance facilitation, and enforcement limited to fraud/manipulationGoal 3 focusSupport a skilled, diverse, equitable, and inclusive workforceOptimise operational efficiency through technology modernisation and performance accountabilityDisclosure directionExpand disclosures for consistency, comparability, and materiality (ESG/climate framing)Simplify and modernise disclosures; reduce reporting burdensEnforcement philosophyActive rulemaking agenda; enforcement used to establish standards in novel areasEnforcement limited to established law; no "regulation by enforcement"Digital assetsAddressed through enforcement actions and ad hoc guidanceExplicit commitment to a principled regulatory framework; Crypto Task Force formalisedDEI/ESG workforce goalsExplicit DEI workforce objectiveAbsent from the planPrivate marketsLimited focusExplicit expansion of private-market access and new capital-raising pathwaysEDGAR/technologyTechnology modernisation mentionedEDGAR named as a legacy system requiring comprehensive review

The Gensler-era plan oversaw an SEC that selectively reviewed disclosures of approximately 5,248 exchange-listed public companies with aggregate market capitalisation of $51 trillion, operating in markets with annual equity trading of roughly $118 trillion. The Atkins plan governs the same scale of markets but with a fundamentally different theory of what the agency should do within them.

What Does 'Modernising and Simplifying Disclosure' Mean for Your 10-K and 10-Q?

Disclosure simplification is Goal 1's most immediate implication for public company finance teams, and the SEC has already started acting on it.

The plan's language frames disclosure reform as reducing burden, not expanding it. In practice, several proposals already in flight reflect this direction:

- Semiannual reporting: In May 2026, the SEC proposed letting domestic issuers replace three Form 10-Qs with a new semiannual Form 10-S. See Finrep's detailed analysis of the Form 10-S vs. 10-Q decision.

- Regulation S-K overhaul: In January 2026, the SEC launched a comprehensive review of Reg S-K and requested public comment on refocusing disclosure on material information.

