ASC 818 vs. IFRS: Accounting for Carbon Credits Under ASU 2026-02

Accounting for carbon credits just got a lot clearer, at least if you report under US GAAP. On May 19, 2026, the FASB issued ASU 2026-02, creating a brand-new Codification Topic, ASC 818, Environmental Credits and Environmental Credit Obligations. For the first time, US preparers have authoritative guidance on how to recognize, measure, present, and disclose environmental credits and the obligations tied to them. IFRS preparers are still navigating a patchwork of IAS 38, IAS 2, IAS 20, and IFRS 9 with no specific standard in sight.

This guide is for CFOs, technical accounting teams, and ESG leads at mid-to-large enterprises who need to set or update accounting policy, avoid restatement risk, and align their financial statements with sustainability disclosures under ISSB and CSRD.

Key takeaway: The compliance-vs-voluntary distinction is the central fault line in ASC 818. Get it wrong and you'll misclassify assets, mistime liabilities, and potentially misstate your sustainability disclosures.

What Are Carbon Credits, Offsets, and Allowances, and Does the Label Matter?

The terminology is inconsistent across frameworks, and that inconsistency is itself a source of accounting confusion. Each carbon credit or carbon offset represents the reduction or removal of one metric tonne of CO2 equivalent (1 tCO2e). But the label matters for accounting purposes.

- Carbon credits / emissions allowances are primarily used in regulated compliance markets, for example, the EU Emissions Trading System (EU ETS), which covers just over a third of the EU's total greenhouse gas emissions and is the world's largest cap-and-trade scheme. In the US, cap-and-trade operates at the state level (e.g., California's program).

- Carbon offsets typically refer to voluntary market instruments, reductions or removals outside regulated systems, used to meet self-imposed net-zero targets.

- RECs (Renewable Energy Certificates) are a distinct category and may fall within ASC 818's scope depending on their characteristics.

KPMG notes that even the ISSB shifted from "carbon offset" to "carbon credit" during redeliberations, acknowledging that "offset" better describes the application of a credit to an entity's net emissions. ASC 818 uses the term "environmental credit" as its umbrella, which covers carbon credits, renewable energy credits, and similar instruments.

Under ASC 818, an environmental credit must meet four criteria: (1) it lacks physical substance and is not a financial asset; (2) it is represented to prevent, control, reduce, or remove emissions or other pollution; (3) it is, or previously was, separately transferable in an exchange transaction (an active market is not required); and (4) it is not an income tax credit.

What Changed with ASU 2026-02 and ASC 818?

Before ASU 2026-02, US GAAP had no authoritative standard specifically addressing carbon credits. Companies applied a patchwork of intangible asset guidance, inventory rules, government grant accounting, and derivative frameworks, with no consensus. The FASB had tried twice before: EITF 03-14 was withdrawn in 2003, and a 2004 proposed FSP was never finalized. ASU 2026-02 is the first time the FASB has successfully completed a standard on this topic.

The new standard also amends several adjacent areas of the Codification:

- ASC 815-10 (Derivatives and Hedging): Environmental credit assets and ECOs within ASC 818's scope are explicitly outside ASC 815's scope. However, and this is a trap many ESG teams miss, a freestanding forward contract to obtain or sell an environmental credit in the future may still be subject to derivative accounting under ASC 815's general requirements. The credit itself is scoped into 818; the forward contract to buy it may not be.

- ASC 832 (Government Assistance): Environmental credit assets within ASC 818's scope are not within ASC 832's scope. This resolves prior ambiguity about government-granted credits (e.g., free allowances in a cap-and-trade program).

- ASC 958-605 (Not-for-Profit Revenue Recognition): Same carve-out for NFPs receiving environmental credits.

- ASC 410-30 (Environmental Remediation Liabilities): Environmental remediation obligations within ASC 410-30's scope are explicitly excluded from ASC 818. This scoping boundary matters: a liability to clean up contaminated land is not an ECO.

For a full technical walkthrough of the standard's scope and definitions, see Finrep's dedicated guide: ASU 2026-02 (Topic 818): Environmental Credits Accounting Guide for 2026.

The ASC 818 Recognition Framework: Intended Use Drives Everything

Under ASC 818, whether you recognize an environmental credit as an asset, and how you subsequently measure it, depends on what you intend to do with it. This intended-use framework is the organizing principle of the entire standard.

