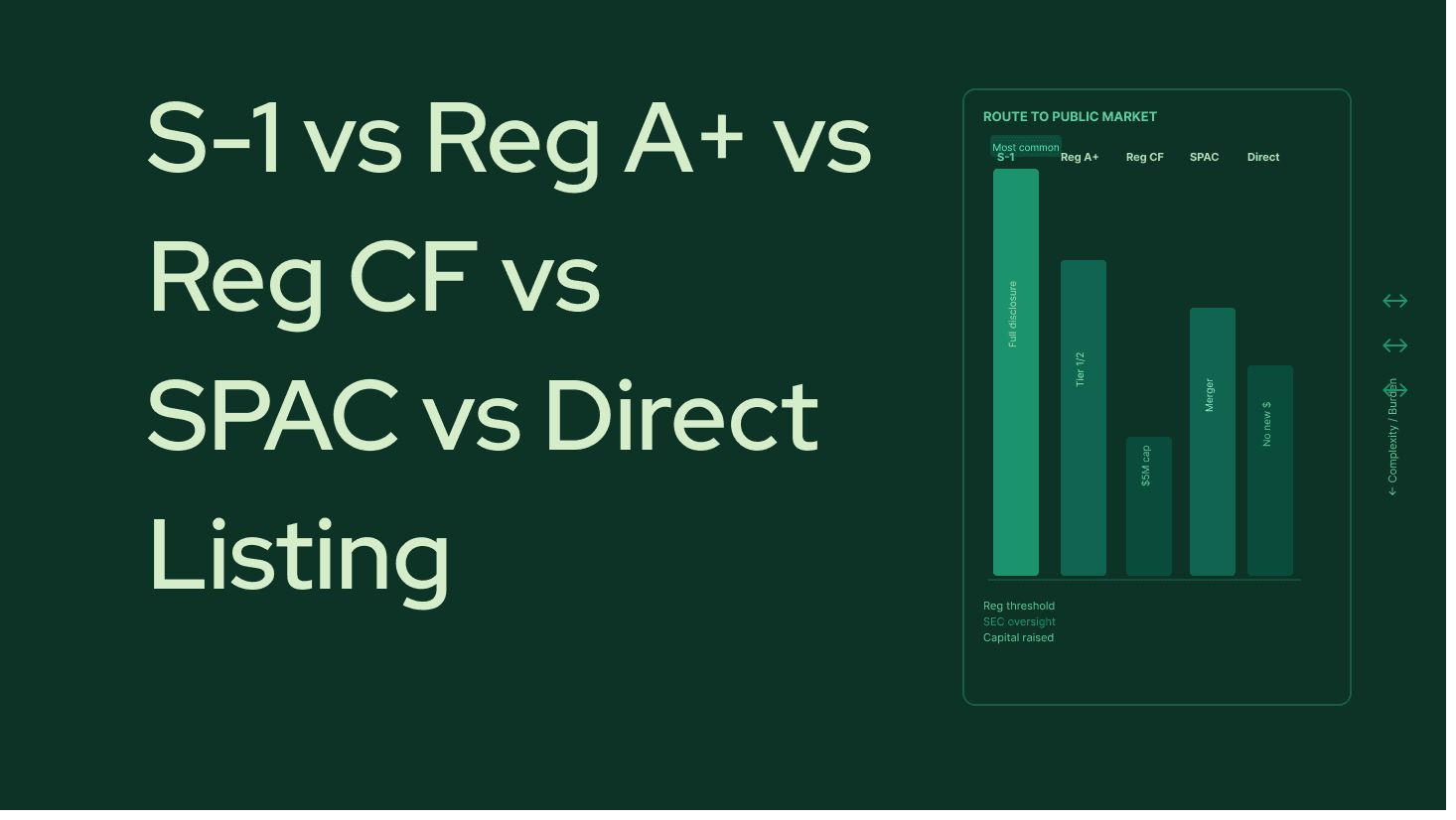

Most founders use "IPO" as a catch-all for five distinct pathways, each with different filings, capital ceilings, investor eligibility rules, ongoing reporting obligations, and aftermarket realities. Choosing the wrong one does not just cost money. It can lock a company into a reporting framework it cannot sustain, a shareholder base that cannot support a liquid aftermarket, or a capital raise that falls far short of what the business requires.

