ASC 718 Stock Compensation Disclosures: 2026 Compliance Checklist

If you prepare, review, or audit a stock compensation footnote, this guide is for you. ASC 718 sets out a disclosure framework that is far more granular than most footnotes reflect, and SEC staff comment letters prove it. This checklist maps every required element to its codification paragraph, flags the most common audit and SEC review failures, and covers what changes in 2027 under ASU 2024-03.

Key takeaway: ASC 718-10-50 has four disclosure objectives. Every required line item flows from one of them. Build your footnote around those four objectives and you will not miss anything material.

What Are the Four ASC 718 Disclosure Objectives?

The entire ASC 718 disclosure framework rests on four objectives stated in ASC 718-10-50-1. Users of the financial statements must be able to understand:

- The nature and general terms of share-based payment arrangements

- The effect of compensation cost on the income statement

- The method and assumptions used to estimate fair value

- The cash flow effects of share-based payment arrangements

As Deloitte's DART roadmap puts it, "ASC 718-10-50-2 and 50-2A outline the 'minimum information' an entity must disclose in its annual financial statements to achieve the four objectives specified in ASC 718-10-50-1." Think of the checklist below as the mandatory floor, not the ceiling.

Annual Disclosure Checklist: Every Required Element

The table below maps each minimum disclosure to its codification paragraph and flags the items most frequently cited in SEC comment letters.

