ASC 820 Fair Value Disclosure Requirements: 2026 Compliance Guide

If you're preparing a 10-K or 10-Q fair value footnote, the question isn't whether ASC 820 applies. It's which of its three disclosure tracks applies to each line item, what ASU 2018-13 changed that your checklist may not reflect, and where SEC staff are most likely to push back. This guide answers all three.

Key takeaway: ASC 820 organises fair value disclosures into three distinct tracks, each with different requirements. Confusing them is the most common preparer error, and it's exactly what SEC comment letters target.

How Does ASC 820 Define Fair Value?

ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. That's an exit-price notion, not an entry price or a liquidation value. The definition has been unchanged since ASU 2011-04 aligned it with IFRS 13 in May 2011.

The three objectives driving every specific disclosure requirement are: (1) the valuation techniques and inputs used, including judgments and assumptions; (2) the uncertainty in fair value measurements as of the reporting date; and (3) how changes in fair value measurements affect performance and cash flows. If a disclosure doesn't serve one of those three objectives, it's probably not required.

What Is Actually in Scope for ASC 820 Disclosures?

Per ASC 820-10-50-1C, the disclosure requirements apply to assets and liabilities measured at fair value on a recurring or nonrecurring basis, plus financial instruments not measured at fair value on the balance sheet but for which fair value is disclosed under other GAAP (e.g., ASC 825-10-50).

That sounds broad. The exclusion list is what narrows it, and it's long.

What ASC 820 Disclosures Do NOT Apply To

The following are explicitly carved out of ASC 820's disclosure requirements. Misapplying these exclusions is one of the most common preparer errors, per Deloitte's ASC 820 Roadmap:

- Share-based payment transactions (ASC 718)

- Lease contracts as defined in ASC 842 (contingent obligations from cancelled leases are not excluded)

- Pension, postretirement, and postemployment benefit obligations (ASC 710, 712, 715)

- Insurance contracts other than financial guarantees (ASC 944)

- Warranty obligations (ASC 450, ASC 460)

- Unconditional purchase obligations (ASC 440-10-50-2)

- Equity method investments (ASC 323)

- Noncontrolling interests and equity investments in consolidated subsidiaries (ASC 810)

- Equity instruments classified in stockholders' equity (ASC 505)

- Receive-variable, pay-fixed interest rate swaps under the simplified hedge accounting approach (ASC 815)

- Fully benefit-responsive investment contracts in employee benefit plans

- Equity securities without readily determinable fair values (ASC 321)

- Trade receivables and payables due within one year

- Deposit liabilities with no defined maturities

- Liabilities from prepaid stored-value products (ASC 405-20-40-3)

Note the interaction with ASC 815: standard interest rate swaps measured at settlement value under the simplified hedge accounting approach are excluded, but EY's September 2025 comprehensive guide confirms that ASC 820's disclosure requirements continue to apply to swaps measured at fair value outside that simplified approach.

The Three Disclosure Tracks: Recurring, Nonrecurring, and Disclosed-Only

This is the framework most practitioners need but almost no existing guidance explains clearly. Which track an item falls into determines exactly which disclosures are required.

TrackDescriptionExampleRoll-Forward Required?Quantitative Inputs Table?Track 1: RecurringMeasured at FV on the balance sheet every periodEquity securities, derivatives, trading debt securitiesYes (Level 3 only)Yes (Level 3)Track 2: NonrecurringMeasured at FV only in certain periods (e.g., impairment)Goodwill post-impairment, long-lived assets held for saleNoYes (Level 3)Track 3: Disclosed-onlyCarried at amortised cost; FV disclosed in footnotesFixed-rate long-term debt under ASC 470NoNo

Track 3 is the most underappreciated. Under ASC 820-10-50-2E, items not measured at fair value on the balance sheet but for which fair value is disclosed (think fixed-rate long-term debt) require only the hierarchy level classification and the fair value amount. The full Level 3 quantitative inputs table, the valuation technique description, and the roll-forward are not required. Entities can voluntarily include those disclosures, but must apply a rational and consistent policy if they do.

For nonrecurring measurements (Track 2), the Level 3 roll-forward is also not required. Many preparers include it anyway, which isn't wrong, but it's not mandated.

What Changed Under ASU 2018-13: Before and After

ASU 2018-13 was effective for fiscal years beginning after December 15, 2019. Calendar-year public companies have been subject to it since their fiscal year 2020 annual reports. As of 2026, that's six full fiscal years. Yet preparers still apply pre-2018 checklists.

