SEC Filer Status 2026: Rule 12b-2 Thresholds, 10-K Deadlines, and the May 2026 Two-Category Proposal

For any public company CFO or SEC reporting team, filer status is not an administrative checkbox. It determines your Form 10-K deadline, whether your auditor must attest to your internal controls, and how much executive compensation disclosure goes into your proxy. Get it wrong and you risk missed deadlines, deficient filings, and lost Form S-3 eligibility.

This guide covers the operative rules you must apply to every 2026 filing under Rule 12b-2, and then layers in the SEC's May 19, 2026 proposal to collapse the current five-category system into two. Most published content covers one or the other. You need both.

What Are the SEC Accelerated Filer Requirements Under Current Rule 12b-2?

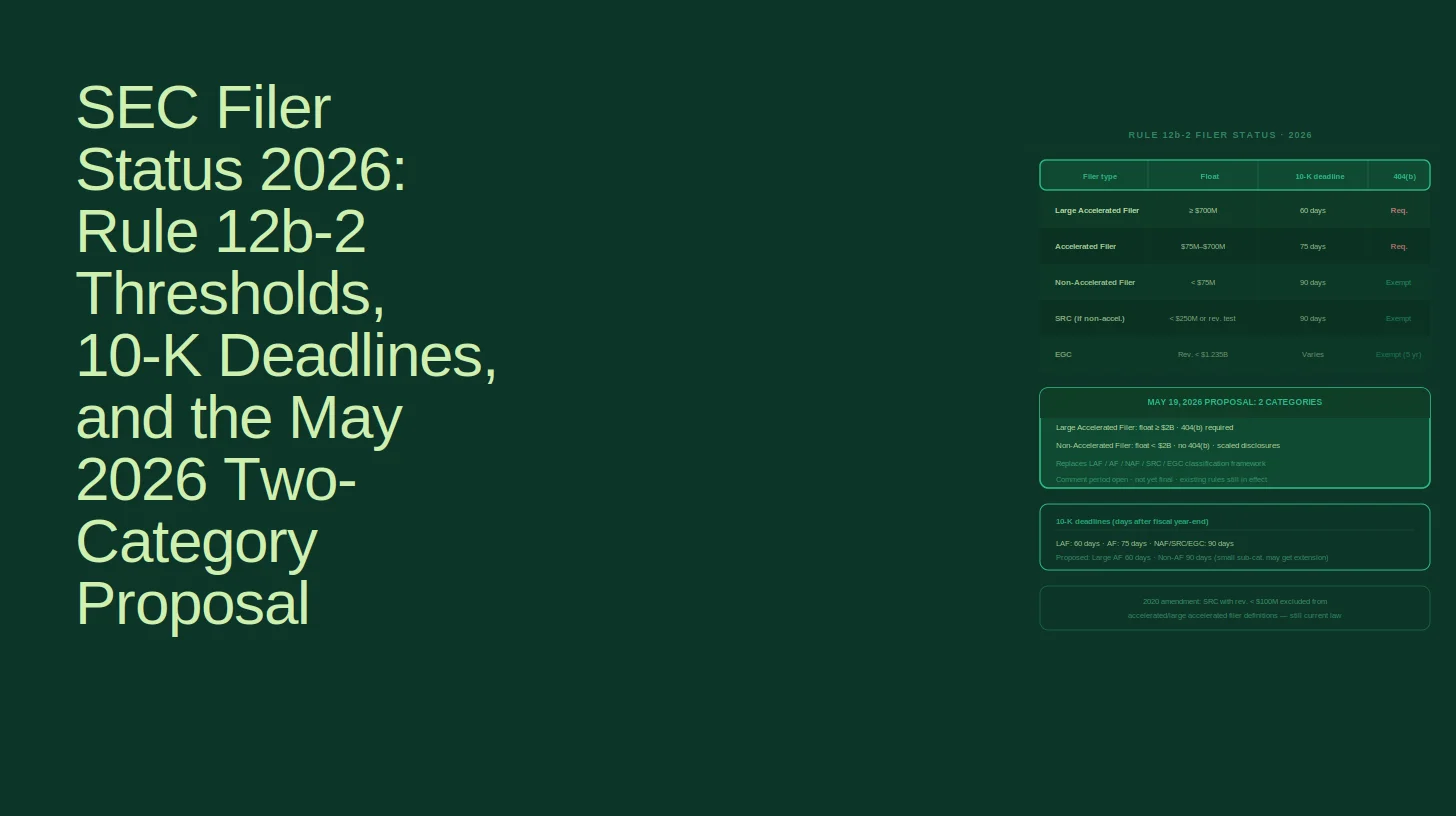

Under current Rule 12b-2 (as last amended March 12, 2020), a company is an accelerated filer if it has a public float of at least $75 million but less than $700 million, has been subject to Exchange Act Section 13(a) or 15(d) reporting for at least 12 calendar months, has filed at least one annual report, and is not excluded by the revenue carve-out described below.

A large accelerated filer meets the same seasoning conditions but has a public float of $700 million or more. Non-accelerated filers are everyone else: companies below $75 million in public float, or those excluded from the accelerated categories by the revenue test.

Public float is measured as of the last business day of the company's most recently completed second fiscal quarter. For calendar year-end companies, that is June 30. As Fenwick & West partners noted in August 2025, once that date passes, companies can lock in their status as large accelerated filer, accelerated filer, or non-accelerated filer for their Form 10-K and Forms 10-Q due in 2026.

The Revenue Carve-Out: The Most Overlooked Condition

The 2020 amendments added a condition that catches many companies by surprise. A company is excluded from both the accelerated and large accelerated filer definitions if it is eligible to be a smaller reporting company (SRC) and had annual revenues below $100 million in its most recently completed fiscal year. This applies regardless of public float.