The SEC publishes annual data on all five pathways. The most recent release, SEC Press Release 2026-29 (March 17, 2026), contains updated statistics on IPOs, Regulation A offerings, and Regulation Crowdfunding offerings through the end of 2025. This post maps every pathway against that data and organises the comparison in the sequence a CFO or founder encounters the questions when evaluating which route to take.

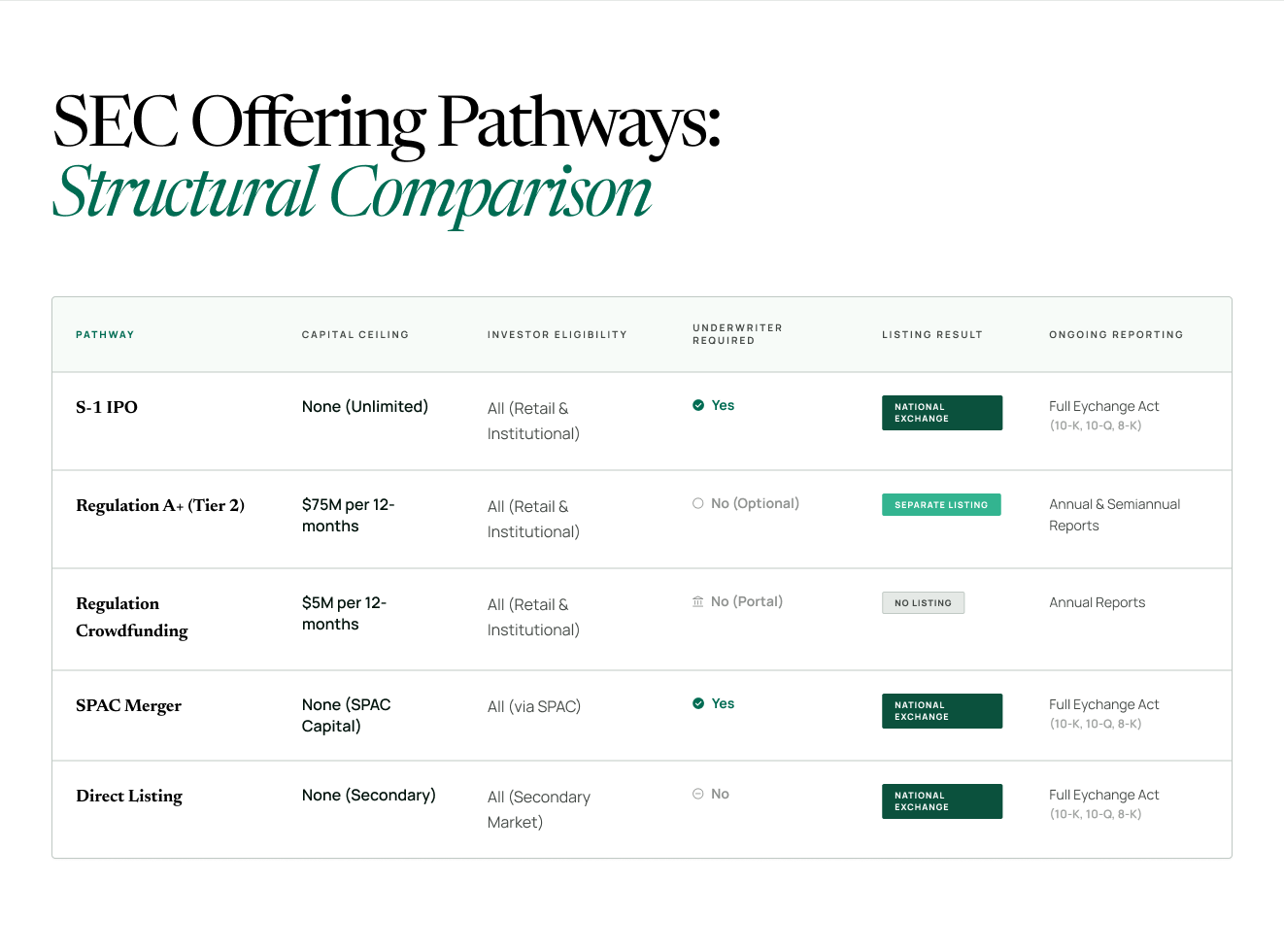

What Are the Five Pathways to Access Public Capital Markets in the US?

