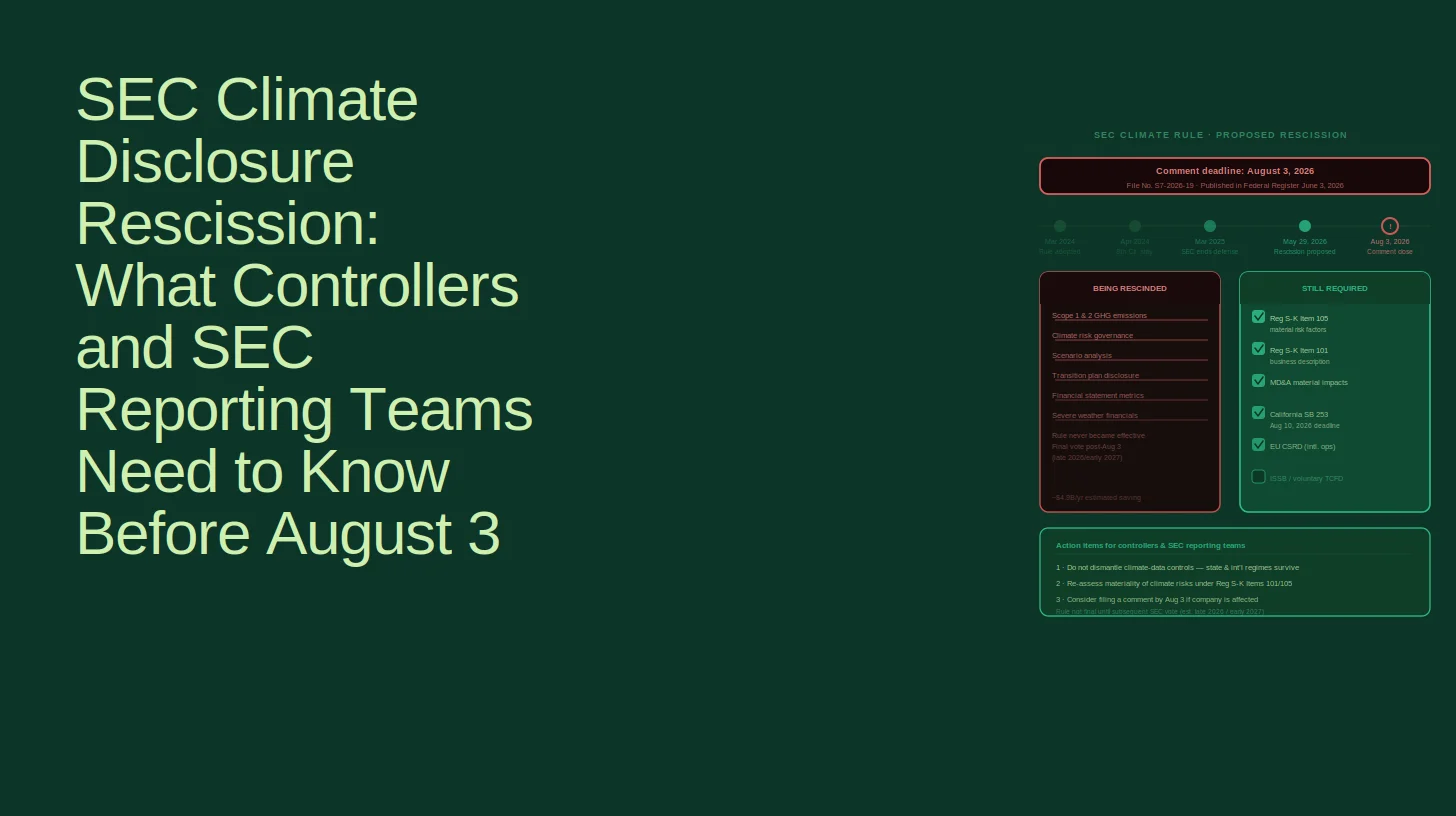

On May 29, 2026, the Securities and Exchange Commission voted to propose the full rescission of the climate-related disclosure rules it adopted in March 2024. The proposing release is Release No. 33-11421 (File No. S7-2026-19). It was published in the Federal Register on June 3, 2026. Public comments are due August 3, 2026.