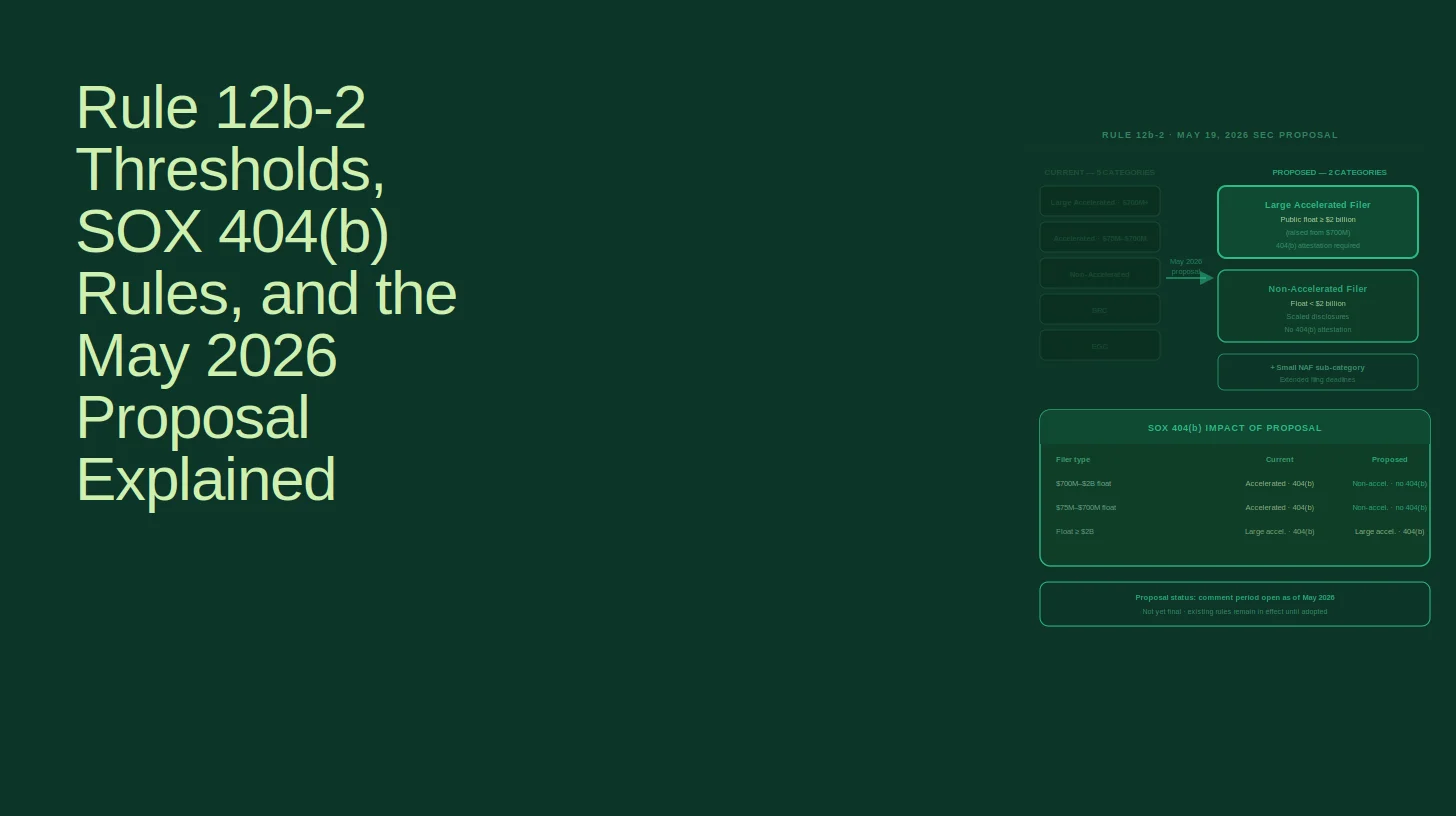

- Filer status reform: In May 2026, the SEC proposed collapsing five filer categories into two and raising the large accelerated filer threshold from $700 million to $2 billion. Finrep's breakdown of how this affects mid-caps covers the SOX 404(b) implications.

- Registered offering reform: Also in May 2026, the SEC proposed broadening Form S-3 shelf eligibility and modernising Form S-1.

The strategic plan does not itself change any rule. But it tells you which direction the rulemaking train is heading. Finance teams that have been building disclosure infrastructure around Gensler-era expansion should expect the next five years to run in the opposite direction.

Practical implication: Do not pre-emptively strip disclosures from current filings based on the plan alone. Wait for final rules. But do flag the pending Reg S-K review and semiannual reporting proposal to your audit committee now, because both have comment periods that overlap with this one.

Does the Plan Signal a Rollback of ESG and Climate Disclosure Requirements?

Yes, and the rollback is already underway through separate rulemaking, not just through the strategic plan's tone.

The Atkins plan conspicuously omits the Gensler-era language around ESG-specific disclosure expansion and DEI workforce goals. More concretely, the SEC voted 3-2 on May 29, 2026 to propose rescinding its 2024 climate disclosure rules in their entirety, with a comment period closing August 3, 2026. Finrep's analysis of what the climate rule rescission means for registrants covers the immediate compliance posture.

For ESG teams, the strategic plan's silence on sustainability reporting is itself a signal. The plan's enforcement goal, which limits SEC action to fraud and manipulation, also reduces the risk that voluntary ESG disclosures will be second-guessed through novel enforcement theories. That said, existing rules, including the cybersecurity disclosure rule adopted in 2023, remain in force until formally rescinded. The plan's retrospective review objective (discussed below) is the mechanism through which those rules could be revisited.

KPMG's Q4 2025 Directors Quarterly flagged "leadership changes at the SEC and PCAOB" and "the SEC's regulatory agenda" as key audit committee watch items, noting that "the third quarter of 2025 has seen clarity begin to emerge as multiple sustainability reporting proposals take shape." The Atkins strategic plan is the formal culmination of that shift.

What Does the Digital Asset Objective Mean for Crypto Disclosures?

The plan commits to a "rational, coherent, and principled" regulatory framework for digital assets, formalising the work of the SEC's Crypto Task Force into the agency's five-year governing document.

For companies with crypto treasury holdings, tokenised securities, or digital asset business lines, this matters in two ways:

- Reduced enforcement risk from novel theories. The Gensler-era practice of using enforcement actions to define the boundaries of securities law for crypto assets is explicitly repudiated. The plan commits to clarifying those boundaries through rulemaking and guidance, not ad hoc actions.

- New disclosure frameworks are coming. The plan's sub-objectives include resolving jurisdictional questions between the SEC and the CFTC and enabling compliant capital formation through tokenised offerings. Companies currently disclosing digital asset risks under general risk factor and MD&A frameworks should expect more specific guidance, but not immediately.

One important clarification: the plan's AI and blockchain modernisation objective under Goal 3 refers to the SEC's internal operations, not a mandate for registrant AI disclosures. Finance teams should not read the plan as creating new AI-related disclosure obligations. The SEC's internal use of AI to improve oversight is distinct from any future rulemaking on AI risk disclosure by registrants.

What Does 'Expanding Access to Private Markets' Mean for IPO Candidates?

The plan's private markets language signals a more permissive regulatory environment for capital formation through 2030, building on proposals already in motion.