CategoryPre-ASU 2018-13Post-ASU 2018-13RemovedDisclose amount of and reasons for Level 1/Level 2 transfersNo longer requiredRemovedDisclose policy for timing of transfers between levelsNo longer requiredRemovedDisclose valuation processes for Level 3 measurementsNo longer requiredModifiedNAV timing of liquidation: always requiredNow required only if the investee has communicated the timingModifiedLevel 3 sensitivity: narrative descriptionNow specifically requires sensitivity to changes in unobservable inputs AND interrelationships between inputsAdded(Not previously required)Changes in unrealised gains/losses included in OCI for recurring Level 3 items held at period endAdded(Not previously required)Range and weighted average of significant unobservable inputs (or other quantitative information) for Level 3

The removal of the valuation processes disclosure is the one most often missed. Pre-2018 footnotes routinely described the entity's internal valuation committee, pricing governance, and challenge processes. That's no longer required under ASC 820, though auditors may still expect it internally.

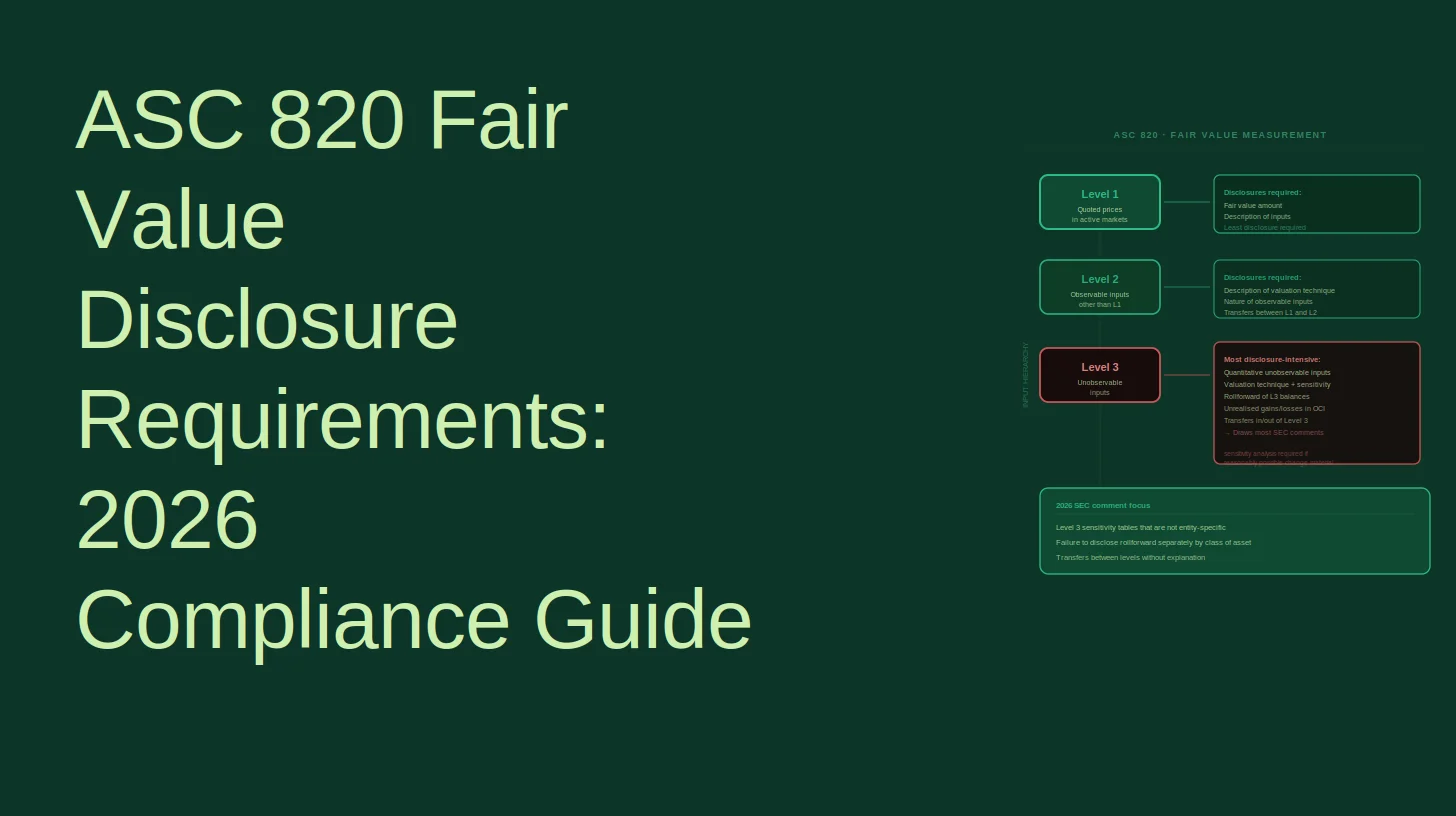

Level 3 Disclosures: What You Must Include

For recurring Level 3 measurements, ASC 820 requires the most extensive disclosure package in the standard. The requirements are:

- The fair value hierarchy table showing the Level 3 balance at the reporting date, disaggregated by class of asset or liability.

