Goodwill Impairment Disclosure Requirements: 2026 Guide (ASC 350-20 and IAS 36)

Goodwill impairment disclosure requirements sit at the intersection of three distinct obligations: the financial statement note, the MD&A critical accounting estimate, and interim triggering-event disclosures. Most articles cover only one of these layers. Getting any one wrong is the most reliable way to land on the SEC staff's comment letter list.

This guide is for CFOs, controllers, and SEC reporting teams at public companies. It covers exactly what must be disclosed under ASC 350-20 and IAS 36, what the SEC expects in MD&A, where the two frameworks diverge, and what the IASB's active project means for IFRS preparers planning ahead.

Key takeaway: Goodwill impairment disclosures are a three-layer system. The financial statement note, the MD&A critical accounting estimate, and interim triggering-event disclosures are each legally distinct and all required. Treating them as interchangeable is the single most common source of SEC comment letters on goodwill.

What Are the Goodwill Impairment Disclosure Requirements Under ASC 350-20?

Under ASC 350-20, goodwill impairment disclosure requirements fall into three buckets: balance sheet presentation, the goodwill rollforward, and impairment-specific disclosures when a charge is recorded.

Balance Sheet Presentation

ASC 350-20-45-1 requires goodwill to be presented as a separate line item on the balance sheet, net of accumulated impairment losses. The gross amount and accumulated impairment losses must both be disclosed in the notes. This requirement was not changed by ASU 2017-04.

The Goodwill Rollforward (ASC 350-20-50-1)

For each period presented, the notes must include a rollforward showing:

- Gross amount and accumulated impairment losses at the beginning of the period

- Goodwill acquired during the period (excluding goodwill in a disposal group that meets held-for-sale criteria on acquisition)

- Adjustments for deferred tax assets recognised under ASC 805-740

- Goodwill included in a disposal group classified as held for sale under ASC 360-10-45-9, and goodwill derecognised without having previously been in a disposal group

- Impairment losses recognised during the period

- Foreign currency translation differences under ASC 830

- Any other changes in carrying amounts

- Gross amount and accumulated impairment losses at the end of the period

This rollforward must be presented by reportable segment as defined under ASC 280. When reporting units do not align neatly with reportable segments, goodwill is aggregated into the segment to which the reporting unit belongs. Companies that reorganise their segment structure frequently miss this requirement in the transition period.

One line item that is routinely omitted in practice: goodwill in a disposal group classified as held for sale. It is a specific required disclosure under ASC 350-20-50-1 and the SEC staff will notice its absence.

When a Goodwill Impairment Charge Is Recorded (ASC 350-20-50-2)

ASC 350-20-50-2 requires two additional disclosures when an impairment loss is recognised:

- A description of the facts and circumstances leading to the impairment

- The amount of the impairment loss and the method used to determine the fair value of the reporting unit (quoted market prices, prices of comparable businesses, a present value technique, or a combination)

ASU 2017-04, effective for public companies for annual periods beginning after December 15, 2019, eliminated the former Step 2 disclosure (the implied fair value of goodwill). The valuation method disclosure in item 2 above survived that simplification and remains required.

The Level 3 Fair Value Exception: What It Does and Does Not Cover

This is the most widely misunderstood provision in ASC 350-20.

ASC 350-20-50-3 provides that the quantitative disclosures about significant unobservable inputs required by ASC 820-10-50-2(bbb) for Level 3 fair value measurements do NOT apply to goodwill fair value measurements after initial recognition. In plain terms: the note disclosure does not require you to state the specific discount rate or terminal growth rate used in your DCF.

Warning: The Level 3 exception covers the financial statement note only. It does not relieve companies of their MD&A obligation under Regulation S-K Item 303 and SEC FR-72 (Release No. 33-8350) to disclose those same assumptions as part of the critical accounting estimate discussion. The note and MD&A are legally distinct. Both are required.

What Does the SEC Expect in MD&A for Goodwill Impairment?

The SEC treats goodwill impairment as a paradigm critical accounting estimate, and its expectations go well beyond what ASC 350-20-50 requires in the notes.