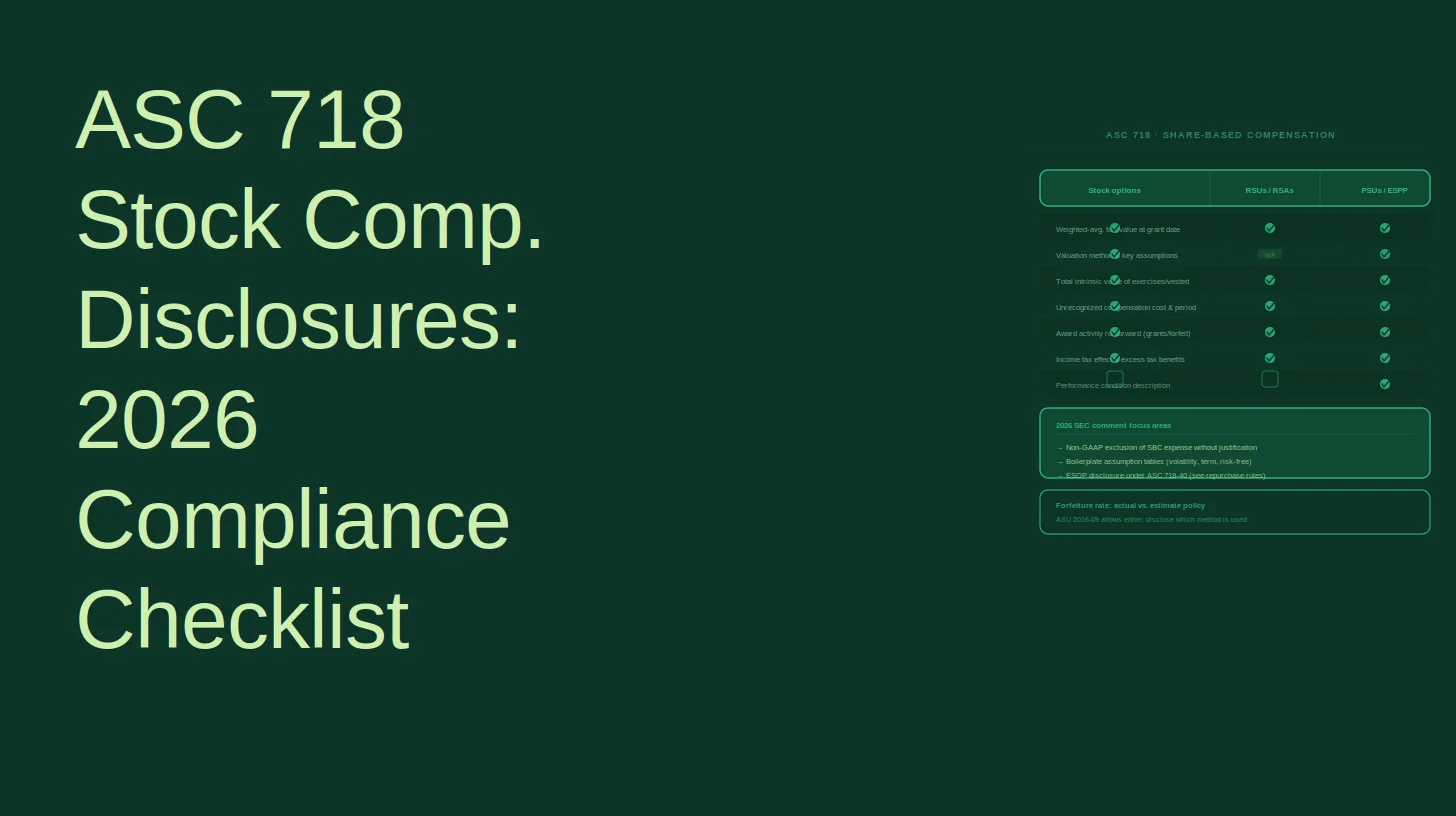

Disclosure ElementASC 718 ParagraphSEC Comment RiskDescription of arrangement(s): requisite service periods, maximum contractual term, shares authorized718-10-50-2(a)LowMethod used to measure compensation cost718-10-50-2(b)LowOption rollforward (outstanding, exercisable, granted, exercised, forfeited, expired) with weighted-average exercise prices718-10-50-2(c)(1)MediumNon-vested instrument rollforward (nonvested, granted, vested, forfeited) with weighted-average grant-date fair values718-10-50-2(c)(2)MediumWeighted-average grant-date fair value of options granted during the year718-10-50-2(d)LowTotal intrinsic value of options exercised, share-based liabilities paid, fair value of shares vested718-10-50-2(d)LowVested and expected-to-vest options: number, weighted-average exercise price, aggregate intrinsic value, weighted-average remaining term718-10-50-2(e)LowValuation model and significant assumptions (expected term, volatility, dividends, risk-free rate)718-10-50-2(f)HighTotal compensation cost recognized and related tax benefit718-10-50-2(i)HighTotal compensation cost capitalized718-10-50-2(i)LowUnrecognized compensation cost and weighted-average recognition period718-10-50-2(j)HighDescription of significant modifications718-10-50-2(k)HighForfeiture policy election (estimate vs. actual)ASU 2016-09 / 718-10-35-1DMediumTax benefit recognized in income statement (post-ASU 2016-09)ASU 2016-09HighLiability-classified award disclosures (intrinsic value outstanding, cash paid to settle)718-10-50-2MediumESPP: plan terms, shares purchased, weighted-average fair value of purchase rights718-10-50-2Medium

Rollforward Tables: Options vs. RSUs vs. PSUs

Options require a separate rollforward from non-vested full-value awards. The option rollforward (ASC 718-10-50-2(c)(1)) must show beginning and ending balances, exercisable shares, and activity during the year (granted, exercised, forfeited, expired), each with weighted-average exercise prices.

For RSUs and PSUs, the non-vested rollforward (ASC 718-10-50-2(c)(2)) tracks beginning and ending nonvested balances plus granted, vested, and forfeited activity, each with weighted-average grant-date fair values. A critical point that practitioners frequently miss: performance-condition awards and market-condition awards should not be aggregated in the same rollforward row if their terms are materially different. SEC staff have asked companies to disaggregate PSU rollforwards when the performance and market condition tranches have different probability profiles.

For above-target or below-target PSU payouts, the shares paid above target are typically shown as an additional rollforward line rather than as new grants. Shares forfeited due to underperformance are often included in the cancellation line, with a footnote explaining the combination.

Valuation Assumptions: What Granularity Does the SEC Expect?

This is the single highest-risk area in the ASC 718 footnote. Under ASC 718-10-50-2(f), for each year an income statement is presented (not just the current year), you must disclose:

- The valuation model (Black-Scholes-Merton, Monte Carlo, lattice)

- Expected term

- Expected volatility, including the methodology (historical, implied, or blended)

- Expected dividends

- Risk-free interest rate

For companies using Monte Carlo simulation for market-condition awards (TSR-based PSUs), the disclosure must describe the model's key assumptions: peer group correlation, peer group volatility, risk-free rate, and dividend yield. As one technology company disclosed in a 10-Q: "We use the Black-Scholes-Merton ('BSM') option pricing model to value stock-based compensation for all equity awards, except market-based awards, which are valued using the Monte Carlo valuation model." Many companies provide robust BSM disclosures but then describe Monte Carlo inputs in a single generic sentence. SEC staff notice the asymmetry.

SAB Topic 14 adds supplemental requirements beyond the codification. For newly public companies or those with limited trading history, SAB Topic 14 requires disclosure of how the peer group was selected for volatility estimation, and whether the simplified method was used for expected term. If you are still using the simplified method, you must disclose that election and confirm you still qualify to use it. SEC staff have asked companies to explain why they continue to use the simplified method years after going public.