In practice, a company with a $300 million public float and $80 million in annual revenue may still be a non-accelerated filer if it qualifies as an SRC under the revenue test. This carve-out was the most substantive change in the 2020 rulemaking and remains widely underappreciated by companies sitting between $75 million and $700 million in float.

For business development companies, which cannot qualify as SRCs, the analogous test uses annual investment income below $100 million rather than operating revenue.

Entry and Exit Thresholds: The Buffer Zone

Entry and exit thresholds are different, and confusing them is a common mistake.

Status ChangeEntry ThresholdExit ThresholdBecome a large accelerated filerPublic float $700M or moreDrop below $560M to exit to accelerated filerBecome an accelerated filerPublic float $75M or more (and not excluded by revenue test)Drop below $60M to exit to non-accelerated filer

The 2020 amendments raised the exit thresholds from $500 million to $560 million (for leaving LAF status) and from $50 million to $60 million (for leaving accelerated filer status). The gap between entry and exit thresholds is intentional: it prevents companies from ping-ponging between categories when their float hovers near a threshold.

One more timing point that trips up compliance teams: losing accelerated filer status at year-end does not change your filing deadlines for the current year. The new status governs the next annual and quarterly filing cycle. Status determined at fiscal year-end applies to all filings in the subsequent year, per PwC's SEC reporting guidance.

Filing Deadlines by Filer Category

Your filer status directly sets your Form 10-K and Form 10-Q deadlines. There is no discretion here: the category you land in at year-end governs every periodic filing in the following cycle.

Filer CategoryForm 10-K DeadlineForm 10-Q DeadlineLarge accelerated filer60 days after fiscal year-end40 days after quarter-endAccelerated filer75 days after fiscal year-end40 days after quarter-endNon-accelerated filer90 days after fiscal year-end45 days after quarter-end

If you need more time, Form 12b-25 provides a limited extension, but it does not reset the underlying deadline obligation.

SOX 404(b): Which Companies Must Get an Auditor Attestation?