FR-72 (Release No. 33-8350, December 2003) established the framework: companies must disclose the nature of the estimate, the sensitivity of the estimate to changes in assumptions, and the effect of changes on reported results. For goodwill, that means the MD&A must include:

- The key assumptions used in the impairment test (discount rate, revenue growth rate, operating margins, terminal growth rate)

- How those assumptions were determined

- The degree of uncertainty associated with each assumption

- Potential events or changes in circumstances that could negatively affect the assumptions and result in a material impairment charge

The SEC staff has been explicit about this. A representative comment letter, cited in Deloitte's DART Roadmap on SEC Comment Letter Considerations, Section 2.11, reads:

"A discussion of the degree of uncertainty associated with all of the key assumptions in the discounted cash flow analysis along with the potential impact changes in the key assumptions would have on your impairment analysis. For example, you state that [an X]% increase in the discount rate would result in an additional impairment charge but do not mention assumptions for future revenue growth, operating margin, and the weighted average cost of capital."

Partial sensitivity analysis is not enough. The staff expects every material assumption to be addressed, not just the one that happens to be closest to a threshold.

When Must You Disclose an "At-Risk" Reporting Unit?

When the fair value of a reporting unit does not substantially exceed its carrying value, the SEC expects a specific set of disclosures in MD&A even if no impairment has been recorded.

The SEC staff's standard comment letter language on this point, cited in Deloitte DART Section 2.11, requires:

- The percentage by which fair value exceeded carrying value at the date of the most recent test

- A more detailed description of the methods and key assumptions used, and how they were determined

- A discussion of the degree of uncertainty associated with the assumptions

- A description of potential events and changes in circumstances that could reasonably be expected to negatively affect the key assumptions

The staff cites Item 303(a)(3)(ii) of Regulation S-K and Section V of SEC Release No. 34-48960 as the authority for these demands.

The phrase "substantially exceeds" is not defined in the codification, but in practice the SEC staff treats a headroom of less than 10-15% as a trigger for these enhanced disclosures. If you are in that range, disclosing the headroom percentage proactively is the cleaner approach.

Interim and Between-Annual-Test Disclosure Obligations

Goodwill disclosures do not freeze between annual tests. When triggering events occur, companies must update their disclosures in 10-Qs even if no impairment charge is recorded.

ASC 350-20-35-3C requires an interim impairment test when facts and circumstances indicate that goodwill may be impaired. The qualitative factors in ASC 350-20-35-22 through 35-24 include macroeconomic deterioration, industry and market conditions, cost factors, and overall financial performance. ASC 350-20-35-30 specifically identifies market capitalisation as an indicator: when a company's net book value exceeds its market cap, the SEC staff treats this as strong evidence that an interim test may be required.

A representative SEC comment letter illustrates the staff's position:

"We further note in your 10-Q for the period ended [June Y, year 2]... your net book value currently exceeds your market capitalization. However, we noted no revisions to your disclosures related to goodwill under critical accounting estimates in MD&A in subsequent quarterly filings that address these factors. Please revise future filings to address if and how these factors impacted your determination to test goodwill for impairment as of an interim date and, if not, explain why not. Please also revise future filings to explain if and how you consider market capitalization in determining the estimated fair values of reporting units."

The staff also expects companies to "connect the dots." If a reporting unit's fair value was close to carrying value at year-end, and the company subsequently records a material impairment charge in a later quarter, the staff will ask why no material uncertainty was flagged in the intervening 10-Qs. Silence in interim filings followed by a surprise impairment charge is a reliable path to a comment letter.

What Are the IAS 36 Goodwill Disclosure Requirements?

Under IAS 36, the disclosure requirements for goodwill impairment are more prescriptive than US GAAP, and there is no qualitative assessment option or Level 3 exception.

Under IAS 36 paragraph 90, goodwill must be allocated to cash-generating units (CGUs) or groups of CGUs and tested for impairment annually. Unlike US GAAP, there is no Step 0 qualitative assessment: a quantitative test is always required for goodwill-bearing CGUs.

IAS 36 paragraphs 130-134 set out the disclosure requirements. When a material impairment loss is recognised, the notes must include:

- The events and circumstances that led to the recognition

- The amount of the impairment loss

- The recoverable amount and whether it is fair value less costs of disposal (FVLCD) or value in use (VIU)

- The valuation technique used if recoverable amount is FVLCD

- The discount rate(s) used in the current and previous estimates if recoverable amount is VIU

- The nature of the asset and its reportable segment

Note that IAS 36 paragraph 124 prohibits reversal of goodwill impairment losses. Once recognised, the charge is permanent. This is the same outcome as US GAAP, but it is worth stating explicitly because impairment of other assets under IAS 36 can be reversed.