The first thing a Controller or SEC Reporting Manager needs to understand is what this proposal does and does not change right now. The 2024 climate rules were stayed by the SEC in April 2024 pending resolution of Eighth Circuit litigation. They have never been effective. They have never required a single disclosure. The proposed rescission does not change the current state of affairs in that respect: the rules remain stayed and ineffective while the comment period runs.

What the proposed rescission changes is the trajectory. If rescission is finalised, the 2024 climate rules will be eliminated entirely rather than eventually going into force. The question for the Controller's office is not what has changed today but what the disclosure landscape looks like if and when rescission is final, and what obligations remain regardless.

This post addresses four questions in the sequence a Controller or SEC Reporting Lead would encounter them: what the proposal actually does, what SEC disclosure obligations remain after rescission, what the SAB 74 treatment is for climate disclosures already filed, and what state and international climate reporting requirements persist independently of the SEC's action.

What Did the SEC's 2024 Climate Rule Require and What Does the Proposed Rescission Eliminate?

The SEC adopted final climate-related disclosure rules on March 6, 2024 under the Securities Act of 1933 and the Securities Exchange Act of 1934. The rules added Items 1500 through 1508 to Regulation S-K and made corresponding amendments to Regulation S-X, Regulation S-T, Securities Act Rule 436, and numerous registration statement and report forms including Forms S-1, S-3, S-4, S-11, F-3, F-4, 10, 10-Q, 10-K, and 20-F.

The rules would have required public companies to disclose, in their registration statements and annual reports, standardised and granular information about climate-related risks, governance, strategy, and targets, as well as quantified Scope 1 and Scope 2 greenhouse gas emissions. The final rules had exempted EGCs, SRCs, and non-accelerated filers from the GHG emissions disclosure requirements, but the risk, governance, strategy, and target disclosures would have applied to all registrants.

The SEC's proposed rescission focuses on returning the agency to its core mandate and restoring a materiality-focused approach to securities regulation. The grounds for the proposed rescission, as articulated in Release No. 33-11421 and the accompanying statements of Chairman Atkins, Commissioner Uyeda, and Commissioner Peirce, are three:

First, the climate rules exceed the Commission's statutory authority. The Commission's current majority holds that the Securities Act and Exchange Act authorise disclosure requirements tied to material information relevant to investment and voting decisions, and that the 2024 rules went beyond that authority by mandating highly specific and granular climate disclosures that are not necessarily material to any specific registrant's financial condition.

Second, the rules are unnecessary and inconsistent with a materiality-based approach to disclosure. The proposing release states that existing disclosure obligations and anti-fraud provisions already elicit information about the material effects of climate-related matters. Regulation S-K Items 101 (business description), 103 (legal proceedings), and 105 (risk factors), as well as the MD&A requirement of Item 303, already require disclosure of material climate-related information without a standalone climate-specific disclosure regime.

Third, the rules impose substantial costs that are not justified by the informational benefits. The proposal estimates that the annualised cost savings if the climate rules are rescinded is approximately $4.9 billion per year over 10 years across all affected registrants.

The proposed rescission would withdraw all amendments to Regulation S-K (including Items 1500 through 1508), Regulation S-X, Regulation S-T, Securities Act Rule 436, and related Securities Act and Exchange Act registration statement and report forms.

The proposed rescission does not terminate the climate rules. The proposal initiates a comment process through which the Commission will consider public input on whether to rescind the climate rules in the manner proposed. A final rescission is unlikely before late 2026 or early 2027. Until a final vote is taken, the rules remain stayed but on the books.

What SEC Disclosure Obligations Remain After Rescission?

This is the most operationally significant question for the Controller's office, and the answer requires precision because most commentary on the rescission conflates the 2024 rule-based requirements with the pre-existing principles-based obligations.

The rescission eliminates the 2024 rules. It does not eliminate any pre-existing SEC disclosure obligation. Companies remain subject to compliance obligations under the existing materiality-based disclosure framework, including Regulation S-K Items 101, 103, and 105, and Regulation S-X, as well as MD&A requirements.

What this means in practice for each Regulation S-K item:

Item 101 (Business description). If climate-related factors are material to understanding the company's business, for example a company whose operations are significantly affected by carbon pricing regulations, extreme weather events, or transition risks that affect its supply chain or competitive position, that information must be included in the business description. This obligation exists under existing S-K requirements and is not changed by the rescission.

Item 103 (Legal proceedings). If the company is a party to material legal proceedings related to climate or environmental matters, those proceedings must be disclosed. This is unchanged.