Specific sub-objectives include modernising rules that inhibit early-stage fundraising, streamlining disclosure requirements for private offerings, and enhancing Regulation A for smaller issuers. The March 2025 draft registration statement expansion and the May 2026 IPO modernisation request for comment are early expressions of this agenda. Finrep's coverage of IPO reform in 2026 and the March 2025 draft registration statement expansion provide the filing-level detail.

For companies considering going public or raising private capital, the strategic plan signals that the regulatory friction of the Gensler era, particularly around disclosure requirements for emerging growth companies and smaller issuers, is likely to decrease. That does not mean listing standards are getting easier; exchange requirements operate independently of the SEC's strategic direction.

How Will the Enforcement Shift Affect SEC Comment Letter Practice?

The plan's enforcement philosophy has direct implications for how the Division of Corporation Finance conducts its selective review of filings, and for how registrants should respond to comment letters.

The Atkins plan commits to measuring enforcement success "not by the number of cases or fines, but by the deterrent effect and the clarity provided to the marketplace." Standalone enforcement actions fell to 313 in FY 2025, the lowest in a decade, and total monetary settlements declined 45% to $808 million, according to the freewritings.law analysis of the plan.

For compliance teams, the practical shift is this: the risk of a novel enforcement theory being applied to a disclosure area that lacks formal rulemaking is lower under this plan. The cybersecurity disclosure rule, the share repurchase disclosure rule, and Reg FD remain in force and carry real enforcement risk. But the Gensler-era pattern of using enforcement to signal expectations in areas like ESG materiality or crypto asset classification is explicitly being wound down.

The plan also calls for increased staff engagement with business and industry groups, which signals a more collaborative posture on comment letter resolution. Companies that have struggled with protracted comment letter exchanges on novel disclosure questions may find the staff more receptive to pre-submission outreach and no-action requests. Finrep's playbooks on avoiding repeat SEC comment letters and anticipating SEC comments in M&A filings remain directly relevant.

What Is the EDGAR Modernisation Initiative and What Does It Mean for XBRL?

The plan names EDGAR as a legacy system requiring comprehensive review, which is the most operationally significant technology signal for registrants and their filing vendors.

EDGAR currently contains more than 70 million pages of documents and is the backbone of structured disclosure. The plan calls for adopting "secure, scalable infrastructure" to enhance data integrity, reduce operational risk, and support advanced analytics.

What this means for XBRL and structured data is genuinely uncertain at this stage, and that uncertainty cuts both ways:

- Potential relief: An EDGAR overhaul could reduce or simplify current XBRL tagging requirements, particularly for smaller filers who find inline XBRL burdensome.

- Potential new requirements: A modernised EDGAR built for advanced analytics could require more granular structured data, not less, as the SEC builds machine-readable disclosure capabilities.

The plan does not resolve this ambiguity. What it does confirm is that EDGAR modernisation is a stated five-year priority, which means registrants and their technology vendors should expect format and submission changes at some point before 2030. Finrep's guide to XBRL tagging errors that trigger SEC review covers the current structured-data requirements and the error categories that draw comment letters today.

Which Existing Rules Are Most Likely to Be Revisited Under the Retrospective Review Objective?

The plan's commitment to "periodic, retrospective reviews of existing rules" is a second channel for regulatory change, separate from formal new rulemaking. The freewritings.law analysis of the plan specifically names the following as areas the SEC has flagged for review:

- Foreign private issuer rules (a concept release on the FPI definition is already underway)

- Quarterly reporting requirements (the semiannual reporting proposal is the leading edge)

- Private fund reporting rules

- Executive compensation disclosure (Item 402 of Regulation S-K roundtable held in May 2025)

Beyond those named areas, the rules most exposed to retrospective review based on the plan's deregulatory direction include:

- The cybersecurity disclosure rule (2023), which imposed new Item 1.05 Form 8-K and annual disclosure requirements

- The share repurchase disclosure rule

- Amendments to the investment company names rule

- Elements of the climate disclosure rule not already addressed by the May 2026 rescission proposal

The plan also includes "an assessment of the agency's administrative law framework," which is significant in the post-Loper Bright environment. The Supreme Court's 2024 decision overruling Chevron deference means the SEC can no longer rely on courts deferring to its interpretation of ambiguous statutory language. The plan signals the agency is rethinking how it exercises and defends its rulemaking authority, which has implications for the durability of any new rules adopted through 2030.

Should Your Company Submit a Comment Letter, and What Should It Say?

Yes, and the 30-day window means you need to start drafting this week.

Strategic plan comment letters carry real weight. The SEC explicitly states it "hopes to gain the benefit of additional outside perspectives" through this process, and the comment infrastructure (File Number DSP-3, the same system used for rulemaking) gives the process formal standing. Institutional investors and governance organisations have used prior strategic plan comment windows to advance substantive policy positions, as the Council of Institutional Investors demonstrated with its PCAOB strategic plan comment letter in 2020.