The SEC's offering pathways framework identifies the primary mechanisms through which a company can raise capital from the public. Five are relevant to most private companies evaluating a public market transaction.

The S-1 IPO is a full registration statement under the Securities Act of 1933. The company files a prospectus with the SEC, receives and responds to comment letters, conducts a road show for institutional investors, prices the offering through its underwriters, and begins trading on a national exchange. All investors retail and institutional can participate. The company becomes a fully reporting public company subject to Exchange Act reporting on the day of listing.

Regulation A (Reg A+) is a simplified offering pathway for smaller companies. Tier 1 of Regulation A permits raises of up to $20 million in any 12-month period from the public, subject to state securities law review. Tier 2 permits raises of up to $75 million in any 12-month period, preempts state securities laws, and requires audited financial statements and ongoing annual and semiannual reporting. Both retail and institutional investors may participate. Reg A+ is not a listing it is an offering. The company does not automatically become listed on an exchange.

Regulation Crowdfunding (Reg CF) permits companies to raise up to $5 million in any 12-month period from the public through SEC-registered crowdfunding portals. All investors may participate, subject to individual investment limits based on income and net worth. The company must file offering documents with the SEC and must file ongoing annual reports while it has more than 300 holders of the crowdfunding security and more than $10 million in total assets.

A SPAC merger (de-SPAC transaction) is not a traditional IPO. A Special Purpose Acquisition Company raises capital from institutional investors in its own IPO, then identifies and merges with a private operating company within a defined time window. The private company goes public through the merger without conducting its own IPO. The de-SPAC merger typically involves filing a proxy statement or S-4 registration statement with the SEC and requires shareholder approval from the SPAC's investors.

A direct listing allows a company to list its existing shares on a national exchange without conducting an offering or raising new capital in the listing event itself. No underwriter is engaged for the listing. Price is determined by the market on the first day of trading. Direct listings on Nasdaq require meeting specific market value of unrestricted publicly held shares (MVUPHS) thresholds and bid price requirements.

What Does the Actual Data Show About Regulation A Offerings?

Regulation A is the most systematically oversold pathway in the small-company capital formation conversation. The data from the SEC's March 2026 data release and the SEC's Regulation A statistics tells a precise story.

Through December 2025, there have been 1,531 qualified Regulation A offerings. Total capital raised across all Reg A offerings through that period is approximately $10.5 billion. The average Tier 2 raise is approximately $13 million against a statutory maximum of $75 million per 12-month period.

Three observations about that data matter for a CFO making a pathway decision.

First, the average raise of $13 million against a $75 million cap means the typical Reg A issuer is raising less than 18 cents of every dollar the pathway theoretically permits. The gap between the statutory ceiling and the actual average raise reflects the aftermarket reality of Reg A offerings: without exchange listing, without institutional sponsorship, and without mandatory research coverage, most Reg A offerings cannot attract sufficient investor demand to approach the ceiling.

Second, 1,531 total qualified offerings since 2015 is approximately 150 per year across the entire US economy. For comparison, traditional IPOs in a normal year run 150 to 300. Reg A is not the mass-market IPO alternative it is sometimes described as.

Third, Reg A offerings do not produce a listed, exchange-traded security by default. The company raises capital from public investors through the Reg A offering, but those investors hold securities that may not be tradeable on any exchange unless the company separately pursues a listing. The aftermarket liquidity that makes an IPO valuable the ability for investors to sell their shares is not automatic in a Reg A offering.

Reg A is the right pathway for a specific type of company: one that needs $5 to $20 million from a broad investor base, has a compelling consumer brand that makes direct-to-consumer fundraising effective, and does not require institutional sponsorship or exchange listing to achieve its objectives. It is not the right pathway for a company whose growth trajectory requires $50 million or more, whose investors expect a liquid aftermarket, or whose post-raise reporting burden must be managed with a small finance team.