SOX Section 404(b) requires an independent auditor to attest to management's assessment of internal control over financial reporting (ICFR). That obligation applies to large accelerated filers and accelerated filers. Non-accelerated filers and emerging growth companies are exempt.

The 2020 amendments effectively removed the 404(b) requirement from low-revenue SRC-eligible issuers by reclassifying them as non-accelerated filers. Those companies still must complete management's own 404(a) assessment and certify disclosure controls under SOX Sections 302 and 906. The auditor attestation, which is the expensive part, no longer applies.

The 2020 amendments also added a check box to the cover pages of Forms 10-K, 20-F, and 40-F requiring companies to indicate whether an ICFR auditor attestation is included. That box must be completed accurately based on current filer status, not last year's status.

For more on what happens when ICFR controls fail, see Finrep's guide to material weakness disclosure requirements.

The Downstream Cascade: Executive Compensation Disclosure

Filer status does not stop at filing deadlines and SOX. It runs directly into your proxy statement. Accelerated and large accelerated filers must comply with the full suite of executive compensation disclosure requirements under Regulation S-K. Non-accelerated filers get scaled accommodations.

What accelerated filers must include that non-accelerated filers do not:

- Compensation Discussion and Analysis (CD&A)

- Pay-versus-performance table (Item 402(v))

- CEO pay ratio disclosure

- Five named executive officers (NEOs) in the Summary Compensation Table, with three years of pay history

- Annual say-on-pay and say-on-frequency advisory votes

Non-accelerated filers disclose compensation for only three NEOs, provide two years of pay history, and are exempt from CD&A, pay-versus-performance, CEO pay ratio, and say-on-pay votes. For companies near the $75 million threshold, this distinction can represent a meaningful reduction in proxy preparation cost and governance complexity.

EGC Status and the LAF Trap

One interaction that catches high-growth companies off guard: qualifying as a large accelerated filer automatically terminates emerging growth company status. EGC and LAF are mutually exclusive under the JOBS Act. A company that IPOs with a rapidly growing market cap and crosses $700 million in public float before its five-year EGC period expires loses EGC accommodations immediately, including the ability to delay adopting new PCAOB auditing standards.

Under the current 12-month seasoning rule, this transition can happen surprisingly fast. A company that goes public in January 2025 and hits $700 million in float by June 2025 could become a large accelerated filer for its first Form 10-K.

Dual-Class Shares: A Genuine Legal Ambiguity

For technology and media companies with dual-class capital structures, the public float calculation carries real uncertainty. Rule 12b-2 defines public float as the aggregate market value of voting and non-voting common equity held by non-affiliates, but it does not specify whether shares of a non-publicly traded class should be included.

As Cooley LLP notes in its filer status guide: "The SEC staff has provided nonbinding, informal oral guidance that, for purposes of calculating public float, only shares of the publicly traded classes of common equity should be included in the calculation. This guidance, like other unofficial guidance from the SEC staff, has no legal force or effect."

In practice, whether you include or exclude the non-traded class can determine whether you land in the accelerated or large accelerated filer bucket. There is no binding rule. Companies near the $700 million threshold with dual-class structures should document their methodology and confirm it with counsel.

A Live Compliance Risk: XBRL Tagging of Public Float

The public float figure on the Form 10-K cover page is also an XBRL-tagged data point, and it has a known accuracy problem. The SEC's Division of Economic and Risk Analysis conducted an assessment of public float XBRL tagging in Forms 10-K for fiscal year 2024 and continued to observe scaling errors in certain filings. A scaling error, such as reporting $500 million as $500,000 or $500 billion, can corrupt the SEC's filer status database and create downstream compliance issues. Check the tagged value, not just the printed number.

The May 2026 Proposal: What Would Actually Change?

On May 19, 2026, SEC Chairman Paul Atkins proposed the most sweeping overhaul of the filer status framework since the categories were created. The proposal, part of his "Make IPOs Great Again" agenda, would collapse the current five-category system into two: large accelerated filers and non-accelerated filers, with a sub-category for small non-accelerated filers.