The IAS 36 Paragraph 134 Disclosures: The Ones Most Preparers Underestimate

IAS 36 paragraph 134 imposes additional disclosures specifically for CGUs carrying goodwill or indefinite-life intangible assets, regardless of whether an impairment loss was recognised. These include:

- The carrying amount of goodwill allocated to the CGU

- The basis of recoverable amount (VIU or FVLCD)

- If VIU: the key assumptions, management's approach to determining values, the projection period, the growth rate used to extrapolate beyond the budget period, and the pre-tax discount rate applied

- A sensitivity analysis: the amount by which the recoverable amount would need to change for the CGU to become impaired, and the key assumptions to which the recoverable amount is most sensitive

The sensitivity analysis in paragraph 134(f) is the requirement most commonly underestimated. It must express headroom in absolute terms and identify the assumptions driving the most risk. Vague statements that "a reasonably possible change in assumptions could result in impairment" do not satisfy the standard.

Under IAS 36, the pre-tax discount rate used in a VIU calculation must be disclosed in the notes under paragraph 134(d)(v). This is a direct contrast with US GAAP, where the Level 3 exception in ASC 350-20-50-3 technically permits omission of that rate from the note (though not from MD&A).

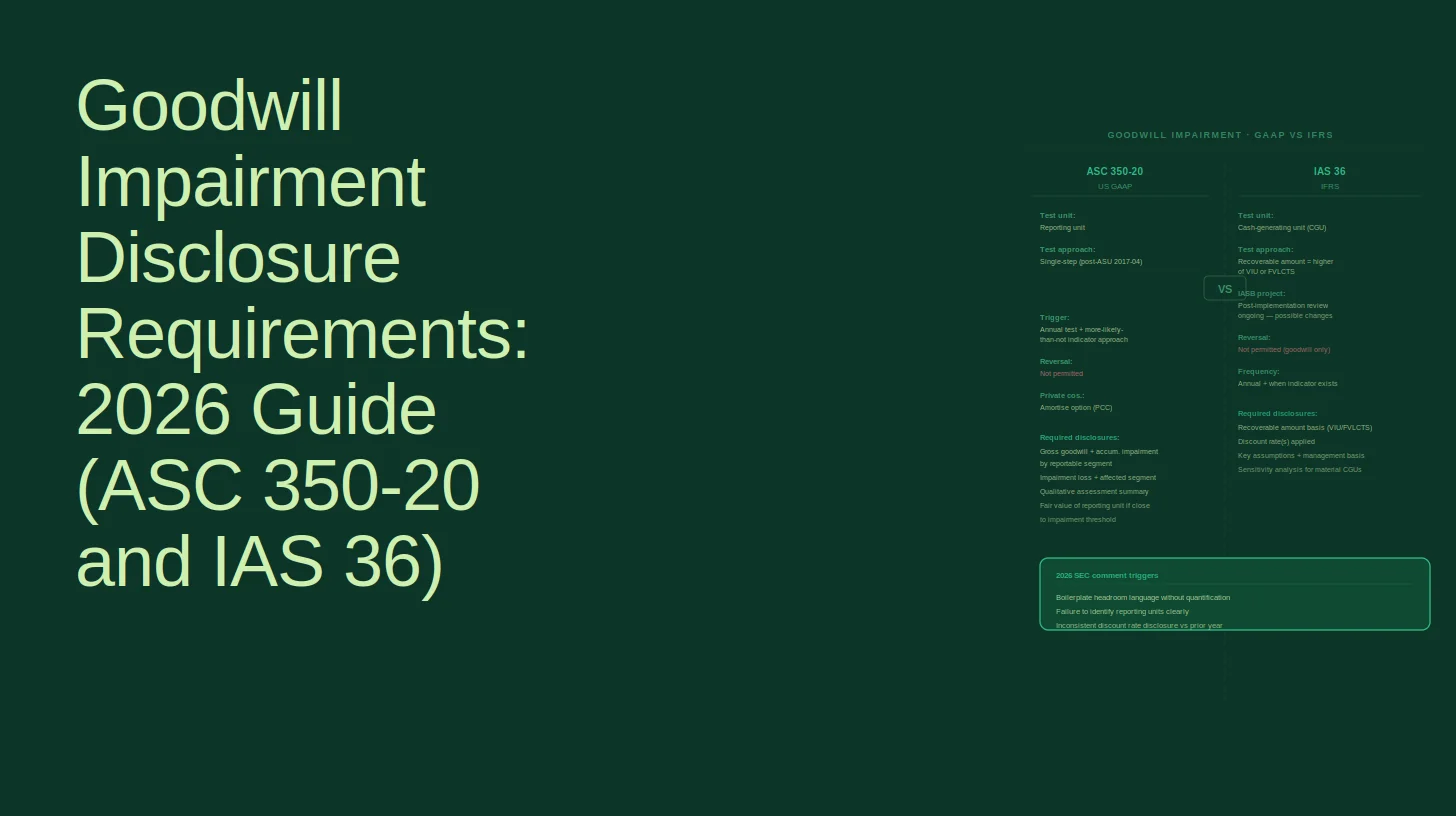

US GAAP vs. IFRS Goodwill Impairment Disclosure Checklist

The table below summarises the key disclosure requirements side by side. Use it as a pre-filing verification tool.

Disclosure ElementUS GAAP (ASC 350-20)IFRS (IAS 36)Annual quantitative test requiredYes (or qualitative Step 0 first)Yes (no qualitative option for goodwill)Goodwill rollforward in notesYes, by reportable segment (ASC 350-20-50-1)Not prescribed in same format; CGU carrying amounts requiredFacts and circumstances on impairmentYes (ASC 350-20-50-2(a))Yes (IAS 36 para 130(a))Amount of impairment chargeYes (ASC 350-20-50-2(b))Yes (IAS 36 para 130(b))Valuation method usedYes (ASC 350-20-50-2(b))Yes, including technique and level (IAS 36 paras 130(e)-(f))Discount rate disclosed in notesNot required (Level 3 exception, ASC 350-20-50-3)Yes, mandatory (IAS 36 para 134(d)(v))Sensitivity analysis in notesNot required in notes; required in MD&AYes, mandatory in notes (IAS 36 para 134(f))MD&A critical accounting estimateYes (Reg S-K Item 303, FR-72)Not applicable (IFRS preparers not subject to SEC MD&A rules unless SEC registrants)At-risk unit headroom percentageSEC expects in MD&AImplied by para 134(f) sensitivity disclosureImpairment reversal permittedNoNo (IAS 36 para 124)Interim triggering event testYes (ASC 350-20-35-3C)Yes (IAS 36 para 9)Private company amortisation optionYes (ASU 2014-02, up to 10 years)No