Item 105 (Risk factors). If climate-related risks are material risk factors for the company, including physical risks such as facility exposure to extreme weather, transition risks such as regulatory cost increases from carbon pricing, or litigation risks from climate-related claims, those risks must be disclosed. The 2024 rules added a specific climate risk factor disclosure structure. The rescission eliminates that structure. The underlying obligation to disclose material risk factors, including climate-related ones, remains.

Item 303 (MD&A). If climate-related factors have materially affected the company's financial condition or results of operations in the period covered by the report, or if management is aware of known trends, demands, commitments, events, or uncertainties related to climate that are reasonably likely to have a material effect on future results, those must be disclosed in the MD&A. This obligation is unchanged. Commissioner Uyeda argued that climate-related matters are already addressed through existing SEC disclosure requirements, where required materials include disclosures relating to business operations, risk factors, management's discussion and analysis, and financial statements.

The practical implication for the SEC Reporting Manager is this: the rescission eliminates the need to produce the specific, standardised, quantified climate disclosures the 2024 rules would have required. It does not eliminate the obligation to disclose material climate-related information under existing principles-based requirements. A company for which climate-related risks are material must still disclose them. The disclosure is just less prescriptive in form and more dependent on company-specific materiality assessment.

What Is the SAB 74 Treatment for Climate Disclosures Already Filed?

SAB Topic 11.M (codified at ASC 250-10-S99-5), known as SAB 74, requires companies to disclose in their financial statements the expected effects of recently issued but not yet effective accounting standards and, by analogy, of SEC rules that have been adopted but not yet effective. Many public companies have been including SAB 74-style disclosures about the 2024 climate rules in their annual reports and quarterly filings since the rules were adopted in March 2024, even though the rules were stayed and never became effective.

The proposed rescission raises two distinct SAB 74 questions that the Controller's office needs to address.

Question 1: Should the SAB 74 climate disclosure be continued while the rescission proposal is pending?

The 2024 climate rules remain on the books, stayed but not rescinded, during the comment period through August 3, 2026 and during the subsequent period until a final rescission vote is taken. The rules are a pending regulatory requirement in the same sense they have been since April 2024. The proposed rescission introduces significant uncertainty about whether the rules will ever become effective, but it does not resolve that uncertainty until the final vote.

The conservative position is to continue including a SAB 74 disclosure in annual and quarterly filings through August 3, 2026, updating the language to reflect the proposed rescission and the uncertainty it creates. The disclosure should acknowledge that the SEC has proposed to rescind the 2024 climate rules, that the proposal is subject to a comment period closing August 3, 2026, and that the company is monitoring the outcome. This approach preserves the company's disclosure record for the period of uncertainty without overstating the likelihood that the rules will become effective.

After a final rescission vote, which is unlikely before late 2026 or early 2027 based on the Duane Morris analysis of the rulemaking timeline, the SAB 74 disclosure for the 2024 climate rules should be removed, because the rules will no longer be pending. No subsequent adoption date will exist for which the company needs to disclose expected effects.

Question 2: Does anything about the rescission trigger a SAB 74 disclosure obligation?

The rescission proposal itself is not an accounting standard or an SEC rule change that requires SAB 74 disclosure. It is a proposed elimination of a rule. The SAB 74 framework addresses newly issued standards not yet effective, not proposals to eliminate existing standards. No new SAB 74 disclosure is triggered by the rescission proposal itself.

Companies that have previously disclosed estimated compliance costs for the 2024 climate rules in their SAB 74 footnote should update those disclosures to reflect the changed circumstances: the proposed rescission, the uncertainty about whether the rules will take effect, and the company's current assessment of the likelihood of adoption.

Companies that never included a SAB 74 disclosure for the 2024 climate rules because the rules were stayed since adoption and the disclosure was assessed as immaterial (a defensible position given that the rules never became effective) have no new disclosure obligation created by the rescission proposal.

What Do California SB 253 and SB 261 Still Require After the SEC Rescission?

This is the question that most US-focused coverage of the SEC rescission fails to address with the specificity that a Controller at a large public company actually needs. The proposed rescission, if finalised, would not eliminate the growing network of climate-related disclosure requirements imposed by state governments, foreign jurisdictions, and international standard-setting bodies. Companies should view the proposal as a change in regulatory emphasis, not as the end of climate-related reporting obligations.

California SB 253 (Climate Corporate Data Accountability Act).