An environmental credit is recognized as an asset when it is probable the entity will:

- Use it to settle an environmental credit obligation (ECO),

- Transfer it in an exchange transaction (i.e., sell it), or

- Use it in a nonreciprocal transfer (e.g., retire it for a voluntary sustainability commitment).

If none of those conditions is probable, the credit is not recognized as an asset. This matters most for credits acquired speculatively or held in uncertain circumstances.

Compliance vs. Noncompliance vs. Voluntary: The Three Buckets

ASC 818 separates environmental credits into three categories, each with different subsequent measurement:

Credit TypeDefinitionSubsequent MeasurementCompliance environmental creditHeld to settle a legal/regulatory ECOFollows the ECO measurement model (see below)Noncompliance environmental creditHeld to sell or transfer in an exchangeCost less impairment (or fair value if elected)Voluntary environmental creditHeld to retire for a self-imposed sustainability commitmentCost; tested for impairment each reporting period

PwC summarizes: "Under the new standard, an entity will recognize and measure environmental credit assets based on their intended use (e.g., compliance environmental credits, noncompliance environmental credits, voluntary credits) as well as how the credits are obtained (e.g., acquired, internally generated)."

What Is an Environmental Credit Obligation (ECO)?

An ECO is a regulatory compliance obligation, arising from laws, statutes, or ordinances, that may be settled with environmental credits. A voluntary net-zero pledge does not constitute an ECO. This distinction is critical: a company that has committed to be carbon neutral by 2030 has not recognized an ECO; a company operating under California's cap-and-trade program has.

ECO measurement depends on whether the obligation is funded or unfunded:

- Funded portion: Measured using the cost of the compliance environmental credits the entity holds and expects to use to settle the obligation.

- Unfunded portion: Measured at the fair value of the additional credits needed to settle the remaining obligation.

Once credits are remitted to the regulator, the ECO is derecognized.

The Voluntary Credit Debate: Expense vs. Asset

This was the most contested issue in the ASU 2026-02 comment letter process, and it directly affects companies making net-zero pledges.

The FASB's December 2024 Exposure Draft proposed that companies purchasing environmental credits for voluntary sustainability commitments must immediately expense the cost as incurred. Industry pushed back hard. Anew Climate LLC, one of the largest carbon credit market-makers in North America, argued:

"We believe that it would be more appropriate to allow companies to record credits purchased for future voluntary sustainability commitments as intangible assets that are subject to amortization in proportion to their use to address such commitments."

Anew Climate's core argument was about comparability: "Two reporting entities that have made similar sustainability commitments would face different future cash flow risks, if one entity has already made meaningful purchases of such credits while the other has not. This difference in cash flow risk would not be apparent to financial statement users, if credits purchased for voluntary commitments were expensed immediately."

They also flagged a practical issue: non-refundable deposits for future carbon credit purchases should be recorded as deposits and reclassified to intangible assets when credits are received, not immediately expensed. Transaction costs, brokerage, transfer, and registry fees, should be included in the cost basis.

The final ASU 2026-02 establishes that voluntary environmental credit assets are recognized at cost and tested for impairment each reporting period, rather than immediately expensed. This represents a meaningful departure from the ED's proposed treatment and a partial win for industry commenters. The impairment testing requirement (versus no impairment for compliance credits) reflects the higher uncertainty around voluntary credit use.

How IFRS Treats Carbon Credits: Still a Patchwork

Under IFRS, there is no specific accounting standard for carbon credits as of mid-2026. The IASB has no active project on this topic. As KPMG states: "Although several standard-setting projects have been attempted, there are currently no accounting requirements under IFRS Accounting Standards (or US GAAP) specific to carbon offsets or credits. IASB attempts over the years were either not finalized or withdrawn."

IFRS preparers must apply existing standards by analogy, and the applicable standard depends on the entity's role and the specific arrangement:

ScenarioPotentially Applicable IFRS StandardCredit held for own use (end-user)IAS 38 (Intangible Assets), residual treatmentCredit held for trading/saleIAS 2 (Inventories)Credit received from government at no/below-market costIAS 20 (Government Grants)Compliance-market credit economically similar to a financial instrumentIFRS 9 (Financial Instruments)Forward contract to purchase creditsIFRS 9 (derivative)

PwC notes that IAS 38 applies to carbon offsets only when they do not fall within the scope of another standard, it is a residual treatment, not a default. The specific facts and circumstances of each arrangement determine which standard governs.