Unrecognized Compensation Cost: Disaggregate by Award Type

ASC 718-10-50-2(j) requires disclosure of unrecognized compensation cost and the weighted-average period over which it will be recognized. This is one of the most frequently cited items in SEC comment letters. The codification does not explicitly require disaggregation by award type, but SEC staff routinely ask companies that present a single aggregate number to break it out by options, RSUs, and PSUs separately.

Best practice: present unrecognized cost and the weighted-average recognition period for each award type in a small table. It takes two additional rows and eliminates a predictable comment.

Forfeiture Policy: Disclose the Election

ASU 2016-09 (effective for public entities for fiscal years beginning after December 15, 2016) gave companies a choice: estimate forfeitures at grant date, or account for them as they occur. Whichever method you chose, it must be disclosed as an accounting policy. Companies that elected actual forfeitures sometimes omit this disclosure, treating it as obvious. It is not obvious to a reader, and it is required.

ASU 2016-09 also moved excess tax benefits and deficiencies from additional paid-in capital to the income statement. The tax benefit recognized in the income statement must be disclosed for each period presented. This is a separate line from the tax benefit disclosed under ASC 718-10-50-2(i), and SEC staff have cited companies that omit it.

Modification Accounting Disclosures

When awards are modified, ASC 718-10-50-2(k) requires disclosure of: the terms of the modification, the number of employees affected, and the total incremental compensation cost resulting from the modification.

Modification accounting under ASC 718-10-25-20 through 25-22 triggers recognition of incremental fair value as additional compensation cost. The disclosure obligation follows automatically. Tender offers and repricing events are the most common triggers, but any change to terms (accelerated vesting for a departing executive, extension of the post-termination exercise window) that increases fair value is a modification.

A point that is consistently underexplained: the grant-date fair value shown in the rollforward table does not change upon modification. The incremental cost is recognized separately. If your financial reporting system tracks only one fair value per award, you may need a manual adjustment to ensure the footnote is correct.

Liability-Classified Awards and ESPPs

Companies with both equity-classified and liability-classified awards (cash-settled SARs, phantom stock, cash-settled RSUs) must provide separate disclosures for each. For liability awards, ASC 718-10-50-2 requires disclosure of the total intrinsic value of liability awards outstanding and the total cash paid to settle liability awards during the period. These disclosures are routinely omitted by companies that focus their footnote entirely on equity-classified awards.

For Employee Stock Purchase Plans, the required disclosures include plan terms (purchase price, offering period, contribution limits), shares purchased, weighted-average fair value of purchase rights, and compensation cost recognized. Plans with look-back features require specific valuation assumption disclosure, including the expected term of the purchase right and the volatility assumption. PwC's Financial Statement Presentation Guide notes that "ASC 718 requires disclosure of awards granted during the year regardless of whether compensation expense has been recognized" -- a point that catches ESPP teams off guard when a new offering period starts late in the fiscal year.

Performance Conditions vs. Market Conditions: Different Disclosure Rules

The classification of a vesting condition as a performance condition or a market condition drives materially different accounting and disclosure. Get this wrong and the entire valuation and expense pattern is misstated.

- Performance conditions (metrics within the company's control, such as revenue targets or EBITDA thresholds): compensation cost is recognized only if achievement is probable. The disclosure must describe the condition and the probability assessment. Specific targets may be omitted if disclosure would be competitively harmful, but the probability methodology must still be described.

- Market conditions (metrics tied to stock price or external indices, such as TSR): compensation cost is recognized regardless of whether the condition is achieved, as long as service is rendered. No reversal if the market condition is not met. The Monte Carlo assumptions must be disclosed.

ESG-Linked Awards: A Growing Disclosure Challenge

ESG-linked equity awards, where vesting depends on sustainability metrics such as emissions reductions, diversity targets, or third-party ESG scores, are increasingly common. Under ASC 718, these are classified as:

- Performance conditions if the metric is within the company's operational control (e.g., an internal carbon reduction target)

- Market conditions if tied to an external index or peer ranking (e.g., a relative ESG score)

The disclosure must clearly describe the vesting condition, the measurement methodology, and the probability assessment. SEC staff have begun asking comment letter questions about how companies are classifying ESG-linked conditions and whether the probability disclosure is sufficient. Companies that describe ESG awards only in the proxy statement and not in the ASC 718 footnote are particularly exposed.

Public vs. Private Company Disclosure Differences

Private companies have three practical expedients not available to public companies, each with its own disclosure requirement.