- Valuation technique(s) and inputs used (e.g., discounted cash flow, Black-Scholes, market comparable approach).

- Quantitative information about significant unobservable inputs including, post-ASU 2018-13, the range and weighted average of those inputs.

- The Level 3 roll-forward, reconciling opening to closing balance and showing: total gains/losses (realised and unrealised), purchases, sales, issuances, settlements, and transfers into and out of Level 3.

- Changes in unrealised gains/losses included in OCI for items held at period end (added by ASU 2018-13).

- A narrative sensitivity disclosure describing how the fair value measurement would change if significant unobservable inputs were changed to reflect reasonably possible alternative assumptions, and the interrelationships between those inputs.

The Quantitative Inputs Carve-Out: Widely Misunderstood

ASC 820 contains a carve-out that many preparers either over-apply or under-apply. As Deloitte's Roadmap states directly:

"A reporting entity is not required to create quantitative information to comply with this disclosure requirement if quantitative unobservable inputs are not developed by the reporting entity when measuring fair value (for example, when a reporting entity uses prices from prior transactions or third-party pricing information without adjustment). However, when providing this disclosure, a reporting entity cannot ignore quantitative unobservable inputs that are significant to the fair value measurement and are reasonably available to the reporting entity."

The practical implication: if your treasury team takes a third-party pricing service's output and applies it without adjustment, you don't have to reverse-engineer the model to populate the quantitative inputs table. But if you adjust the third-party price, or if you know the significant inputs and they're reasonably available, you can't claim the carve-out. SEC staff have pushed back on entities that appeared to use the carve-out as a shield against disclosure rather than as a genuine reflection of their valuation process.

ASU 2022-03: New Disclosures for Lock-Up Equity Securities (Now Fully Effective)

ASU 2022-03 clarified that a contractual restriction on the sale of an equity security is not part of the unit of account and therefore cannot reduce the fair value measurement. No lock-up discount is permitted.

More practically for disclosure purposes, ASU 2022-03 added three new required disclosures for equity securities subject to contractual sale restrictions:

- The fair value of those securities reflected in the balance sheet.

- The nature and remaining duration of the restriction(s).

- The circumstances that could cause a lapse in the restriction(s).

Effective dates: Public business entities, fiscal years beginning after December 15, 2023 (calendar-year 2024 and beyond). All other entities, fiscal years beginning after December 15, 2024 (calendar-year 2025 and beyond). As of mid-2026, both public and non-public calendar-year entities are fully subject to these requirements.

One transition nuance flagged by EY's September 2025 guide: the guidance is applied prospectively, with special provisions for investment companies under ASC 946 that previously applied a discount for contractual sale restrictions. Those entities must unwind that practice prospectively, not retrospectively.

Aggregation and Disaggregation: The Principles-Based Judgement That Draws Comments

ASC 820 does not define a bright-line rule for how granular "classes" of assets and liabilities must be in the fair value hierarchy table. Instead, it requires entities to consider: the level of detail necessary to satisfy the disclosure objectives; how much aggregation or disaggregation to undertake; and whether users need additional information to evaluate the quantitative information disclosed.

In practice, this means a company with a diverse portfolio of Level 3 investments cannot simply lump them all into a single "other investments" line. SEC staff have commented on disclosures that aggregate dissimilar instruments with different risk profiles, different valuation techniques, and different unobservable inputs into a single class. The test is whether a reader can understand the nature of the measurement uncertainty from the disclosure as presented.

A reasonable starting point: disaggregate by instrument type (corporate bonds, equity securities, real estate, structured products) and then consider whether instruments within a type share similar valuation techniques and inputs. If they don't, further disaggregation is likely warranted.

The NAV Practical Expedient

For investments in certain entities that calculate net asset value per share (or its equivalent), ASC 820 permits a practical expedient: the NAV may be used as a measure of fair value without further adjustment, and those investments are excluded from the fair value hierarchy table entirely.

Disclosures required for NAV-measured investments include the fair value amount, the nature of the investment, any unfunded commitments, redemption terms, and restrictions. Post-ASU 2018-13, the timing of liquidation of investee assets and the date when redemption restrictions might lapse need only be disclosed if the investee has communicated that information. This is a meaningful change from the pre-2018 requirement, which required disclosure regardless of whether the investee had provided the information.

ASC 820 vs. IFRS 13: What Dual Reporters Need to Know

The FASB and IASB issued substantially converged requirements in May 2011, with IFRS 13 and ASU 2011-04 issued simultaneously. As IASB Chairman Sir David Tweedie said at the time: "The finalisation of this project marks the completion of a major convergence project and is a fundamentally important element of our joint response to the global financial crisis."