How to Submit a Comment

Comments must reference File Number DSP-3 and can be submitted by any of these methods:

- Online: Use the SEC's internet comment form at sec.gov/rules-regulations/public-comments/dsp-3

- Email: rule-comments@sec.gov (include DSP-3 in the subject line)

- Mail: Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090

Use only one method. All submissions are posted publicly without redaction of personal identifying information.

What to Address, by Registrant Type

Registrant typeHighest-priority comment topicsLarge accelerated filerReg S-K simplification priorities; cybersecurity rule retrospective review; EDGAR modernisation transition timingMid-cap / newly public companyFiler status threshold reform; semiannual reporting election mechanics; comment letter engagement philosophyCompany with digital asset exposureDigital asset disclosure framework timeline; Crypto Task Force guidance integration; jurisdictional clarity (SEC vs. CFTC)ESG-heavy reporterVoluntary disclosure safe harbours; retrospective review of climate rule elements; interaction with ISSB/CSRD for cross-listed issuersIPO candidate / private companyRegulation A enhancement; draft registration statement process; private placement rule modernisationForeign private issuerFPI definition review timeline; interaction of disclosure simplification with home-country reporting obligations

What Makes a Comment Letter Effective

- Be specific. Name the rule, form, or item number you are commenting on. "Disclosure simplification" is too broad; "Item 303 of Regulation S-K MD&A requirements" is actionable.

- Quantify the burden. If a current requirement costs your team a specific number of hours per quarter, say so. The SEC's cost-benefit analysis in future rulemakings will draw on these data points.

- Propose, don't just object. Comments that suggest concrete alternative approaches carry more weight than those that only flag concerns.

- Coordinate where appropriate. Industry associations and peer companies filing aligned comments amplify the signal.

Action Checklist: What to Do Before July 2, 2026

- Read the plan. The full draft is linked from SEC Press Release 2026-51. It is shorter than a typical rulemaking release.

- Brief your audit committee and board. The plan's deregulatory direction, enforcement philosophy shift, and EDGAR modernisation commitment all belong in the next board update on regulatory risk.

- Identify your highest-priority issues. Use the registrant-type table above as a starting framework.

- Decide whether to file independently or through an industry association. Both channels are legitimate; the choice depends on how specific your company's concerns are.

- Draft and submit your comment letter before July 2. Allow time for legal review and sign-off.

- Monitor the retrospective review process. The plan creates a second channel for rule changes beyond formal rulemaking. Subscribe to SEC rulemaking updates for the specific rules most relevant to your disclosure obligations.

- Update your SEC examination and comment-letter response playbook to reflect the new enforcement philosophy and the more collaborative stakeholder engagement posture the plan signals.

FAQ

What is the comment deadline for the SEC's FY 2026-2030 draft strategic plan?July 2, 2026. The plan was published on June 2, 2026, giving a 30-day window. Comments must reference File Number DSP-3.

Does the strategic plan change any current SEC rules?No. The plan does not itself create, amend, or rescind any rule. It signals the SEC's priorities and the direction of future rulemaking. Rule changes require separate notice-and-comment rulemaking.

What happened to the SEC's DEI and ESG workforce goals from the prior plan?They are absent from the Atkins FY 2026-2030 plan. The Gensler-era plan's third goal explicitly called for a "diverse, equitable, inclusive" workforce. The Atkins plan replaces that goal entirely with operational efficiency and technology modernisation.

Will EDGAR modernisation create new XBRL requirements?The plan does not specify. It commits to a comprehensive review of EDGAR as a legacy system and adoption of scalable infrastructure, but the implications for XBRL tagging formats and requirements will only become clear through subsequent rulemaking or staff guidance.

How does the enforcement philosophy shift affect my company's fraud and manipulation exposure?It does not reduce it. The plan narrows enforcement focus to established violations, specifically fraud and manipulation. Companies with material misstatement risk, insider trading exposure, or market manipulation concerns face the same enforcement risk as before. What changes is the risk of novel enforcement theories in areas lacking formal rulemaking.

Is this the first time the SEC has published a strategic plan for public comment?No. This is the third consecutive cycle. The Clayton-era FY 2018-2022 plan and the Gensler-era FY 2022-2026 plan (comment deadline September 29, 2022) both followed the same Government Performance and Results Modernization Act of 2010 process. The pattern is now well-established, and each plan has reliably predicted the rulemaking agenda that followed it.

The July 2 deadline is not a soft target. Companies that want to shape the SEC's five-year regulatory direction need to be in the comment file before it closes.