ExpedientStandardDisclosure RequiredCalculated value method (use industry sector index volatility instead of own stock price)ASC 718-10-30-20Disclose election and index usedIntrinsic value method for liability-classified awardsASC 718-10-30-21Disclose election; no fair value assumption disclosure required for those awardsCurrent share price practical expedient (use 409A or reasonable valuation method)ASU 2021-07Disclose election and valuation method used

ASU 2021-07 is effective for private companies for fiscal years beginning after December 15, 2021. It allows private companies to use a "reasonable application of a reasonable valuation method" (including the IRS Section 409A safe harbor) to determine the current share price for option awards, rather than requiring a full ASC 820 fair value measurement. Companies electing this expedient must disclose both the election and the method used.

Pre-IPO companies face a transition challenge: the practical expedients available as a private company are not available after going public. The S-1 registration statement will need to present financial statements that comply with public-company disclosure requirements, including full fair value assumption disclosure under SAB Topic 14 for periods presented. See Mastering S-1 Disclosures: Avoiding Critical Errors in Your IPO for the broader IPO disclosure picture.

For ESOP-specific disclosure obligations, which sit at the intersection of ASC 718 and ERISA reporting, see ESOP Repurchase Obligation SEC Disclosure: 2026 Compliance Guide.

Interaction with Regulation S-K Item 402 and SAB Topic 14

ASC 718 footnote disclosures and Regulation S-K Item 402 executive compensation tables are related but distinct. The grant-date fair value column in the Summary Compensation Table must be computed in accordance with ASC 718, per SEC Regulation S-K Item 402. The Grants of Plan-Based Awards table and Outstanding Equity Awards at Fiscal Year-End table also draw directly from ASC 718 data.

Companies should cross-reference these proxy tables to the ASC 718 footnote. Inconsistencies between the two, even if explainable, draw SEC questions.

SAB Topic 14 also requires that valuation assumptions be disclosed in MD&A, not just in the financial statement footnotes. Many companies satisfy the footnote requirement and forget the MD&A layer entirely.

Quarterly (Interim) Disclosure Requirements

Annual ASC 718 disclosures are more extensive than quarterly ones. Under ASC 270-10-50-1, interim disclosures focus on material changes in estimates (forfeiture rates, performance condition probability) and significant modifications. The full rollforward tables, valuation assumption disclosure, and unrecognized cost schedule are annual requirements.

However, SEC registrants filing Form 10-Q must update the stock compensation footnote if there are material changes from the annual disclosure. If a large block of PSUs was modified in Q2, or if a significant change in performance condition probability occurred, that must be disclosed in the 10-Q even though the full annual disclosure is not required.

What Changes in 2027: ASU 2024-03 Income Statement Disaggregation

This is the most significant near-term change to ASC 718 disclosure practice, and almost no existing guidance addresses it in the context of stock compensation.

ASU 2024-03 (Disaggregation of Income Statement Expenses, Subtopic 220-40) requires public business entities to disclose, in the notes, the amounts of employee compensation (including stock-based compensation) included in each relevant income statement expense caption. Effective for annual periods beginning after December 15, 2026, calendar-year public companies must first apply it in their 2027 annual reports (the 10-K filed in early 2028), with interim adoption required in the first quarter of 2028.

What this means in practice:

- You will need to break out stock-based compensation separately within cost of revenues, R&D, SG&A, and any other income statement line where it is included

- Many companies currently disclose only total stock-based compensation expense in the footnote, with a single line in the cash flow statement reconciliation

- ASU 2024-03 requires the disaggregated view by P&L line, which most equity administration systems do not currently capture at that level of granularity

- Early adoption is permitted, and companies with complex equity programs should start mapping their data now

This is an operational challenge as much as a disclosure one. If your equity plan administration system allocates stock comp expense to cost centers but not to income statement line items, you will need a new data layer before the 2027 close.

Interaction with the 1% Excise Tax and CAMT

Two provisions of the Inflation Reduction Act of 2022 create direct financial statement interactions with ASC 718 disclosures that are almost entirely absent from existing guidance.

1% excise tax on stock repurchases (IRC Section 4501): The tax applies to net repurchases. Shares issued under employee compensation plans reduce the taxable base, per IRS proposed regulations. Companies must track shares issued under ASC 718 plans to calculate the netting offset, and the excise tax liability (or offset) should be disclosed in the financial statements. The ASC 718 footnote is the natural home for the disclosure of shares issued under compensation plans that reduce the excise tax base.