What Is the Private-Company Alternative and How Does It Change Disclosures?

Private companies and not-for-profits may elect to amortise goodwill under ASC 350-20, which simplifies the impairment test but does not eliminate disclosure obligations.

Under the private-company alternative introduced by ASU 2014-02, goodwill is amortised on a straight-line basis over a period not to exceed 10 years. The impairment test is triggered only by a triggering event, not annually, and is performed at the entity level rather than the reporting unit level.

Key disclosure differences for private companies that elect this alternative:

- The amortisation method, useful life, and aggregate amortisation expense must be disclosed

- Amortisation and any impairment charges are presented within continuing operations on the income statement

- Impairment testing is event-driven, but when a triggering event occurs, the same facts-and-circumstances and valuation method disclosures apply

- The goodwill rollforward still applies, but the entity-level test simplifies the segment-level presentation question

ASU 2021-03 added a further alternative allowing private companies and NFPs to assess triggering events only as of the end of the annual (or interim) reporting period, rather than continuously throughout the year. Companies that elect this option must disclose that election.

What Is the IASB Doing to Change Goodwill Disclosures?

The IASB's Goodwill and Impairment project is the most significant pending change to IFRS goodwill accounting in over a decade, and IFRS preparers should be tracking it now.

The IASB published Discussion Paper DP/2020/1 in March 2020, receiving over 100 comment letters from investors, preparers, and auditors globally. The project is considering:

- Whether to reintroduce amortisation of goodwill under IFRS (currently prohibited)

- New post-acquisition performance disclosures under IFRS 3, including the amount or range of expected synergies at the acquisition date and subsequent performance against those synergies

- A requirement to disclose the acquiree's revenue, operating profit or loss, and cash flows from operating activities since the acquisition date in years after the acquisition (currently only required in the acquisition year under IFRS 3 paragraph B64(q))

As the IASB's May 2019 staff paper AP18A stated: "The Board set the project an objective of exploring whether disclosures could be improved to help investors to assess more effectively whether a business combination was a good investment decision and whether the acquired business is performing after the acquisition as was expected at the time of the acquisition."

The IASB's October 2017 staff paper AP18D identified the core investor complaint: impairment recognition arrives "too little, too late," and sensitivity disclosures are too generic to be useful.