Key takeaway: The proposal is still open for public comment. Final rules could be adopted by end of 2026, according to Pay Governance analysts writing on the Harvard Law School Forum. Every 2026 filing must use current Rule 12b-2 thresholds. Plan for the proposal in parallel, but do not apply it yet.

Current Rules vs. Proposed Rules: Side-by-Side

DimensionCurrent Rule 12b-2May 2026 ProposalLarge accelerated filer thresholdPublic float $700M or morePublic float $2B or moreAccelerated filer category$75M to $700M public floatEliminatedNon-accelerated filerBelow $75M (or revenue carve-out)All companies below $2BFloat measurementSingle-day closing price, last business day of Q210-trading-day average, last 10 days of Q2Consecutive years requiredOne year above thresholdTwo consecutive years above thresholdSeasoning requirement12 calendar months60 calendar months (5 years)SOX 404(b) requiredLAFs and accelerated filers (non-EGC)LAFs onlySay-on-payRequired for accelerated and LAFsLAFs onlyCD&ARequired for accelerated and LAFsLAFs onlyNEOs disclosed5 (3 years of pay history)3 for NAFs (2 years of pay history)Small filer sub-categoryNoneSmall NAFs (total assets $35M or less, 2 years) get +30 days for 10-K, +5 days for 10-Q

Who Gets Reclassified?

Based on 2024 filing data covering 5,976 domestic registrants, the SEC's own fact sheet projects:

- 19.2% of current public companies would be large accelerated filers (down from 35.4% today)

- 80.8% would be non-accelerated filers (up from approximately 64.6% today)

- 17.9% of all public companies would qualify as small non-accelerated filers

- Large accelerated filers would still hold 93.5% of total public float

Nearly all S&P 500 and S&P 400 companies would remain large accelerated filers under the $2 billion threshold. The relief is targeted squarely at mid-cap and smaller public companies, the segment currently classified as accelerated filers.

The Five-Year IPO On-Ramp

The proposed 60-month seasoning requirement is a fundamental shift. Under current rules, a company can become a large accelerated filer after just 12 months of Exchange Act reporting if its float exceeds $700 million. Under the proposal, no company, regardless of float, can become a large accelerated filer until it has been a reporting company for five consecutive years.

This creates a true five-year on-ramp for all newly public companies, analogous to the EGC accommodation period under the JOBS Act. A company that IPOs in 2027 with a $5 billion float would still be a non-accelerated filer until 2032. The interaction with M&A transactions, specifically whether a merger resets the seasoning clock, is an open question the proposal does not address and will likely require SEC guidance.

The Co-Filing Edge Case

One nuance the SEC's fact sheet flags explicitly but that has received almost no third-party attention: approximately 91 registrants (1.5% of all registrants) that would be non-accelerated filers under the proposal currently co-file with registrants that would remain large accelerated filers. Those companies may remain implicitly subject to LAF requirements and deadlines even after reclassification. If your company co-files with a LAF parent or subsidiary, this is worth a close read of the final rule when it arrives.

Governance Strategy: What to Voluntarily Retain?

If the proposal passes, companies reclassified as non-accelerated filers will face a real governance decision, not just a compliance one. As Pay Governance's Mike Kesner and Jon Weinstein wrote on the Harvard Law School Forum: "Many companies may choose to eliminate some current disclosures, such as pay-versus-performance and the CEO pay ratio, while retaining others, such as the CD&A (perhaps in a more streamlined format). Some companies may also decide to retain Say on Pay to give investors a direct means of expressing their views on executive compensation rather than limiting that expression to votes on Compensation Committee member elections."

Institutional investors and proxy advisors have not yet signaled how they will treat companies that drop say-on-pay. Companies with significant institutional ownership should model investor reaction before deciding to eliminate any disclosure that investors currently use.