For most disclosures, dual reporters can align their ASC 820 and IFRS 13 footnotes. The key remaining difference: IFRS 13 requires a quantitative sensitivity analysis for Level 3 measurements, showing the effect of reasonably possible alternative assumptions on fair value. ASC 820's post-ASU 2018-13 requirement is a narrative description of sensitivity and interrelationships. IFRS 13's requirement is more prescriptive and typically more burdensome. Companies filing both a 10-K and an IFRS-based annual report should build the IFRS 13 quantitative sensitivity table first, then use it to inform (and simplify) the ASC 820 narrative.

Note also that non-public entities under US GAAP are exempt from several disclosure requirements that apply to public entities, a distinction that has no direct IFRS 13 parallel.

SEC Comment Letter Patterns on ASC 820 Disclosures

As EY's September 2025 guide notes: "The Securities and Exchange Commission (SEC) staff continues to ask registrants for additional information and disclosures about fair value measurements."

The most common comment themes, based on the dossier and SEC staff guidance:

- Thin Level 3 quantitative inputs tables. Staff ask for the specific unobservable inputs used (e.g., discount rates, revenue growth rates, EBITDA multiples), their ranges, and weighted averages. Disclosures that list only the valuation technique without the inputs draw comments.

- Sensitivity disclosures that are generic. Boilerplate language like "a change in the discount rate would affect fair value" without specifying direction, magnitude, or interrelationships is a frequent target.

- Valuation technique changes without explanation. If you changed from one approach to another between periods, ASC 820 requires disclosure of the change and the reason. Staff notice when the technique changes but no disclosure appears.

- Aggregation that obscures risk. Lumping dissimilar Level 3 instruments into a single class, as discussed above.

- Missing ASU 2022-03 disclosures. For entities holding lock-up equity securities, the three new required disclosures are now in scope and SEC staff are checking for them.

One structural factor amplifies this risk: the SEC's EDGAR XBRL taxonomy includes a specific element for the entire ASC 820 fair value disclosure, referencing ASC 820-10-50-2. That means SEC staff can programmatically screen fair value disclosures across all registrants and flag outliers. Thin or inconsistent disclosures are easier to identify at scale than they were in a paper-filing world.

For a broader framework on avoiding repeat SEC comments, see How to Prevent Repeat SEC Comment Letters: A 2026 Process Guide for CFOs. For the interaction between disclosure controls and material weakness risk, Material Weakness Disclosure Requirements: 2026 SEC Compliance Guide covers the SOX 404 dimension.

FAQ

Are private companies required to disclose the fair value of debt under ASC 820?

Private companies (non-public entities) that carry long-term debt at amortised cost are generally required by ASC 825-10-50 to disclose its fair value, which then triggers the lighter-touch Track 3 disclosures under ASC 820-10-50-2E: hierarchy level and fair value amount. The full Level 3 quantitative inputs table is not required for Track 3 items. Non-public entities are also exempt from several other ASC 820 disclosure requirements that apply to public business entities.

Does GAAP allow fair value accounting?

Yes. US GAAP both requires and permits fair value measurement in various contexts. ASC 820 governs how to measure and disclose fair value when another standard requires or permits it. ASC 825 (Financial Instruments) provides a fair value option for many financial instruments. ASC 820 does not itself specify when fair value measurement is required; that determination comes from the specific standard governing the asset or liability.

What is the ASC for the fair value option?

The fair value option is governed by ASC 825-10 (Financial Instruments, Subtopic 10). When an entity elects the fair value option for an eligible instrument, ASC 820's full measurement and disclosure requirements apply to that instrument on a recurring basis.

When is the Level 3 roll-forward not required?

The roll-forward is required only for recurring Level 3 fair value measurements. It is not required for nonrecurring measurements (Track 2) or for items in the disclosed-only track (Track 3). It is also not required for investments measured using the NAV practical expedient, since those are excluded from the hierarchy table entirely.

What transfers between Level 1 and Level 2 must we disclose post-ASU 2018-13?

ASU 2018-13 removed the requirement to disclose the amount of and reasons for transfers between Level 1 and Level 2. Transfers into and out of Level 3 must still be disclosed in the roll-forward, including the policy for when transfers are recognised (beginning or end of the reporting period).

How does XBRL tagging affect ASC 820 comment letter risk?

The SEC's EDGAR taxonomy includes a specific XBRL element for ASC 820-10-50-2 fair value disclosures. This allows SEC staff to run programmatic screens across all registrants, comparing disclosure depth and consistency. Entities with thin or inconsistent tagging are more likely to receive a comment. Ensuring your XBRL tags accurately reflect the substance of the footnote is as important as the footnote itself. See Newly Public Company XBRL Obligations: 2026 Compliance Timeline for the broader tagging framework.