Deloitte identifies three distinct participant roles that drive IFRS treatment:

- Project developer (generates credits from emission reduction projects)

- Intermediary (facilitates transfer between developer and end-user)

- End-user (retires credits against its own emissions)

The accounting treatment differs materially depending on which role the entity occupies. A developer generating credits for sale will likely apply IAS 2 (inventory); an end-user holding credits for retirement will likely apply IAS 38.

The Real-World Diversity Problem

Research presented at the IFRS Research Forum in November 2023 analyzed four cases in Brazilian voluntary and regulated carbon markets and found no consensus. In Brazil's regulated CBIO market (decarbonization credits under RenovaBio), one buyer company audited by KPMG classified CBIOs as non-current intangible assets with indefinite useful life at historical cost. A seller company in the same market, audited by PwC, classified them as current asset inventories at net receivable value. Same market, same instrument, opposite accounting treatments.

The researchers concluded: "There is a consensus that carbon credits are assets, but the accounting classification of these assets is not consensual. The favorite accounting treatment is as intangible assets. However, practitioners have adopted different accounting treatments, such as inventories or financial instruments. It leads us to think carbon credits do not fit perfectly into intangible assets."

A key threshold question under IFRS is whether a carbon credit even meets the definition of a separate asset at all. KPMG highlights that for immediately retired credits, the economic benefits may have already been consumed, meaning no separate asset exists to recognize.