Corporate Alternative Minimum Tax (CAMT): CAMT uses adjusted financial statement income, which includes stock-based compensation expense. This can create deferred tax implications that must be disclosed under ASC 740. The KPMG Handbook on Share-Based Payments (4th edition, 2024) specifically addresses the interaction between ASC 718 and ASC 740, including deferred tax assets related to stock compensation and the treatment of excess tax benefits post-ASU 2016-09.

Common SEC Comment Letter Themes on ASC 718

Based on SEC staff comment letters from 2023 through mid-2026, the most frequently cited ASC 718 issues are:

-

Insufficient volatility methodology description. Staff ask companies to explain how they selected the peer group for volatility estimation, especially for companies that went public within the last three to five years. A generic statement that "volatility is based on historical prices of comparable companies" does not satisfy SAB Topic 14.

-

Simplified method still in use without justification. If you are using the simplified method for expected term, you must disclose the election and explain why you still qualify. Staff have asked companies with several years of post-IPO exercise history to justify continued use.

-

Performance condition probability disclosure is vague. Statements like "management believes achievement is probable" without describing the methodology draw follow-up questions. Staff want to understand the process, not just the conclusion.

-

Unrecognized compensation cost is aggregated. A single number covering options, RSUs, and PSUs is technically compliant but draws disaggregation requests. Present it by award type.

-

Tax benefit in the income statement is missing. Post-ASU 2016-09, the excess tax benefit recognized in the income statement is a required disclosure. Many companies include it in the tax footnote but not in the stock compensation footnote. Staff cite both.

-

Modification disclosures are incomplete. When a modification occurs, the description must cover the terms, the number of employees affected, and the total incremental cost. One-line disclosures that say only "certain awards were modified" are consistently flagged.

-

Monte Carlo assumptions are underspecified. Companies that use Monte Carlo for TSR-based PSUs often provide less detail on those assumptions than they do for BSM options. Staff expect symmetry.

-

Multi-plan aggregation obscures material differences. If you have a broad-based RSU plan and a separate executive PSU plan with materially different terms, aggregating them into a single rollforward table draws a request to disaggregate.

Retirement-Eligibility Provisions: A Frequently Missed Disclosure

For awards with provisions that accelerate or continue vesting upon retirement, ASC 718 requires compensation cost to be recognized over the period from grant date to the date retirement eligibility is achieved, if that date is earlier than the nominal vesting date. For employees who are already retirement-eligible at grant date, the full cost must be recognized immediately.

As one large retailer disclosed in its fiscal year 2015 10-K: "For awards with such provisions, the Company recognizes compensation expense over the period from the grant date to the date retirement eligibility is achieved, if that is expected to occur during the nominal vesting period." The disclosure must describe both the policy and the amount recognized immediately for retirement-eligible grantees. This is a common source of errors in companies with senior executive populations.

FAQ

Does ASC 718 require disclosure of awards granted even if no expense has been recognized?Yes. ASC 718 requires disclosure of awards granted during the year regardless of whether compensation expense has been recognized. This catches companies off guard when awards are granted late in the year with performance conditions that make recognition uncertain at year-end.

What is the difference between annual and quarterly ASC 718 disclosure requirements?Annual requirements include the full rollforward tables, valuation assumption disclosure, unrecognized compensation cost schedule, and modification disclosures. Quarterly requirements under ASC 270-10-50-1 are limited to material changes in estimates and significant modifications, but SEC registrants must update the footnote in any 10-Q where material changes have occurred.

When does ASU 2024-03 require stock-based compensation to be broken out by P&L line?For calendar-year public companies, ASU 2024-03 is effective for the 2027 annual report (10-K filed in early 2028), with interim adoption required in the first quarter of 2028. Early adoption is permitted.

Can private companies use a 409A valuation to satisfy ASC 718 fair value requirements?Under the ASU 2021-07 practical expedient, private companies may use a reasonable valuation method (including the IRS Section 409A safe harbor) to determine the current share price for option awards. The election and method must be disclosed. This expedient is not available after a company goes public.

How should ESG-linked vesting conditions be classified and disclosed?Classify as a performance condition if the metric is within the company's operational control, or as a market condition if tied to an external index or peer ranking. The disclosure must describe the vesting condition, the measurement methodology, and the probability assessment. SEC staff are actively reviewing these disclosures.

What must be disclosed when awards are repriced or exchanged in a tender offer?Under ASC 718-10-50-2(k), a significant modification requires disclosure of the terms of the modification, the number of employees affected, and the total incremental compensation cost. A tender offer or repricing is a modification. The grant-date fair value in the rollforward table does not change; only the incremental cost is separately disclosed.