SB 253 applies to entities doing business in California with annual revenues exceeding $1 billion. The law requires annual reporting of Scope 1 and Scope 2 greenhouse gas emissions, with the first reporting deadline scheduled for August 10, 2026. The California Air Resources Board (CARB) adopted its initial regulation at its February 2026 board hearing and has reaffirmed the August 10, 2026 deadline. Companies that were already collecting emissions data by December 2024 are expected to file. If not, a company can submit a non-collection statement for 2026, but this is a last resort. The company will be expected to file a full inventory with assurance from 2027.

Scope 3 reporting requirements under SB 253 will begin in 2027, accompanied by phased assurance requirements that become increasingly rigorous over time.

SB 253 is a California law. The SEC's proposed rescission of a federal rule has no effect on SB 253. A company with over $1 billion in annual revenues doing business in California must comply with SB 253 regardless of what happens at the federal level.

California SB 261 (Climate-Related Financial Risk Act).

SB 261 requires biennial public reports on climate-related financial risks and mitigation strategies from companies with over $500 million in annual global revenue doing business in California. The initial statutory deadline was January 1, 2026. Enforcement of SB 261 has been enjoined by the Ninth Circuit, pending appeal. A decision on the appeal could be issued at any time and may have implications beyond SB 261. Companies should continue building SB 261 compliance capability rather than assuming the injunction will be permanent.

How Does the EU's CSRD Interact With the SEC Rescission for Dual-Reporting Companies?

For US-headquartered public companies with significant EU operations, the proposed SEC rescission does not change their CSRD obligations. The CSRD is an EU directive that applies based on EU nexus, not based on SEC filing status.

At the international level, the EU adopted legislation in February 2026 to narrow the scope of the CSRD and postpone implementation timelines. The February 2026 EU omnibus package reduced the number of companies in scope for the CSRD by approximately 80% from the original 2022 directive's scope, primarily by raising the size thresholds for non-EU companies. The threshold change means that many US companies that were previously in scope for CSRD may no longer be, depending on their EU revenue and employee counts. Companies should confirm their CSRD scope status under the February 2026 amendments rather than assuming they remain in or out of scope based on the 2022 directive's original thresholds.

For companies that remain in CSRD scope, the SEC rescission creates one practical complication: the alignment between CSRD disclosures and SEC filings that many companies had anticipated building may not materialise. A company that was planning to produce a single climate disclosure dataset that would satisfy both the SEC's 2024 rules and CSRD requirements will now need to produce CSRD-compliant sustainability reports without the benefit of a parallel SEC climate disclosure framework to draw on for data collection discipline.

The ISSB's IFRS S2 standard, which forms the basis of many non-EU jurisdictions' emerging climate disclosure requirements, was recently amended to reduce complexity in GHG emissions disclosure requirements. The specific amendments to IFRS S2 and their effective dates should be confirmed against the most current ISSB publications before building or updating a climate data collection process.

What Should the Controller's Office Do Before the Comment Period Closes on August 3?

Four actions are worth taking before August 3, 2026.

Action 1: Update your SAB 74 climate disclosure for the Q2 2026 10-Q. If your company has been including a SAB 74 disclosure about the 2024 climate rules, update the language in the Q2 2026 10-Q to reflect the proposed rescission and the uncertainty it creates. The disclosure should acknowledge the proposed rescission, note that the comment period closes August 3, 2026, and state that the company is monitoring the outcome. Do not remove the SAB 74 disclosure while the rules remain technically on the books, even in stayed form.

Action 2: Confirm the California SB 253 August 10, 2026 deadline. If your company has over $1 billion in annual revenues and does business in California, the SB 253 Scope 1 and Scope 2 emissions filing deadline is August 10, 2026, eight days after the SEC comment period closes. These two deadlines fall in the same week. The Controller's office should confirm which of three positions applies: the company has been collecting emissions data and will file, the company has not collected data and will file a non-collection statement, or the company does not meet the SB 253 threshold.

Action 3: Assess whether materiality-based climate disclosure in your SEC filings needs updating. If your company has included climate-related risk factors, MD&A disclosures, or business description disclosures based on a materiality assessment of climate risk, the rescission does not change the obligation to make those disclosures if the underlying risks remain material. Review your fiscal 2026 disclosures against your current materiality assessment, not against the 2024 rule requirements.