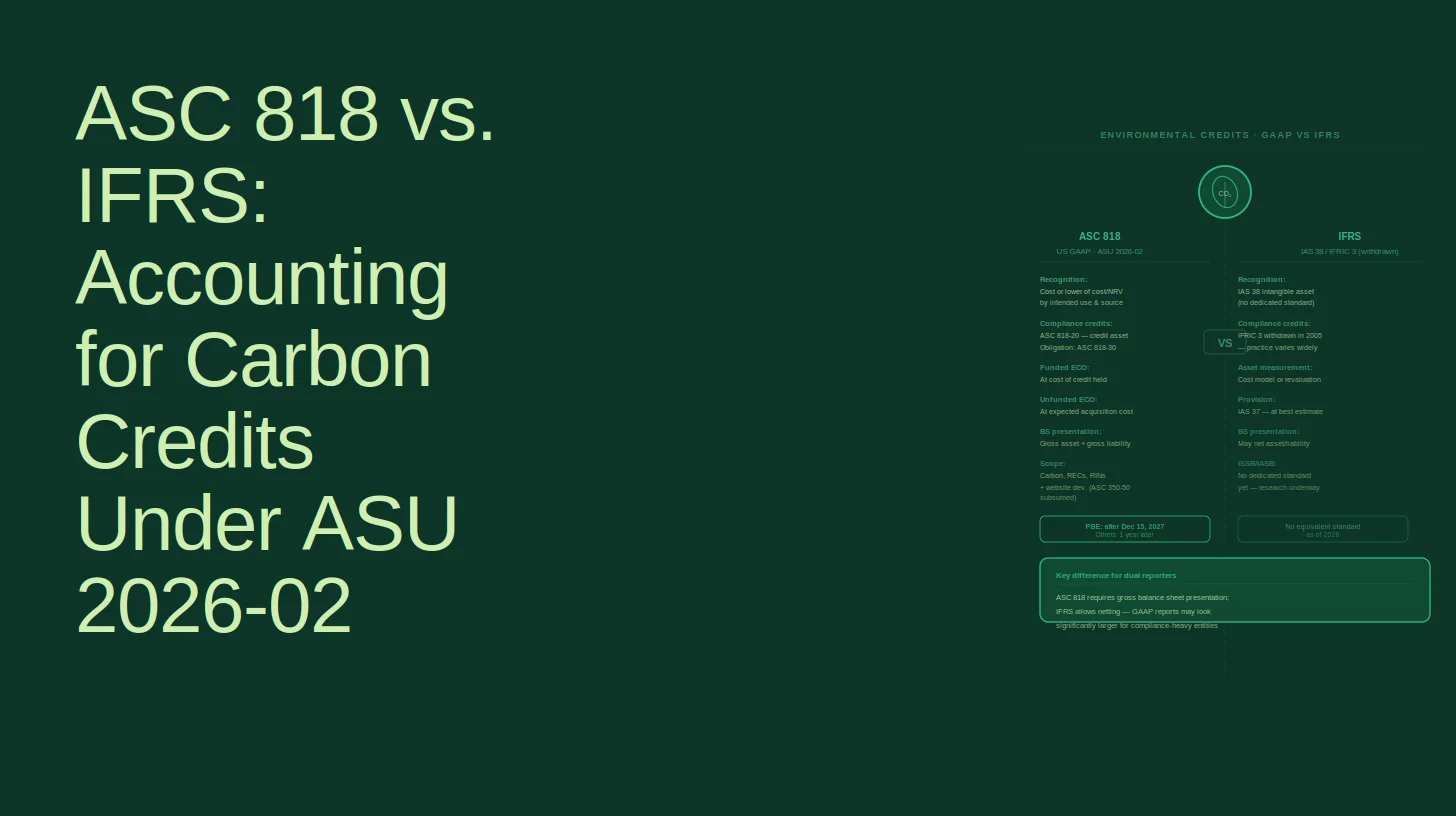

US GAAP vs. IFRS: Side-by-Side Comparison

IssueUS GAAP (ASC 818)IFRS (No Specific Standard)Authoritative guidanceYes, ASU 2026-02, effective Dec 15, 2027 (PBEs)No, apply IAS 38, IAS 2, IAS 20, or IFRS 9 by analogyOrganizing principleIntended use (compliance / noncompliance / voluntary)Facts and circumstances; role of entityCompliance creditsSpecific ECO model; funded/unfunded measurementLikely IAS 38 or IFRS 9; diversity in practiceVoluntary creditsRecognized at cost; impairment tested each periodLikely IAS 38 (residual); no impairment model specifiedGovernment-granted creditsScoped out of ASC 832; governed by ASC 818IAS 20 may apply; judgment requiredForward purchase contractsMay be derivatives under ASC 815 (separate analysis)IFRS 9 derivative analysis requiredBusiness combinationsSpecific guidance in ASC 818ASC 805 analog (IFRS 3); judgment on PPA allocationDisclosureSpecific ASC 818 requirements (see below)IAS 38 / IAS 1 general disclosure principlesConvergence outlookStandard issued; stableIASB horizon-scanning only; no active project

The Forward Contract Trap Under ASC 815

This is a nuance that ESG teams and treasury functions frequently miss. ASU 2026-02 explicitly scopes environmental credit assets and ECOs out of ASC 815-10 (Derivatives and Hedging). But that carve-out applies to the credit itself once held, not to the contract used to acquire it.

A freestanding forward contract to purchase carbon credits in the future may still be a derivative under ASC 815. If the contract has a notional amount, an underlying (the credit price), requires or permits net settlement, and has no initial net investment, it meets the derivative definition. Companies entering into multi-year forward purchase agreements for voluntary credits, a common structure in the voluntary carbon market, need to run the ASC 815 analysis before assuming the contract is simply a purchase commitment.

Disclosure Requirements Under ASC 818

ASC 818 introduces specific disclosure requirements that go well beyond what most companies currently provide. For environmental credit assets, preparers must disclose:

- A breakdown of significant holdings by type

- Cash paid for credits during the reporting period

- Revenues, gains, or losses from selling credits

- Impairment losses recognized on voluntary credits

- Qualitative information on how credits are obtained, used, and accounted for

For ECOs, disclosures must include:

- The funded vs. unfunded portions of the obligation

- Information on the regulatory programs that created the obligation

- The activities that triggered the obligation

Presentation on the face of the financial statements requires environmental credit assets to be shown separately, they cannot be netted against ECO liabilities.

For IFRS preparers, disclosure follows the general principles of IAS 38 (for intangibles) or IAS 1, there are no carbon-credit-specific disclosure requirements, but accounting policy disclosures and qualitative descriptions of arrangements are expected.

Effective Date, Transition, and the Early Adoption Question

ASU 2026-02 is effective for public business entities in annual periods beginning after December 15, 2027, including interim periods within those annual periods. All other entities get one additional year: annual periods beginning after December 15, 2028. Early adoption is permitted as of the beginning of any annual reporting period.