As of mid-2026, no final standard has been issued. An Exposure Draft has been under deliberation. IFRS preparers should monitor the IASB's project page and consider whether voluntary early adoption of enhanced synergy disclosures would reduce the risk of a step-change compliance burden when the standard is finalised.

The Most Common SEC Comment Letter Themes on Goodwill

Based on the comment letter patterns documented in Deloitte DART Section 2.11, the SEC staff consistently challenges:

-

Boilerplate process descriptions. Disclosures that describe how goodwill impairment testing works in general, without providing reporting-unit-specific facts, assumptions, and outcomes. The staff demands entity-specific disclosure, not a restatement of the accounting standard.

-

Incomplete sensitivity analysis. Disclosing the impact of a discount rate change while omitting revenue growth, operating margin, and WACC assumptions. The staff expects all material assumptions to be addressed.

-

Failure to update interim disclosures. When macroeconomic conditions deteriorate between annual tests (rising rates, falling market cap, softening demand), the staff expects 10-Q MD&A to address whether a triggering event occurred and, if not, why not.

-

The market cap / book value gap. When net book value exceeds market capitalisation, the staff cites ASC 350-20-35-30 and expects explicit MD&A disclosure of how management considered this in its impairment assessment.

-

Surprise impairment charges. Recording a material goodwill impairment charge without having flagged any material uncertainty in prior interim filings. The staff will ask why the risk was not visible in the quarterly disclosures that preceded the charge.

-

Misapplying the Level 3 exception. Treating ASC 350-20-50-3 as permission to omit key assumptions from all disclosures, when it only covers the financial statement note, not MD&A.

For companies that have already received a comment letter on goodwill, the Finrep guide to preventing repeat SEC comment letters covers the remediation process in detail. The MD&A disclosure practices that reduce comment letter risk are also addressed in the results-of-operations disclosure guide.

FAQ

How often does goodwill need to be evaluated for impairment?

Under ASC 350-20, public companies must test goodwill for impairment at least annually, on the same date each year. The testing date can be any date during the fiscal year, not just year-end, but must be consistent. An interim test is also required whenever a triggering event under ASC 350-20-35-3C indicates that goodwill may be impaired. Under IAS 36, the annual quantitative test is mandatory for all goodwill-bearing CGUs, with no qualitative option.

Do we have to disclose the discount rate used in our goodwill DCF?

In the financial statement note under US GAAP, no: ASC 350-20-50-3 provides a Level 3 fair value measurement exception that relieves you of that specific quantitative disclosure. In MD&A, yes: Regulation S-K Item 303 and FR-72 require disclosure of key assumptions, including the discount rate, as part of the critical accounting estimate discussion. Under IFRS, yes in all cases: IAS 36 paragraph 134(d)(v) requires the pre-tax discount rate to be disclosed in the notes.

What disclosures are required for intangible assets with indefinite lives?

Under ASC 350-30, indefinite-lived intangible assets must be tested for impairment annually (or more frequently if triggering events occur) and disclosed separately from goodwill on the balance sheet. The same SEC comment letter themes that apply to goodwill apply equally to indefinite-lived intangibles: boilerplate disclosures, incomplete sensitivity analysis, and failure to flag at-risk assets are all common targets.

What does "substantially exceeds" mean for the at-risk reporting unit disclosure?

The term is not defined in ASC 350-20. In practice, the SEC staff has challenged companies where fair value exceeded carrying value by margins that, in context, did not provide meaningful cushion against reasonably possible adverse changes in assumptions. A headroom of less than 10-15% is a practical threshold at which enhanced MD&A disclosures should be considered, though the analysis is always facts-and-circumstances specific.

Can a goodwill impairment loss be reversed?

No. Under both US GAAP (ASC 350-20) and IFRS (IAS 36 paragraph 124), goodwill impairment losses cannot be reversed in a subsequent period, even if the conditions that caused the impairment improve. This is a key difference from the treatment of other long-lived asset impairments under IAS 36, where reversal is permitted when conditions change.

What changes if we elect the private-company goodwill amortisation alternative?

Under ASU 2014-02, goodwill is amortised straight-line over up to 10 years, the impairment test is triggered by events rather than performed annually, and the test is at the entity level rather than the reporting unit level. Disclosure requirements are simplified but not eliminated: the amortisation method, useful life, and any impairment charges must still be disclosed. The election must be applied to all existing and future goodwill.