What Does the Actual Data Show About Regulation Crowdfunding Offerings?

Regulation Crowdfunding (Reg CF) data from the SEC's March 2026 release is even more specific about what this pathway can and cannot do.

Through December 2025, there have been 9,461 Reg CF offerings. Total capital raised is approximately $1.546 billion. The average raise is approximately $359,000.

The $359,000 average raise tells the story directly. Regulation Crowdfunding has a statutory maximum of $5 million per 12-month period. The typical Reg CF offering raises less than 8% of that maximum. The investor base for Reg CF offerings is primarily retail, subject to individual investment limits tied to income and net worth. The amounts individual investors can contribute are small. Building a $5 million raise from dozens or hundreds of small contributions through a crowdfunding portal is mechanically possible but operationally demanding.

Reg CF is the right pathway for a specific narrow use case: a company at an early stage that wants to build community ownership among its customer base, needs $200,000 to $1 million in capital, and can use the fundraising process itself as a marketing and brand-building exercise. It is not a viable pathway for a company that needs institutional-scale capital, exchange listing, or a traditional public company reporting structure.

The gap between the $5 million statutory ceiling and the $359,000 average raise is the most informative number in the Reg CF dataset. It is not a regulatory failure. It reflects the economic reality of asking retail investors with investment limits to fund a company through a crowdfunding portal without the institutional backing, research coverage, or exchange listing that makes larger investments defensible.

What Does the Actual Data Show About SPAC Activity?

SPAC activity has been cyclical. After the 2020-2021 peak when SPACs dominated IPO volume and de-SPAC mergers became the preferred route for many late-stage private companies SPAC activity collapsed in 2022 and 2023 as the SEC tightened the regulatory framework and the post-merger performance of SPAC targets disappointed investors.

The most recent data shows a significant recovery. In Q1 2026, there were 62 SPAC IPOs raising approximately $11.8 billion, approximately four times the volume of the prior year period. This recovery is concentrated among larger SPACs targeting larger deal sizes, not a broad democratisation of the SPAC structure.

The SPAC pathway has specific characteristics that make it appropriate for a narrow set of situations and inappropriate for most. The advantages are speed a de-SPAC merger can be completed in three to four months versus six to twelve months for a traditional IPO and certainty of proceeds, since the SPAC has already raised its capital before identifying the target. The disadvantages include the 2024 SEC SPAC rules, which imposed new disclosure, liability, and underwriter requirements that significantly increased the regulatory cost of de-SPAC transactions, and the persistent structural issue of SPAC dilution, where warrants and redemptions by SPAC shareholders reduce the capital available to the target company.

For a CFO evaluating a SPAC, the relevant question is not whether a SPAC sponsor has expressed interest. It is what the target company will actually receive in cash after redemptions, warrant exercise, and deal costs, and whether the pro forma public company structure with its disclosure obligations and ongoing reporting requirements is one the team can sustain.

What Does a Traditional S-1 IPO Actually Require?

The S-1 IPO is the pathway most founders have in mind when they say "going public." It is also the most demanding in terms of preparation time, management bandwidth, and ongoing compliance cost.

The preparation timeline for a traditional IPO is typically nine to eighteen months from the decision to pursue a listing to the first day of trading. The process includes selecting underwriters, auditing historical financial statements (typically three years for a non-EGC), preparing the registration statement, completing the SEC review process (which now typically uses the confidential DRS process discussed in this series), conducting the road show, and pricing the offering.

The capital raised in a traditional IPO is the only one of the five pathways with no regulatory ceiling. A company that has sufficient institutional investor demand can raise hundreds of millions or billions of dollars in a single IPO. The SpaceX S-1 filed May 20, 2026 targets a raise of $75 billion to $80 billion the largest planned IPO in history.

The cost of a traditional IPO includes underwriter commissions (typically 5% to 7% of the gross proceeds for a standard-size IPO), legal and accounting fees, SEC filing fees, exchange listing fees, and the ongoing annual compliance costs of being a fully reporting public company. According to the data in the anchor blog in this series, post-SOX compliance costs for companies under $1 billion in revenue average $2.8 million to $5 million annually.