Transition uses a retrospective cumulative-effect adjustment to beginning retained earnings (or net assets for NFPs) at the date of initial application. Entities must recognize and measure all credits and obligations on the balance sheet at that date.

The early adoption question is real. Companies that have been expensing voluntary credits immediately, or carrying them as intangibles under pre-818 practice, will need to assess the transition impact. If your current policy is materially different from ASC 818's model, early adoption in fiscal year 2027 (for a calendar-year PBE) gives you a full year to embed the new policy before mandatory adoption.

For a detailed breakdown of who ASC 818 applies to and the full scope analysis, see What Is FASB Topic 818 and Who Does It Apply To?.

What the IASB Is Watching

The IASB's June 2024 horizon-scanning staff paper flagged carbon credits as a potential future agenda item, noting that "carbon credits in the compliance market could be included in the scope of IFRS 9 Financial Instruments as they are economically similar to financial instruments." The IASB's Accounting Standards Advisory Forum received a research paper from the Canadian standard-setter (ACSB) in July 2024 raising unresolved questions: should credits be recognized as an asset or expense? What happens if claimed emissions reductions are not actually achieved? How do you account for credits that are immediately retired?

None of these questions has a definitive IFRS answer yet. The IASB is watching, not acting. IFRS preparers should document their accounting policy choices carefully, disclose them clearly, and monitor IASB developments, because when a standard does emerge, it may require retrospective adjustment.

Carbon Credit Accounting and ISSB/CSRD Disclosure Alignment

EY's March 2025 report puts it plainly: "CFOs must develop an understanding about how carbon credits are valued and accounted for as businesses scale their investments in carbon credits to meet [net-zero commitments]."

The reason is consistency. ISSB IFRS S2 and CSRD/ESRS both require quantitative disclosure of carbon credit use, volumes purchased, retired, and held. If the numbers in your sustainability report don't reconcile with the assets and expenses in your financial statements, auditors and investors will ask why. The financial accounting treatment under ASC 818 (or your IFRS policy) directly affects what appears in footnotes, and those footnotes will be read alongside your TCFD-aligned or ESRS-compliant climate disclosures.

The practical implication: build your carbon credit accounting policy and your sustainability disclosure policy together, not in separate silos. A voluntary credit recognized as an asset under ASC 818 should appear consistently in both your balance sheet footnotes and your ISSB S2 disclosure of carbon credit holdings.

FAQ

Are carbon credits an asset or an expense under US GAAP?Under ASC 818, carbon credits are recognized as assets when it is probable they will be used to settle an ECO, sold, or retired for a voluntary commitment. Voluntary credits are carried at cost and tested for impairment. They are not immediately expensed, a key change from some pre-ASC 818 practice.

What is an Environmental Credit Obligation (ECO)?An ECO is a legally enforceable compliance obligation arising from laws, statutes, or ordinances that may be settled with environmental credits. A voluntary net-zero pledge does not qualify as an ECO under ASC 818. The ECO liability is recognized when the underlying emissions occur.

Does ASC 818 apply to forward contracts to purchase carbon credits?Not directly. The credits themselves, once held, are within ASC 818's scope. But a freestanding forward contract to purchase credits in the future requires a separate derivative analysis under ASC 815 and may qualify as a derivative.

Which IFRS standard applies to carbon credits?There is no single answer. IAS 38 applies as a residual treatment for end-users holding credits for retirement. IAS 2 may apply for trading inventories. IAS 20 may apply for government-granted credits. IFRS 9 may apply for compliance-market credits or forward contracts. The entity's role and the specific arrangement determine which standard governs.

When is ASU 2026-02 effective, and should we early adopt?Public business entities must adopt for annual periods beginning after December 15, 2027. All other entities have until after December 15, 2028. Early adoption is permitted. Companies whose current policy differs materially from ASC 818 should model the transition impact now and consider early adoption to avoid a disruptive adjustment at mandatory adoption.

How do carbon credit accounting policies interact with ISSB S2 and CSRD disclosures?The volumes and values disclosed in sustainability reports under ISSB IFRS S2 or CSRD/ESRS must be consistent with what appears in financial statement footnotes. Build both policies together to avoid inconsistencies that auditors or investors will flag.