Action 4: Submit a comment letter if the rescission materially affects your company. The SEC's comment process is the formal mechanism through which reporting companies influence whether and how a proposed rule is finalised. Companies that have already invested in climate data collection infrastructure in anticipation of the 2024 rules, or companies that believe the principles-based disclosure framework is insufficient to produce the climate information their investors need, have specific operational experience that is directly relevant to the SEC's deliberations. Comments are submitted at sec.gov and become part of the public rulemaking record.

Frequently Asked Questions

What did the SEC's proposed rescission release actually do on May 29, 2026?

The SEC voted to propose the full rescission of the climate-related disclosure rules adopted in March 2024. The proposing release is Release No. 33-11421. Published in the Federal Register on June 3, 2026, it initiated a 60-day comment period closing August 3, 2026. The proposed rescission does not finalise the elimination of the 2024 rules. A subsequent commission vote, expected no earlier than late 2026 or early 2027, would be required for the rescission to become final.

Have the 2024 climate disclosure rules ever required any company to make a disclosure?

No. The SEC voluntarily stayed the 2024 climate rules in April 2024, immediately after adoption, pending resolution of consolidated Eighth Circuit litigation. The rules have been stayed continuously since then and have never been effective. No company has been required to make any disclosure under the 2024 climate rules.

What SEC disclosure obligations remain if the rescission is finalised?

Regulation S-K Items 101, 103, and 105, and the MD&A requirement of Item 303, continue to require disclosure of material climate-related information in the same way they require disclosure of any other material business, legal, risk, or operational information. A company for which climate-related risks or opportunities are material to its financial condition, results of operations, or risk profile must continue to disclose that information under the principles-based framework. What is eliminated is the prescriptive, standardised, quantified disclosure structure the 2024 rules would have imposed.

What should companies do with their SAB 74 climate disclosures while the rescission is pending?

Companies that have included SAB 74 disclosures about the 2024 climate rules should update the language to reflect the proposed rescission and the uncertainty it creates. The disclosure should acknowledge the proposed rescission, note the August 3 comment deadline, and state that the company is monitoring the outcome. The SAB 74 disclosure should not be removed while the rules remain technically on the books in stayed form. After a final rescission vote, the disclosure should be removed.

Does the SEC rescission affect California SB 253 compliance?

No. SB 253 is a California law that applies independently of SEC rules. Companies with over $1 billion in annual revenues doing business in California must comply with SB 253 regardless of what happens at the federal level. The first Scope 1 and Scope 2 emissions reporting deadline under SB 253 is August 10, 2026.

Does the SEC rescission affect CSRD compliance for US companies with EU operations?

No. The CSRD is an EU directive that applies based on EU nexus. The February 2026 EU omnibus package narrowed CSRD scope by raising size thresholds, which may affect whether specific US companies remain in scope. Companies with EU operations should confirm their CSRD scope status under the February 2026 amendments regardless of the SEC rescission.

Key Takeaways

- On May 29, 2026, the SEC proposed the full rescission of its 2024 climate disclosure rules under Release No. 33-11421. The proposal was published in the Federal Register on June 3, 2026. Comments are due August 3, 2026. Final rescission, if adopted, is unlikely before late 2026 or early 2027.

- The 2024 climate rules have been stayed since April 2024 and have never been effective. The proposed rescission does not change the current state of affairs during the comment period.

- Regulation S-K Items 101, 103, 105, and the MD&A requirement of Item 303 continue to require disclosure of material climate-related information under the existing principles-based framework. The rescission eliminates the prescriptive, standardised disclosure structure of the 2024 rules, not the underlying obligation to disclose material information.

- Companies that have included SAB 74 disclosures about the 2024 climate rules should update the language to reflect the proposed rescission and the uncertainty it creates. Do not remove the SAB 74 disclosure while the rules remain technically on the books in stayed form.

- California SB 253 is independent of the SEC's action. Companies with over $1 billion in annual revenues doing business in California face a Scope 1 and Scope 2 emissions reporting deadline of August 10, 2026, eight days after the SEC comment period closes.

- California SB 261 enforcement remains enjoined by the Ninth Circuit pending appeal. A decision could be issued at any time. Companies should continue building compliance capability rather than assuming the injunction will be permanent.

- The CSRD applies based on EU nexus and is not affected by the SEC rescission. The February 2026 EU omnibus package narrowed CSRD scope. US companies with EU operations should confirm their current CSRD scope status under the February 2026 amendments.