For a company with $50 million in annual revenue, those ongoing costs represent 5 to 10% of revenue. The traditional IPO is the right pathway when the company needs institutional-scale capital, when the shareholder base and growth trajectory support sustained exchange listing and analyst coverage, and when the management team and finance function are ready to operate as a fully reporting public company from day one.

What Is a Direct Listing and When Does It Make Sense?

A direct listing allows an existing private company to list its shares on a national exchange without conducting an IPO, raising new capital, or engaging underwriters for the listing event itself. The company's existing shareholders founders, employees, and private investors become able to sell their shares to public investors from the first day of trading.

The Nasdaq Capital Market requirements for a direct listing include a minimum market value of unrestricted publicly held shares (MVUPHS) of $30 million under the valuation-based standard or $37.5 million under the evidence-based standard, and a minimum bid price of $8 per share under the valuation-based standard or $10 per share under the evidence-based standard.

The direct listing pathway is appropriate for a company that does not need to raise new capital in the listing event, wants to provide liquidity to existing shareholders, and has sufficient existing investor interest and brand recognition to generate price discovery without underwriter support. Spotify's 2018 NYSE direct listing is the most prominent example. The company did not raise new capital at listing; it simply allowed its existing shareholders to sell into the public market.

The direct listing is not appropriate for a company that needs to raise capital in the listing transaction. In 2020, the SEC approved a new form of direct listing that permits concurrent capital raising a direct listing with a capital raise. But the structure is operationally complex and rarely used. The practical reality is that direct listings remain primarily a liquidity event for existing shareholders, not a capital raising mechanism for the company.

How Do You Choose Between the Five Pathways?

The decision framework maps to four questions in sequence. Each question eliminates one or more pathways before the next is asked.

Question 1: How much capital does the company need?

If the answer is under $5 million, Reg CF is technically viable but practically difficult at that ceiling. If the answer is $5 million to $75 million, Reg A+ is the only exempt offering pathway that can reach that level. If the answer is above $75 million, the company must use a registered offering a traditional S-1 IPO, a SPAC merger, or a direct listing with capital raise.

Question 2: Does the company need new capital in the transaction, or is the goal primarily liquidity for existing shareholders?

If the goal is primarily liquidity founders and early investors want to sell shares a direct listing is the relevant registered pathway. If the goal is raising new capital for the company, a traditional S-1 IPO or a SPAC merger is the appropriate route.

Question 3: Does the company need the speed and certainty of proceeds that a SPAC offers, or can it manage a nine-to-eighteen-month IPO process?

If timeline certainty and a defined capital amount are critical, a SPAC merger is worth evaluating understanding that the 2024 SPAC rules impose materially higher regulatory and liability costs than the pre-2024 framework. If the company can sustain the IPO timeline, the traditional S-1 process typically produces better outcomes for the issuer in terms of capital raised and post-listing trading performance.

Question 4: Can the company sustain the ongoing reporting obligations of a fully public company?

Both the traditional IPO and the SPAC merger result in a fully reporting public company subject to Exchange Act periodic reporting, SOX certification, and exchange listing standards. If the company's finance function is not ready for those obligations, the listing event is not the right next step regardless of which pathway is chosen.

Frequently Asked Questions

What is the difference between a Reg A+ offering and a traditional S-1 IPO?

A Reg A+ offering is an exempt offering that allows companies to raise up to $75 million from the public without a full S-1 registration statement. Tier 2 requires audited financial statements and ongoing annual and semiannual reporting but is significantly less burdensome than Exchange Act quarterly and annual reporting. A traditional S-1 IPO is a full registered offering with no capital ceiling that results in exchange listing, full Exchange Act reporting, and SOX certification obligations from day one. Reg A+ offerings do not automatically result in exchange listing. The average Tier 2 Reg A raise through December 2025 was approximately $13 million against a $75 million statutory ceiling.

What does the Reg CF data say about Regulation Crowdfunding as a pathway?