What to Do Right Now: A Practical Checklist

Compliance teams should be running two tracks simultaneously.

Track 1: Current rules (applies to all 2026 filings)

- Confirm your public float as of June 30, 2026 (or the last business day of your second fiscal quarter if you have a non-calendar fiscal year).

- Apply the revenue carve-out test: if your annual revenues are below $100 million and you are SRC-eligible, you may be a non-accelerated filer regardless of float.

- Check the entry and exit thresholds, not just the headline numbers. If your float dropped below $560 million, you may have exited LAF status.

- Verify the XBRL-tagged public float on your Form 10-K cover page matches the printed figure, with correct scaling.

- Confirm the ICFR auditor attestation check box is completed accurately.

- If you have a dual-class structure near the $700 million threshold, document your float calculation methodology and confirm with counsel.

- If your company changed its fiscal year, follow FRM 1340.8 guidance for the public float test, as confirmed by SEC staff at the March 2026 CAQ/SEC joint meeting.

Track 2: Proposed rules (model now, do not apply yet)

- Determine whether your company would be a large accelerated filer or non-accelerated filer under the $2 billion threshold.

- If you would be reclassified as a non-accelerated filer, model the SOX 404(b) cost savings and the reduction in executive compensation disclosure obligations.

- Assess whether the two-consecutive-year requirement would delay your reclassification even if your float drops below $2 billion after the first year.

- Evaluate whether to submit a comment letter during the 60-day public comment period after Federal Register publication.

- Brief your compensation committee and proxy advisors on the potential elimination of say-on-pay and CD&A obligations, and decide in advance whether to retain them voluntarily.

For a deeper look at how the proposal reshapes obligations for companies between $700 million and $2 billion in float, see Finrep's analysis of how the SEC's 2026 proposal affects mid-caps and the full breakdown of the two-category filer system.

FAQ

When is accelerated filer status determined?Filer status is assessed annually as of the last day of the fiscal year, based on public float measured as of the last business day of the most recently completed second fiscal quarter (June 30 for calendar year-end companies). The status determined at year-end governs all Form 10-K and Form 10-Q filings in the subsequent annual cycle.

What is the difference between a large accelerated filer and an accelerated filer?Under current rules, a large accelerated filer has a public float of $700 million or more; an accelerated filer has a public float between $75 million and $700 million. Both must have 12 months of Exchange Act reporting history and at least one filed annual report, and neither can be excluded by the revenue carve-out. The key practical difference is the Form 10-K deadline: 60 days for LAFs versus 75 days for accelerated filers.

Do all accelerated filers need a SOX 404(b) auditor attestation?Yes, under current rules, both accelerated filers and large accelerated filers must obtain an auditor attestation on ICFR, unless they also qualify as emerging growth companies. Non-accelerated filers and EGCs are exempt from 404(b), though all filers remain subject to management's 404(a) assessment.

What is the non-accelerated filer revenue carve-out?A company with a public float between $75 million and $700 million is still a non-accelerated filer if it is SRC-eligible and had annual revenues below $100 million in its most recently completed fiscal year. This carve-out was added by the March 2020 amendments and is frequently overlooked.

Will the May 2026 proposal eliminate the accelerated filer category entirely?Yes, if adopted. The proposal would eliminate the accelerated filer category and the SRC category, leaving only large accelerated filers (public float $2 billion or more, met for two consecutive years, with 60 months of seasoning) and non-accelerated filers. All other companies, including today's accelerated filers, would become non-accelerated filers.

How does filer status interact with EGC status?They are mutually exclusive at the large accelerated filer level. A company that qualifies as a large accelerated filer automatically loses its EGC status. Under the current 12-month seasoning rule, a fast-growing company can hit the $700 million LAF threshold before its five-year EGC period expires, triggering an early loss of EGC accommodations. Under the proposed 60-month seasoning rule, this conflict would be eliminated because no company could become a LAF within its first five years regardless of float.