Through December 2025, 9,461 Reg CF offerings raised approximately $1.546 billion in total, for an average raise of approximately $359,000. The statutory ceiling is $5 million per 12-month period. The average raise at 7% of the ceiling reflects the structural limitations of the pathway: small investment limits per investor, retail-only capital base, no exchange listing, and limited aftermarket liquidity. Reg CF is appropriate for early-stage companies that want to build community ownership among their customer base and need under $1 million in capital.

What happened to the SPAC market after the 2024 SEC rules?

The 2024 SPAC rules, effective July 2024, imposed new disclosure, liability, and underwriter requirements on de-SPAC transactions that materially increased regulatory and legal costs. SPAC volume declined significantly in 2022 and 2023. Q1 2026 data shows 62 SPAC IPOs raising approximately $11.8 billion, approximately four times the volume of Q1 2025, indicating a recovery in activity. The recovery is concentrated among larger SPACs targeting larger deals rather than a broad return to the 2021 pace.

What are the minimum listing requirements for a direct listing on Nasdaq?

The Nasdaq Capital Market requires a minimum market value of unrestricted publicly held shares of $30 million under the valuation-based standard or $37.5 million under the evidence-based standard, and a minimum bid price of $8 per share (valuation-based) or $10 per share (evidence-based). A direct listing does not raise new capital for the company in the listing event. It provides liquidity for existing shareholders. A concurrent capital raise in a direct listing is permitted but operationally complex and rarely used.

How do you choose between a SPAC merger and a traditional S-1 IPO?

The SPAC advantages are speed (three to four months versus nine to eighteen for a traditional IPO) and certainty of proceeds since the SPAC has already raised its capital. The disadvantages are structural dilution from warrants and redemptions, the higher regulatory cost under the 2024 SPAC rules, and the persistent post-merger performance record of SPAC targets. A traditional S-1 IPO typically produces better capital raised outcomes and post-listing trading performance when the company can sustain the longer timeline. The SPAC is the right choice when timeline certainty and a defined capital amount are the overriding priorities.

What is the ongoing reporting obligation after each pathway?

An S-1 IPO and a SPAC merger both result in a fully reporting public company subject to Exchange Act annual and quarterly reporting, SOX certification, and exchange listing maintenance standards. A Reg A+ Tier 2 offering requires annual and semiannual reports but not quarterly Exchange Act reports. Regulation Crowdfunding requires annual reports while the company has more than 300 crowdfunding security holders and more than $10 million in total assets. A direct listing results in the same full Exchange Act reporting obligations as a traditional IPO.

Key Takeaways

- There are five pathways to access public capital markets: S-1 IPO, Regulation A+, Regulation Crowdfunding, SPAC merger, and direct listing. Each has a different capital ceiling, investor eligibility structure, regulatory cost, and aftermarket outcome. Choosing the wrong one is a material business decision error.

- Regulation A+ through December 2025: 1,531 qualified offerings, approximately $10.5 billion raised, approximately $13 million average Tier 2 raise against a $75 million statutory ceiling. The gap between ceiling and average reflects the aftermarket limitation of offerings without exchange listing or institutional sponsorship.

- Regulation Crowdfunding through December 2025: 9,461 offerings, approximately $1.546 billion total, approximately $359,000 average raise against a $5 million statutory ceiling. This pathway is appropriate for early-stage companies building community ownership, not for companies that need institutional-scale capital.

- SPAC activity recovered in Q1 2026 to 62 IPOs raising approximately $11.8 billion, approximately four times Q1 2025 volume. The 2024 SPAC rules materially increased regulatory costs and liability exposure for de-SPAC transactions. SPAC mergers trade speed and certainty of proceeds against dilution and higher post-merger regulatory burden.

- A direct listing provides liquidity for existing shareholders without raising new capital for the company. It requires meeting Nasdaq minimum MVUPHS thresholds and bid price requirements. It is not a capital-raising mechanism in standard form.

- The decision framework runs in four questions: how much capital is needed, is the goal new capital or shareholder liquidity, can the company manage an IPO timeline, and is the finance function ready for full Exchange Act reporting obligations. Answering these four questions in sequence eliminates most pathways before the fifth is needed.